Applying volatility benchmarks correctly is the key to effective portfolio management. This article explains how volatility and VaR (Value at Risk) is utilized in a market neutral, long-short, volatility-based strategy to yield the most predictable and stable alpha.

To apply volatility correctly, investors must identify a relatively stable stock first, which is the key task before opening long-short positions. There are several various metrics and methods used for determining a relatively stable stock. We use an estimate based on 99% VAR (Value at Risk).

According to Investopedia's definition, Value at Risk (VaR) is a statistical measure that quantifies the extent of possible financial losses within a firm, portfolio, or position over a specific time frame. This metric is most used to determine the extent and probabilities of potential losses in their institutional portfolios. Risk managers use VaR to measure and control the level of risk exposure.

VaR is calculated as = [Expected Weighted Return of the Portfolio − (z-score of the confidence interval × standard deviation of the portfolio) × portfolio value

The most important metrics in calculating VaR estimate for every particular security are the calculated VAR values or quantiles of the threshold range of 95% or 99% VAR.

The smaller the dispersion of the security’s closing price within VaR limits and the lower the quantity and VaR tail values, then the more stable is the stock.

We can use this security in the future for calculating volatility and threshold deviations from volatility based on normal, or in some more complex cases, abnormal distribution models.

Not only quantity and quality of VaR values and range limits are important factors but we also need to tie them in with the confidence level of the VaR estimate and recalculate it for every additional period, shifting each trading day to the right. If we calculate that the confidence level of the VAR estimate is within the stable volatility range, we can use this security in further transactions within the range limits of critical volatility range limits, namely: within two to four sigma values depending on the volatility type that can be directed, non-directed, extended, narrowed or normal.

Tying VaR with long-short stock

Let us first define what is a Long-Short approach? The Long-Short approach usually means that an investor would sell the overvalued stock position and would the undervalued one. Now we will examine how VaR can help us identify overvalued and undervalued stocks.

The stability of VaR points to the stock’s propensity to return to its mean value. The actual value of VaR and VaR tail quantiles that we gathered from the analysis of the VaR critical range in our former post, purportedly indicates the frequency and magnitude of VaR tail quantiles breaking through the VAR’s limits.

The Long-Short Approach based on VAR must include two important prerequisites:

- Both securities must have a stable VAR at the same time. As we covered in our previous post on volatility, the stability is expressed in confidence level to VAR estimate that shows the correspondence of the forecast VAR ranges to its real values over time.

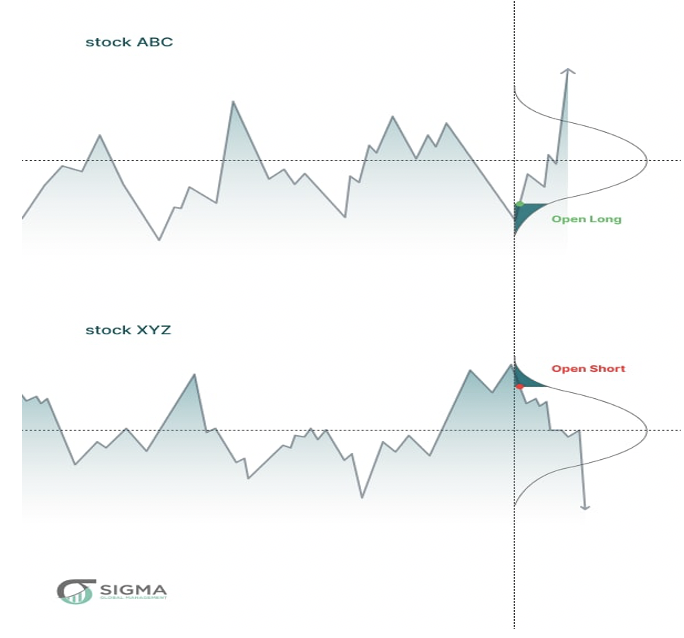

- Both securities must simultaneously diverge in the opposite direction seeking to return to their mean value. One of the securities is positioned in the upper boundary of the VAR tag quantile, and the other is positioned in the lower boundary of the VAR tag quantile, as depicted in the drawing below.

Chart 1. VaR and Long-Short Approach

Consequently, to select a long-short stock pair, we need to find two equities seeking to return to their mean value; sell the stock that has been gaining considerable value over a long period; buy the stock that has been losing significant value for too long.

These are the fundamentals of forming long-short positions for two stocks based on VAR. However, other important parameters must be included in the analysis, namely: risk associated with particular positions, how much money should be invested in each position, the duration of keeping the positions, and things that involve metrics other than VAR. In addition, paired stocks must have some core features in common: industry sector, market capitalization, reported metrics, or corporate events.

Stay tuned with Sigma Global Management, and we will give you an overview of these points in our next post on asset management.

© Sigma Global Management

Read more commentaries by Sigma Global Management