Bull Market Rhymes

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhile I employ a great many adages and quotes in my writings, my main go-to list consists of a relatively small number. One of my favorites is widely attributed to Mark Twain: “History doesn’t repeat itself, but it does rhyme.” It’s well documented that Twain used the first four words in 1874, but there’s no clear evidence that he ever said the rest. Many others have said something similar over the years, and in 1965 psychoanalyst Theodor Reik said essentially the same thing in an essay titled “The Unreachables.” It took him a few more words, but I think his formulation is the best:

There are recurring cycles, ups and downs, but the course of events is essentially the same, with small variations. It has been said that history repeats itself. This is perhaps not quite correct; it merely rhymes.

The events of investment history don’t repeat, but familiar themes do recur, especially behavioral themes. It’s these that I study.

In the last two years, we’ve seen dramatic examples of the ups and downs Reik wrote about. And I’ve been struck by the reappearance of some classic themes in investor behavior. They’ll be the topic of this memo.

I want to mention up front that this memo has nothing to do with assessing the markets’ likely direction from here. Bullish behavior came out of the pandemic-related bottom of March 2020; since then, significant problems have developed inside the economy (inflation) and outside (Ukraine); and there’s been a significant correction. No one, including me, knows what the sum of those things implies for the future.

I’m writing only to place recent events in the context of history and point out a few implied lessons. This is important, because we have to go back 22 years – to before the bursting of the tech-media-telecom bubble in 2000 – to see what I consider a real bull market and the ending of the resultant bear market, and I imagine many of my readers entered the investment world too late to have experienced that event. You may ask, “What about the market gains that preceded the Global Financial Crisis of 2008-09 and the pandemic-related collapse of 2020?” In my view, in both cases, the preceding appreciation was gradual, not parabolic; it wasn’t driven by overheated psychology; and it didn’t take stock prices to crazy heights. Moreover, high stock prices weren’t the cause of either crisis. The excesses in the former lay in the housing market and the creation of securities backed by sub-prime mortgages, and the latter collapse was a consequence of the arrival of Covid-19 and the government’s decision to shut down the economy to limit the spread of the disease.

When I refer above to “a real bull market,” I’m not talking about standard definitions such as these from Investopedia:

- A period of time in financial markets when the price of an asset or security rises continuously

- A situation in which stock prices rise by 20%, usually after a drop of 20%

The first of these is too bland, failing to capture a bull market’s emotional essence, and the second attempts false precision. A bull market shouldn’t be defined as a percentage price movement. For me, it’s best described by what it feels like, the psychology behind it, and the behavior that psychology leads to.

(I started investing before the development of numerical criteria for bull and bear markets, and I consider such yardsticks meaningless. Take a look, for example, at a couple of recent newspaper articles. On May 20, the S&P 500 Index’s decline from the top passed the “magic” 20% threshold; thus on May 21 the Financial Times wrote, “Wall Street stocks slumped into a bear market yesterday . . .” But because a late rally reduced the final decline to just under 20%, the headline of the same day’s New York Times read, “S&P 500 Drops . . . but Evades Bear Market.” Does it really matter whether the S&P 500 is down 19.9% or 20.1%? I prefer the old-school definition of a bear market: nerve-racking.)

Excesses and Corrections

My second book is Mastering the Market Cycle: Getting the Odds on Your Side. It’s well known that I’m a student of cycles and a believer in cycles. I’ve lived through (and been schooled by) several significant cycles during my years as an investor. I believe understanding where we stand in the market cycle can give us a hint regarding what’s coming next. And yet, when I was about two-thirds of the way through writing that book, a question dawned on me that I hadn’t considered before: Why do we have cycles?

For example, if the S&P 500 has returned just over 10% a year on average over the 65 years since it assumed its present form in 1957, why doesn’t it just return 10% every year? And updating a question I asked in my memo The Happy Medium (July 2004), why has its annual return been between 8% and 12% just six times during this period? Why is it so far from the mean 90% of the time?

After pondering this question for a while, I landed on what I consider the explanation: excesses and corrections. If the stock market was a machine, it might be reasonable to expect it to perform consistently over time. Instead, I think the substantial influence of psychology on investors’ decision-making largely explains the market’s gyrations.

When investors turn highly bullish, they tend to conclude that (a) everything’s going to go up forever and (b) regardless of what they pay for an asset, someone else will come along to buy it from them for more (the “greater-fool theory”). Because of the high level of optimism:

- Stock prices rise faster than company profits, soaring well above fair value (excess to the upside).

- Eventually, conditions in the investment environment disappoint, and/or the folly of the elevated prices becomes clear, and they fall back toward fair value (correction) and then through it.

- The price declines generate further pessimism, and this process eventually causes prices to far understate the value of stocks (excess to the downside).

- Resultant buying on the part of bargain-hunters causes the depressed prices to recover toward fair value (correction).

The excess to the upside makes for a period of above average returns, and the swing toward excess on the downside makes for a period of below average returns. There can be many other factors at work, of course, but in my view, “excesses and corrections” covers most of the ground. We saw a number of excesses to the upside in 2020-21, and now we’re seeing corrections thereof.

Bull Market Psychology

In a bull market, favorable developments lead to price rises and lift investor psychology. Positive psychology induces aggressive behavior. Aggressive behavior leads to higher prices. Rising prices encourage rosier psychology and further risk-taking. This upward spiral is the essence of a bull market. When it’s underway, it feels unstoppable.

We saw a classic collapse of asset prices in the early days of the pandemic. For example, the S&P 500 reached a then-all-time high of 3,386 on February 19, 2020 before falling by one-third in just 34 days to a low of 2,237 on March 23. After that, a number of forces combined to produce massive price gains:

- The Federal Reserve cut the fed funds rate to roughly zero, and the Fed was joined by the Treasury in announcing massive stimulative measures.

- These actions convinced investors that these institutions would do whatever it took to stabilize the economy.

- The interest rate cut significantly reduced the prospective returns required to make investments look attractive in relative terms.

- The combination of these factors forced investors to bear risks they had been running from just a short time earlier.

- Asset prices rose: by late August, the S&P 500 had retraced its decline and surpassed its February high.

- The FAAMGs (Facebook, Amazon, Apple, Microsoft and Google), software stocks, and other tech stocks rose dramatically, pushing the market higher.

- Eventually, investors concluded – as they often do when things are going well – that they could expect more of the same.

The most important thing about bull market psychology is that, as cited in the final bullet point above, most people take rising stock prices as a positive sign of things to come. Many are converted to optimism. Relatively few suspect that the gains to date might have been excessive and borrowed from future returns and that they presage reversal, not continuation.

That reminds me of another of my favorite adages – one of the first ones I learned, roughly 50 years ago – “the three stages of a bull market”:

- the first, when a few forward-looking people begin to believe things will get better,

- the second, when most investors realize improvement is actually underway, and

- the third, when everyone concludes that things will get better forever.

It’s interesting to note that even though the market moved from despondent in March 2020 to booming in May, largely thanks to the Fed, the most frequent attitude I encountered during that period was dubiousness. And the question I was asked most frequently was “If the environment is so bad – with the pandemic raging and the economy shuttered – isn’t it wrong for the market to rise?” It was hard to find any optimists. Many of the buyers were what my late father-in-law used to call “handcuff volunteers”: they didn’t buy because they wanted to; they bought because they had to, since the return on cash was so low. And once markets started to rise, people were afraid of being left behind, so they chased prices higher. Thus, the market gains seemed to be the result of the Fed’s manipulation of the capital markets, rather than positive corporate developments or optimistic psychology. It was only around the end of 2020 – when the S&P 500 was up by 16.3% for the year and 67.9% from the March bottom – that investor psychology caught up with the booming stock prices.

The bull market of 2020 was unprecedented in my experience, in that there was essentially no first stage and very little of the second. Many investors went straight from hopeless in late March to highly optimistic later in the year. This is a great reminder that, while some themes do recur, it’s a big mistake to expect history to repeat exactly.

Optimistic Rationales, Super Stocks, and the New, New Thing

Raging bull markets are examples of mass hysteria. At the extreme, thinking and thus behavior become unmoored from reality. In order for this to occur, however, there has to be some factor that activates investors’ imagination and discourages prudence. Thus, special attention should be paid to an element that almost always characterizes bull markets: a new development, invention or justification for the rising stock prices.

Bull markets are, by definition, characterized by exuberance, confidence, credulousness, and a willingness to pay high prices for assets – all at levels that are shown in retrospect to have been excessive. History has generally shown the importance of keeping these things in moderation. For that reason, the intellectual or emotional rationale for a bull market is often based on something new that history can’t be used to discount.

Those last six words are very important. History amply demonstrates that when (a) markets exhibit bullish behavior, (b) valuations become excessive, and (c ) the latest thing is accepted without hesitation, the consequences are often very painful. Everyone knows – or should know – that parabolic stock market advances are generally followed by declines of 20-50%. Yet those advances occur and recur, abetted by what I learned in high school English class to call “the willing suspension of disbelief.” Here’s another of my very favorite quotes:

Contributing to . . . euphoria are two further factors little noted in our time or in past times. The first is the extreme brevity of the financial memory. In consequence, financial disaster is quickly forgotten. In further consequence, when the same or closely similar circumstances occur again, sometimes in only a few years, they are hailed by a new, often youthful, and always supremely self-confident generation as a brilliantly innovative discovery in the financial and larger economic world. There can be few fields of human endeavor in which history counts for so little as in the world of finance. Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present. (John Kenneth Galbraith, A Short History of Financial Euphoria, 1990 – emphasis added)

I’ve shared that quote with readers many times over the last 30 years – since I think it so beautifully sums up a number of important points – but I haven’t previously shared my explanation for the behavior it describes. I don’t think investors are actually forgetful. Rather, knowledge of history and the appropriateness of prudence sit on one side of the balance, and the dream of getting rich sits on the other. The latter always wins. Memory, prudence, realism, and risk aversion would only get in the way of that dream. For this reason, reasonable concerns are regularly dismissed when bull markets get going.

What appears in their place is often intellectual justifications for valuations that exceed historical norms. On October 11, 1987, Anise Wallace described this phenomenon in an article in The New York Times titled “Why This Market Cycle Isn’t Different.” Optimistic thinking was being embraced at the time to justify unusually high stock prices, but Wallace said it wouldn’t hold:

The four most dangerous words in investing are “this time it’s different,” according to John Templeton, the 74-year-old mutual fund manager. At stock market tops and bottoms, investors invariably use this rationale to justify their emotion-driven decisions.

Over the next year, many investors are likely to repeat those four words as they defend higher stock prices. But they should treat them with the same consideration they give “the check’s in the mail.” No matter what brokers or money managers say, bull markets do not last forever.

It didn’t take a year. Just eight days later, the world experienced “Black Monday,” when the Dow Jones Industrial Average dropped by 22.6% in a single day.

Another justification for bull markets is often found in the belief that certain businesses are guaranteed to enjoy a terrific future. This applies to the Nifty-Fifty growth companies in the late 1960s; disc drive manufacturers in the ’80s; and telecom, Internet and e-commerce companies in the late ’90s. Each of these developments was believed to be capable of changing the world, such that the past realities of business need not constrain investors’ imaginations and willingness to pay up. And they did change the world. Nevertheless, the highly elevated asset valuations they were thought to justify didn’t hold.

In many bull markets, one or more groups are anointed as what I call “super stocks.” Their rapid rise makes investors increasingly optimistic. In the circular process that often characterizes the markets, this rising optimism takes the stocks to still-higher prices. And some of this positivity and appreciation reflects favorably on other groups of securities – or all securities – through relative-value comparisons and/or because of the general improvement in investors’ mood.

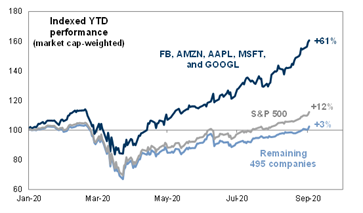

Topping the list of companies that fed investors’ excitement in 2020-21 were the FAAMGs, whose level of market dominance and ability to scale had never been seen before. The dramatic performance of the FAAMGs in 2020 attracted the attention of investors and supported a widespread swing toward bullishness. By September 2020 (that is, within six months), these stocks had nearly doubled from their March lows and were up 61% from the beginning of the year. Notably, these five stocks are heavily weighted in the S&P 500, so their performance resulted in a good overall gain for the index, but this distracted attention from the far-less-impressive performance of the other 495 stocks. The performance of the super stocks inflamed investors’ ardor, enabling them to disregard worries regarding the persistence of the pandemic or other risks.

Source: Goldman Sachs

The raging success of the FAAMGs created a luster that reflected positively on tech stocks in general. Demand soared for stocks in the sector and, as is usual in the investment world, strong demand encouraged and enabled supply. One notable barometer in this case is the attitude toward IPOs from unprofitable companies. Prior to the tech bubble of the late 1990s, IPOs from companies that didn’t make money were relatively rare. They became the norm during the bubble, but their number sunk again thereafter. In the 2020-21 bull market, IPOs from unprofitable companies experienced a big resurgence, as investors easily made allowance for tech companies’ desire to scale and biotech companies’ need to spend on drug trials.

If companies with bright futures provide fuel for bull markets, things that are new to the markets can supercharge market excesses. SPACs are a great recent example. Investors gave these newly formed vehicles blank checks for acquisitions on the proviso that investors could get their money back with interest (a) if no acquisition was consummated within two years or (b) if investors didn’t like the acquisition that was proposed. This seemed like a “no-lose proposition” (three of the most dangerous words in the world), and the number of SPACs organized soared from just 10 in 2013 and 59 in 2019 to 248 in 2020 and 613 in 2021. Some produced big profits, and in other cases investors took back their money with interest. But the lack of skepticism surrounding this relatively untested innovation – fueled by bull market psychology – allowed too many SPACs to be created, by competent and incompetent organizers alike who would be highly paid for pulling off an acquisition . . . any acquisition.

Today, the average SPAC that de-SPAC-ed since 2020 by completing an acquisition (in each case, with the approval of its investors) is selling at $5.25, versus its issue price of $10.00. This is a good example of a new thing that turned out to be less dependable than investors – who fell once again for a can’t-lose silver bullet – had thought. SPACs’ defenders argue that these vehicles are just an alternative way to take companies public, but their potential usefulness isn’t my concern. I’m focused on how readily investors embraced an untested innovation in hot times.

Another dynamic involving novel factors deserves mention, since it exemplifies the way “the new thing” can contribute to bull markets:

- Robinhood Markets began offering commission-free trading in stocks, ETFs and cryptocurrencies in the years before the pandemic. Once the Covid-19 crisis hit, this encouraged people to “play the stock market,” as casinos and sports events were closed for betting.

- Generous stimulus checks were sent to millions who hadn’t lost their jobs, meaning many people saw their disposable income rise during the pandemic.

- Bulletin boards like Reddit turned investing into a social activity for people shut in at home.

- As a result, large numbers of novice retail investors were recruited online, many of whom lacked the experience needed to know what constitutes investment merit.

- Newcomers were stirred by a popular cult figure who said, “stocks only go up.”

- As a result, many tech and “meme stocks” soared.

The final element worth discussing is cryptocurrency. Proponents of Bitcoin, for example, cite its variety of uses, as well as the limited supply relative to the potential demand. Skeptics, on the other hand, point to Bitcoin’s lack of cash flow and intrinsic value and thus the impossibility of assigning a fair price. Regardless of which side will turn out to be right, Bitcoin satisfies some characteristics of a bull market beneficiary:

- It’s relatively new (although it has been around for 14 years, it’s been in most people’s consciousness for only five).

- It enjoyed a dramatic price spike, rising from $5,000 in 2020 to a high of $68,000 in 2021.

- And it’s certainly something that, per Galbraith, prior generations “do not have the insight to appreciate.”

- In all these regards, it perfectly satisfies Galbraith’s description of something “hailed by a new, often youthful, and always supremely self-confident generation as a brilliantly innovative discovery in the financial . . . world.”

Bitcoin is off a little more than half from its 2021 high, but others among the thousands of cryptocurrencies that have been created have declined much more.

The striking performance of the FAAMGs, tech stocks generally, SPACs, meme stocks and cryptocurrencies in 2020 reinforced the craze for them and added to investors’ general optimism. It’s hard to imagine a full-throated bull market arising in the absence of something that’s never been seen or heard before. The “new, new thing” and belief that “this time it’s different” are shining examples of recurring bull market themes.

The Race to the Bottom

Another bull market theme that rhymes from cycle to cycle is the deleterious impact of bull market trends on the quality of investors’ decision-making. In short, when burning optimism takes over from levelheadedness:

- asset prices rise,

- greed grows relative to fear,

- fear of missing out replaces fear of losing money, and

- risk aversion and caution evaporate.

It’s essential to bear in mind that it’s risk aversion and the fear of loss that keep markets safe and sane. The developments listed above typically combine to lift markets, drive out cautious investigation and deliberation, and make the markets a dangerous place.

In my 2007 memo The Race to the Bottom, I explained that when there’s too much money in the hands of investors and providers of capital and they’re too eager to put it to work, they bid too aggressively for securities and the chance to lend. Their spirited bidding drives down prospective returns, drives up risk, weakens security structures, and reduces the margin for error.

- The cautious investor, sticking to her guns, says, “I insist on 8% interest and strong covenants.”

- Her competitor responds, “I’ll accept 7% interest and demand fewer covenants.”

- The least disciplined, not wanting to miss the opportunity, says, “I’ll settle for 6% interest and no covenants.”

This is the race to the bottom. This is why it’s often said that “the worst of loans are made in the best of times.” This is something that can’t happen when people are smarting from recent losses and afraid of experiencing more. It’s not a coincidence that the record-long 10-plus-year economic recovery and stock market rise that followed the Fed’s massive response to the Global Financial Crisis were accompanied by:

- a wave of IPOs from money-losing companies;

- record issuance of sub-investment grade securities, including risky CCC-rated debt;

- debt issuance from companies in volatile industries such as tech and software that lenders are likely to shun in more cautious times;

- rising valuation multiples on acquisitions and buyouts; and

- shrinking risk premiums.

Favorable developments also encourage the increased use of leverage. Leverage magnifies gains and losses, but in bull markets, investors feel sure of gains and disregard the possibility of loss. Under such conditions, few can see a reason not to incur debt – with its piddling interest cost – to increase the payoff from their successes. But putting more debt on investments made at high prices late in the up-cycle is no formula for success. When times turn bad, leverage turns disadvantageous. And when investment banks issue late-cycle debt that they can’t place with buyers, they’re stuck with it. Debt “hung” on banks’ balance sheets is often a “canary in the coal mine” with regard to what’s in store.

Since I’m relying on time-worn investment adages, it’s appropriate at this point to invoke the one I consider the greatest regarding investor behavior over cycles: “What the wise man does in the beginning, the fool does in the end.” People who buy in stage one of a bull market, when prices are low because of prevailing pessimism (such as during the Global Financial Crisis of 2008-09 and in the early days of the Covid-19 pandemic in 2020), have the potential to earn high prospective returns with little risk: the main prerequisites are money to spend and the nerve to spend it. But when bull markets heat up and good returns encourage investors’ optimism, the traits that are rewarded are eagerness, credulousness, and risk-taking. In stage three of a bull market, new entrants buy aggressively, keeping it aloft for a while. Caution, selectivity, and discipline go out the window just when they’re needed most.

Particularly noteworthy is the fact that investors who are in a good mood and being rewarded for risk tolerance typically cease to practice discernment regarding investment opportunities. Not only do investors consider it a certainty that some examples of “the new thing” will succeed, but eventually they conclude that everything in that sector will do well, so differentiating is unnecessary.

Because of all the above, the term “bull market psychology” isn’t a positive. It connotes carefree behavior and a high level of risk tolerance, and investors should find it worrisome, not encouraging. As Warren Buffett puts it, “The less prudence with which others conduct their affairs, the greater the prudence with which we should conduct our own affairs.” Investors have to know when bull market psychology is in ascendance and apply the required caution.

The Pendulum Swings

Bull markets don’t arise out of thin air. The winners in each bull market are winners for the simple reason that a grain of truth underlies their gains. However, the bullishness I’ve described above tends to exaggerate the merits and pushes security prices to levels that are excessive and thus vulnerable. And the upward swing doesn’t last forever.

In On the Couch (January 2016), I wrote, “in the real world, things generally fluctuate between ‘pretty good’ and ‘not so hot.’ But in the world of investing, perception often swings from ‘flawless’ to ‘hopeless.’” The way things are seriously overdone in the markets is one of the key characteristics of investor behavior. During bull markets, investors conclude that difficult, unlikely, and unprecedented things are sure to work. But in less ebullient times, favorable economic news and “earnings beats” fail to inspire buying, and rising prices no longer make life painful for people who are underinvested. Thus, we stop seeing the willing suspension of disbelief, and psychology flips to negativism.

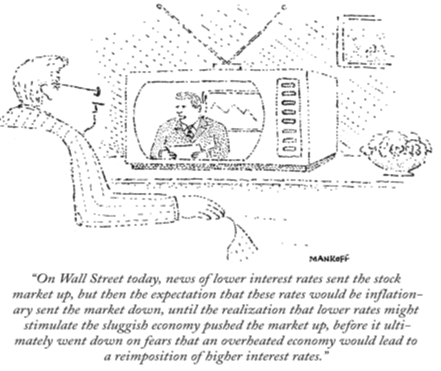

The key lies in the fact that investors are capable of interpreting virtually any piece of news either positively or negatively, depending on how it’s reported and on their mood. (The cartoon below, one of my all-time favorites, was published many decades ago – check out those rabbit ears and the depth of the TV set – but clearly the caption is relevant to this very moment.)

Reflecting the “flawless-to-hopeless” progression I mentioned earlier, prevailing narratives are subject to reversal. While the argument supporting the bull market may have been reasonably likely to hold, investors treated it as ironclad when all was going well. When some of the argument’s flaws come to light, however, it’s dismissed as all wrong.

- In the happy season (all of a year ago), the tech bulls said, “You have to buy growth stocks for their decades of potential earnings increases.” But now, after a significant decline, we instead hear, “Investing based on future potential is too risky. You have to stick to value stocks for their ascertainable present value and reasonable prices.”

- Likewise, in the heady times, participants in IPOs of money-losing companies said, “There’s nothing wrong with companies that report losses. They’re justified in spending to scale up.” But in the present correction, many say, “Who would invest in unprofitable companies? They’re just cash incinerators.”

People who haven’t spent much time watching markets may believe that asset prices are all about fundamentals, but that’s certainly not so. The price of an asset is based on fundamentals and how people view those fundamentals. So the change in an asset price is based on a change in fundamentals and/or a change in how people view those fundamentals. Company fundamentals are theoretically subject to something called “analysis” and possibly even prediction. On the other hand, attitudes regarding fundamentals are psychological/emotional, not subject to analysis or prediction, and capable of changing much faster and more dramatically. There are adages that capture this dimension, too:

- The air goes out of the balloon much faster than it goes in.

- It takes longer for things to happen than you thought it would, but then they happen much faster than you thought they could.

As for the latter, in my experience, we often see positive or negative fundamental developments pile up for a good while, with no reaction on the part of security prices. But then a tipping point is reached – either fundamental or psychological – and the whole pile suddenly gets reflected in prices, sometimes to excess.

Then What Happens?

Bull markets don’t treat all sectors the same. In bull markets, as I discussed earlier, optimism coalesces most powerfully around certain groups of securities, such as “the new thing” or “super stocks.” These rise the most, become emblematic of the bull in this period, and attract further buying. The media pay these sectors the most attention, extending the process. In 2020-21, the FAAMGs and other tech stocks were the best examples of this phenomenon.

It goes without saying – but I’ll say it anyway – that investors holding large amounts of the things that lead in each bull market do very well. And fund managers who are smart enough or lucky enough to be dedicated exclusively to those things report the highest returns while optimism prevails and show up on the front page of newspapers and on cable TV shows. In the past, I’ve said our business is full of people who got famous for being right once in a row. That can go double for fund managers who are smart or lucky enough to be overweight the sectors that lead a bull market.

However, the stocks that rise the most in the up years often experience the greatest declines in the down years. The applicable adages here are from the real world, but that doesn’t reduce their relevance: “live by the sword, die by the sword;” “what goes up must come down;” and “the bigger they are, the harder they fall”:

- One tech fund rose by 157% in 2020, moving from obscurity to fame. But it lost 23% in 2021 and is down another 57% so far in 2022. $100 invested at year-end 2019 was worth $257 a year later, but that’s down to $85 today.

- Another tech fund, somewhat less volatile, was up by 48% in 2020 but is down by 48% since. Unfortunately, up 48% and down 48% don’t combine to produce zero change, but rather a net decline of $22 per $100 invested.

- A third tech fund was up a startling 291% in year one, but it fell by 21%, 60%, and 61% in the three years that followed. $100 invested at the beginning of this four-year period was worth $43 at the end, a decline of 89% from the end of that incredible first year. But wait a minute: there haven’t been four years in the current boom/bust. No, the results I cite are from 1999-2002, when the last tech bubble inflated and collapsed. I include them only as a reminder that the current performance pattern is a recurrence.

Earlier I mentioned Robinhood, the originator of commission-free trading. It epitomized the role of the digital in the 2020-21 bull market. Robinhood went public in July 2021 at $38, and over the next week, the stock price shot up to $85. Today it’s at $10, an 88% drop from the high in less than a year.

But the equity averages aren’t doing that badly, right? The tech-heavy Nasdaq Composite is “only” down 27.4% in 2022. One of the characteristics of this bull market is that the biggest companies’ stocks – which are the most heavily weighted – have done the best, buoying the indices. Consider what that implies for the rest; 22% of Nasdaq stocks are down at least 50%. (Data here and below are as of May 20.)

Here are the declines from the top of some well-known tech/digital/innovation stocks that I picked at random. Maybe there are a few here that, when they were at their peak, you kicked yourself for not having bought:

|

PayPal |

-57% |

|

Beyond Meat |

-63 |

|

Coinbase |

-74 |

|

Salesforce |

-37 |

|

Carvana |

-86 |

|

DocuSign |

-50 |

|

Moderna |

-46 |

|

Netflix |

-69 |

|

Shopify |

-74 |

|

Spotify |

-54 |

|

Uber |

-44 |

|

Zoom |

-51 |

|

Average |

-59% |

Let’s say you still believe market prices are set by a consensus of intelligent investors on the basis of fundamentals. If that’s the case, then why are all these stocks down by such large percentages? And do you really believe the value of these businesses has more than halved on average in the last few months? This line of inquiry leads to something else I think about often. On days when the stock market makes its biggest moves, Bitcoin often moves in the same direction. Is there any fundamental reason why the two should be correlated? The same goes for international links: when Japan starts off the day with a big decline, Europe and the U.S. often follow suit. And sometimes it seems U.S. stocks lead and it’s Japan that falls in line. Are these countries’ fundamentals connected enough to justify co-movement?

My answer to all these questions is generally “no.” The common thread isn’t fundamentals: it’s psychology, and when the latter changes significantly, all of these things are similarly affected.

The Lessons

As always for students of investing, what matters most isn’t what events transpired in a given period of time, but what we can learn from these events. And there’s a lot to be learned from the trends in 2020-21 that rhymed with those in previous cycles. In bull markets:

- Optimism builds around the things that are doing spectacularly well.

- The impact is strongest when the upswing arises from a particularly depressed base in terms of psychology and prices.

- Bull market psychology is accompanied by a lack of worry and a high level of risk tolerance, and thus highly aggressive behavior. Risk-bearing is rewarded, and the need for thorough diligence is ignored.

- High returns reinforce belief in the new, the unlikely, and the optimistic. When the crowd becomes convinced of those things’ merit, they tend to conclude “there’s no price too high.”

- These influences cool eventually, after they (and prices) have reached unsustainable levels.

- Elevated markets are vulnerable to exogenous events, like Russia’s invasion of Ukraine.

- The assets that rose the most – and the investors who over-weighted them – often experience painful reversals.

These are themes I’ve seen play out numerous times during my career. None of them relates exclusively to fundamental developments. Rather, their causes are largely psychological, and the way psychology works is unlikely to change. That’s why I’m sure that as long as humans are involved in the investment process, we’ll see them recur time and time again.

And, as a reminder, since the major ups and downs of the markets are primarily driven by psychology, it’s clear that market movements can only be predicted, if ever, when prices are at absurd highs or lows.

May 26, 2022

Legal Information and Disclosures

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Oaktree.

© Oaktree Capital Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All