Friday, June 3, 2022

Labor Markets Are Tight With Little Signs Of Loosening

Employment in May grew by 390,000, driven by strong gains in leisure and hospitality, in professional and business services, and in transportation and warehousing. Job growth does not exist in an economy that has a high chance of going into a recession. The LPL Chart of the Day shows the 3-month average gain dipped from the highs from last year. “A softer trend is consistent with the slowdown in economic growth in the coming quarters but not outright contraction” explained LPL Financial Chief Economist Jeffrey Roach. Unemployment in May was 3.6%, unchanged for the third consecutive month and average hourly earnings increased 5.2% from a year ago. In this post, we look at the lingering effects from the pandemic and why the labor market is stubbornly tight.

Unemployment Is Too Low, Too Long For Some People

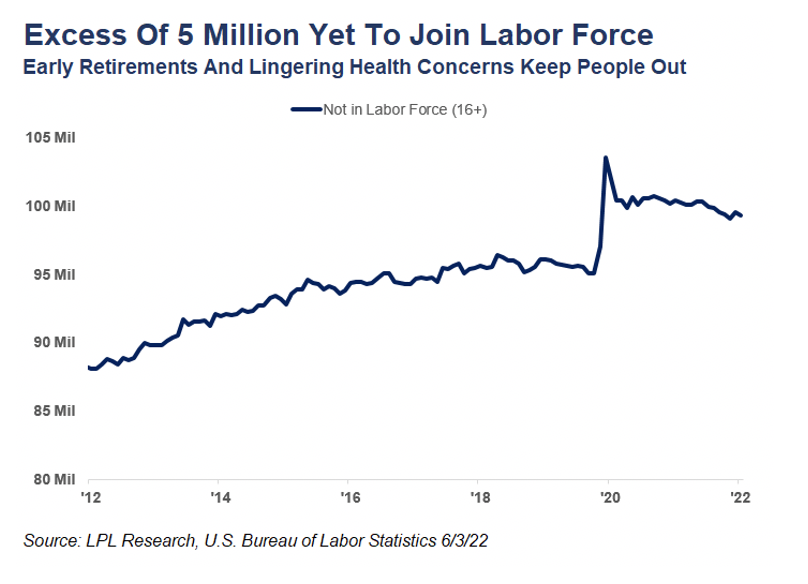

One reason that unemployment is low is from the large amount of individuals not in the labor force. Relative to pre-pandemic levels, the economy has an excess of roughly 5 million people who do not have a job nor are looking for a job. The Bureau of Labor Statistics does not include individuals without a job in the unemployment rate if those individuals are not actively looking for work.

The long-term unemployed account for roughly 23% of all unemployed persons and should be a concern as “skill erosion” sets in for those out of work for an extended period. Even after social distancing restrictions lifted in many areas, schools and day care facilities remained constrained last year, causing many caregivers to remain unemployed. Those unemployed for over 27 weeks are considered long-term unemployed and if this category remains elevated for an extended period, the economy could have lasting scars.

Construction Job Market Is Especially Tight

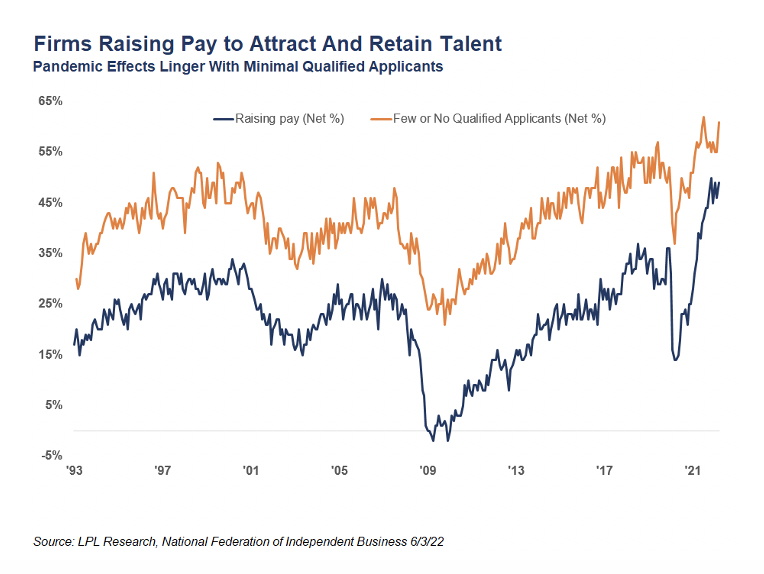

The National Federation of Independent Business (NFIB) report that 61% of firms in all sectors are having few or no qualified applicants for current job openings. This metric is at all-time highs but the construction sector is more concerning: 69% of construction firms reported few or no qualified applicants. As a result, firms are raising total compensation to attract and retain talent. We see this as a risk to the inflation outlook if these imbalances remain and become embedded in the economy. But encouragingly, employment prospects are good and a strong labor market will help offset the impact of rising borrowing costs.

From the earlier Job Openings and Labor Turnover Survey (JOLTS), the labor market is extremely tight as quit rates are high, revealing that workers in many industries know they can likely get higher wages if they move from one firm to another. Still, the economy had roughly 2 openings for each unemployed individual.

Federal Reserve Likely to Continue on Projected Tightening Path

Job gains in May were broad based and with another good labor report, the Federal Open Market Committee (FOMC) can emphasize the imbalances to price stability over supporting labor markets. Inflation is the paramount concern for committee members and a tightening labor market adds fuel to the fire. As job gains moderate and more people come into the work force, we could see the unemployment rate increase, removing some of the tightness of the labor market. Our base case projection is the FOMC increases rates again in June by 50 basis points (0.5%).

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. For more information on the risks associated with the strategies and product types discussed please visit https://lplresearch.com/Risks

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

Tracking # - [as is applicable]

LPL Research looks at the May jobs report and its impact on markets and Federal Reserve (Fe

Read more commentaries by LPL Financial