Global Economic Outlook: Tightening Up

In the two years following the discovery of COVID-19, the world has endured cycles of slowdowns and recovery that were often well-aligned. Fighting the virus was a global challenge, as were the complications endured in global supply chains. Headlines from any region might sound familiar to readers anywhere else.

Today, the growth of economies around the world is slowing, but in ways that are less coordinated and comparable. Not all nations have learned to live with the virus; spillover from the war in Ukraine is uneven; and inflation is more bearable for some economies than others. Most central banks are moving toward tightening, but at different speeds.

Slowing does not mean contracting. Moderations in growth do not necessarily lead to recession. We believe the world’s major economies can pull through today’s challenges, but downside risks are growing.

Here are perspectives on how major economies are poised to perform this year and next.

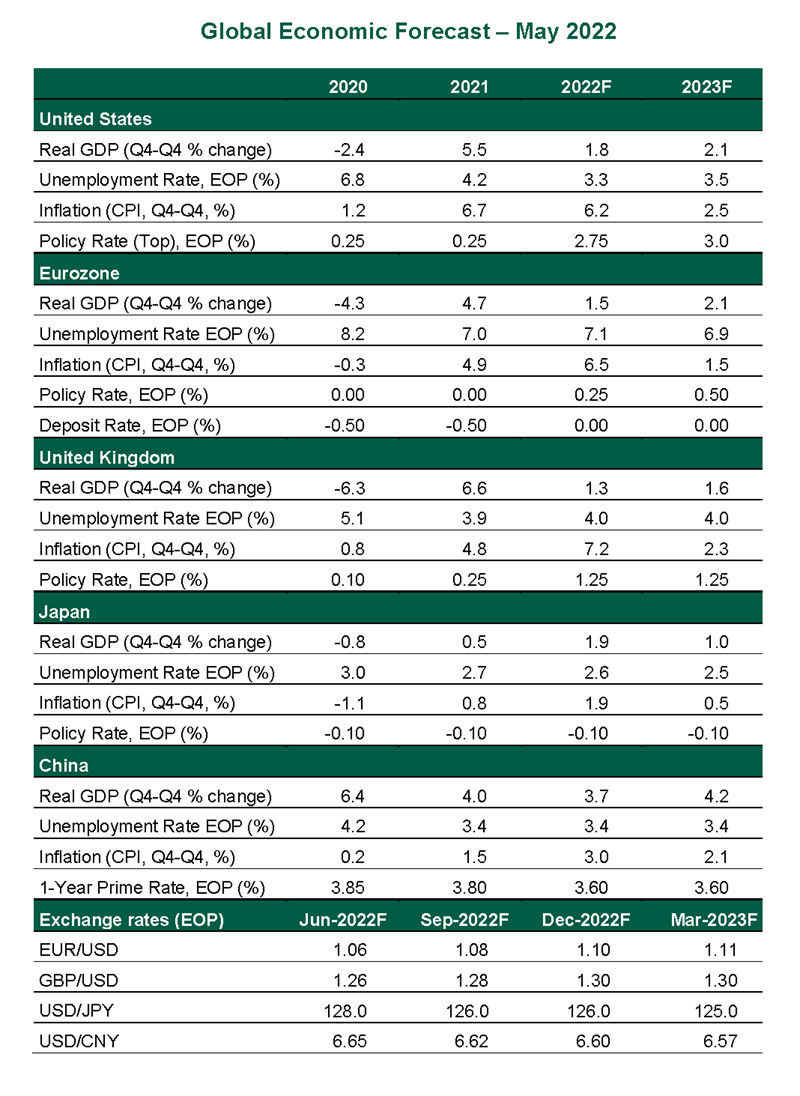

United States

- The April reading of the consumer price index (CPI) was a slight improvement from March, and likely marks the start of a decline in inflation. However, the rate is still far too high, and the decline too slow. The Federal Reserve is acting decisively, raising the overnight Fed Funds rate by 50 basis points in May and starting to reduce its balance sheet in June. We expect two more hikes of the same size to follow, continuing in smaller increments into 2023, to a top level of 3.0%.

- Despite inflation and rising interest rates, the U.S. economy is performing well. Domestic demand is resilient, and job creation continues, with April unemployment holding at 3.6%. As long as labor markets hold their stamina, the Fed will focus on fighting inflation, and the economy can keep growing. These favorable prospects are adding to the value of the dollar, which will also help curb domestic inflation.