"It is incumbent on every generation to pay its own debts as it goes. A principle which, if acted on, would save one-half the wars of the world." -Thomas Jefferson

Rising debt levels

To begin with, an admission. The subtitle of this month’s Absolute Return Letter – Is Gold the Answer? – will only get a brief mention this month and will instead be covered in more detail next month. It is a terribly important topic and deserves more space than the couple of paragraphs I could allocate to it this month.

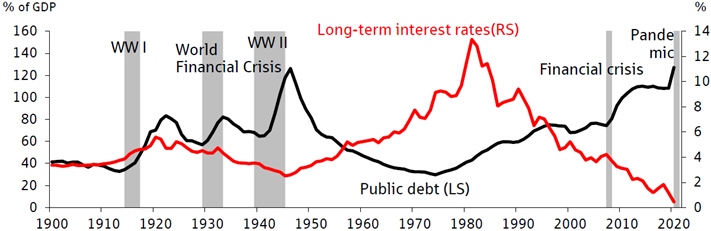

Next, the bad news. According to the IMF, global debt continues to rise at a mind-blowing pace. On a worldwide basis, as at the end of 2020, public debt-to-GDP in advanced economies had risen to 124% (sources: IMF and Exhibit 1). The 2021 numbers have not been published yet but, given the continued economic damage from COVID-19, an even grimmer picture will probably emerge later this year, when those numbers are published.

Exhibit 1: Public debt-to-GDP in advanced economies

Sources: Finanzgruppe Deutscher Sparkassen und Giroverband, IWF, Helaba

According to the IMF, at the end of 2020, total global debt (household, corporate non-financial and government debt combined) added up to US$226Tn – equivalent to a debt-to-GDP ratio of 256% – up 28% from the previous year with government borrowings accounting for slightly more than half of the increase. I am sure some of you will argue that 124% is not the end of the world, but those who argue that seem to have forgotten that:

i. once you have removed those countries from the list that manage their debt responsibly, a much bleaker picture emerges;

ii. with interest rates rising rapidly, refinancing existing debt will be a great deal more expensive than many governments are prepared to admit; and

iii. although you may not remember this, when the Eurozone was created, 60% public debt-to-GDP was considered the most member countries were allowed.

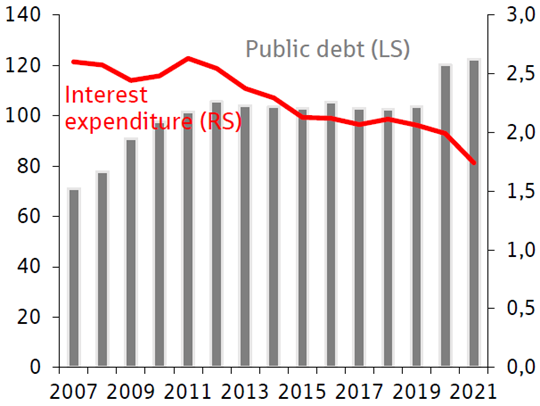

On the second point, and as you can see in Exhibit 2 below, the cost of servicing public debt in advanced economies has actually fallen over the last 15 years despite debt levels rising incessantly. Now, with interest rates rising again, some countries could be in trouble relatively soon.

Exhibit 2: Public debt vs. interest expenditures in advanced economies, % of GDP Sources: Finanzgruppe Deutscher Sparkassen und Giroverband, IWF, Helaba

As far as the third and final point is concerned, there was, and still is, a reason for the debt ceiling to be set at 60%. Governments depend on taxes to finance public debt, and tax revenues are a function of economic activity – the faster GDP grows, the more tax revenues come in. When the founders of the euro agreed to 60%, it was (at least partially) because interest rates fluctuate over time. By limiting public debt-to-GDP to 60%, they expected the new currency to be rock-solid even during adverse economic conditions. Many member countries have since forgotten all about that and have instead chosen to manage their debt as if interest rates will remain close to 0% forever. As we have learnt in recent months, that is a pretty poor hypothesis.

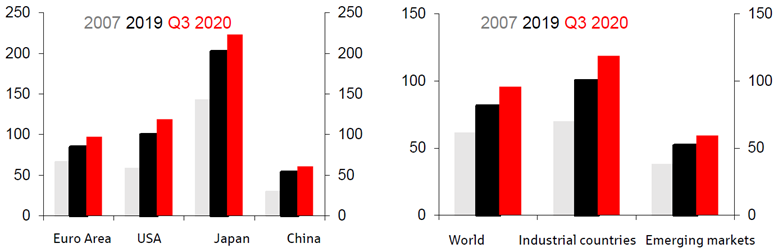

Before I make it sound like excessive debt levels are specific to the eurozone, I should mention that US debt levels are higher than what we are accustomed to in the eurozone, and that Japanese debt levels are on a different planet altogether (Exhibit 3). The Japanese have (so far) gotten away with it as Japanese government bonds are absorbed almost exclusively by domestic investors who have (so far) chosen to support the government, but a public debt-to-GDP level well in excess of 200% spells problems at some point.

Exhibit 3: Public debt-to-GDP Sources: Finanzgruppe Deutscher Sparkassen und Giroverband, IWF, Helaba

Meanwhile, the US government benefits from the US dollar’s status. Being the primary reserve currency of the world grants the Americans a number of advantages that are not on offer to the average borrower. However, should the Chinese succeed with their strategy to make the renminbi a significant reserve currency, the Americans will suddenly find it more difficult to get away with current debt levels.

Is gold the answer?

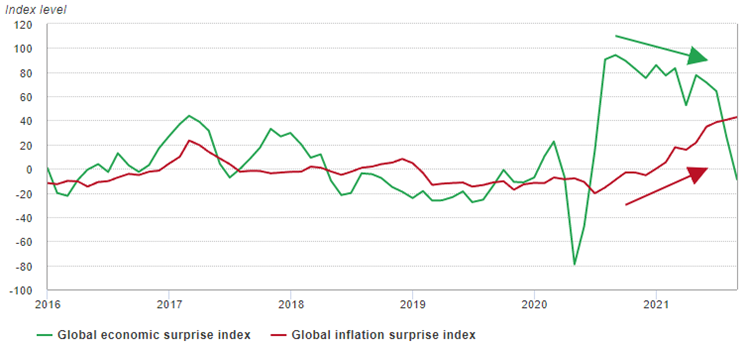

As I have pointed out in previous Absolute Return Letters, gold is a robust hedge against unanticipated inflation but not such a great hedge, when nearly everybody can see the inflation coming. Exhibit 4 below measures to what extent already published economic data were in line with expectations. As you can see, over the last couple of years, economic growth data have surprised a great deal more than inflation data have.

Exhibit 4: Global surprise indices Source: gold.org

This may explain the modest participation of gold so far in the ‘inflation party’, and it most definitely explains my modest appetite for gold in the most recent inflation cycle – at least so far. Having said that, I see some worrying signs that inflation won’t go away as easily as many predict it will. For that reason, in my book, the jury is still out on gold. I will seek to dig deeper on this topic in next month’s Absolute Return Letter.

Obviously, the worst possible mix is no or negative economic growth combined with high inflation – aka stagflation. In that context, I note that, only a week ago, I increased the probability of a forthcoming global recession. If you are a subscriber to ARP+ and haven’t read that paper yet, I urge you to do so. You can find it here.

Final few words

There can be no doubt that certain European governments (e.g. the government of Italy) have taken some considerable comfort from Japan’s ability to get away with much higher debt levels than anything we have seen (so far) in Europe or North America. However, that is a poorly thought-through argument, which I doubt will stand the test of time.

First and foremost, large Japanese institutions are loyal to the Japanese government to an extent we don’t see anywhere in Europe or North America. Secondly, the Japanese government’s dependence on foreign investors to take a portion of its newly issued bonds is non-existent. Non-Japanese investors are quite simply a complete non-factor in the Japanese government bond market. You can hardly say the same about any European or North American country.

Should interest rates continue their rapid move upward, I therefore believe we’ll have a financial accident of some sort in our part of the world, but please note my words – it is still “if” and not “when”. Much will depend on how aggressively unions respond to the recent rise in food and energy prices. If they go for their members to be fully compensated, a situation will most likely emerge that bears a striking resemblance to the late 1970s. In that scenario, we could suddenly face double digit interest rates, in which case one or two OECD governments could face serious problems, given current debt levels.