Russia’s invasion of Ukraine happened only three weeks ago, but the magnitude of the event is being felt in all economies. The U.S. economy is well removed from the conflict, both geographically and commercially (due to small trade linkages with both nations).

The conflict’s effects on energy and commodity markets, however, are unavoidable. A spike in oil prices has added to inflationary pressures that were already high. Consumers notice the increase in gasoline prices immediately, while higher energy costs flow through to the final prices of nearly all goods and services.

The war did not change our baseline U.S. outlook. The domestic economy has a number of tailwinds: low COVID-19 cases, higher wages, pent-up demand and elevated savings will motivate consumers to continue spending. Inventories will rebuild as supply chain challenges are gradually overcome. We expect that positive momentum will allow the economy to keep growing, but downside risks are accumulating.

Key Economic Indicators

Influences on the Forecast

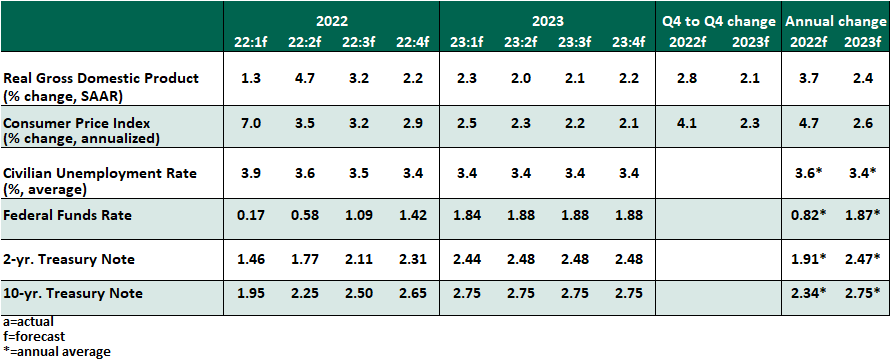

- At its March meeting, the Federal Open Market Committee (FOMC) began an interest rate hiking cycle. The quarter-point increase will be followed by several more. We forecast six more hikes, leveling off in a range of 1.75-2.0%. The quarterly Summary of Economic Projections indicated several committee members expect an even more rapid trajectory of increases. High inflation and strong employment are the signals for a central bank to tighten, and we expect those conditions will persist.

- The employment recovery continues apace. In February, payrolls increased by 678,000, the fourteenth consecutive month of gains. Total payrolls are now 2.1 million lower than their pre-pandemic peak, a gap that will continue to close.

- The labor force participation rate has recovered to 62.3% overall and 82.2% for prime-age (25-54) workers, each about 1% below their pre-pandemic levels. There is room for more workers to return, and no shortage of opportunity, with over 11 million job openings as of January.

- Wages were flat month over month and grew 5.1% year over year, which is not enough to keep pace with inflation. While policymakers are keen to avoid a wage-price feedback loop, real wage declines are a contributor to dour consumer sentiment.

- The February reading of the consumer price index (CPI) showed prices increased by 7.9% from a year before, the fastest rate in 40 years. Inflation was highest in energy and food prices, the categories that keep inflation front of mind for consumers. The Fed’s preferred measure, the deflator on core personal consumption expenditures, grew 5.2% in January, far beyond the FOMC’s comfort.

- We expect the first quarter will bring the highest core inflation readings; as production recovers and pent-up demand cools, prices will cease to increase quite so rapidly.

- Some inflation, like in shelter costs, is likely to prove sticky, while energy markets have entered a new era of higher prices and greater volatility. After a long run of predictable, well-controlled inflation, the years ahead will feature new pricing dynamics.

- Elevated inflation and monetary tightening are evident in fixed income markets, as the 10-year U.S. Treasury yield pushed to a post-pandemic high of over 2.1%. However, the yield curve has flattened overall; the risk of inversion could cause some FOMC members to second-guess their hiking intentions.

- Congress passed a $1.5 trillion omnibus spending package that will fund the government through the remainder of the fiscal year, ending a chain of continuing resolutions that left open the risk of a government shutdown. Discussions of additional stimulus emerge in fits and starts, but authorization for any significant additional spending seems unlikely at this time.

- The outlook for higher interest rates is likely to cool rate-sensitive sectors, notably housing. The Federal Housing Finance Agency estimates that in the full year 2021, residential house price values grew by 16.8% nationwide, an unsustainable rate of appreciation, while rents are also increasing across markets. Renters and new home buyers are left feeling outsized inflation pressures.

© Northern Trust

Read more commentaries by Northern Trust