What kind of opportunities has the down market created?

While every Russell 2000 Index sector except for Energy was down year-to-date through 2/24/22, a disproportionate amount of negative performance has so far come from Health Care and Information Technology. Within those sectors, industries populated with companies that have no or low profitability but high long-term growth expectations, e.g., biotechnology and software, have been among the hardest hit. This correction in speculative growth small-caps has thus far yielded fewer new opportunities for us given our focus on reasonably valued, high-quality business models that generate and sustain high returns on invested capital and consistent free cash flow. However, as the market often throws the baby out with the bathwater in sector drawdowns, we’ve found buying opportunities in existing holdings or new purchase candidates among select, highly profitable niche market leaders in these sectors.

In addition, several cyclical areas, such as semiconductor equipment, machinery, and consumer-related names, have also seen sharp pullbacks rooted in concerns they’ve reached peak profitability given the potential for slower GDP growth as the Fed begins to raise rates. Evaluating these businesses on the basis of normalized earnings power has revealed some superior companies that are at or approaching attractive valuations, even assuming profitability contracts to mid-cycle levels.

Have there been any notable trends in guidance or outlooks in the most recent earnings seasons?

It has been a bit of déjà vu—mostly similar to the second half of 2021, with supply constraints and inflation pressuring financial results and forward guidance. Commentary from management teams about demand has generally been very positive, supported by healthy order rates and with unusually high backlogs that provide promising sales visibility as supply chain issues gradually ease. Another common theme we’ve seen is accelerating investments in capacity expansion—both in plant & equipment and in headcount—to address existing bottlenecks and/or support industry or company-specific secular growth trends. In general, companies seem to be guiding that 2022 results will be muted early before growing more favorable in the second half of the year, with margins improving each quarter. Unlike what we saw in the second half of 2021, however, this news has often not been well received by investors. The continuing push-out of backlog conversion has raised concerns that projected profit may not fully materialize if macro factors such as the end of pandemic stimulus programs, higher prices, rising interest rates, and geopolitical issues cause demand to decelerate as the year goes on.

“Commentary from management teams about demand has generally been very positive, supported by healthy order rates and with unusually high backlogs that provide promising sales visibility as supply chain issues gradually ease. — Lauren Romeo

Can you discuss one holding that’s held up well so far in 2022 and what’s helped it to do so?

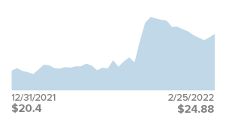

A notable mention is Meridian Bioscience (VIVO), a profitable health care company that derives more than half of its revenue from its Life Sciences segment in which it sells consumable reagents used to make in-vitro diagnostic (IVD) tests. The remainder of Meridian’s sales comes from its Diagnostics segment where the company develops and manufactures IVD tests and instruments, with a particularly strong niche position in various gastrointestinal diseases. Meridian’s stock was up 19.8% year-to-date through 2/24/22, boosted by above average results in its most recent quarter that reflected improved organic growth in Diagnostics despite the absence of sales for its high margin, blood lead level test that Meridian voluntarily recalled from the market last summer due to a supplier quality issue. We think momentum for the Diagnostics segment will accelerate due to four factors: gastro and respiratory test volumes returning toward pre-pandemic levels, share gains in gastro aided by a complementary acquisition made last year, the addition of Meridian’s newly approved Covid test to its molecular test menu (for the June quarter), and the resumption of distribution of the blood lead level test, which was recently restarted.

Meridian also continues to work to better commercialize new tests on a more consistent cadence, including the likely submission of four new assays to the FDA this year. Assuming normal approval rates, regular new test introductions should further bolster the case for Diagnostics to be at least a mid-single digit organic growth business. At that level, the segment (which will be marginally profitable this year) should begin to leverage its R&D spend and fixed costs, driving meaningful annual operating margin expansion toward Meridian’s longer-term goal of 20% for Diagnostics. In Life Sciences, Meridian won a significant number of new commercial customers during the pandemic by being able to supply reagents for test manufacturers scrambling to ramp up Covid test production. While that elevated volume won’t be sustained, Meridian has increased confidence in the new level of “normalized” run rate revenue for Life Sciences as Covid will likely become a standard respiratory test and because Meridian has been successfully expanding its reagent sales for other tests with its new customers. These market share gains, along with the ongoing introduction of new products, should support low double-digit Life Sciences sales growth off the normalized revenue base. And reagents sales generate high incremental margins, further fueling Meridian’s overall earnings and cash flow growth.

Meridian Bioscience (VIVO) 12/31/21 through 2/25/22

Can you also tell us about a holding that hasn’t done well but in which you still have long-term confidence?

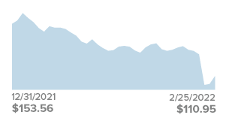

John Bean Technologies (JBT) derives the majority of its sales and profits from Food Tech, i.e., food processing systems and automation solutions used across the production value chain for protein, plant-based, and liquid food producers. The company’s leading market shares and broad solution set mean that if we ate or drank something today, there’s a very good chance that JBT technology played a part in its preparation. Nonetheless, its stock has fallen more than 30% so far in 2022 after 4Q21 earnings and 1Q22 guidance were significantly impacted by the trifecta of difficulties sourcing a sufficient supply of electronic components that complete the functionality of JBT’s equipment, higher logistics costs to bring in what components it could get, and labor shortages exacerbated by Omicron in January.

While disappointing, we believe these issues are temporary and fixable rather than representing a structural change in the company’s competitive position or long-term growth prospects and earnings power. Demand remains robust, with Food Tech orders in the quarter up 22% over the pre-pandemic 4Q19 level. Strong order growth, combined with recent production and shipping delays, has driven backlogs to all-time highs, which provides JBT with some enhanced revenue visibility. The backlog should remain firm. Cancellations or “double-ordering” have historically been low since JBT requires a 25% nonrefundable deposit on orders. Visibility toward a return to more historically normal profitability is further supported by the fact that about 45% of the Food Tech segment’s annual revenue is recurring, reflecting aftermarket parts and services on JBT’s large and expanding installed base of equipment. Price increases, which lag cost inflation by about a quarter, and a recovery in sales to more normalized quarterly run rates should push incremental margins back to the company’s traditional level over the next several quarters. Finally, given its strong market position and innovative product offerings, JBT is poised to benefit from strong food tech tailwinds, including rising global protein consumption as per capita incomes increase, food producers’ increasing investment in labor-saving and yield-enhancing automation, and heightened emphasis on food safety and “clean” or natural ingredients.

John Bean Technologies (JBT) 12/31/21 through 2/25/22

Read more commentaries by Royce Investment Partners