Global Economic Outlook: Prices And Peacemaking

As COVID-19 concerns fade, the global economy has the opportunity to make further progress. But a sustained bout of inflation and geopolitical tensions have taken center stage. Inflation continues to surge, with the peak yet to be seen in some countries. The Ukraine-Russia conflict is fueling uncertainty and pushing down sentiment.

For now, risks are tilted to the upside, and central banks will be tightening policy in response. The end of accommodation reflects an orderly return to the pre-crisis normal. But a broader conflict in Eastern Europe could provoke a wholesale reevaluation of the outlook.

Following are perspectives on how major economies are poised to perform.

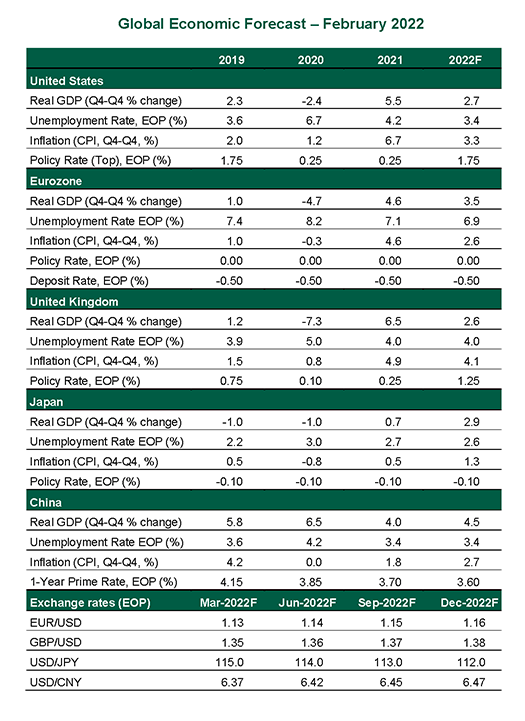

United States

- Inflation persists at uncomfortable levels, with the consumer price index (CPI) gaining 7.5% during the year ending in January. Rapid appreciation of rents, energy costs and most categories of food have been among the biggest contributors. As the pandemic recedes, consumption patterns may shift away from goods and towards services, which would alter but not diminish price pressures in the months ahead.

- At its January meeting, the Federal Open Market Committee affirmed a course of ending asset purchases in March, with rate hikes set to commence at their March meeting. The Fed will have to raise rates steadily to combat inflationary forces, though some are beyond their control. We expect considerable tightening through 2022, with the policy rate peaking at 2% early next year.