Inflation remains the primary point of discussion in the economic outlook. Data for January found consumer prices 7.5% higher than one year prior, the highest escalation since 1982. Forecasters, including ourselves, have persistently underestimated the pace of the price level; there may be more unpleasant surprises ahead.

This has prompted a rapid change in posture from the Federal Reserve. Rate increases are imminent, to be followed by balance sheet reduction. All of this has had a profound impact on the bond market.

The U.S. economy is fundamentally performing well; maybe too well. The Omicron variant of COVID-19 hindered activity in the early part of the year, but case counts are falling rapidly. This could allow a surge in activity as spring begins. Employment and wage gains continue, keeping demand elevated above supply.

Inflation is emerging as the price to be paid for a rapid recovery. This may be a better problem to have than an enduring recession, but it is a problem nonetheless.

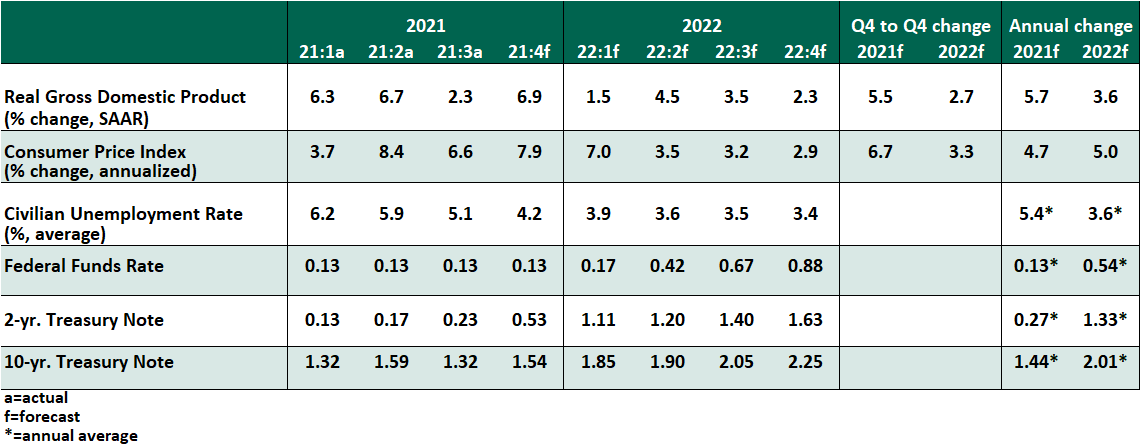

Key Economic Indicators

Influences on the Forecast

- Inflation persists at uncomfortable levels. On a month-over-month basis, consumer prices increased 0.6% both overall and on a core basis (excluding food and energy): lower than the peak months of 2021, but still too high. Rapid appreciation of rents, energy costs and most categories of food highlighted the report.

Concerningly, service prices may come under additional pressure in the months ahead. Should the pandemic become less threatening, consumption patterns may shift away from goods and towards activities like entertainment and travel. Those sectors are struggling with labor shortages, which has the potential to make them more expensive.

- The January Employment Situation Summary revealed continued improvement in spite of COVID-19. Omicron-related absences from the workplace last month led to expectations that the report would be a negative anomaly; instead, payrolls grew by 467,000. Hourly wages increased by 0.7%, bringing the year over year increase in this measure to 5.7%.

- The routine annual benchmarking in this report had a noteworthy outcome. Continuing a trend of upward revisions, payroll growth last year was stronger than initially reported. Employment is now 2.9 million jobs shy of its pre-pandemic peak.

- At its January meeting, the Federal Open Market Committee affirmed a course of ending asset purchases in March, with rate hikes all but guaranteed to commence at their next meeting on March 16. The questions ahead are:

- How many rate hikes will follow? To cool economic activity, the Fed would need to raise rates sizably and rapidly. However, much of the current inflation is driven by supply constraints that will ease this year, lowering inflation and taking away some of the current urgency to act. We have considerable tightening in our forecast, but we may add additional moves on the basis of the FOMC meeting in March.

- How soon and to what extent will the balance sheet shrink? The meeting included a set of principles for reducing the balance sheet, which were too vague to be taken as firm guidance, but made clear that asset reduction would begin only after rate hikes commence. Our views on quantitative tightening can be found here.

- Fourth quarter 2021 gross domestic product grew at a 6.9% annualized rate. The primary driver of the high growth figure was a return to inventory restocking following three quarters of depletion. Consumer spending and business investment cooled as the year ended, and we have adjusted our forecast to expect a slower start to the year, with a return to stronger activity in the second quarter as the COVID surge fades.

- As central bank tightening looms and inflation persists, bond yields are rising, with the U.S. 10-year treasury bill reaching a post-pandemic high of 2.0%. A steadier outlook should allow for steadier pricing going forward; we expect gradual yield gains across the curve.

- The Omicron surge appears to have played out in the best case scenario: infections were generally less severe, and infection rates are falling rapidly nationwide. Renewed calls for loosened COVID policies are a sign of a stronger appetite for normal consumer spending, which may include more trips taken and meals eaten out.

© Northern Trust

Read more commentaries by Northern Trust