Recently, euro-based investors have been able to access higher-yielding US dollar bond markets while hedging their currency risk at low cost. Now, interest rates are set to rise in the US—and we think it’s time for US dollar investors to consider opportunities in euro fixed-income markets.

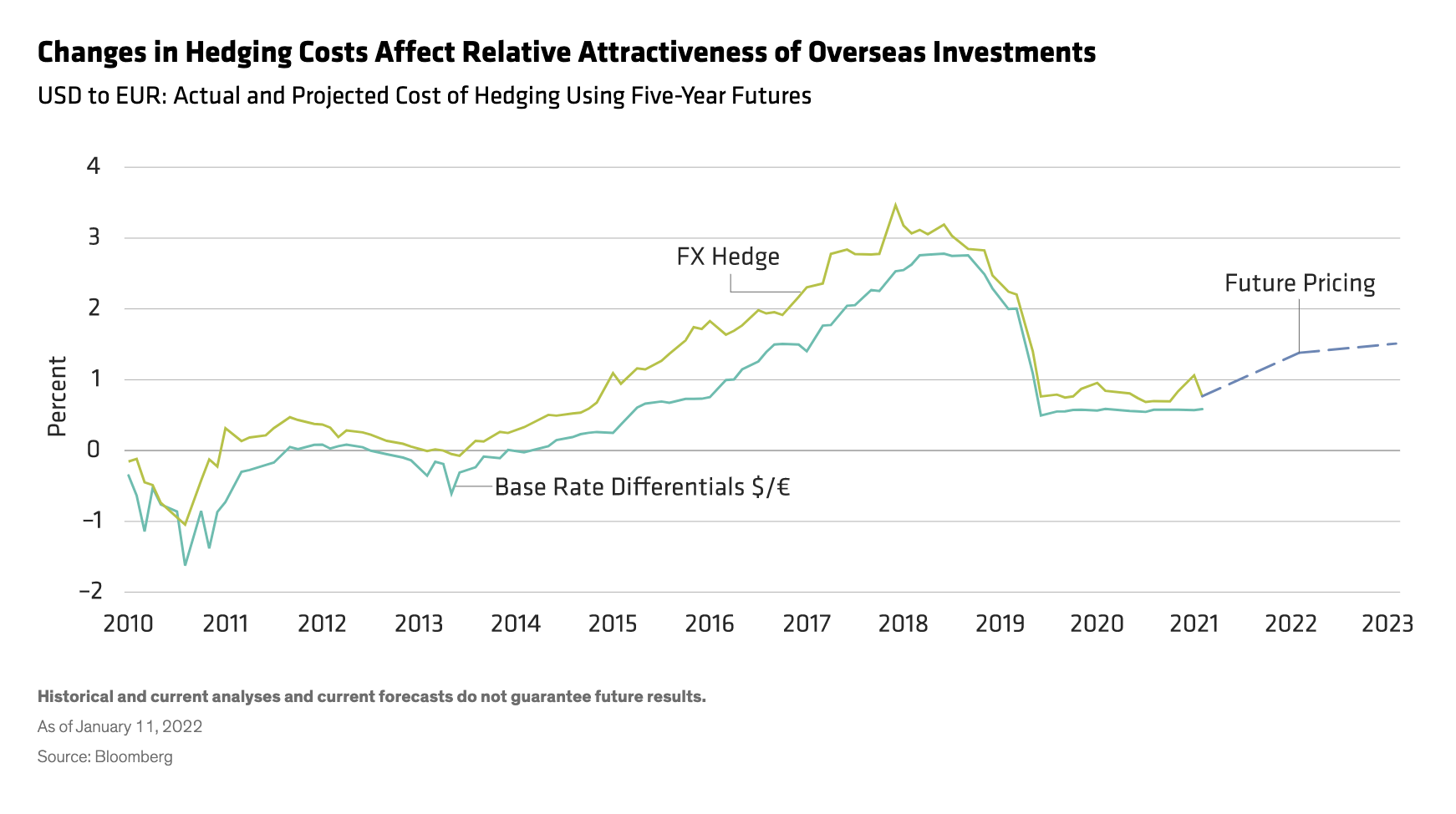

The cost of hedging foreign currency risk changes over time, mostly reflecting shifts in interest-rate differentials between currency pairs. When hedging costs are low or negative, it can make sense for investors to take advantage of attractive opportunities overseas. For instance, over the last 12 years, there have been two periods where low or negative US-dollar-to-euro hedging costs have made it attractive for investors in the eurozone to buy higher-yielding US dollar–denominated bonds (Display).

Now, as US interest rates are expected to increase, things are changing. Forward currency markets show that the cost of hedging dollars to euros will rise, making dollar-denominated bonds less attractive for Europeans on a currency-hedged basis relative to their home markets.

Conversely, rising US rates will make hedging euros back to US dollars more attractive for dollar-based investors. From their perspective, hedging costs have been negative for some time, bringing currency-hedged yields nearer to parity. But now, the economics of putting US dollars to work in euro fixed-income markets are looking much more compelling, for several reasons.

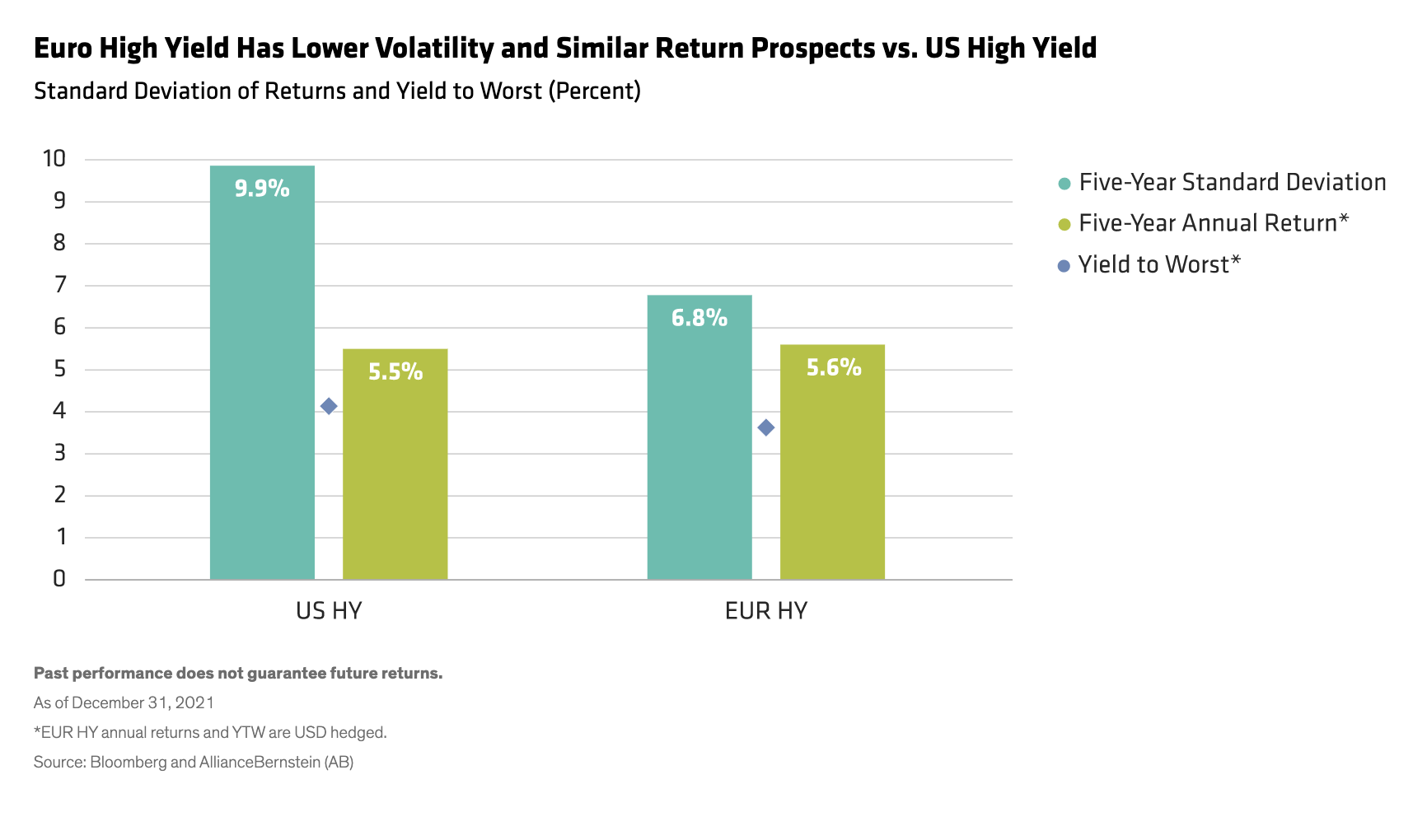

Firstly, returns in euro markets look similar, but with lower risk. In high yield, for instance, yield to worst across both markets is very close at around 4% on a US dollar–hedged basis. Returns have been similar over the last five years too, but volatility has been markedly lower in euro markets (Display).

We think euro market volatility will stay lower in future too, because of some important technical and fundamental differences between the two markets.

Euro Fixed Income Has Stronger Support and Higher Quality

Secondly, unlike the US, euro fixed-income markets will continue to benefit from very strong central bank support. European Central Bank (ECB) President Lagarde continues to warn against premature policy tightening in the eurozone. Consequently, we expect a continuation of large-scale corporate bond purchases by the ECB, with no rate rises in the euro area at least through the current year.

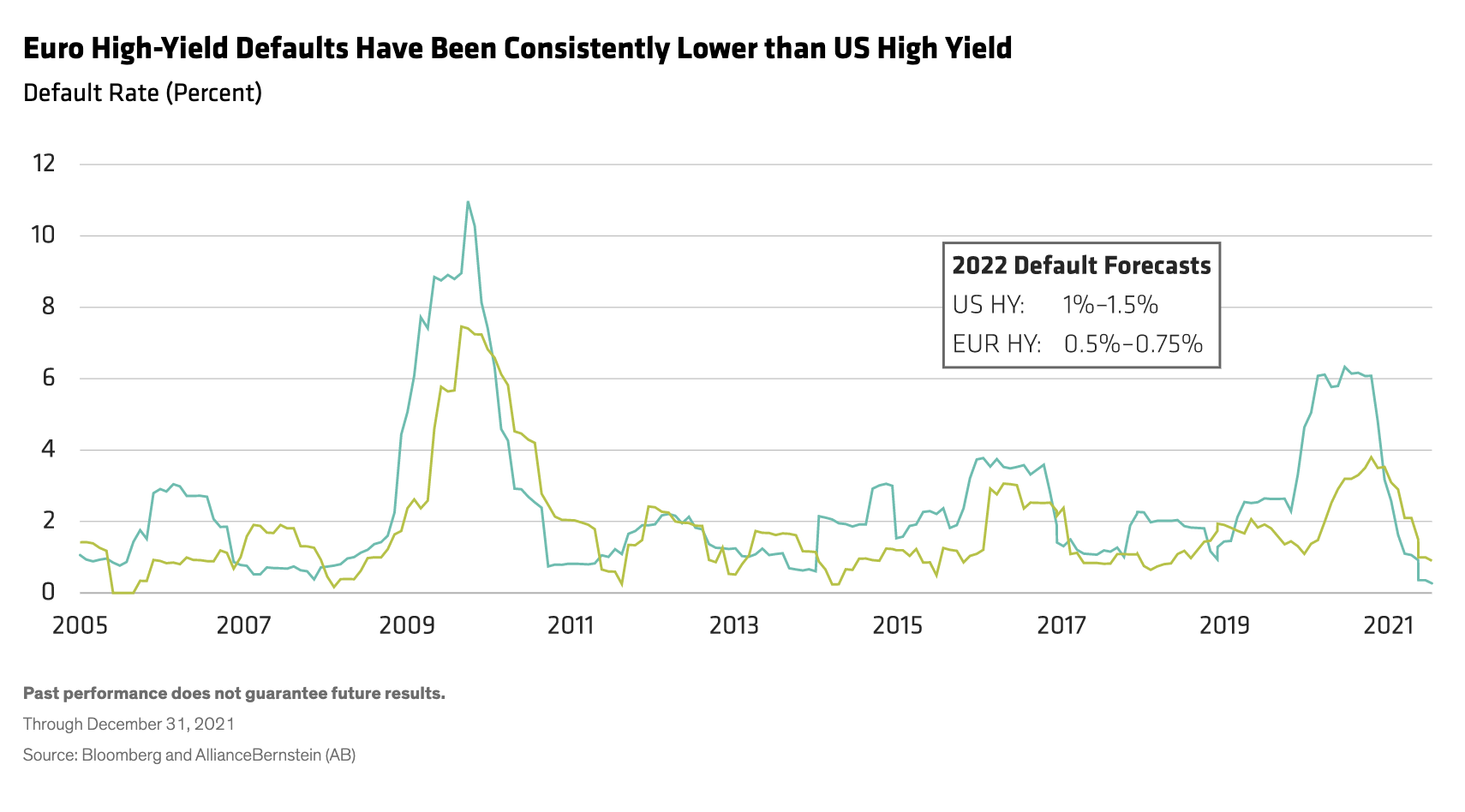

Also, the euro high-yield market has better credit quality than US high yield, with a higher proportion of BB-rated issues (14% more) and correspondingly fewer B and CCC-rated bonds. Euro high yield likewise has experienced a lower annualized default rate over the last five years than US high yield (3% versus 5%) and has a lower forecast default rate for the current year (Display).

Euro High-Yield Spreads Are Attractive

Lastly, the timing is good for US dollar investors to diversify into euro fixed income. Euro spreads tend to be tighter than the US, by an average 34 b.p. over the last 20 years for BBB IG credits as an example. However, they have widened recently to be on par with US spreads. Considering the qualitative differences between the two markets, we think that over time the spread differential should revert to the mean, favoring euro fixed-income bonds.

One particular spread sector where European banks have the largest share of issuance is bank subordinated debt, in particular AT1s. We think European AT1s that are liable to be redeemed shortly represent good potential value: They offer attractive coupons but with much less interest-rate sensitivity (duration) than the broader investment-grade or high-yield markets. Europe also leads in terms of ESG-linked bond structures, with the potential for spreads to narrow in this increasingly popular market segment.

Of course, US fixed-income markets remain the world’s largest and most diversified, with spread sectors of their own that look particularly attractive—notably, in the mortgage and securitized segments. So US dollar-based investors are likely to keep their main fixed-income exposure at home. But with currencies and markets always moving to create fresh opportunities, now looks to be a good time to diversify into euro fixed income.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein