Labor's Love Lost: A Deep Dive Into "The Great Resignation"

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIt’s been called “Mass Attrition,” “The Big Quit,” and “The Great Resignation.” These epithets all attempt to summarize the sea change that has come over the American labor market. COVID-19 appears to have created permanent changes in the workforce, leaving businesses short-handed and economists bewildered.

While there are still millions of people who have not held jobs since February 2020, U.S. labor market conditions are consistent with full employment. Wages are rising rapidly, contributing to a surge in inflation. Job turnover is at a record level, and there are 10.6 million unfilled roles in the U.S. economy.

A series of studies have attempted to understand the root causes of these developments. A scan of this literature reveals that there are several different forces at play, all of which intensify trends that had been underway prior to COVID-19. As they evolve, they will have significant short- and long-term consequences.

The Old World

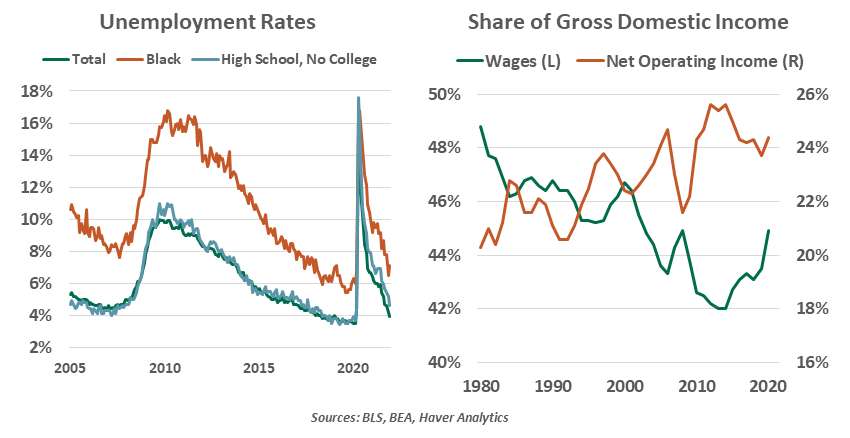

When evaluating whether a situation is good or bad, we often use our most recent experience as an anchor. And it’s a lofty comparison in this case. Stretching over ten years, payrolls grew by 22.7 million during the last expansion. The unemployment rate fell from a peak of 10% in 2009, holding at or below 4% for two years prior to the pandemic.

The labor market recovery was broad-based, reaching every potential worker. The labor force participation rate of workers over 65 climbed by two percentage points in the two years leading up to the COVID-19 crisis, representing 1.7 million workers. Minorities also benefitted from the last recovery: the Black unemployment rate fell from 16.8% in 2009 to below 6% in 2019. Jobs were available to just about everyone who wanted one.

Full employment can be a mixed blessing, though. Tight labor markets can pressure wages and inflation. But fears of inflation never came to be. Nonsupervisory wage gains throughout the last cycle were tepid, averaging only 2.4% annually during the last decade. This was well below the norms of prior cycles, and provided further evidence that firms had significant leverage over the workforce, even at full employment. The wage share of gross domestic income has fallen steadily from its peak in 1970, as worker protections have faded and globalization and automation have reduced the costs of labor.

COVID-19 shutdowns sent those promising labor market charts right off a cliff. In two painful months, 22 million jobs went away. The unemployment rate reached a modern record of 14.8%. Fortunately, the recovery began in short order; but nearly two years on, the labor market that has emerged is not the same one that existed prior to the pandemic. Its size is smaller, and its members have retaken the upper hand.

|

The post-pandemic labor force is smaller, and its members have regained the upper hand. |

The established experience of recessions is that people try to get back to work as soon as possible, in any job available. In this cycle, however, many workers have been in no hurry to return; as of December, payrolls remain 3.6 million jobs shy of where they stood in February 2020.

This recovery cycle broke from past experiences with its elevated level of demand. Government intervention and adaptive work arrangements allowed most people to maintain their incomes and rebuild their savings. As a result, demand for workers has been elevated. Wages are rising, especially among lower-wage workers. Year-ago debates about whether to raise the national minimum wage now seem quaint, as small and large employers alike advertise generous starting pay and incentives to attract new hires.

These conditions are dramatically different from those that prevailed just two years ago. Below, we analyze several of the drivers that have left a lasting mark on the labor market.

The Great Retirement

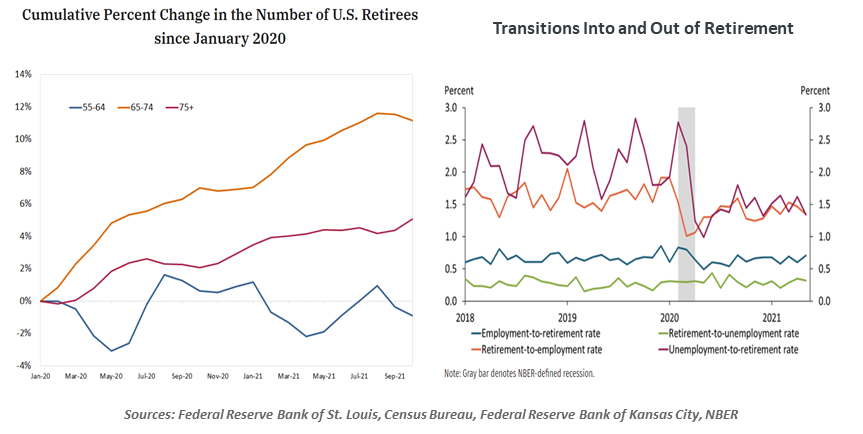

The United States has been in the midst of a secular retirement boom since the beginning of the century. At that point, the post-war generation began reaching ages at which work became more optional; many had benefitted from the sustained bull market, which gave them the resources to leave the labor force before the age of 65. Economists have estimated that labor force participation has been falling by 0.3% every year recently simply because of changes in the nation’s age profile.

Prior to the pandemic, however, the strong labor market was leading many workers to postpone retirement. Opportunities were ample, and many roles could be performed well by more senior workers. Labor force participation among those over the age of 55 had increased from 32.5% in 2000 to 40.4% in early 2020.

COVID-19 rudely interrupted this trend. Older people have been at much greater risk of contracting the virus, requiring hospitalization, and losing their lives to the virus. Those who have survived infection are more likely to experience lengthy recoveries.

|

3.3 million people report that they have retired since the pandemic began. |

For more senior Americans, the prospect of returning to crowded work environments has not seemed appealing; at the same time, the loss of social interaction from remote work diminished the value many derive from employment. Strong financial markets strengthened many household balance sheets, reducing the urgency of rejoining the labor force.

According to the Census Bureau’s Current Population Survey, 3.3 million people have retired since the pandemic began. The Federal Reserve Bank of St. Louis estimates that this total is about 2.4 million in excess of what would have been expected based on demographics alone. The vast majority of these individuals are over the age of 65.

Retirement is not a permanent state for everyone. A certain percentage of retirees go back to work every year, but the rates at which this occurs have been declining during the pandemic.

Many of those now retired are still young enough to work. And as we discussed last summer, some may reach a point later this year when they need to return to work. Better wages and reduced health risks should invite some recovery in labor supply, but getting those people placed may take time. The longer someone is out of work and the older they are, the more that their networks and skills atrophy.

In sum, “The Great Retirement” may be a more permanent development than previously thought. And that will continue making labor markets tighter.

Prime-Aged Participation

Many Americans who are in their prime working years have not taken jobs since being displaced by the pandemic. The number of employed people between the ages of 25 and 54 has declined by almost two million since the beginning of 2020. About half of those people have left the labor force.

There are a host of reasons that people have stepped away from working. In most cases, we expect these workers to find their way back to employment.

The pandemic and its consequences are keeping some workers away. Fear of contracting COVID-19, especially among immune-compromised workers, should fade as the virus becomes better controlled. We are more concerned about the developing story of “long COVID,” in which patients take a long time to recover from their infections. One study estimates over a million jobs may be unfilled today due to long COVID complications. As time passes and treatments improve, we hope to see more of these impaired workers make a full return to productive work.

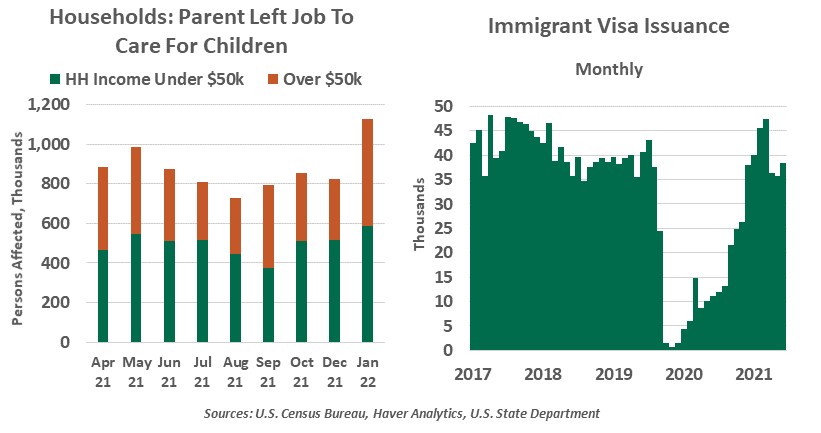

Family obligations have also been a challenge during the pandemic. Child care has been a complication: Over 13 million households have children under age six. Many day care centers closed during the pandemic and have been slow to reopen, with staffing an acute challenge.

Even after the children are of school age, their ability to attend school is not as certain as it once was. Quarantines and remote learning are still common. Despite widespread efforts to stay open, over 7,000 schools experienced disruptions amid the recent Omicron surge. A conventional job may simply not fit with the demands currently placed on families, or be deemed unworthy of the effort and risk. This challenge will remedy itself if only for the simple reason that children grow older and become more self-sufficient, giving parents more autonomy.

Adults can be demanding, as well. Those suffering COVID-19 may need the assistance of their spouses or adult children to cope with the disease. The Census Bureau estimates nearly nine million people missed work in January because they or their family members were sick with COVID-19. As cases recede, availability to work will improve.

|

Those providing care to family members during the pandemic should be able to return to working at some point. |

Gig work or small freelance jobs are a transition before workers find more formal employment. Small business formation has been robust during the pandemic; during their infancy, new firms are not well covered by the formal employment metrics. We may see greater evidence of returns to work through this avenue in the quarters ahead.

Immigration also fell off in the pandemic as nations justifiably closed their borders to limit contagion. The U.S. has been left with a substantial backlog of willing entrants who remain in their home countries, impairing hiring. Immigrant visa issuances are returning to their pre-pandemic levels, but a substantial backlog remains, complicated by ongoing shutdowns at local consulates.

Apart from COVID concerns, financial considerations will dictate when and whether prime-aged workers return. As savings cushions deplete, workers will find their way back into the workforce.

A European View

Tighter job markets aren’t confined to the United States. Economic recovery is being constrained by worker shortages in other parts of the world.

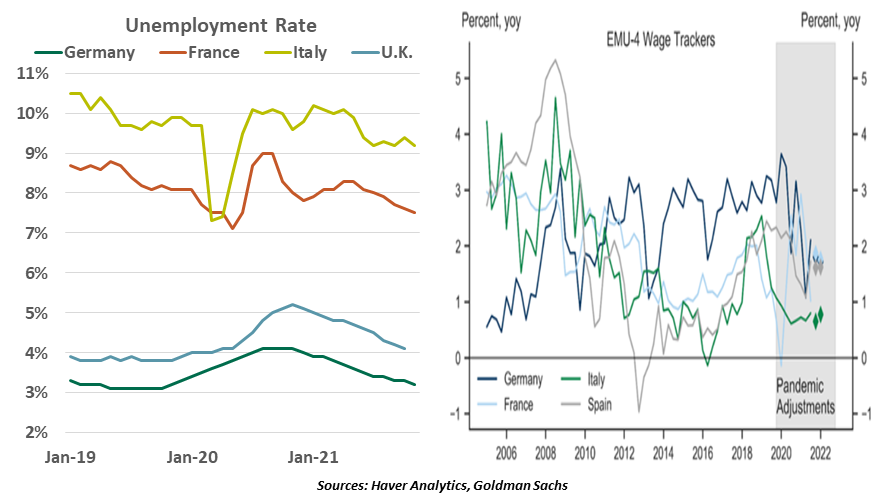

The European labor markets appear to be about as tight as they were before the pandemic. After the 2008 financial crisis, unemployment in the eurozone rose for four years. By contrast, joblessness has fallen closer to an all-time low of 7.1% in the past year.

Most European economies adopted short-time work and furlough schemes, which provide benefits to employers that retain and pay staff while businesses were impaired. Maintaining these links avoids the challenge presented by job searches and sustains worker skill sets and networks. This led to relatively small increases in unemployment during the pandemic.

By contrast, nations such as the U.S., Ireland and Canada, which relied on unemployment benefits, saw bigger increases in unemployment rates at the peak of the pandemic shock. This suggests that furlough schemes were potentially a more effective policy tool to preserve the employer–worker relationship.

Still, the continent is facing record-breaking numbers of vacancies and worker shortages. According to a survey by the European Commission, labor shortages are limiting production more than ever. British businesses endured an increasing number of voluntary resignations in 2021, and there are currently 1.2 million job openings in the U.K.

Higher pay, quality of life, border closures, and skill mismatches have been among the key factors behind higher quits and shortages in Europe. Travel restrictions have disrupted the flow of seasonal and migrant workers. Central European economies are close to full employment, with wages growing, creating scarcities of truck drivers, meat packers and hospitality staff in countries like Germany and the U.K.

|

Europe’s labor markets are tight, but wage growth has been subdued. |

Despite widespread reports of worker shortages, wage growth in Europe has remained subdued. There are two important reasons for this. Firstly, the level of pandemic stimulus provided by European governments was significantly smaller than it was in the United States. A good portion of the euro area’s pandemic relief program has yet to be disbursed, so aggregate demand is nowhere near as strong. In addition, the eurozone has seen an increase in participation for workers 55 years or over, the opposite of what has been seen in the U.S. Weaker demand and stronger supply mean reduced pressure on wages.

As a final element, European culture and law create much better balance between the interests of firms and labor. The opportunity to regain leverage, which has been a powerful driver for U.S. workers, is not as strong on the other side of the Atlantic.

While there are elements in common between U.S. and European labor markets, they have reached very different equilibria.

Long-Term Implications

Even the temporary absence of so many American workers from the labor force has had a profound impact on wage growth. As firms report very strong pricing power, increased personnel costs are being passed along to consumers. As we discussed last fall, the potential for a wage-price feedback loop is increasing.

Should recent departures prove more permanent, it will diminish growth in the labor force, which has also been challenged by falling birthrates, reduced immigration (even prior to COVID-19) and damage done by the pandemic. This will limit potential growth in the economy, which is critical to increases in standards of living, market performance, and debt sustainability.

Labor market developments have surprised us at several points in the past two years: some have been positive, others have not. Hopefully, better public health news in the months ahead will allow many more people to get back to work. That would be a very welcome outcome, on many levels.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All