The surge of the coronavirus omicron variant has implications not only for broader asset-class allocations but also for macro exposures within asset classes. We believe that modestly capping exposure to certain COVID-19-sensitive assets can enhance risk management.

It’s been quite a challenge for investors to manage portfolio risk in the pandemic era. Sudden twists and turns in the public-health trajectory of COVID-19 have had wide-ranging effects on the global economy, prospects for individual asset classes, industries and companies, and portfolios.

The omicron variant is the latest disruptor, following on the heels of the initial coronavirus outbreak and delta variant—each outbreak bringing uncertainty and sizable downside risks in the near term. One approach to tackling these risks is to dial exposures to risk assets up or down.

However, that’s a fairly blunt tool, because asset classes aren’t monolithic. The pandemic’s impact varies greatly within equity, fixed income, commodities and currencies, and the sensitivities cut both ways: some market segments benefit when outbreaks force mobility restrictions, while others suffer.

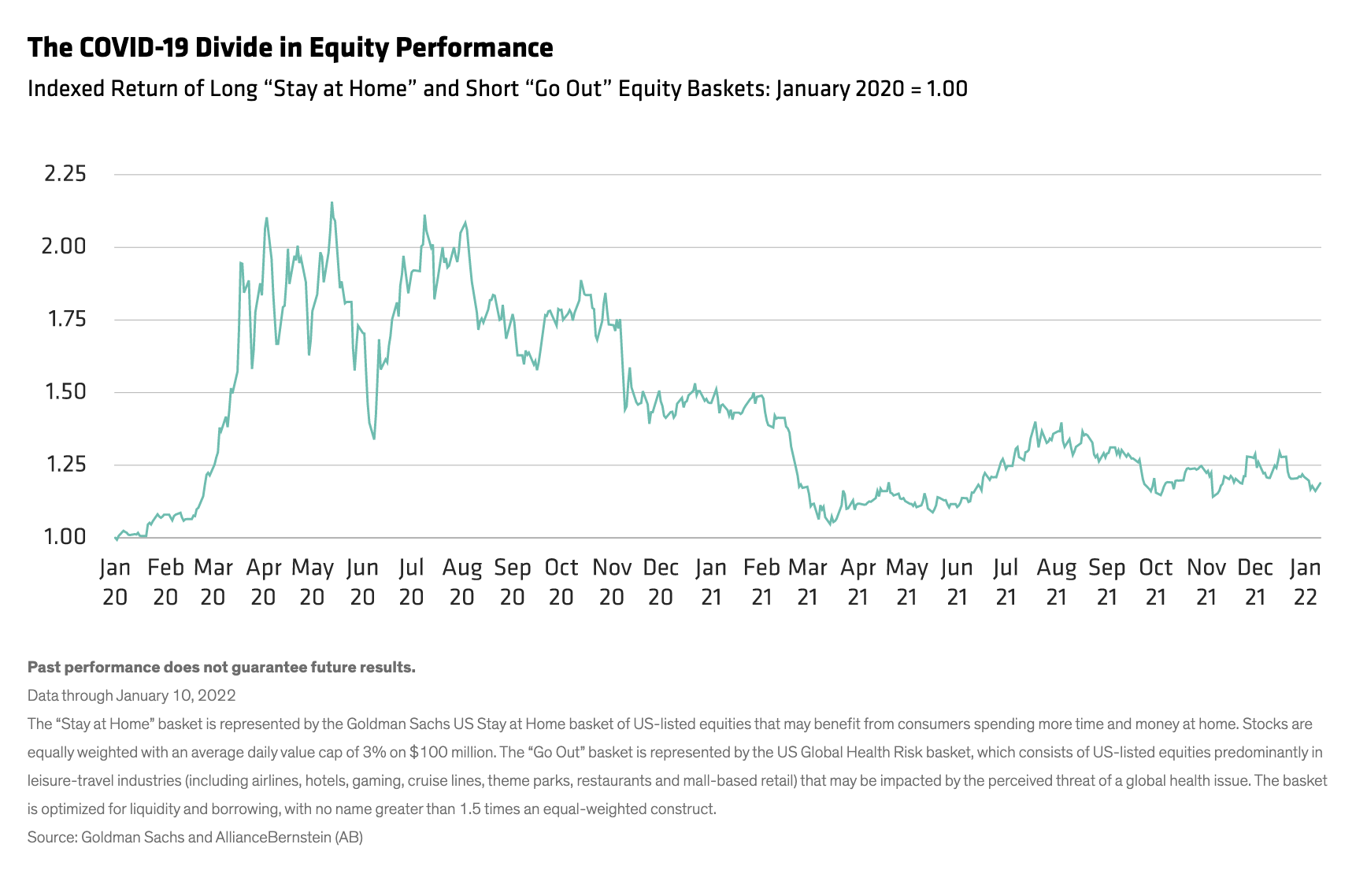

This performance divide is visible in US equity markets by comparing a “stay at home” stock basket and a “go out” stock basket.

Stay-at-home stocks, which have benefited during COVID-19 outbreaks, include issuers such as at-home entertainment firms and remote work enablers. Go-out issuers, which have fared well as activity recovers, include resorts and airlines. A combined long position in stay-at-home stocks and short position in go-out stocks (Display) rallied during both the initial outbreak, which started in February 2020, and the delta variant outbreak, which first surfaced in August 2021.

Past performance does not guarantee future results.Data through January 10, 2022

The “Stay at Home” basket is represented by the Goldman Sachs US Stay at Home basket of US-listed equities that may benefit from consumers spending more time and money at home. Stocks are equally weighted with an average daily value cap of 3% on $100 million. The “Go Out” basket is represented by the US Global Health Risk basket, which consists of US-listed equities predominantly in leisure-travel industries (including airlines, hotels, gaming, cruise lines, theme parks, restaurants and mall-based retail) that may be impacted by the perceived threat of a global health issue. The basket is optimized for liquidity and borrowing, with no name greater than 1.5 times an equal-weighted construct.

Source: Goldman Sachs and AllianceBernstein (AB)

Identifying COVID-19-Sensitive Assets in the Macro Landscape

There’s been plenty of analysis focused on the winners and losers from COVID-19 among individual issuers, but we’ve seen little coverage of the sensitivity of macro assets, such as equity and government-bond country indices, currencies and commodities, to global pandemic risk.

By evaluating the performance patterns of different segments of equity, fixed-income, commodity and currency markets, we think it’s possible to isolate assets with more directional sensitivity—both positive and negative—to COVID-19 outbreaks. Oil and oil-sensitive assets, for example, struggled as reduced oil demand undermined prices. A lack of agricultural workers, on the other hand, pushed prices for those products up, benefiting agricultural commodities. Safe haven currencies, such as the US dollar, rallied as investors fled riskier assets.

Some assets behaved in ways that defied a clear label. The pound sterling, for example, lost ground in the initial COVID-19-related wave but rose slightly during the delta variant outbreak. Other influences played roles too. The Hong Kong dollar was also affected by heightened tensions with China over the same time frame, making it harder to discern the influence of the pandemic alone.

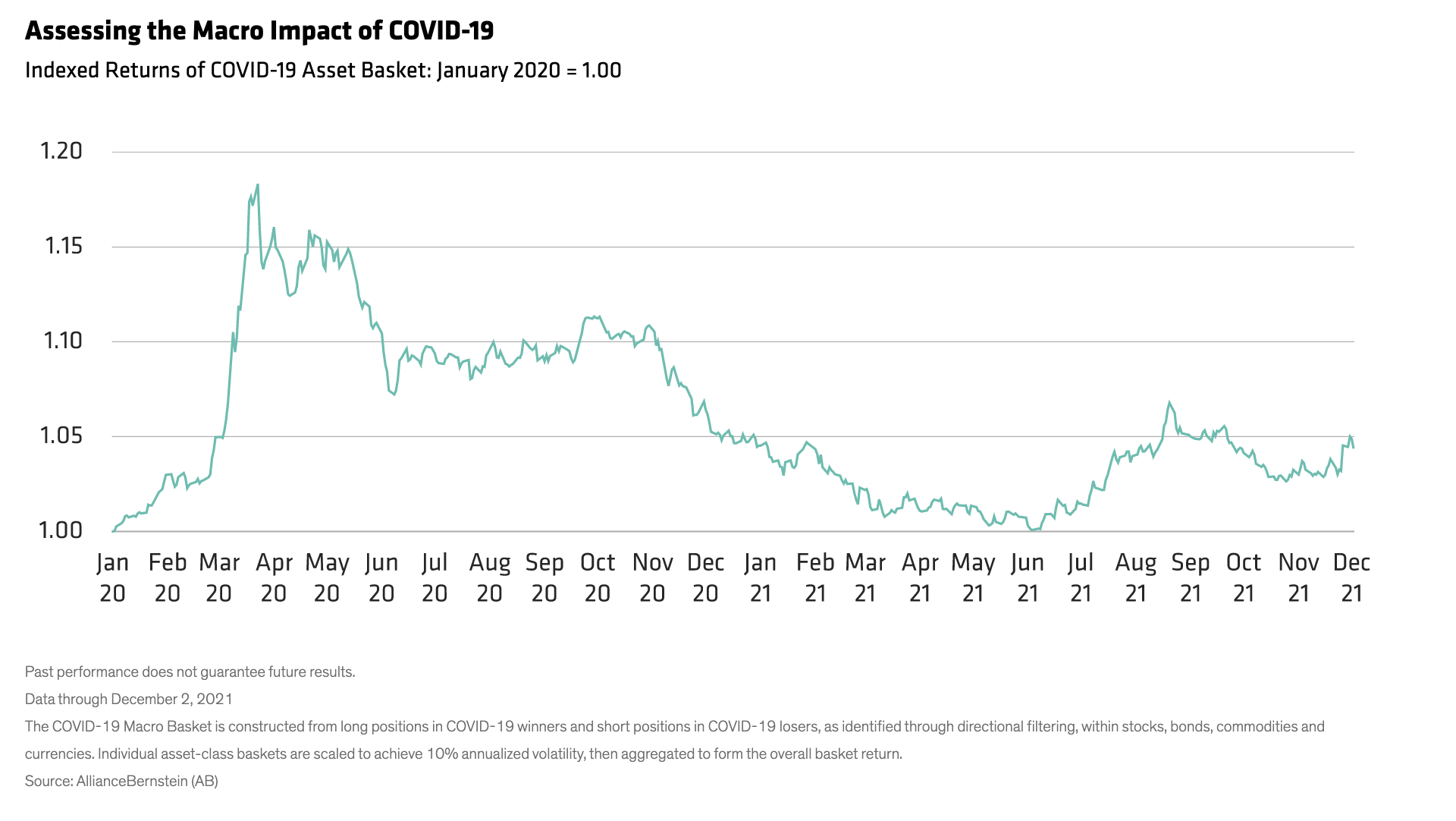

A broad basket of some 40 or so asset segments, with long positions in winners from COVID-19 outbreaks and short positions in COVID-19 losers (Display), clearly gains from the early 2020 initial outbreak and the mid-2021 delta variant outbreak. It also rises to a lesser extent during the outbreak of the omicron variant, which has so far been more transmissible but generally less disruptive.

Past performance does not guarantee future results.

Data through December 2, 2021

The COVID-19 Macro Basket is constructed from long positions in COVID-19 winners and short positions in COVID-19 losers, as identified through directional filtering, within stocks, bonds, commodities and currencies. Individual asset-class baskets are scaled to achieve 10% annualized volatility, then aggregated to form the overall basket return.

Source: AllianceBernstein (AB)

Capping Exposures to Moderate Portfolio Risk

Informed by this basket, investors can cushion portfolios against COVID-19-outbreak tail risks in a more targeted way than a general risk-off, risk-on switch. The key mechanism is placing limits on allocations to COVID-19-sensitive assets. The limits would be one-directional—aimed at capping exposures in the direction that would magnify portfolio risk.

Let’s use industrial issuers as an example. These companies have generally suffered during COVID-19 outbreaks, when economic activity broadly slows down. So it makes sense to limit the portfolio’s ability to overweight industrials exposure, which could increase risk. The Swiss franc, on the other hand, has rallied during the previous two COVID-19 outbreaks. To moderate risk, it’s logical to cap the portfolio’s ability to underweight the Swiss franc.

These allocation limits should be relatively modest, complementing other portfolio risk-control measures. They’re also not without cost, so they’re not intended to be permanent fixtures. The natural next question is: In a pandemic that’s been anything but predictable, how would an investor know when—and how—to remove these risk guardrails?

When Is Coronavirus Variant Protection No Longer Needed?

Given COVID-19’s unpredictable public-health trajectory, the best approach seems to be adjusting these asset limitations in stages—and based on a broad dashboard of indicators. These signals include the evolving public-health picture, market-based signals and fundamental judgment.

On the public-health front, trends in virus cases, hospitalizations, critical patients and other pandemic effects would be part of the mix. From a market lens, the amount of COVID-19 risk priced into assets should be considered, so the performance of the various COVID-19 baskets should be monitored closely. And as shown earlier, fundamental interpretation and judgment are vital in interpreting signals.

Two previous COVID-19 outbreaks—and part of a third—are a relatively small historical sample, which is one reason allocation limits should be modest. Assets may behave unexpectedly and nonpandemic factors can affect returns too. However, while this may not be a perfect solution, we think it has the potential to improve on a large-scale risk-off shift during outbreaks—whether they’re related to omicron or the next variant.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein