Every year, we hope for a calm return to work in January after a refreshing break over the December holidays. For the second year in a row, our plans were foiled.

The challenges of COVID-19, tangled supply chains, and tight labor markets have carried over into the new year. The persistence of these factors has prompted increasing anxiety at the Federal Reserve, which has been sending clear signals that policy tightening is fast approaching. Multiple rate hikes are in store.

Our base expectation remains for the year to return to normal: cooler inflation, steadier growth, and stable employment. Rates above the zero lower bound are a component of a normal economy, but they are coming sooner than we had anticipated.

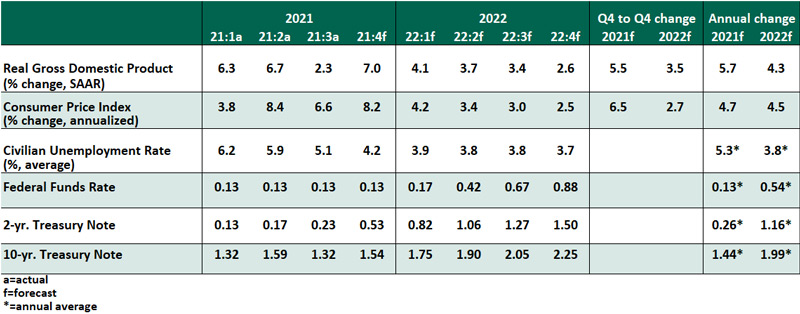

Key Economic Indicators

Influences on the Forecast

- Messaging from the Federal Reserve since our December U.S. Economic Outlook has set clear expectations for earlier and more significant action.

- At its December meeting, the Federal Open Market Committee (FOMC) accelerated the taper of its asset purchases. Bond buying is now on track to conclude in March, advancing from the original trajectory of ending in June.

- The FOMC’s quarterly Summary of Economic Projections showed all members expect a rate liftoff in 2022. Opinions range from one to four hikes of 25 basis points this year, with more to follow in 2023 and 2024. We expect to see the first post-pandemic interest rate increase in March, with two others to follow later this year. Overnight borrowing costs will reach the pre-pandemic range of 1.25%-1.50% by the middle of next year.

- Later in 2022, we expect the Fed to begin reducing its balance sheet. Minutes of the December meeting showed an active discussion of when this process should start and how quickly it should proceed. The Fed’s portfolio could be unwound quickly if needed, as $1.1 trillion (20%) of its Treasury assets will mature within one year.

- The employment recovery continues. In December, the unemployment rate fell further to 3.9%, a startling improvement of two percentage points in just six months. Combined with upward revisions to payrolls, the economy is closer to full employment that initially understood, giving further urgency for the Fed to act. Total payrolls remain 3.6 million below their pre-pandemic peak, but not all workers can be expected to return.

- Inflation remains elevated, with the December consumer price index showing prices grew 7.0% from a year before. On a monthly basis, prices increased 0.5%, an encouragingly slower rate than seen in October (0.9%) and November (0.8%). The latest release showed price increases were broad-based, and pandemic-affected sectors like travel and automobiles continue to show high readings. While we expect inflation to cool, lower readings will not come soon enough for the Fed to stay patient, reinforcing the case for more rapid action.

- The Omicron variant is spreading rapidly, but economic activity has carried on. Policy restrictions on activity have been limited, with little appetite for any return to shutdowns or significant precautions. January is typically a slow month for discretionary spending, a well-timed coincidence. We are encouraged by results showing Omicron infections are typically less severe than the outcomes of past variants; in the best-case scenario, mass exposure now will set the stage for a year of less worry about contracting the virus.

- Supply chain constraints have hopefully passed their peak. The December Purchasing Managers Index showed an improvement in supplier delivery times, inventory backlogs and prices paid for both manufacturing and services sectors. Fears of an undersupply of holiday gifts did not reach their worst potential outcomes. The greatest economic risk is to production in China, where policymakers have held firm to a zero-COVID policy of quarantines and shutdowns to manage the virus.

- While much focus is on the Fed’s next actions, the legislative outlook for 2022 is much quieter than it was for the past few years. Temporary COVID stimulus programs have ended, and the collapse of Build Back Better (BBB) negotiations suggests an end to ambitious spending programs, though a subset of BBB proposals could be revived. The government remains funded on a continuing resolution into February, which can be continued again, and the debt limit has been raised to an extent that will avoid worry until 2023.