Understanding General Obligation Municipal Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGiven all the municipal bonds to choose from, how do you decide which ones should make up the core of your portfolio? With $3.9 trillion of muni debt outstanding1 spread among tens of thousands of issuers, the choice may seem daunting, but we’ll help you break it down.

Municipal bonds are sold by local and state governments to help fund public projects or municipal government operations, like building new schools or repairing city sewer systems. Their interest payments are usually exempt from federal income taxes, and may be exempt from state income taxes if the bond issuer is located in the investor’s home state. For these reasons munis are often attractive to income-oriented investors in higher tax brackets looking to reduce income tax bills.

Munis can generally be classified into two camps—general obligation bonds and revenue bonds. General obligation, or GO, bonds are often backed by the general revenue of the issuing municipality, while revenue bonds are supported by a specific revenue source, such as revenue from a toll road.

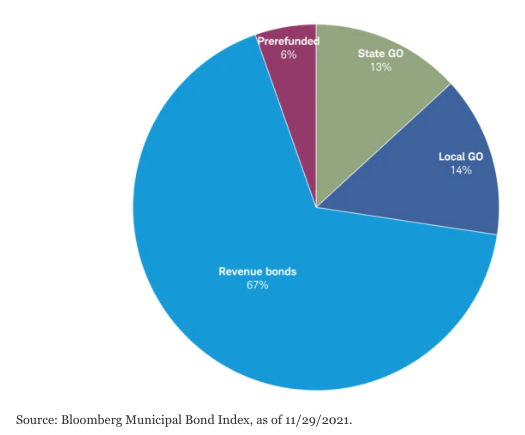

In this article, we’ll focus on GO bonds. They account for 27% of the investment-grade muni market and are usually backed by the taxing authority of the bond issuer. Most states and local governments issue GO bonds to help fund operations or specific projects. The dollar value of GOs issued by states compared to local governments is roughly equal, even though there are fewer states than local governments. In other words, the amount of debt issued per state is much larger than the amount of debt issued per local government.

General obligation bonds make up about a quarter of the muni market

The market’s perception of GOs has changed

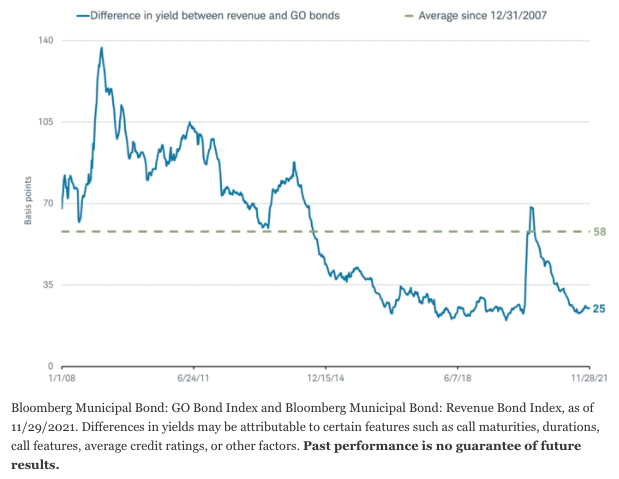

Although general obligation bonds account for only about a quarter of the muni bond market, they tend to get the most attention. Historically, GO bonds were considered the more secure of the two options, because they are often backed by the full faith and credit of the municipal government. Given GO bonds’ perceived security advantage, revenue bonds used to yield more than GO bonds on average—but that has changed in recent years, as illustrated in the chart below. The change can be partly attributed to Detroit’s bankruptcy in 2013. Initially, Detroit tried to treat its GO bondholders as “unsecured” creditors,2 which would have gone against the market’s longstanding belief of the security pledge of GOs. Detroit’s bankruptcy was settled outside the court, so there was no legal opinion on its security pledge. The result was that muni market participants began to scrutinize GO bonds more closely.

Revenue bonds used to yield much more than GO bonds

There are different types of general obligation bonds

A common mistake some municipal bond investors make is assuming that any general obligation bond issued by a state or local government is backed by the same pledge. Since the yield on the average GO bond has moved closer to the yield on the average revenue bond, it’s especially important today to understand the different credit pledges on GO bonds. The most common types of GO bonds issued are:

- GOs backed by a dedicated tax pledge as well as unlimited taxing authority

- GOs backed by unlimited taxing authority, with no dedicated tax

- GOs backed by limited taxing authority

These three types are listed in order from generally the strongest to the weakest, in terms of their financial pledges.

1. Unlimited tax GO, with dedicated tax

These bonds are often backed by a dedicated tax—usually property tax—that the municipality collects. Frequently, these bonds are also backed by a pledge that the issuer will use all other available revenue sources, such as other taxes or state support, if the taxes specifically authorized to repay the bonds aren't sufficient.

In California, for example, school districts often issue bonds backed by a property tax dedicated specifically to debt service on the bonds. Voters within the school district must agree to the tax, and the dedicated property tax cannot be mixed with the school's other revenues. If the school district doesn't have the necessary funds to pay the bonds, it typically must increase property taxes to meet the amount due. In our view, this is one of the strongest security pledges for municipal bonds.

2. Unlimited tax GO, with no dedicated tax

These bonds are backed by the general revenues of an issuer, including taxes. Unlike dedicated tax GOs, however, they do not have a specific tax pledged to repay them. Instead, bondholders are paid from general revenues, and if those prove insufficient to cover debt service, the issuer typically must raise taxes. In our view, this is a very strong pledge.

3. Limited tax GO

Like unlimited tax GOs, these bonds are backed by the general revenues of an issuer, including taxes. However, the issuer doesn't have the ability to increase taxes by an unlimited amount to pay the bonds back. The limit on the amount of tax increase allowed is generally described in the bond offering statement, and the bonds are clearly labeled. Although we believe this is still a strong pledge, the limit on the tax lessens the security of the bonds.

Investors can find the bond’s pledge by reviewing the official statement on Schwab.com or the EMMA (Electronic Municipal Market Access) website. A fixed income specialist can also assist, as official statements can be long and cumbersome.

GO bonds tend to be highly rated and usually pay interest and principal on time

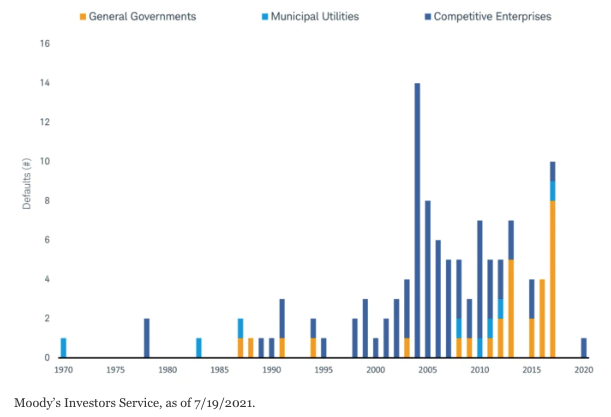

With high-profile cases like Detroit’s bankruptcy and Puerto Rico’s effective bankruptcy in 2017, it may seem like GOs frequently default—but that’s not the case. It may also seem like the COVID-19 crisis devastated the finances of many state and local governments and caused an increase in defaults, but that’s also not the case. As illustrated in the chart below, defaults are rare in the muni market and even rarer for general governments, which include GO bonds. In fact, only one issuer that Moody’s rates defaulted in 2020. Although the financial issues caused by COVID-19 will likely linger and will be an added credit pressure for state and local governments, we expect defaults to continue to be rare.

General governments, which include GO bonds, have rarely defaulted historically

What investors can consider now

Given the financial pressures that COVID-19 is creating for some municipal governments, we think it’s especially important today to know what is backing your municipal bond and how to combine different muni bond types to build a well-diversified portfolio.

General obligation bonds, in combination with other essential service revenue bonds, can serve as the core of a muni portfolio. First, focus on higher rated issuers—those rated AA-/Aa3 or above. More speculative investors looking for higher interest income could consider no more than 30% in lower rated issuers—those rated between BBB-/Baa3 and A+/A1. As one would expect, a lower-rated bond has a much greater chance of default than one with higher ratings.

If you’re a Schwab client investing in municipal bonds through mutual funds or exchange-traded funds (ETFs), you can find the ratings distribution and breakdown of GO and revenue bonds on the “Portfolio” tab on Schwab.com. For help in selecting municipal bond investments that are right for your personal situation, consider reaching out to a Schwab Fixed Income Specialist.

1 Bloomberg, as of 11/30/2021.

2 City of Detroit Proposal for Creditors, as of 6/14/2019.

Important Disclosures:

Investors should consider carefully information contained in the prospectus or, if available, the summary prospectus, including investment objectives, risks, charges, and expenses. Please read it carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(1221-1C9P)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All