Despite a moderate pick-up in growth during Q4, the leading indicators of the economic growth cycle suggest we are nearing a period of stagflation and potentially disinflation as growth resumes in deceleration. For 2022, the culmination of peaking inflation, peaking liquidity conditions and peak growth, brought on by rising prices, falling real incomes, the fiscal cliff, stronger dollar and rising rates could usher in a period of disinflation whereby both economic growth and inflation decelerate in tandem. A continued shift from cyclical to defensive assets and equity sectors ought to serve investors well over the medium term.

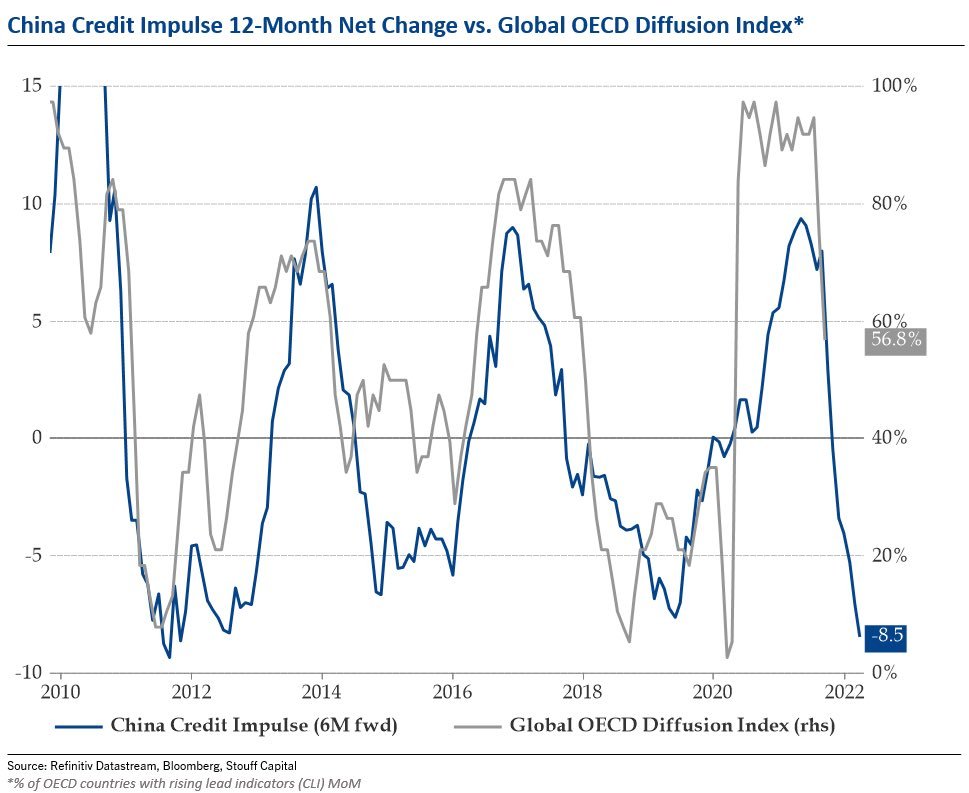

Beginning with the long leading indicators, they have for some time been telling us that 2022 will be very different from what we experienced during 2021. The Chinese credit impulse leads the growth cycle by around twelve months, given China’s role as one of the primary drivers of world growth. The credit impulse metric measures the rate of change of newly created credit via commercial bank lending and government stimulus. This peaked in early-to-mid 2021.

Source: Julien Bittel, Stouff Capital

Such a deceleration in credit creation should begin to be reflected in realised growth and asset prices potentially as early as the first half of 2022. Prometheus Research, who forecast the growth cycle via systematic modelling and NowCasting are projecting the deceleration of growth to be pronounced in 2022, as we can see below.

Source: Prometheus Research

Confirming this message are the liquidity conditions. Liquidity is another excellent long-term leading indicator for both the growth cycle and asset markets and is similar to the credit impulse. Whilst still accommodative for now, liquidity has well and truly peaked and should transition into realised growth and asset market performance sometime in the first half of 2022.

Source: Prometheus Research

Another measure of liquidity and long leading indicator is the Marshallian K, which compares the ratio of the money supply (M2) relative to GDP. This metric peaked in early 2021 and again leads the growth cycle by around 12 months.

An accelerated taping by the Fed brought forward due to continued inflationary pressures is likely to only worsen liquidity conditions in 2022. That however, remains a story for 2022.

Turning now to housing and construction, housing permits are well below their April 2021 peak on an annual growth rate perspective.

A reduction in building permits is indicative of slowing growth in housing and construction as building permits precede the construction of new housing and indicate lessening demand, they are also impacted by various cyclical factors such as disposable income and interest rates. Given housing’s importance to the economy, building permits do a solid job forecasting the housing market.

From a consumer perspective, higher prices continue to impact both the demand for goods as well as real income. The University of Michigan Consumer Buying Intentions Survey for vehicles, houses and household goods all remain near their lowest levels in years. Though the survey data for housing and vehicles appears to have slightly ticked upward over the past couple of months, indicative of the small bounce in growth we have experienced during Q4.

Source: Acheron Insights, University of Michigan

Indeed, looking at the growth of real disposable income per capita and real disposable income excluding transfer receipts (i.e. ex-stimulus), the former remains in negative territory in a year-over-year basis whilst the latter continues to decelerate.

Disposable income is struggling to outpace inflation, particularly when government stimulus is removed from the equation. Indeed, on an absolute basis, real disposable income per capital is beginning to fall below the pre-COVID trend. As stimulus fades and the fiscal cliff approaches, it appears as though one of the primary drivers of real growth over the past 18 months is dissipating.

This is particularly worrisome when assessing how far the labor force participation rate is from its pre-COVID levels. Though the labor market may be tight and wages on the rise, any positive growth impact from rising wages is being offset via a shrinking labor force.

It is not just inflation that is eating away at incomes but interest costs too. Mortgage costs are over 30% higher than where they were 12 months ago.

Higher interest costs and higher costs in general is damaging unless offset by rising real income. If real incomes continue to decline, demand will likely continue to follow suit and with it consumption.

From a shorter-term perspective, the short leading indicators did pick up the growth bounce seen in Q4. How long this continues remains to be seen, but, as I will detail below, the markets appear to no longer be pricing in much of a continued bounce through the outperformance of cyclical assets. Ideally, we would need to see the consensus of the short leads pick up materially to confirm this view. Whilst the long leads give as a guide of what could occur over the next six to twelve months, the short leads provide confirmation of cyclical turning points, particularly when used in conjunction with asset market data.

Firstly, the Economic Cycle Research Institute (ECRI) Weekly Leading Index did turn up in October. Should this index continue to accelerate on a rate of change basis, we could see this growth bounce continue to surprise to the upside throughout the next couple of months and into the first quarter of 2022.

Source: Economic Cycle Research (ECRI)

Again, confirming the growth bounce was Citibank’s economic surprises index, which has picked up into positive territory over recent weeks, though perhaps somewhat of a function of Q3 growth being lower than expected.

Source: SentimenTrader, Citigroup

The shorter leads of the manufacturing sector however appear to be confirming the notion of the longer leading indicators that a deceleration of growth is set to continue and the growth bounce is nearing exhaustion.

The US ISM survey’s Manufacturing New Orders index provides a timely insight as to the demand for manufacturing. This survey just reported its lowest reading in over a year.

US ISM Manufacturing New Orders Index

Source: Institute of Supply Management, Investing.com

Confirming this is the US Census Bureau’s reporting of manufacturing new orders, both in consumer durables and total manufacturing. The Census Bureau data peaked in April 2021 on a growth basis and has been decelerating since.

The manufacturing sales to inventory ratio too continues to decelerate, per the US Census Bureau manufacturing data. When sales are rising at a greater pace than sales and the ratio rises, then more inventory needs to be produced, thus putting upward pressure on prices, as well as an increased need for workers and hours worked, positive for growth. When inventories rise at a greater pace then sales and the ratio falls, the inverse occurs.

After peaking in May on a growth basis and again spiking in October, industrial commodities and metals are decelerating, confirming the manufacturing data above. Industrial commodities are more closely linked to the growth cycle than energy and agricultural commodities. A continued decline in the acceleration of growth in industrial commodities is suggestive that a Q4 bounce in growth is only temporary.

Forecasting growth from a data driven perspective is only half the story however, we must take heed of what financial markets are doing and whether they are pricing in continued growth or slowing growth.

Firstly, the various iterations of the yield curve are by and large trending lower. Clearly, the shorter curves (such as the 5s/3ms and 10s/3ms) are rising to reflect the impending monetary tightening. However, the longer iterations of the yield curve are continuing to trend lower, as the bond market continues to price in slowing growth and slowing inflation for 2022. We are not seeing any real form of curve steepening whereby longer-term rates rise faster than short-term rates, indicative of higher growth and inflation expectations. Particularly notable is the 10s/2s spread recently breaking down to new cyclical lows.

After pricing in the growth bounce in late September to early October, the pro-growth sectors and style factors have largely underperformed during November.

Meanwhile, the anti-inflation asset classes appear to be rebounding from their underperformance over recent months, whereby inflation continued to accelerate to the upside. This market shift could well be signaling peak inflation.

The currency markets too are by and large indicating a continued slowdown in growth, as the pro-cyclical currencies are largely heading lower. This is particularly pronounced in emerging markets, whereby US dollar strength wreaks havoc as foreign debt costs rise with the dollar.

The dollar itself has been on a tear lately, with the dollar index up nearly 9% over the past six or so months. Fortunately, it looks as though we may be in for a reprieve over the next month or two as a dollar correction or consolidation is well over due. Should this occur, such a scenario would be supportive of a Santa Claus rally in risk-assets and a potential continued growth bounce into early Q1 2022.

The dollar recently triggered a weekly DeMark 9 sell count, and is entering overbought territory.

Dollar seasonality is supportive of this view, as December is historically the worst month for the dollar.

Lacy Hunt refers to the currency markets as the most forward-looking of all markets, and a higher dollar indicative of a weakening economy. Should this hold true, we should expect to see a resumption in growth deceleration at some point during the first half of 2022.

The bond market is certainly conveying this message, with the 30-year yield at a critical point and threatening to break lower, though we could see a bounce off this resistance level and a retest of the descending trendline before a break lower, which would again be supportive of risk assets over the next couple of months.

The bond market tends to get these things right; we saw yields peak in early Q2 this year as growth peaked before turning lower and again rebounding in late September/early October amid the recent bounce in growth. This is a chart investors should be keeping a close eye on.

What’s more, if we look at positioning in the futures market, speculators (i.e. the dumb money) have on their shortest bond positions since early 2020, whilst hedgers (i.e. the smart money) are currently net-long at a level not seen since early 2019 when long-term bonds rallied nearly 50% over the next 12 months. Historically, rates have struggled to move much higher in such circumstances.

Additionally, the long-term chart of the stocks-to-bonds ratio is at the upper end of its decade long channel and is looking like bonds are ready to outperform. I don’t believe we will see such relative outperformance of bonds to the extent we reach the lower bound of this channel, but this chart is suggestive of some level of bond outperformance in the next year or so when interpreted in conjunction to that which I have detailed throughout this article.

Summary

In summary, it appears as though we may be heading towards an inflection point in early 2022 whereby we begin to see the rate of growth continue its deceleration to the downside. Whether inflation follows suit remains to be seen, though my base case in the direction of change in inflation could surprise to the upside again in December and perhaps even January as the owners’ equivalent rent (roughly 25% of the CPI basket) continues its inflationary tailwind, before unfavorable base effects and the slowing of demand and consumption alleviates the persistent supply chain pressures in the first half of 2022.

Should we see both growth and inflation begin decelerate in tandem on a rate of change basis, risk assets will no longer be the place to have the majority of one’s capital. Until then, it may be prudent for investors to slowly transition from the high-beta, cyclical, short-duration asset classes and sectors that perform will in a pro-growth, pro-inflation environment, and rotate into their defensive counterparts over the coming months.