Newsletter - November 2021

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAS I GET OLDER I REALIZE:

● I talk to myself because sometimes I need expert advice.

● The biggest lie I tell myself is, “I don’t need to write that down, I’ll remember it.”

● When I was a child, I thought nap time was punishment. Now it’s like a mini vacation.

● The day the world runs out of wine is just too terrible to think about.

● Even duct tape can’t fix stupid, but it can muffle the sound.

● “Getting Lucky” means walking into a room and remembering why I’m there.

ALWAYS HAPPY TO BE IN GOOD COMPANY

JPMorgan chief executive officer Jamie Dimon said, "I personally think that bitcoin is worthless…I don’t think you should smoke cigarettes either."

THIS IS A CLASSIC!!!

Watch Who’s on First? HERE.

A GOOD GIG

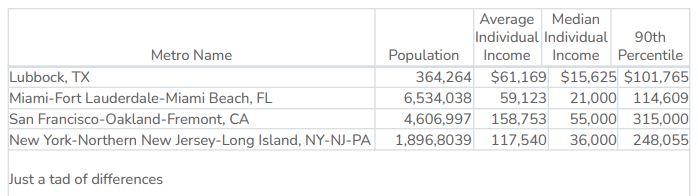

Top 5 Highest paid CEOs in financial services in 2021

I wonder where all this money comes from?

WHO ARE THEY?

SAME SONG SECOND VERSE

(Actually, more like the 10 zillionth verse)

Using Dividends For Retirement Income And Capital Preservation, Lawrence DePaulis is a broker with UBS Financial Services Inc.

Heading into retirement, one of the most important issues to address is how to best structure clients' investment portfolios to provide the income needed for everyday expenses. This is a time when outperforming a market benchmark becomes less important than maximizing the probability that clients' income will last throughout the remainder of their life. There are many ways to approach this transition from growth to income, and one of many possible strategies is to construct an equity income portfolio and live off the dividends.

Doesn’t seem to matter how many times I beat this drum, focusing on dividends and not total return is looking at the trees and missing the forest. Maximizing risk adjusted, after tax and expenses, total return along with an intelligent cash flow strategy is the best way to “maximizing the probability that clients' income will last throughout the remainder of their life.”

Below is the total return of a few representative large “dividend” funds compared to the Russell 3000 along with some measures of cost, risk adjusted return and tax efficiency (or lack thereof).

FEQTX – Fidelity Equity Income (0.43%/0.64/2.06) NOBL – ProShares S&P 500 Dividend Aristocrats (the only ETF focusing on a rare breed of companies within the S&P 500 that have raised their dividends for at least 25 consecutive years) (0.35%/0.69/0.84)

IWV – iShares Russell 3000 ETF (0.15%/1.02/0.51)

(Expense ratio/Sharpe ratio/Tax cost ratio) Expense ratio is the % of your annual return going to pay the brokerage firm (if any) and fund management.

Sharpe ratio is a measure of risk adjusted return, i.e. your return per unit of risk – the higher the better.

Tax cost ratio in the percentage of your annual return going to taxes.

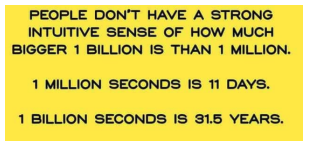

INTERESTING STATISTICS

From my friend Monty

WISE WORDS

From my partner Michael

INFLATION HEDGE? NOT!

Gold as an Inflation Hedge: What the Past 50 Years Teaches Us from the WSJ

On the anniversary of the metal’s unleashing by Nixon, gold’s believers may be disappointed by the record.

On a Sunday evening 50 years ago—on Aug. 15, 1971, to be exact—then-President Nixon interrupted “Bonanza,” one of the most popular TV shows of that era, to announce that he was ending the convertibility of the U.S. dollar into gold.

“Gold is only a good inflation hedge over time frames far longer than any of our investment horizons, according to research conducted by Duke University professor Campbell Harvey and Claude Erb, a former commodities portfolio manager at TCW Group. They found that it’s only when measured over very long periods—a century or more—that gold has done a relatively good job maintaining its purchasing power. Over shorter periods its real, or inflation-adjusted, price fluctuates no less than that of any other asset.”

Gold as an Inflation Hedge: What the Past 50 Years Teaches Us

YEP, I’M OFFICIALLY OLDER THAN DIRT (17 of 17)

PERSPECTIVE

2 NEW BUY ALERTS WITH 8% DIVIDEND YIELD AND HIGH UPSIDE

More of the “same song.” I’m constantly amazed that these high current return stories never seem to end but they don’t.

I’ll give the writer credit for laying out the risk; however, I’m still in the “total return” camp. It doesn’t matter what your current dividend is, what matters is what the dividend is along with the growth (or loss) of the underlying investment. I can guarantee you an 8% annual return for almost 13 years. Problem is at the end of the term your investment is ZERO!

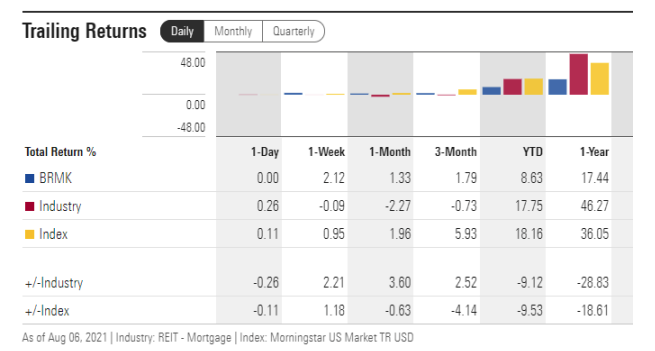

Broadmark Realty Capital (BRMK)

Mortgage REITs don't buy properties to rent them out. Instead, they lend money to other real estate investors in order to earn interest income.

These REITs fell out of favor at the onset of the crisis because the memories of mass defaults in 2008-2009 continue to haunt them.

To be fair, this is a risky sector with common issues regarding overleverage, loan defaults, and management misalignment. Some mortgage REITs deserve to trade at lower levels given these risks, but a few opportunities stand out.

BRMK is one of them.

With a total return strategy, you’d have had a far better outcome with a whole lot less risk investing in the broad market.

Omega Healthcare Investors (OHI)

Omega Healthcare Investors is a REIT that specializes in skilled nursing properties.

It is feared by the market because skilled nursing facilities have been on government life-support over the past year.

The pandemic disrupted them by killing patients and delaying or cancelling move-ins. Operators were running on thin margins prior to the pandemic so you can imagine that 2020 and 2021 are very rough years for them.

Therefore, OHI is at high risk of suffering lease defaults from tenants that simply cannot afford to pay rent anymore… Why would you then want to buy OHI?

Simply because we think that (1) the pain is already priced in, (2) it is mostly temporary, and finally, (3) the rapidly aging population is a strong long-term tailwind…

Omega’s much longer history is more impressive but with a total return strategy you’d also have had a better outcome with less risk.

2 New Buy Alerts With 8% Dividend Yield And High Upside

I WAS A SOPHOMORE

2 STOCKS THAT COULD TURN $200,000 INTO $1,000,000 IN 10 YEARS

If you're looking for excellent stocks to buy and hold through the next decade, here are two that could turn $200,000 into $1,000,000 (that's a compound annual growth rate of about 17.5%) in the next 10 years: Abbott Laboratories (NYSE:ABT) and Match Group (NASDAQ:MTCH). Let's see why both are worth adding to your portfolio.

17 ½% is a pretty ambitious goal but I guess anything is possible. It seems Abbott has a long way to go but Match certainly did it in the past. Of course, the returns during the short period from 3-5 years must have been most impressive. Needless to say, I believe chasing the pot of gold at the end of the rainbow has a high probability of delivering a pot of poo, keep an eye out for my NewsLetter in 10 years and I’ll report back.

2 Stocks That Could Turn $200,000 Into $1,000,000 in 10 Years

NOW THERE’S A STRATEGY I DIDN’T KNOW ABOUT

Thirty-two percent of investors in a new survey from MagnifyMoney acknowledged that they have bought or sold an investment while intoxicated, including 59% of Gen Zers.

Seventy-one percent of respondents who make their own investments said they have made a regrettable decision, compared with 59% of those who take a more hands-off approach. [I’m shocked.]

Nearly a Third of Investors Cop to Trading While Drunk: Survey Think Advisor

HEDGING YOUR BETS

Blue Skies Unless It’s Cloudy

San Francisco Chronicle

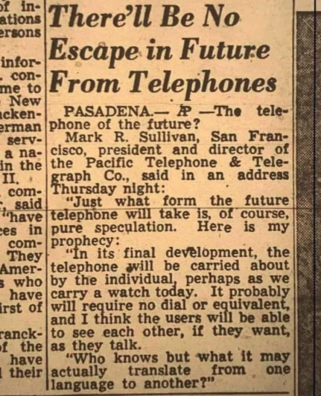

WISH I HAD HIS CRYSTAL BALL

April 11, 1953

ONE MORE GREAT OPPORTUNITY

This Incredible Dividend Grower Will Yield 9% (Buy Now)

Covered-call funds’ higher cash returns make them a go-to in a stormy market. But when markets grind higher, as they are these days, we can often find ourselves an out-of-favor covered-call fund trading at a nice discount, and with a healthy dividend, too.

Consider the BlackRock Enhanced Global Dividend Trust (BOE), which holds top US blue chips like Microsoft (MSFT), Texas Instruments (TXN), UnitedHealth Group (UNH) and Visa (V). About 60% of the portfolio is in the US.

Below is a comparison to the IOO, an iShare (also owned by Blackrock) Global 100. I used it as BOE is about ½ domestic and ½ international.

These “amazing” investments must be the ones selected by MagnifyMoney “strategy.”

This Incredible Dividend Grower Will Yield 9% (Buy Now) (forbes.com).

AGING WISDOM

From my “little” brother (He’s a lot taller than me.)

● My doctor asked if anyone in my family suffered from mental illness. I said, "No, we all seem to enjoy it.”

● My bucket list: keep breathing. ● Camping: where you spend a small fortune to live like a homeless person.

● Just once, I want a username and password prompt to say, "Close enough."

● I'm a multitasker. I can listen, ignore and forget all at the same time!

● Retirement to do list: Wake up. Nailed it!

● Went to an antique auction and people were bidding on me.

● People who wonder if the glass is half empty or half full, miss the point. The glass is refillable.

● I don't have grey hair; I have wisdom highlights.

● Sometimes it takes me all day to get nothing done.

● I don't trip, I do random gravity checks.

● My heart says chocolate and wine, but my jeans say, please, please, please eat a salad!

● Never laugh at your spouse's choices. You are one of them.

● One minute you're young and fun. The next, you're turning down the car stereo to see better. ●

I'd grow my own food if only I could find bacon seeds.

● Losing weight doesn't seem to be working for me, so from now I'm going to concentrate on getting taller.

● My body is a temple; ancient and crumbling.

● Common sense is not a gift. It's a punishment because you have to deal with everyone else who doesn't have it.

● I came. I saw. I forgot what I was doing. Retraced my steps. Got lost on the way back. Now I have no idea what's going on. But, I remembered to send this to you.

JUST REMEMBER

Hindsight is 20/20

“Never miss another market movement!

Never miss a critical market update with:

● The latest news on-the-go

● Portfolio updates wherever you are

● Real time alerts on new market analysis”

A pitch for a market app. At least it’s free.

CLICK HERE

MORE “HINDSIGHT IS 20/20”

Or maybe comparing “Apples to Elephants”

From my friend Prof. Taft

Wall Street ignores these ‘orphan’ stocks, but they’ve beaten the S&P 500 over 20 years

Comparing the performance of an individual stock to the broad market is nonsense, also known as “cherry picking.”

And, don’t know about the 20 year, but the 15 year is impressive. Unfortunately, that’s yesterday’s news. The recent five year and three year is a bit less impressive. In fact, the three year is really depressing.

What can I say. Financial pornography sells papers. For pornography I’d prefer Playboy.

46 OUT OF 50, NOT BAD FOR OLDER THAN DIRT

I missed dancing in the rain, jumping out of a plane [but still on my bucket list], riding an elephant and a tattoo (but it’s not too late).

FINANCIAL PORNOGRAPHY SEEMS ENDEMIC

I'm Doubling Down On These 2 Rich 8% Dividends

● Capital gains are nice for the future, but dividend-paying stocks provide income security for the present.

● I highlight 2 high dividend names that provide both income and capital gain potential.

These stories never seem to end. Never have figured out why investors just buy headlines and never look below the surface. Capital gains along with dividends (total return) provide “security” for the present and the future.

Omega, one of the author’s top picks looks a tad better than the industry average but abysmal compared to a simple, broadly based investment alternative.

I'm Doubling Down On These 2 Rich 8% Dividends Seeking Alpha

WE DIDN’T MAKE #1 BUT #6 ISN’T BAD

More Than One-Fourth Of America’s 400 Richest Went To One Of These 12 Colleges

#6 Cornell University Forbes 400 Members: 9 (Harvard was #1 with 15 members)

Unfortunately, I didn’t make the Cornell list.

More Than One-Fourth Of America's 400 Richest Went To One Of These 12 Colleges (forbes.com)

HELLO HAROLD

I’ve been on this Total Return soap box so long I thought I’d include a chapter from my small book Hello Harold (free on Amazon - https://www.amazon.com/Hello-Harold-Veteran-Financial-Investor-ebook/dp/B019G0SSJ4)

Chapter 10

Real Cash Flow:

A Fix for the Fixed Income

Andrew Jacobs (AJ): Hello, Harold. May I call you Harold?

Harold Evensky: I guess it depends. Who are you and how did you end up in my office?

CJ: My name is Andrew Jacobs. I’m a wholesaler for the Special Income Portfolio.

HE: Andrew, I have to ask you this: how did you get past the receptionist? I don’t normally take cold meetings with mutual fund wholesalers or fund salespeople. I prefer to speak to them after I’ve done my own preliminary analysis.

CJ: Actually, I waited until your receptionist was distracted by another guest, and then I crawled along the floor until I reached the hallway and slipped past the doors of your other coworkers as soon as they turned their heads away from the door.

HE: That’s quite remarkable. All right, Ninja wholesaler, now that you’re here, have a seat. What can I do for you?

CJ: I’m here to convince you to recommend the Special Income Portfolio to all of your clients. I even brought some golf balls as a nice gift to get the conversation started.

HE: You can keep the golf balls. Just tell me the facts about your fund. This could turn into a very quick visit.

CJ: It’s an income fund. Some of your clients are retired, aren’t they?

HE: Yes, they are.

CJ: And they need income from their investments to supplement their pension and Social Security to support their lifestyle. By the way, if you don’t play golf, I brought candy. Or maybe you’re interested in one of these cute little jump drives with our company’s logo on it.

HE: My retired clients need cash flow from their investments to supplement their other income sources, and I don’t want or need candy or one of those jump drives.

CJ: Well, the Special Income Portfolio is carefully designed to give your clients exactly what they need in the form of dividends and interest. It’s invested in companies that pay high dividends and bonds that pay high income. I have a little form you can fill out so you can start moving your clients’ assets over right away—

HE: Hold on a minute. You just hit one of my hot buttons. Maybe you should sit back and relax. This could take longer than either of us expected.

CJ: What do you mean?

HE: I have to confess that I’ve got a lot of pet peeves about the kind of nonsense that gets foisted on the public as good investment advice. But one of my biggest is what I call the myth of dividends and interest. CJ: I can assure you that our portfolio manager doesn’t invest in myths.

HE: What you’re saying probably sounds plausible to 99 percent of the investing public. Of course, many investors need cash flow from their portfolio. So you put the words income fund in the name of a mutual fund, and it sounds exactly like what people need.

CJ: It is what people need.

HE: I disagree. We plan for a lot more than a fixed income. We plan for a consistent real income.

CJ: I’m not sure I follow you.

HE: I’ll make it easy. Does the carton of milk you bought last week, your last doctor’s visit, or your last new car cost more than it did five, ten, or fifteen years ago?

CJ: Of course.

HE: And do you think all those things and everything else will cost more in the next twenty to thirty years?

CJ: Probably lots more.

HE: Today’s dollar isn’t what it used to be and tomorrow it won’t be worth what it is today. Do you agree? Don’t you think you and I and everyone else will need more of those greenbacks in the future just to hold our own?

CJ: Yes, I suppose we will.

HE: How long have you been doing this work as a wholesaler?

CJ: Oh, I have weeks of experience. I know my way around, let me assure you.

HE: Somewhere in your sales training, you heard that professionals use the term real dollars to mean an amount of money that will buy the same goods and services (milk, doctor’s visits, and cars) in the future as it will today. A real dollar means the same purchasing power going forward.

CJ: I think I have that somewhere in my notes, yes. But I think you’re missing the point. When someone retires, he or she needs a fixed income.

HE: What horsepucky!

CJ: Excuse me?

HE: Dangerous advice like that really infuriates me. If people plan a retirement based on a fixed income, they had better be planning on changing their diet from steaks to cat food throughout the balance of their lifetime. What retirees need is an income that will increase every year by the inflation rate. Other than winning the lottery, that’s the only way people can maintain their standard of living.

CJ: We also have a lottery fund that invests in a diversified portfolio of state lottery tickets that I could show you—

HE: Let’s go back to deciding what kind of investments my clients need to make in order to supplement their pension and Social Security income. Suppose they buy into this myth you’re selling and construct an “income” portfolio.

CJ: Great idea! That’s exactly the fund I want to talk to you about.

HE: Now they have a portfolio bond/stock allocation that is largely fixed by design—inappropriate design. In almost all cases, it will cause an inferior portfolio for two reasons: Not only will the portfolio not allow them to accomplish their goals in real dollars, but it will also be inefficient.

CJ: Okay, I understand that you have objections.

HE: What do you mean?

CJ: The sales training said that I should overcome your objections, and the first step is to get your objections out in the open. So tell me your objections.

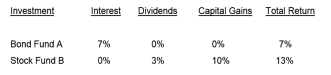

HE: With pleasure. In fact, I’ll draw you a picture. Here’s an example I use when discussing this issue with my clients. Consider a simple world in which you have only three investment choices—a money market, Bond Fund A, and Stock Fund B. In this world, the investments will provide exactly the returns I’m writing down in this simple table:

Does that look right?

CJ: It could be.

HE: Now suppose you’ve saved $200,000 for retirement and you need $14,000 a year from your savings to add to your Social Security and pension income. If you planned to get your needed $14,000 cash flow from dividends and interest, you would have to invest 100 percent in the Bond Fund. The reason is because, as you can see from this table I’m now drawing, the cash flow from Stock Fund B’s dividend payments is so low, any amount invested in stocks would drop your cash flow to an amount less than the $14,000 you need.

Bond A Cash Flow Stock B Cash Flow

Allocation from Bond Allocation from Stock Total Cash Flow

90 percent $12,600 10 percent $ 600 $13,200

50 percent $7,000 50 percent $3,000 $10,000

40 percent $5,600 60 percent $3,600 $9,200

CJ: Doesn’t that make my point?

HE: No. Because if you look at the future, then the purchasing power of that $14,000 starts to decline. Let’s say you’re retired, and I recommend the all Bond Fund. You might feel good today receiving the $14,000 you need; however, how would you feel ten years later if inflation had been 3 percent and your $14,000 only bought $10,417 worth of stuff?

CJ: I’d be calling my attorney to see if I had grounds for a lawsuit against you.

HE: And what happens twenty years later, when your diet has switched from steak to cat food, because that’s all you can afford?

CJ: I don’t like where this is going.

HE: I don’t want to give my clients fixed income when they need real income from a long-term portfolio that has an allocation to investments that are likely to rise in value and provide protection against inflation. In other words, I don’t want to guarantee that my clients will suffer losses in real-dollar terms. And that’s what you’re offering me.

CJ: Is that your objection?

HE: My objection is that investors do not need dividends or interest—they need real cash flow. So, they shouldn’t fall for this myth that you’re selling about dividends and interest. Now you can feel free to overcome my objections if you want. And please put those golf balls away.

CJ: Actually, I was wondering if I should move my money out of the fund.

HE: If you’re planning to live more than a couple of years, you might think about it.

CJ: Thanks, Harold. Thanks for the advice. Are you sure you don’t want one of these jump drives?

EVEN MORE OLDER THAN DIRT

MORE APPLES TO ELEPHANTS

Also from my friend Prof. Taft

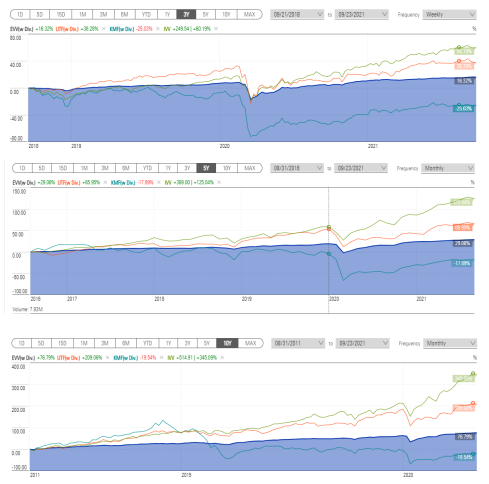

I like wines and my partner Taylor is a true wine connoisseur and sophisticated investor. I’m sure he makes wise wine investment decisions but for the novice investor there is so much wrong with this pitch it’s hard to know where to begin.

I’ll start with the graphs above. First the graph ends at 2018. Go figure. If you look at the return on the second graph from the 2012 highlight (I know it’s hard to read. It says “2012 –

Wine:2020% S&P 500 490% [for the last 20 years]”) Again, I don’t know why it ends in 2018 but you’ll notice that if you purchased in 2012 by 2018 you would have lost money compared to a nice return in the S&P 500. There is no information to calculate risk adjusted return but based on the graph I believe the wine investment statistics would not look too pretty.

Also, there is the “assurance” of “consistent returns.” As my friend Taft points out, if you look at the two graphs, they must have a different definition of “consistent.”

Finally, there is the question of cost. The standard fee is a stiff 2.85%. Unfortunately, there is no information on the cost (markup) on wines purchased. I “love” black box investments. Reminds me of the good old days of Limited Partnerships. I remember early in my career being pitched on a private placement real estate investment. In that case there was information available if you wanted to pour through a hundred pages of small print. I did and I saw that the property had been purchased for around $15,000,000 a month earlier and was valued in the partnership at $18,000,000. When I asked the wholesaler how that could be, he said “Don’t worry about it, your manager says it’s fine. Besides, we need to make money somewhere.” Wow, those were indeed the “good old days.”

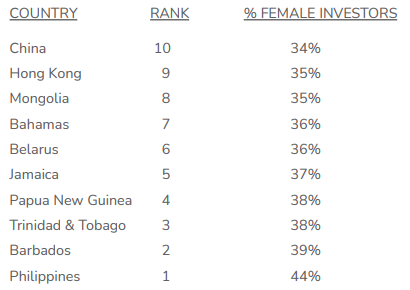

INTERESTING (AND SURPRISING) STATISTICS

10 countries with the most female investors

10 countries with the most female investors - InvestmentNews

MY NO-NONSENSE GUIDE TO RETIRING ON DIVIDENDS (WITH JUST $500K SAVED) - Forbes

“Do yourself a favor and shut out all the “experts” who say it’s impossible to retire on dividends alone. They’re just plain wrong! Because even today, with stocks soaring (and dividend yields in the tank), you absolutely can build a portfolio yielding a solid 7%+… Our first example is the BlackRock Enhanced International Dividend Trust (BGY)”.

“The portfolio is a laundry list of household-name (in their home markets) stocks like AstraZeneca PLC (AZN), Prudential PLC PBIP -0.6% (PUK), spirit maker Diageo PLC (DEO) and Canadian telecom Telus Corp. (TU).”

True, but you have to go way down the ownership list to find a name you might recognize. Here’s a list of the largest positions.

My No-Nonsense Guide To Retiring On Dividends (With Just $500K Saved) (forbes.com)

IT MIGHT BE TIME TO MOVE TO ETHIOPIA

Here’s How Much You Need To Earn To Be ‘Rich’ in 23 Major Countries Around the World

COUNTRY Annual Pre-Tax Income to be in the Top 10%

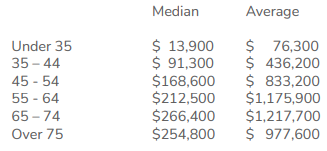

EVEN MORE INTERESTING STATISTICS

Average Net Worth of People Your Age

This Is The Average Net Worth Of People Your Age - 2021 (wealthgang.com)

I’M CLEARLY NOT VERY SOPHISTICATED

Take the Money and Run

Danish artist Jens Haaning was recently loaned approximately $84,000 to recreate two of his earlier artworks. However, Haaning has decided to use the cash to create a new artwork—by keeping the money for himself. He has given the piece the apt title: Take the Money and Run.

White on White

In the summer of 1951 Robert Rauschenberg created his revolutionary White Paintings at Black Mountain College, near Asheville, North Carolina. At a time when Abstract Expressionism was ascendant in New York, Rauschenberg's uninflected all-white surfaces eliminated gesture and denied all possibility of narrative or external reference. In his radical reduction of content as well as in his conception of the works as a series of modular shaped geometric canvases, Rauschenberg can be seen as presaging Minimalism by a decade.

Crazy

YOUR WARRANTY HAS EXPIRED!

THEY SAY A PICTURE IS WORTH A THOUSAND WORDS

I couldn’t resist adding just one more…..

This Dividend-Powered Plan Lets You Retire In 7 Years

Here’s the picture (Remember, Total Return) - IVV is the iShares S&P 500

The Dividend-Powered Plan Lets You Retire In 7 Years (forbes.com)

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz/Foldes Financial Wealth Management [“EK-FF]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from EK-FF. EK-FF is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the EK-FF’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.evensky.com. Please Remember: If you are a EK-FF client, please contact EK-FF, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your EK-FF account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your EK-FF accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, membership in any professional organization, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if EK-FF is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, EK-FF did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of EK-FF by any of its clients. ANY QUESTIONS: EK-FF’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits