In a recent post I opined how the stock markets internals are weakening, whilst also briefly touching on how a couple of leading economic growth indicators are beginning to roll over. Within this article, I intend to delve a little deeper into the various leading economic indicators to assess where we are in the current growth cycle and what this means for investors. As I discuss below, my reading of the current environment is relatively clear; both the longer-term and shorter-term leading growth indicators are pointing toward the heightened possibly of slowing cyclical growth. As a result, these downward trends suggest investors ought to be rotating out of the reflation and cyclical trades and into the defensive counterparts, or reducing risk entirely.

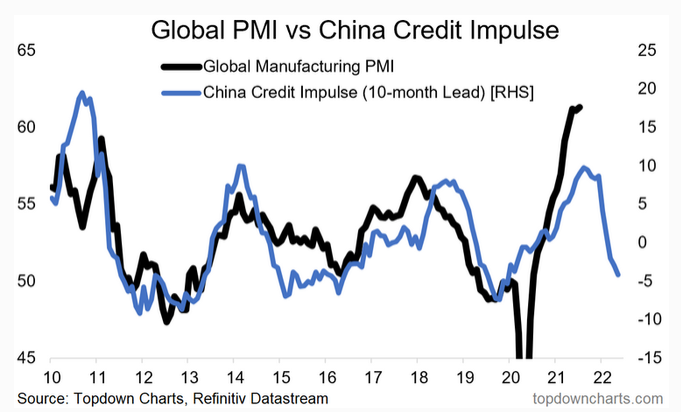

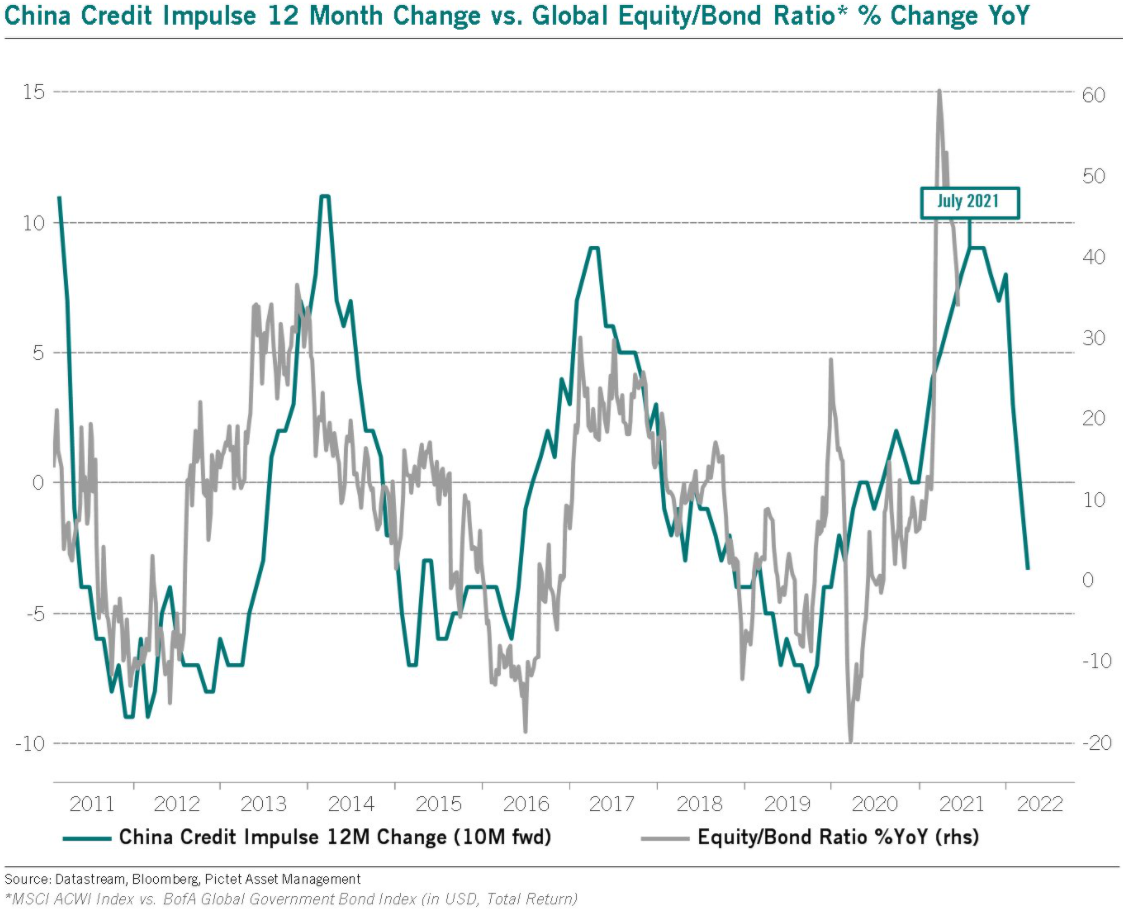

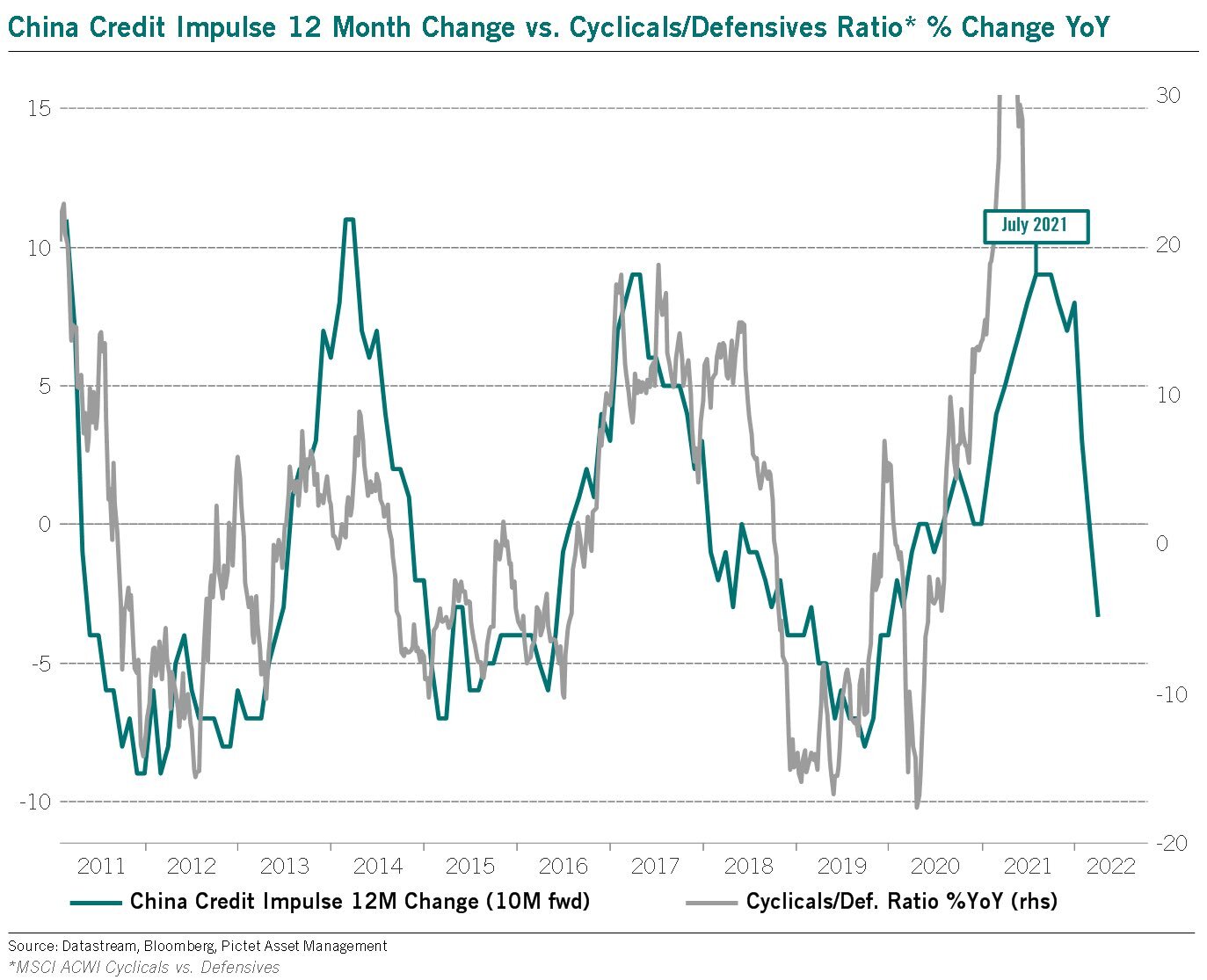

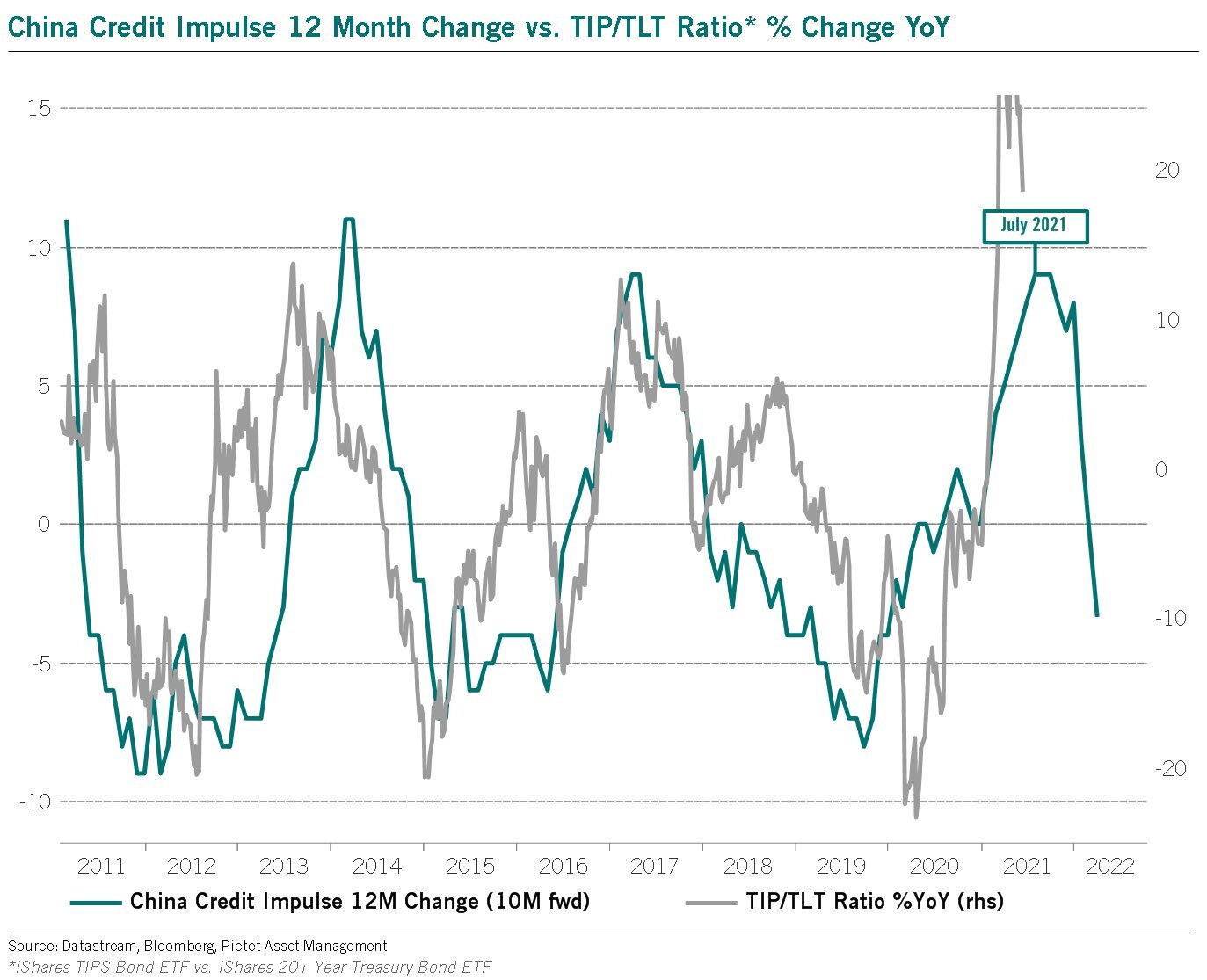

Beginning with the longer-term leading data, almost all of the variables I monitor peaked earlier this year and are now rolling over or trending downward. My favourite of which is the China credit impulse. Credit impulse measures the rate of change of new credit creation by both commercial banks and fiscal budget deficits. As it stands, credit creation is the truest measure of money creation and thus leads many economic variables by around 10-12 months. We can see the credit impulse from China peaked some months ago and has since turned negative. This is important as China remains the worlds largest manufacturer and drives much of the worlds business cycle.

Drilling deeper into the commercial bank credit creation process, we can see commercial bank lending on a year-over-year basis has been trending downward for the past 12 months and is now in negative territory.

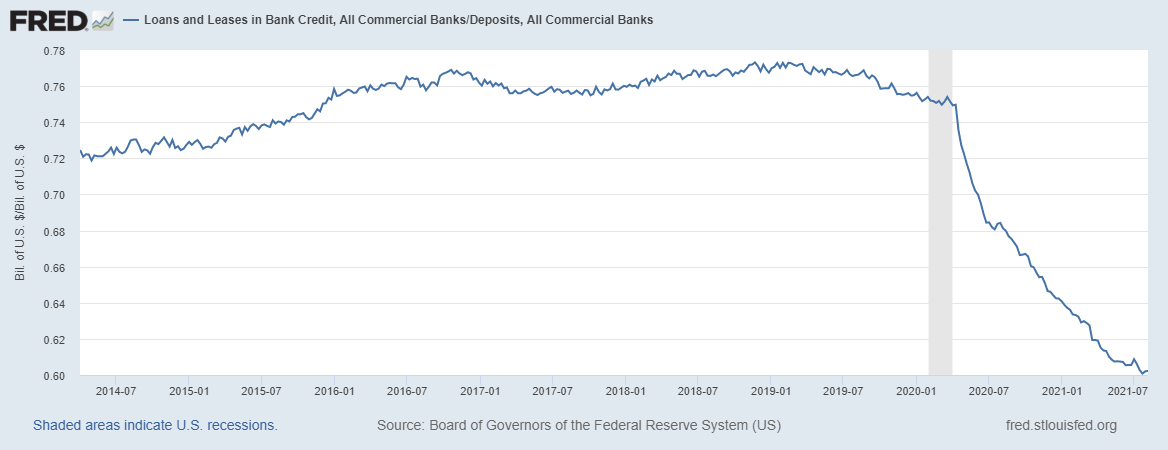

To me, despite the impending shift to fiscal dominance and central planning, credit growth in the private sector is still the best driver of the economy and is one of the more reliable indicators of long-term growth prospects. The fact that growth in private sector credit is now contracting is worrisome. We can extrapolate this further by analyzing the private sector loan-to-deposit ratio. A falling ratio indicates money is not leaving the banking system and being spent in the real economy, but instead remains trapped within the banking system. This ratio can be thought of almost as a proxy for the velocity of money. The loan-to-deposit ratio has been in a downward spiral ever since the COVID-19 crisis began.

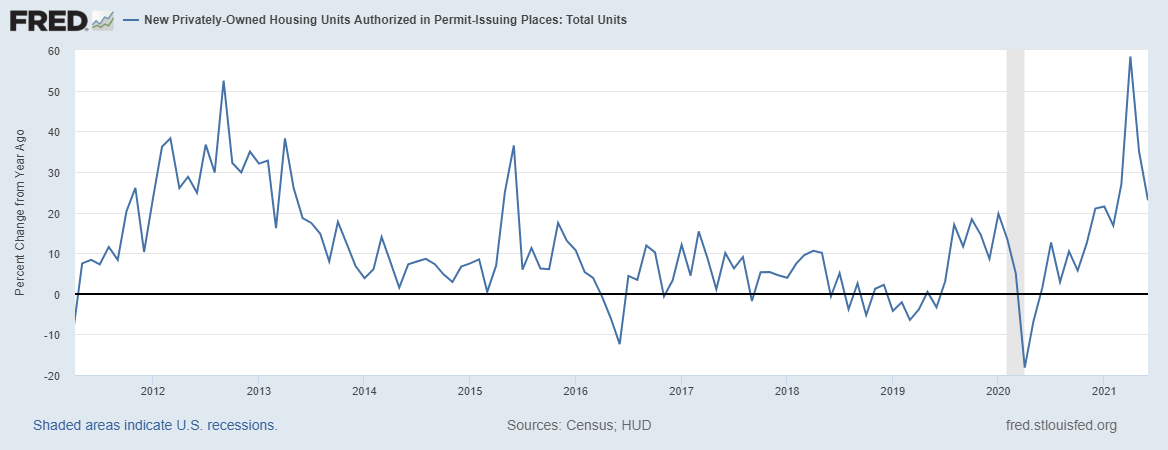

Confirming this trend in credit creation is building permits year-over-year rate of growth, which looks to have peaked. Like most assets, the housing market has been hot of late and if building permits are any guide, may be slowing down.

It is important to keep in mind however these long-term indicators are, by definition, long-term in nature, and thus for there to be any actionable asset allocation decisions to be made based on their readings, we need to see the shorter-term leading indicators confirming the trend.

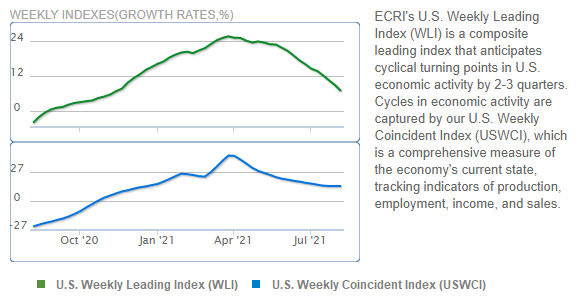

Of the shorter-term leading indicators, ECRI’s weekly leading index peaked back in April and has since rolled over. ECRI’s Lakshman Achuthan recently appeared on the MacroVoices podcast to discuss the implications of the weakening in their leading indicators.

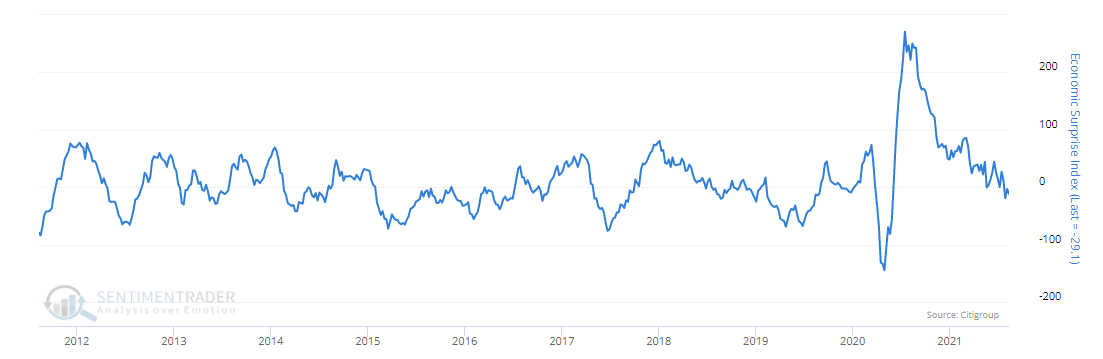

Citibank’s Economic Surprises Index, a measure of economic data coming out better or worse than expected has too recently turned negative, again signaling peak growth has passed and better than expected economic data is no more.

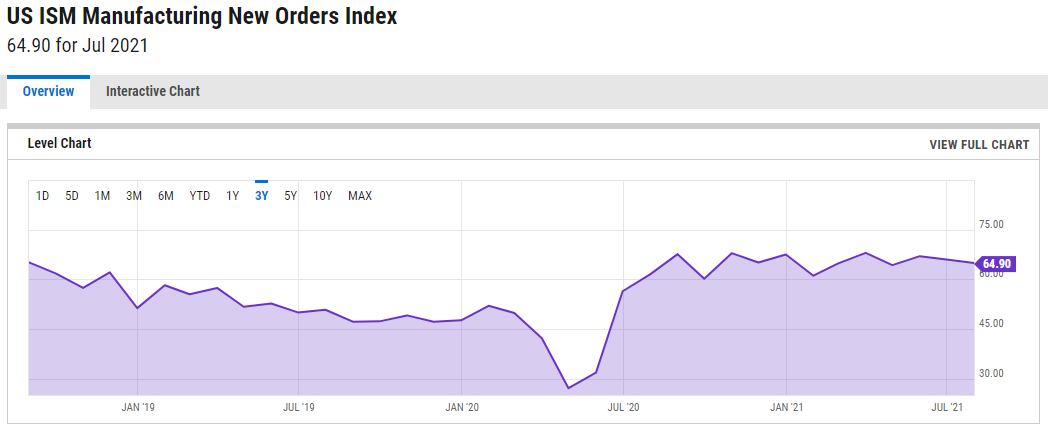

The manufacturing new orders subcomponent of the ISM Purchasing Managers Index (PMI) has flattened over the last new months, clearly signaling a slowdown in manufacturing demand.

Source: YCharts

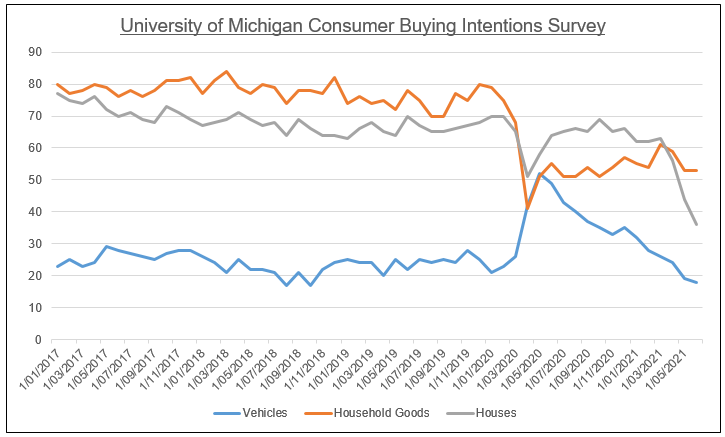

Meanwhile, the University of Michigan Consumer Buying Intentions Survey for vehicles, houses and household goods have all recently plummeted to their lowest levels in some time. Clearly, the spike in inflation over the past number of months is beginning to take its toll on consumers. Demand is waning not just in the manufacturing sector but in households too.

Source: Quandl, Acheron Insights

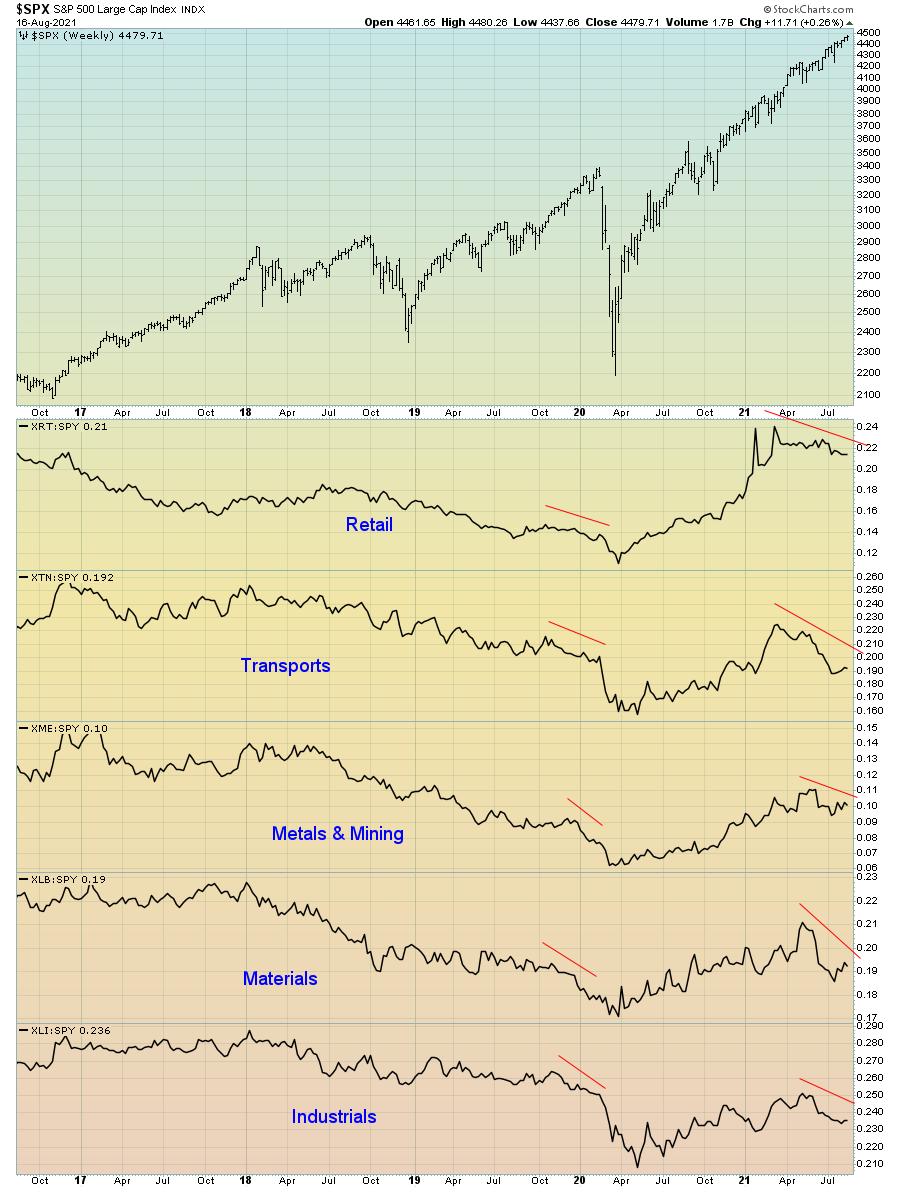

Turning now toward the financial markets, some of the most cyclically sensitive and economically sensitive stock market sectors have too been confirming this message of slowing growth. The retail, transports, metals and mining, materials and industrials sectors all peaked back in the March to April period and have been out of favour ever since. Investors appear to be pricing in this slower growth and taking profits in the reflation trade that has performed so well over the past 12 months.

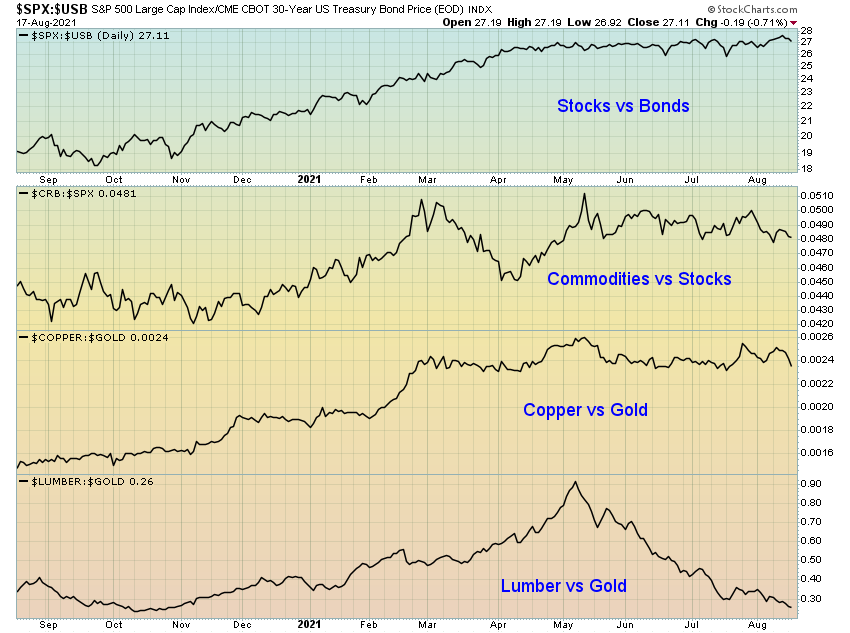

In addition to the stock market sectors confirming the downward trend in growth, we can see other market performance data is sending a similar message. Indeed, the performance of stocks relative to bonds, commodities relative to stocks, copper relative to gold and lumber relative to gold all peaked in the April to May period. Should growth continue in its current downward trend over the coming months as the leading data suggest it might, we should expect to see these relative market performance trends continue rolling over.

So, what matters then is the investment implications of a slowing economy. Firstly, it is important to remember the macro environment is inherently slow moving. Just because the long-term leading indicators suggest growth may slow in the coming quarters, unless the shorter-term leading and market data too confirm this message it can be costly to act prematurely. However, as I have endeavored to illustrate above, it seems as though both the long-term and short-term economic data are aligning and suggest we are well and truly entering a period of slowing growth.

As such, the most obvious step for investors to take is to allocate a greater portion of their capital to defensive bets that appear likely to outperform in a slowing growth environment. For instance, we should expect to see equities underperform bonds.

Utilities is one such example of a defensive, long-duration equity sector that looks attractive from a purely technical perspective, recently breaking out strongly to the upside.

The performance of utilities companies is heavily linked to interest rates, as rates are a strong driver of their earnings power given the high debt to equity ratios of the sector. The outperformance of utilities is thus a good indicator of the markets expectation of falling interest rates and slowing growth.

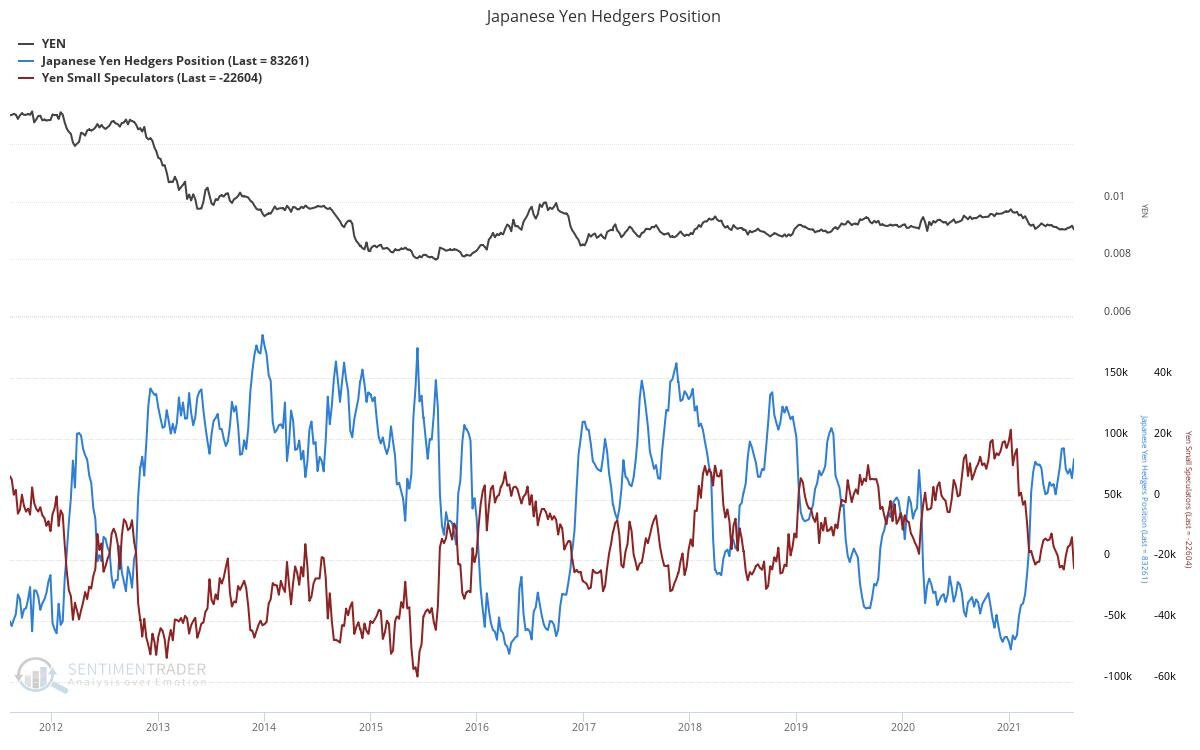

In addition to utilities, another attractive opportunity at present on the defensive side is the Japanese yen. The yen is effectively the ultimate risk-off, safe-haven currency. Even more so than the dollar. From a sentiment perspective, commercial hedgers (i.e. the smart money) in the futures market remain net-long whilst speculators (i.e. the dumb money) are the shortest they have been in years.

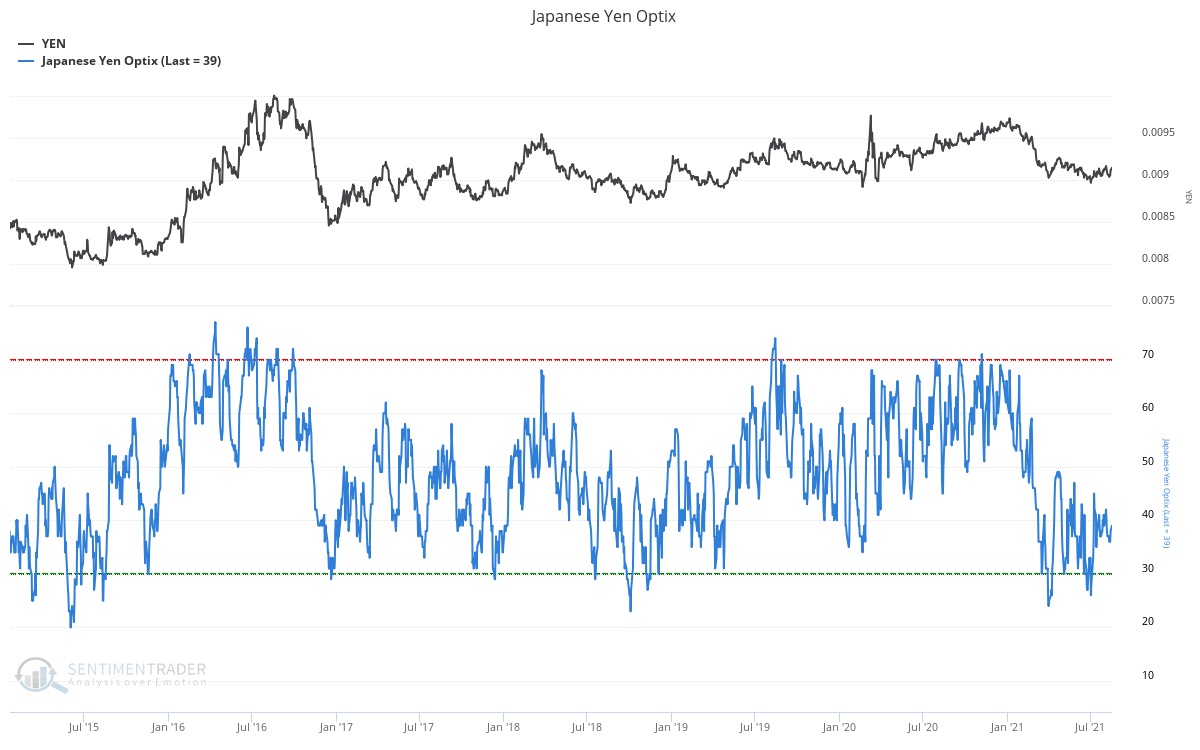

Optix, another measure of investor sentiment, is also showing a relatively bullish reading.

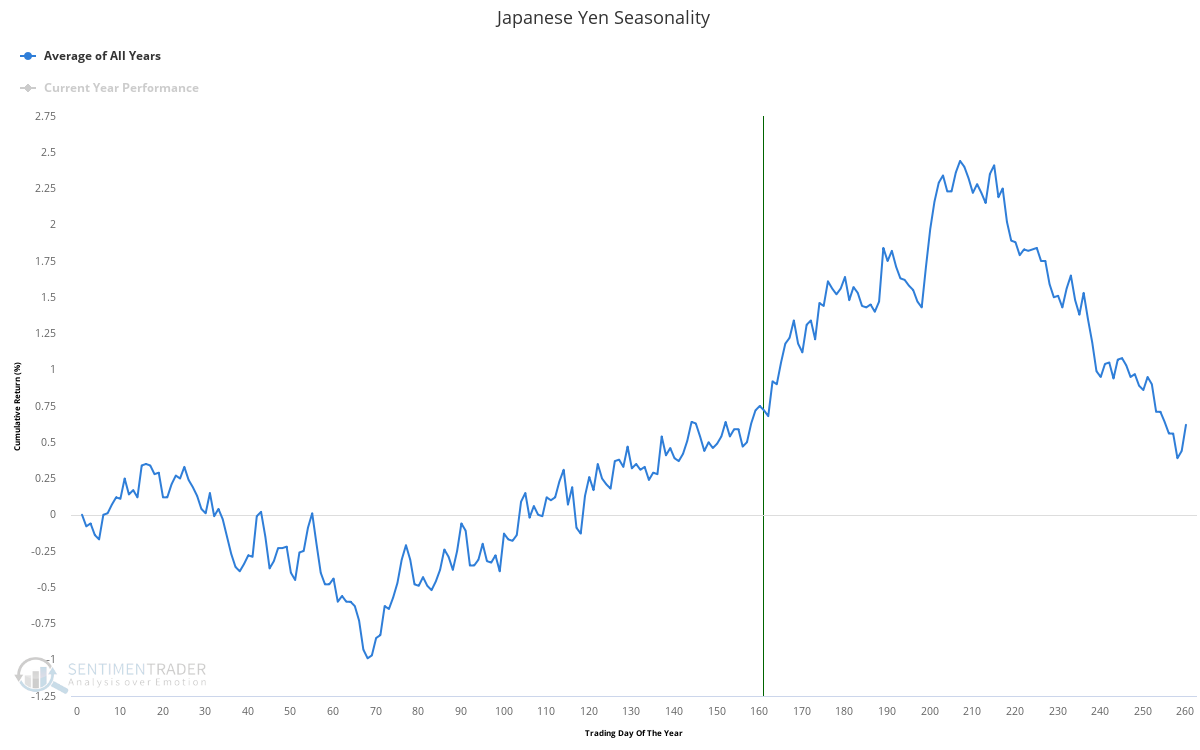

What’s more, seasonality is quite encouraging for the next few months.

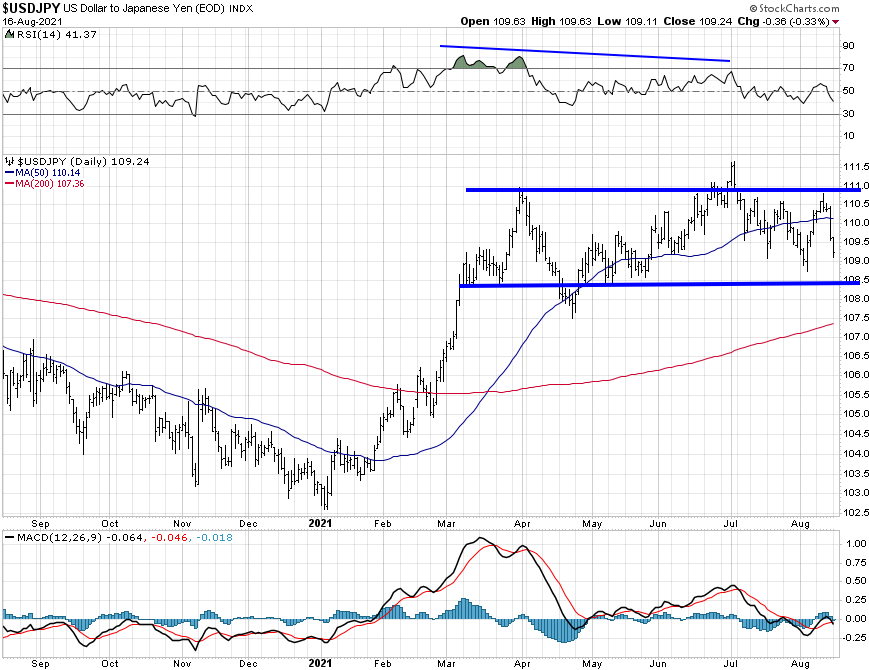

And from a technical perspective, a break of the 108.5 area would seemingly confirm this thesis and potentially provide a good tactical trading entry point.

In all, we can see economic growth is clearly slowing and is beginning to be priced into risk assets. What this means going forward is we are likely to see a continued outperformance of defensive, long-duration type assets and equities, with the reflation trade likely done for the time being. Investors would do well to position their portfolios accordingly, whether that be taking profits from the cyclical trades, accumulating cash or deploying capital in defensive type opportunities as I have detailed above.