Govcoin

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsInnovation is the outcome of a habit, not a random act.

Let me begin with a confession. Govcoin is a made-up name. Don’t for one second think there is a new cryptocurrency called Govcoin. And, before I start, let me make another one. I didn’t come up with that name myself but was beaten to it by The Economist which, in the second week of May, published a series of articles on the forthcoming wave of proper digital currencies which will most likely transform the world as we know it.

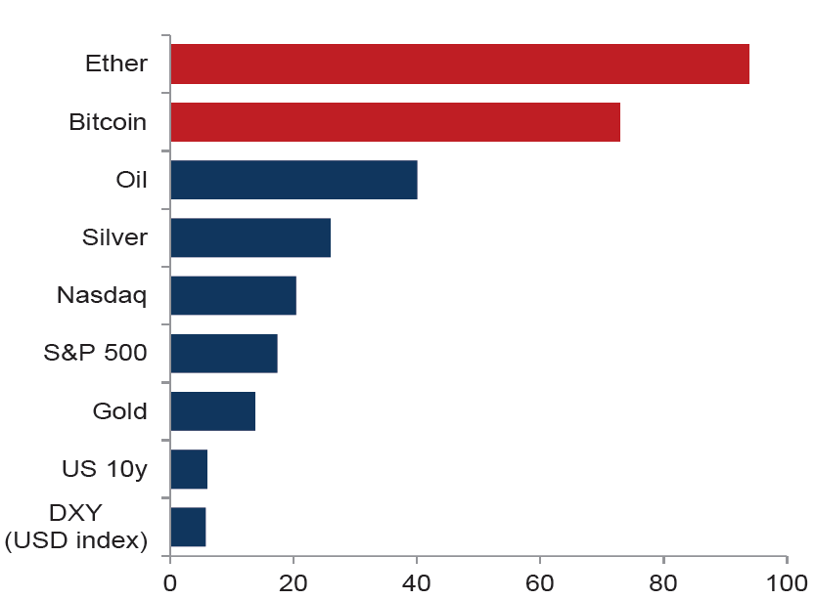

Proper – what do I mean by that? Is Bitcoin not a proper digital currency? No, I don’t think it is, although I will probably upset a few of my readers by saying that. Sponsors of Bitcoin claim it is a digital currency; however, for money to be proper, it must be issued by a central bank, and it must be far less volatile than the average cryptocurrency is today. As you can see in Exhibit 1, the volatility of Ethereum and Bitcoin, the two biggest cryptocurrencies by market capitalisation, is in a league of its own. The volatility of DXY, the USD index, is only a fraction of the volatility of most cryptocurrencies. How would you feel if you money were suddenly worth 20% less than it was yesterday? I know one or two people who would have a problem with that (me included), but that happens to Bitcoin almost every week.

Source: Goldman Sachs Global Investment Research

Don’t get me wrong. Just because Bitcoin and other cryptocurrencies are not proper currencies, they are not necessarily bad investments, but currencies they aren’t. For those of you who subscribe to ARP+, you should read my recent paper on the phenomenon, if you haven’t done so already. I called it Cryptocurrency Mania, and you can find the paper here.

The digital race is on

Bank for International Settlements (BIS), which is the central bank of central banks, have recently conducted a survey on digital currencies. The objective was to take the ‘digital’ temperature on the world’s central banks, i.e. whether they are likely to launch their own digital currency any time soon and, if so, get a sense of how far down the road they are. You can find the survey here.

When looking at the number of central banks responding to BIS’ survey, it is obvious that most central banks are at least exploring the viability of launching a CBDC (insiders’ term for a Digital Currency issued by a Central Bank). According to BIS, more than 60 central banks responded, representing 72% of the world’s population and 91% of global economic output. Interestingly, more EM countries responded than did DM countries (Exhibit 2).

Source: BIS Paper No. 114

No less than 86% of those who responded stated that they are currently exploring the pros and cons of CBDC, and whether it would be viable to go either partially or fully digital in the not-so-distant future. BIS did its first study on CBDC in 2018, and the 2020 study was the third of its kind. As you can see below, the share of central banks which are likely go digital within a handful of years continues to grow (Exhibit 3).

Note: Short-term: up to 3 years; medium term: up to 6 years.

Source: BIS Paper No. 114

The winner is …

When I started to look into this topic, it quickly dawned on me that many of the biggest, and supposedly most sophisticated countries are dragging their feet when it comes to introducing CBDC, thereby running the risk of falling behind the curve. Why it is important not to fall behind the curve, I will explain later.

Take for example the biggest economy of them all – the US. While Congress has expressed some interest in introducing CBDC, the Federal Reserve Bank has (so far) largely been sitting on its hands. Its research into CBDC is still very preliminary, and the US is nowhere near ready to roll out CBDC.

In Europe, none of the big five (Germany, France, Italy, Spain and the UK) are doing meaningfully better than the Americans. The leading light in Europe on CBDC is actually Sweden. Already largely cashless, Sweden could go digital from early 2023, but it depends on the outcome of an ongoing parliamentary inquiry, which will almost certainly end in a parliamentary vote in November 2022. Sweden is already virtually cashless, but don’t assume that going cashless is akin to going digital – it isn’t the same. The said, Riksbank (the Swedish central bank) has committed to converting to CBDC quickly thereafter, should the Swedish parliament vote in favour of going digital next year.

The country in the yellow jersey is not Sweden, though. The clear leader in the digital race is China. A pilot scheme is already up and running with the digital yuan (e-yuan) operating in cyberspace alongside notes and coins. About 500,000 people have now received a small amount of e-yuan that they can spend in certain outlets by downloading an app and holding their smartphone against a scanner in those outlets.

Although the Chinese have not yet indicated when they will go 100% digital, the intention is obvious. Sceptics are saying that it is yet another step towards Big Brother, and that is probably correct, but law-abiding citizens can benefit immensely – more on that below (you can read about the rollout of e-yuan here). And, yes, I am aware that the Bahamas have also issued digital money already (called sand dollars), but I honestly don’t think the sand dollar will assume the same role on the global stage as the e-yuan will.

What is all the fuss about?

From the government’s perspective, introducing digital money is about taking control of the financial system (mostly commercial banks) and of its citizens. Taking control of commercial banks will inevitably stabilise an inherently unstable industry, which is good for all parties. Taking control of its citizens contains both good and bad elements.

Source: The Global Economy

On the positive side, going digital should, all other equal, reduce tax rates over time. The introduction of digital currencies will pretty much eliminate the shadow economy, which law-abiding citizens will benefit from tax-wise. In table 4 above, you can see which countries have the biggest and smallest shadow economy (and please accept my apologies for not having more recent data).

I am often confronted with the argument that people will just pay their builders in a currency that hasn’t gone digital yet, and that is indeed correct; however, it should be relatively easy for regulators to monitor and control movements of foreign currencies that cannot easily be explained. For example, you would never take $20,000 in cash on your 2-week summer holiday to Mallorca, would you? A bigger challenge will be to prevent the economy from turning into a barter economy. Nothing will prevent the accountant from suggesting to the builder that he will do his accounts the next three years if the builder will give his bathroom a facelift.

On the negative side, going digital is potentially another step towards Big Brother. Real-time, you can suddenly monitor what Joe and his wife are having for dinner. The following day, you can see that Joe is not having dinner with his wife but with somebody else. You can then look into who that somebody else is. In other words, if all that information ends up in the wrong hands, it can be badly abused.

As far as the Fed’s inactivity is concerned, allow me to make an important point. If the Fed sits on its hands for too long, the US dollar could lose its status as the premier reserve currency of the world. One of the (many) reasons the US dollar has held on to this status for so long has to do with how frequently the dollar is used when transferring money internationally – particularly between poorer people in EM countries. If there is suddenly a digital alternative which will be virtually cost-free, the dollar may struggle to hold on.

This is important to the Americans, as reserve currencies get away with things other currencies don’t, for example running large external deficits without it having a noticeable impact on the value of the currency. It is also important to the rest of us. Assuming the e-yuan continues to grow in significance, do we really want the world’s premier reserve currency to be under the control of an authoritarian regime?

Let me make one additional comment on the tax implications of going digital. As you can see in Exhibit 4 above, the shadow economy is much bigger in most EM countries than it is in the average DM country, but governments all over the world could do with higher tax revenues, following 16 months of reduced economic activity and massive public spending, which has driven government debt-to-GDP much higher – on average about 20% (source: The World Bank). As you can see, even the supposedly law-abiding Nordic countries have a sizeable shadow economy. In Denmark and Norway, it is so big that the two countries are not even in the bottom 25, worldwide. Those two Scandinavian countries may be law-abiding in other respects, but that is clearly not the case when it comes to tax compliance.

Why Govcoin, not Bitcoin, is the way forward

My professor at university told me that money has three functions. It is a medium of exchange, a unit of account and a store of value. Imagine the mess we could end up in if cryptocurrencies, which are completely unregulated, take over and become the preferred medium of exchange of goods and services.

As we have learned over the years, banks collapse on a fairly regular basis and are particularly ill-equipped to deal with major financial crises. If anything, they have been the cause of many of them, and that is despite banks being highly regulated. Privately issued cryptocurrencies are completely unregulated. How somebody can think that a financial system based on Bitcoin, Ethereum, etc., will be more stable than what we have today is beyond me.

Ideally, money provides a safe and reliable store of value. Going back to Exhibit 1 for a moment, do you think an asset class with a volatility 4-5 times higher than that of Nasdaq stocks deserves to be classified as safe and reliable? The technology behind cryptocurrencies – a technology called blockchain – deserves a pad on the shoulder, but privately issued cryptocurrencies should never be accepted as a medium of exchange. It is a road to financial disaster.

An e-currency issued by a sovereign is an altogether different story, though. As a depositor, you no longer take a risk on commercial banks, as your savings are effectively held by the central bank and thus guaranteed by the country in question. Furthermore, you can transfer your money from A to B at a fraction of the cost charged by commercial banks today. Why? Because it costs almost nothing to transfer digital money. In effect, you circumvent commercial banks and deal directly with your central bank. The introduction of digital money is therefore a humongous risk to the entire banking industry. Before long, we could quite possible live in a world without any commercial banks at all.

According to The Economist, the introduction of Govcoins could, once fully implemented, cut the operating expenses of the global financial system by almost $3Tn annually or about $350 annually for every person on Earth. Furthermore, the 1.7 billion people who do not have a bank account today could get one, as long as they have a smartphone, which many people in the poorest regions of the world already have. As The Economist concludes, “… for ordinary users, the appeal of a free, safe, instant, universal means of payment is obvious”.

Last few words

Short of a major incident – and I am not even sure that would be enough to stop it – we will soon have proper digital currencies (CBDC) on our doorstep. Obviously, some central banks will act faster than others, but the advantages are so obvious, and so many, that pretty much everybody will ultimately sign up.

All the additional debt that governments all over the world have assumed in a desperate attempt to control COVID-19 will only make what is already pretty much a given even more evident. Governments can, with a blink of the eye, improve the revenue intake significantly without changing the tax rate for law-abiding people.

Furthermore, relatively poor people, who work day and night in countries far from home to support their family in some remote village, will suddenly have a low-cost alternative to Western Union, MoneyGram, Xoom, OFX, Wise and other firms which charge through the nose to wire money. That business model will essentially be wiped out with the introduction of CBDC, and the poorest people of the world will benefit the most.

Why do some central bankers vehemently oppose CBDC? Is it because they are shareholders in one of the above-mentioned firms? Or is it because they have just bought a new mansion which requires a great deal of work, which they cannot afford to refurbish unless they pay the builders under the table? I honestly don’t know, but I do know that the Absolute Return Letter will return in early September, as long as I can afford to pay the builders I am about to sign up. Have a wonderful summer.

Niels C. Jensen

1 July 2021

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All