The United Kingdom: A “Value Market” With Exciting Small-Cap Growth Opportunities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWasatch Global Investors

After Brexit and a poor early response to Covid-19, the U.K. economy is now recovering—and a continued rotation toward small caps may be in the offing.

KEY TAKEAWAYS

- Brexit and the pandemic didn’t change the fundamental attractiveness of great U.K. companies with high returns on capital and strong management teams operating in expanding business segments.

- Now that uncertainties are lessening, we believe investors will increasingly recognize which companies are most underpriced and best-positioned to expand and take market share over the long term.

- There’s been a remarkable recovery in the U.K. economy. GDP growth at over 7% in 2021 is expected to be the strongest since the aftermath of World War II, and significant growth is likely to continue through 2022.

- After five years of underperformance, the 2021 year-to-date outperformance by U.K. small caps may be the start of more to come as vaccine distribution continues, the economy further reopens, and businesses and consumers increasingly gain confidence.

- Especially today, economically sensitive stocks are often considered synonymous with “value stocks” because they had been major laggards over the past several years as investors preferred technology-related names.

- At Wasatch, we’re emphatically growth-oriented investors in high-quality companies. But we also seek exposure to continued economic reopening in places like the United Kingdom. And we think we have another wind at our backs based on lower valuations for U.K. stocks.

THE U.K. IS BACK ON TRACK!

- For the past several years, high-quality U.K. companies performed remarkably well considering the challenges they faced. But they were diverted from their growth orientation in order to navigate the uncertainties of Brexit and Covid-19. With the shackles coming off and the clouds lifting, we believe the U.K. is back on track to be one of our favorite places for finding innovative and exciting small caps.

- Before Brexit, those investing in the United Kingdom had generally placed a premium on small companies over large ones because small caps historically had good access to capital and significant headroom for domestic and international growth. Now that Brexit and Covid uncertainties are lessening and the economy is improving, we think our U.K. companies will be particularly adept at taking advantage of idiosyncratic opportunities to create new products and services, make acquisitions and expand geographically.

- Although the United Kingdom is a large country (ranked 21st by population), citizens are densely concentrated in just several areas. This allows a small company that provides unique or superior products or services to quickly become a market leader. Oftentimes, such a company can then extend its leadership position throughout the U.K.’s sizable economy and into foreign countries. The proliferation of well-run small companies is one reason the U.K. has the highest e-commerce penetration of any developed country.

- Beyond e-commerce, we see strong opportunities in retail more broadly, the digitalization of government and business services, biotechnology, travel, hospitality and real estate. For example, housing transactions have recently come in at 15-year highs. The improvement in real estate has been driven by elevated levels of consumer savings and improving household balance sheets. These factors also bode well for housing-related goods and services.

- Based on our firsthand research, we think U.K. small caps have some of the world’s best innovations, management teams and competitive advantages. We tend to emphasize companies that we categorize as strong cash-flow generators, global businesses headquartered in Britain, serial acquirers and technology disruptors.

When we talk about some of our favorite countries for finding attractive investments, clients are often surprised to hear that the United Kingdom is high on our list. After all, the U.K. had to deal with issues surrounding Brexit for the past several years and the country’s initial reaction to the coronavirus pandemic was inadequate.

From our perspective, we think Brexit and the pandemic will definitely have lasting repercussions—but these events didn’t change the fundamental attractiveness of great companies with high returns on capital and strong management teams operating in expanding business segments. In other words, these events created uncertainties that tested—rather than materially damaged—the competitive advantages of innovative British companies, which also benefit from some of the world’s best academic institutions.

Now that these uncertainties are lessening, we believe investors will increasingly recognize which companies are most underpriced and best-positioned to expand and take market share over the long term. This is why we consider the United Kingdom to be a “value market” with exciting small-cap growth opportunities.

EVENTS AND WASATCH ACTIONS OVER THE PAST SEVERAL YEARS

Before we describe the company fundamentals that we think are attractive in the U.K., let’s start with a brief discussion of events over the past several years. In June 2016, 52% of British voters chose to leave the European Union (EU) in a move commonly referred to as Brexit. Although we didn’t expect the vote to go the way it did, we had reduced our U.K. exposure earlier that year as a risk-control measure related to uncertainties surrounding the referendum.

Roughly speaking, in 2015—before Brexit looked likely—we had a U.K. weight in our International Small Cap Growth strategy (and International Growth Fund) of around 18%, which was overweight relative to the benchmark MSCI AC (All Country) World ex U.S.A. Small Cap Index. At that time, approximately 65% of our U.K. holdings were focused on domestic sales and approximately 35% were focused on international sales.

As Brexit looked increasingly probable in 2016, we gradually reduced our U.K. exposure—specifically our exposure to domestically focused companies. After the vote took place in June 2016, we further reduced our overall U.K. exposure. Domestically focused companies dropped to 35% of our U.K. weight, and internationally focused companies increased to 65%. This was because we thought domestically focused companies would struggle to a greater extent amid Brexit uncertainty. And because internationally focused U.K. companies tend to have operations overseas, we believed their businesses wouldn’t be significantly impacted by Brexit.

Our actions described in this section may appear to have been macro-driven. But that’s not the case. Instead, our actions were driven by our fundamental research including what we were hearing from companies on the ground.

In early 2020, the coronavirus pandemic hit the U.K. especially hard. To make matters worse, the government dragged its feet in procuring essential equipment and tests, issued mixed messages about public-health practices, and lagged behind continental Europe in implementing social distancing and other restrictions.

In the years from 2016 through 2020, most U.K. companies tightened their belts and cut back on allocating capital due to Brexit- and then Covid-related uncertainties. As a result, the companies’ stock prices generally lagged those of companies in continental Europe. Interestingly, however, many U.K. companies—especially those we liked for several years—maintained relatively high returns on capital. We think this shows how great companies find a way to stay competitive even during difficult macro environments in which stock prices temporarily languish.

Building on the resilience of U.K. companies over the past several years, there’s been a remarkable recovery in the country’s economy. GDP (gross domestic product) growth at over 7% in 2021 is expected to be the strongest since the aftermath of World War II, and growth is likely to be strong again in 2022. Vaccine development and distribution have been efficient collaborations of government, business, big pharma and the academic establishment. In fact, these collaborations have been among the most effective in the world. Additionally, during the pandemic, the United Kingdom has widened its lead in the adoption of e-commerce—which is one sign of a country’s technological advancement.

Regarding Brexit, the transition period for the U.K. to exit the European Union ended on December 31, 2020. So it’s still too early to know whether or not Brexit—with 20/20 hindsight—will eventually be viewed as a success. But with the uncertainty of the transition gone, with the rules for engaging the EU in place and with a market-friendly political party in power for at least a few more years, our independent research and our discussions with management teams indicate that businesses are increasingly investing in future growth opportunities and allocating capital more freely. Moreover, cash-rich consumers are progressively optimistic.

Additionally, countries around the globe appear to be in a synchronized economic recovery. And stock-price movements tend to precede economic news, which is why we’ve prepared ahead of time. What’s more, small caps are often the market leaders early in a recovery.

Based on these improvements, the U.K. weight in our International Small Cap Growth strategy (and International Growth Fund) is now over 20%, which is nearly double that of the benchmark. In terms of domestically focused companies versus internationally focused companies, we’ve increased our domestically focused exposure to approximately half of our U.K. weight.

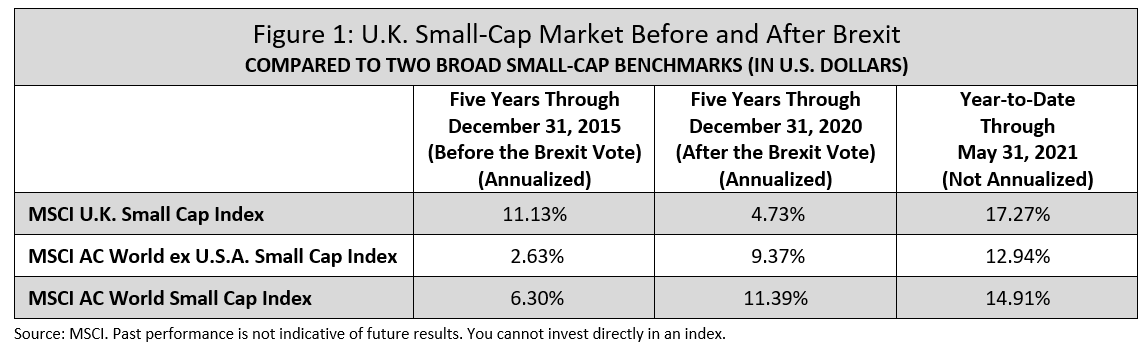

STOCK PERFORMANCE BEFORE AND AFTER THE BREXIT VOTE

Having described the events over the past several years, let’s look at comparative stock-market performance. Since the Wasatch strategy invests in international small caps, our focus, as shown in Figure 1, is on the relevant small-cap indexes including the MSCI U.K. Small Cap Index versus the MSCI AC World ex U.S.A. Small Cap Index. We also present the MSCI AC World Small Cap Index, which includes the U.S.A., to provide a perspective for global investors.

Figure 1

As shown in Figure 1, the MSCI U.K. Small Cap Index led the other two small-cap indexes during the five years through December 31, 2015 (before the widespread publicity surrounding the Brexit vote). And the MSCI U.K. Small Cap Index trailed the other two indexes during the five years through December 31, 2020 (after the Brexit vote). This makes sense given the uncertainty and corporate belt-tightening during the five years after the vote. Please note that even though the Brexit vote took place in June 2016, we consider the “before” period to end on December 31, 2015 and the “after” period to start on January 1, 2016 because Brexit affected companies and markets several months in advance of the actual vote.

Beyond the two five-year periods presented above, over longer periods the U.K. market has tended to move in cycles of outperformance and underperformance relative to other international developed small-cap markets. So Brexit and the early pandemic response have likely magnified this cyclicality. The 2021 year-to-date outperformance by the MSCI U.K. Small Cap Index may be the start of more to come as vaccine distribution continues, the economy further reopens, and businesses and consumers increasingly gain confidence.

WHERE THE UNITED KINGDOM STANDS TODAY

Again, while we notice macro cycles, we don’t invest based on them. Instead, we’re hearing from companies and consumers that conditions in the U.K. are improving. Likewise, these conditions are being reflected in the numbers we see in our work.

To evaluate our current investments and analyze potential new investments, we start by screening databases of corporate information based on our strict criteria. Some metrics we include are ROE (return on equity), ROA (return on assets), ROIC (return on invested capital), and sales, earnings and cash-flow growth. We also consider the quality of a company’s balance sheet. For example, the U.K. is home to more than 100 high-quality small companies—between $300 million and $5 billion in market cap—with an ROE above 15%. This is about one-third the number of companies meeting the same criteria in the U.S.

Based on these and other criteria, we see that some of our most interesting opportunities are located in the United Kingdom—partially because U.K. companies are particularly effective at allocating capital. Moreover, when we do our on-the-ground research, we find that U.K. companies—including small caps—have some of the world’s best innovations, management teams and competitive advantages.

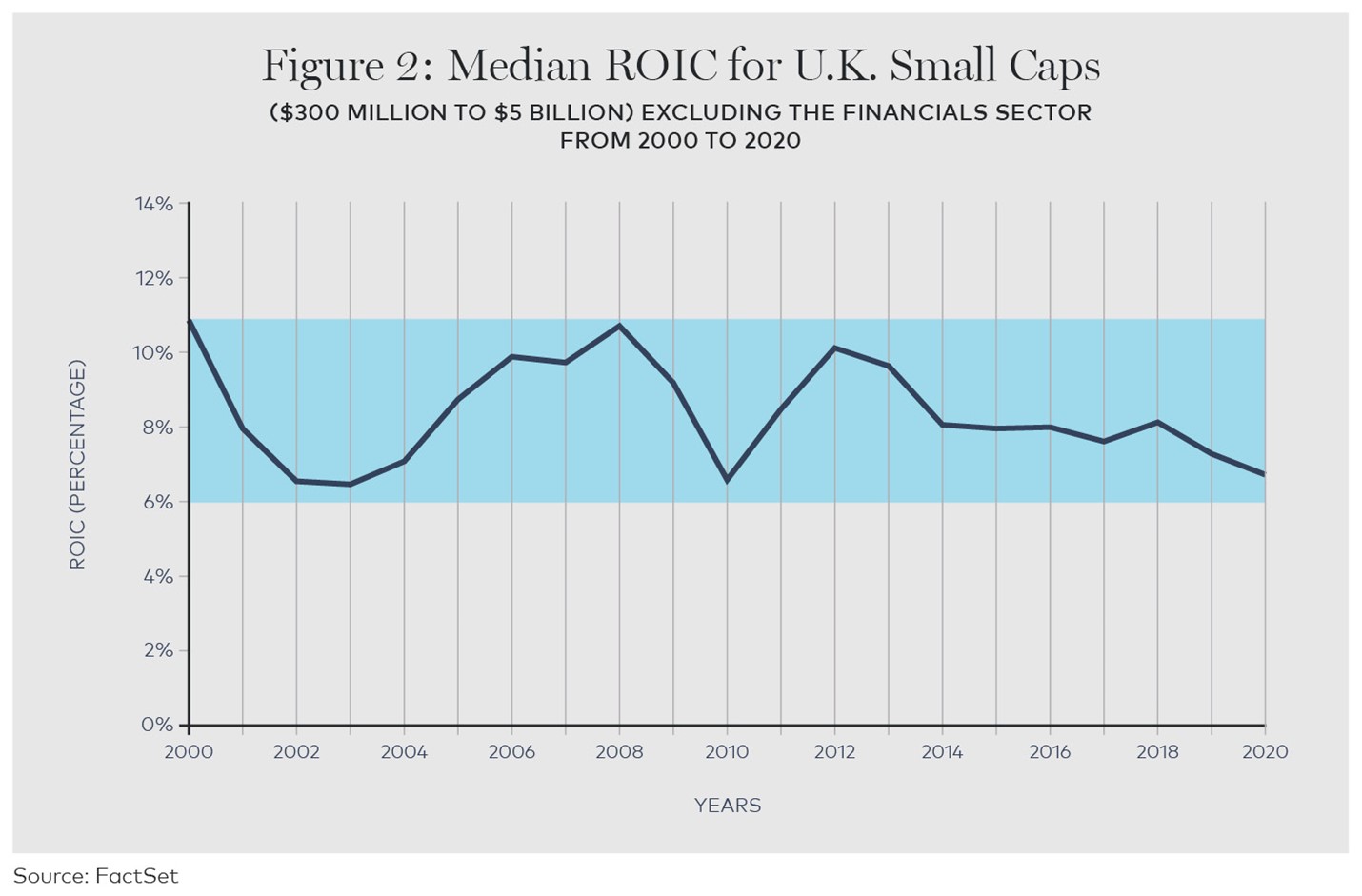

Figure 2 indicates the median ROIC for U.K. small caps ($300 million to $5 billion) from 2000 to 2020. Financial companies are excluded from the data because ROIC isn’t a relevant statistic for these companies. As you can see, ROIC has persistently stayed within an attractive band. And ROIC has been significantly above the companies’ cost of capital for years on end—including through periods like the global financial crisis and Brexit. We believe this sustainability has been a long-term indication of a high-quality market. In other words, U.K. companies have consistently been able to put their capital to work in productive ways, which is especially attractive amid very low yields on government and corporate bonds.

Figure 2

Another consideration is that the United Kingdom has its own independent currency, the British pound. In fact, even when the U.K. was part of the European Union, the country maintained the pound as a medium of exchange. Although having an independent floating currency is nothing new for the U.K., we mention this because it’s important to understand that a floating currency acts as a “temperature gauge” and as a “shock absorber” for a country. For example, when the global business and investment communities lose some confidence in a country, the currency can float downward as a gauge of falling value relative to other currencies. This can absorb some of the negative effects by making the country’s debt less onerous to repay and its exports less expensive to the rest of the world, helping the country get back on its feet.

WHY WE CONSIDER THE UNITED KINGDOM TO BE A “VALUE MARKET” WITH EXCITING SMALL-CAP GROWTH OPPORTUNITIES

As we said, over long periods, the U.K. market has tended to move in cycles of outperformance and underperformance relative to other developed markets. Additionally, based on our fundamental research, we believe U.K. small caps in particular may have recently entered a period of outperformance.

Beyond these long-term cycles, U.K. stocks may be affected by shorter-term economic changes. For example, we believe the stock market will take some cues from the manufacturing-related PMI (purchasing managers’ index), which has been showing economic expansion for the past several months. Especially today, economically sensitive stocks are often considered synonymous with “value stocks” because they had been major laggards over the past several years as investors preferred technology-related names that could grow and take market share in any economic environment.

At Wasatch, we’re emphatically growth-oriented investors in high-quality stocks. What really excites us is that, on the ground in the United Kingdom, we see some of the best and most plentiful small-cap growth opportunities based on innovation and managerial expertise. Additionally, we think we have another wind at our backs based on lower valuations and heightened sensitivity to positive economic news in the U.K.

In gauging the expensiveness of companies, we look at factors like price to earnings, price to sales, price to book value, EV (enterprise value) to EBITDA (earnings before interest, taxes, depreciation and amortization) and EV to sales. Many U.K. companies look relatively inexpensive to us based on these metrics.

Bolstering the factors described above, U.K. companies and their investors should benefit from increased spending on R&D (research and development) and from a healthy environment for IPOs (initial public offerings). The government’s target is for the public and private sectors to spend a combined 3% of GDP on R&D by 2034. In U.S. dollar terms, that would amount to around $130 billion—roughly double the current spending level. And since the Brexit vote in June 2016, the United Kingdom has seen over 260 IPOs.

CATEGORIES OF COMPANIES WE LIKE, AND SOME SPECIFIC EXAMPLES

The U.K. companies we like generally fall into the following categories:

- Strong cash-flow generators that are domestically focused for the most part

- Global businesses that were impacted due to their headquarters being located in Britain

- Serial acquirers

- Technology disruptors

The strong cash-flow generators usually deploy their cash in a balanced way—some cash reinvested into the business for growth, some paid out as dividends and some used for share buybacks. We consider these companies to be relatively inexpensive compared to the growth they experience, and they should benefit even more from an improved domestic economy. Examples of strong cash-flow generators include: (1) B&M European Value Retail, a discount retailer of general merchandise ranging from electronics to home goods; (2) Domino’s Pizza Group plc, which holds the exclusive master franchise to own and operate Domino’s Pizza stores in the U.K. and Ireland; (3) Howden Joinery Group, a designer, manufacturer and seller of fitted kitchens; and (4) Rightmove, which operates a website that lists properties across Britain and publishes a house-price index.

Even though some of our holdings are global businesses, they were impacted by the misperception that they were particularly vulnerable to Brexit-related woes. In reality, many global businesses have operations in multiple countries. But the misperception gave us the opportunity to build positions in these companies at attractive prices. Examples of global businesses include: (1) Abcam, a biotechnology company that offers antibodies, reagents and assay kits to carry out analyses; (2) Fevertree Drinks, which offers premium mixers for alcoholic beverages; and (3) Electrocomponents plc, a distributor of electronics and electrical, mechanical, automation, health and safety components.

The serial acquirers tend to operate globally and use most of their free cash flow to buy other companies. Our serial acquirers have a history of successful capital allocation and are attractively priced based on the synergies they achieve by combining companies in order to grow more quickly. Examples of serial acquirers include: (1) Diploma plc, whose subsidiaries manufacture and distribute building components, special seals, and an assortment of scientific and laboratory equipment and telecommunications products; and (2) Halma, which manufactures products that detect hazards and also protect assets and people in public and commercial buildings.

Based on the presence of advanced academic institutions and innovation in the United Kingdom, it’s no surprise that technology disruptors are prevalent in the business landscape. Such disruptors include: (1) AJ Bell, a provider of an investment platform that offers stockbroking, wealth management, custody, settlement and dealing services; and (2) Endava, which offers software engineering, cloud transformation, test automation, technology consulting and other related services.

SUMMARY AND OUTLOOK

We should acknowledge that our nature is to be optimistic. This is because economies tend to grow over time and great companies usually find a way to thrive over the long run. But we ultimately make decisions based on company fundamentals. The numbers we see in our analysis and the findings of our on-the-ground research keep us tethered to realistic projections and help us ignore pollyannaish forecasts. Today, our analysis and research are leading us to an overweight position in the U.K.—which for decades has been home to many high-quality companies.

As a possible analogy, we can look at Brexit like the Y2K (Year 2000) problem. In the few years before Y2K, many “experts” were predicting that the turn of the millennium would create a computing meltdown. In the end, there were obstacles, but governments and businesses performed exceptionally well overall. Although the dust will probably take a few years to settle, the same may turn out to be true for Brexit.

Regarding the coronavirus pandemic, it’s clear that lockdowns, social distancing, contact tracing and testing were implemented too slowly in the United Kingdom and many other countries. Additionally, PPE (personal protective equipment) preparedness was extremely poor. But especially in the U.K. and the U.S., highly effective vaccines were developed, manufactured and distributed in record time that exceeded the expectations of even the most optimistic forecasters.

From a currency perspective, the weak British pound was helpful as the United Kingdom struggled with Brexit and the pandemic. But now that the country is on firmer footing, we think the pound may strengthen. In particular, we believe a stronger pound may benefit non-British (e.g., American) investors holding U.K. securities denominated in pounds.

In terms of innovation—according to Cornell University, INSEAD and the World Intellectual Property Organization—the United Kingdom ranks fourth among 131 economies in the 2020 Global Innovation Index. The country ranks second based on the quality of universities, including Oxford and Cambridge, which are among the top 10 universities in the world. In addition, the U.K. is home to four of the world’s top 100 science and technology clusters: the cities of London, Cambridge, Oxford and Manchester. Cambridge and Oxford are also the most science- and technology-intensive clusters in the world. As for Nobel Prize laureates, the United Kingdom has 133—second only to the United States.

With the global economic recovery broadening, we expect the U.K. to be a major beneficiary. In the environment we foresee, we’d expect to witness not only revenue growth but also profit-margin expansion—which could magnify the effects of the economic recovery for many U.K. companies. And investors appear to be taking notice: According to Financial Intelligence, aggregate flows into U.K. equity funds compared to assets under management have started to see the biggest turnaround since the date of the formal announcement that the Brexit vote would take place.

More specifically, when it comes to market capitalization, the United Kingdom has a long history of embracing small caps. As mentioned, the pipeline of IPOs is vibrant. In addition, once a publicly traded small cap exhibits significant operating success, the stock tends to be rewarded with a premium price and ample liquidity. For our part, we also like small caps because return drivers and risk factors in these companies are usually less complicated. So we can more readily create a diversified portfolio of exciting small-cap growth stocks that have lower correlations with one another.

--

ABOUT THE PORTFOLIO MANAGERS

Ken Applegate, CFA, CMT

Lead Portfolio Manager

5 Years on Strategy / 7 Years at Wasatch

Mr. Applegate is a Portfolio Manager, the head of international developed markets investing and a member of the global research team. He joined Wasatch Global Investors in 2014.

During more than two decades of investing, Mr. Applegate has focused exclusively on global small cap companies. His career began in 1994 in London, where he served as a financial analyst and later as a co-manager of a foreign exchange hedge portfolio for Refco. In 1996, he moved to the U.S. where he spent 11 years specializing in small cap investing for RCM and then Berkeley Capital Management. Later, he returned to his native New Zealand to join Fisher Funds as a senior portfolio manager, and was integral in launching and managing international small cap funds. In 2012, he moved back to the U.S. to launch the Pacific View Asset Management international small cap strategy.

Mr. Applegate completed his Bachelor of Management studies at the University of Waikato in New Zealand. He is also a CFA charterholder and a Certified Market Technician (CMT).

Ken enjoys cycling, surfing and snowboarding.

Linda Lasater, CFA

Portfolio Manager

7 Years on Strategy / 14 Years at Wasatch

Ms. Lasater is a Portfolio Manager on the international micro/small cap and global research teams. She joined Wasatch Global Investors as a Senior Analyst in 2006. She also completed a successful research internship with Wasatch during the summer of 2005.

Prior to joining Wasatch, Ms. Lasater worked as a project lead and systems analyst in the portfolio analytics group at AIM Investments, where she developed tools that enabled portfolio managers and analysts to make informed investment decisions.

Ms. Lasater earned a Master of Business Administration from the Tuck School of Business at Dartmouth. Earlier, she received a Bachelor of Business Administration in Management Information Systems from the University of Texas, where she was a chairperson and membership director of the Asian Business Students’ Association. She is also a CFA charterholder.

Linda is conversational in Vietnamese and fills her free time learning new languages. She enjoys hiking, cycling and table tennis.

Derrick Tzau, CFA

Associate Portfolio Manager

1 Year on Strategy / 3 Years at Wasatch

Mr. Tzau is an Associate Portfolio Manager on the international small cap research team. He joined Wasatch Global Investors in 2018 as a Senior Analyst.

Prior to joining Wasatch, Mr. Tzau was a senior international equity analyst at Rainier Investment Management. He was a founding member of Rainier’s international small/mid cap growth strategy and covered companies in developed and emerging markets across all sectors, with an emphasis on health care, consumer products and services, industrials and financials. Earlier, he was an equity research associate and an assistant portfolio manager at WHV Investment Management, where he covered U.S. small caps, U.S. micro caps, and emerging markets equities across a broad range of countries, sectors and market capitalizations.

Mr. Tzau earned a Master of Science in Finance from Seattle University, and a Bachelor of Science in Pharmaceutical Science from the University of British Columbia. He is also a CFA charterholder.

Before moving to Salt Lake City, Derrick lived in Hong Kong, Toronto, Vancouver and Seattle. He enjoys hockey, basketball and traveling.

RISKS AND DISCLOSURES

Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visitwasatchglobal.com or call 800.551.1700. Please read the prospectus carefully before investing.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

Wasatch Advisors, Inc., trading as Wasatch Global Investors ARBN 605 031 909, is regulated by the U.S. Securities and Exchange Commission under U.S. laws which differ from Australian laws. Wasatch Global Investors is exempt from the requirement to hold an Australian financial services licence in accordance with class order 03/1100 in respect of the provision of financial services to wholesale clients in Australia.

The Wasatch International Growth Fund’s investment objective is long-term growth of capital.

Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk.

As of March 31, 2021, the Wasatch International Growth Fund had 1.6% of its net assets invested in B&M European Value Retail S.A., 1.3% in Howden Joinery Group plc, 1.4% in Rightmove plc, 2.1% in Abcam plc, 1.8% in Fevertree Drinks plc, 2.3% in Electrocomponents plc, 1.9% in Diploma plc, 1.8% in Halma plc, 1.1% in AJ Bell plc and 1.2% in Endava plc.

Domino’s Pizza Group plc was not held in the Wasatch International Growth Fund as of March 31, 2021, but was purchased subsequently.

Wasatch Advisors, Inc., doing business as Wasatch Global Investors, is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Global Investors.

CFA® is a trademark owned by the CFA Institute.

DEFINITIONS

Brexit is an abbreviation for “British exit,” which refers to the June 23, 2016 referendum whereby British citizens voted to exit the European Union. The referendum roiled global markets, including currencies, causing the British pound to fall to its lowest level in decades.

The “cloud” is the internet. Cloud-computing is a model for delivering information-technology services in which resources are retrieved from the internet through web-based tools and applications, rather than from a direct connection to a server.

Correlation, in the financial world, is a statistical measure of how asset classes, securities, markets, or countries move in relation to each other.

Earnings growth is a measure of growth in a company’s net income over a specific period, often one year.

Enterprise value (EV) is a measure of a company’s value calculated as market capitalization plus debt, minority interest and preferred shares, minus total cash and cash equivalents.

The EV-to-EBITDA (earnings before interest, taxes, depreciation and amortization) ratio is enterprise value, as defined above, divided by annual EBITDA.

The EV-to-sales ratio is enterprise value, as defined above, divided by annual sales. The ratio helps to measure a company’s expensiveness.

The global financial crisis, also known as the 2008-2009 financial crisis, is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

An initial public offering (IPO) is a company’s first sale of stock to the public.

INSEAD stands for Institut Européen d’Administration des Affaires. INSEAD is recognized globally as one of the top business schools.

The price-to-book value ratio is used to compare a company’s book value to its current market price.

The price-to-earnings (P/E) ratio, also known as the P/E multiple, is the price of a stock divided by its earnings per share.

The price-to-sales ratio is a stock’s capitalization divided by the company’s sales over the trailing 12 months. The value is the same whether the calculation is done for the whole company or on a per-share basis.

The Purchasing Managers Index (PMI) is an indicator of the economic health of the manufacturing sector. The PMI is based on five major indicators—new orders, inventory levels, production, supplier deliveries, and the employment environment.

Return on assets (ROA) measures a company’s profitability by showing how many dollars of earnings a company derives from each dollar of assets it controls.

Return on equity (ROE) measures a company’s efficiency at generating profits from shareholders’ equity.

Return on capital is a measure of how effectively a company uses the money, owned or borrowed, that has been invested in its operations.

Return on invested capital (ROIC) is a way to assess a company’s efficiency at allocating the capital under its control to profitable investments.

Sales growth is the increase in sales over a specified period of time, not necessarily one year.

The World Intellectual Property Organization (WIPO) is a global forum for intellectual property (IP) services, policy, information and cooperation. It is a self-funding agency of the United Nations, with 193 member states.

Valuation is the process of determining the current worth of an asset or company.

The MSCI AC (All Country) World ex U.S.A. Small Cap Index is an unmanaged index and includes reinvestment of all dividends of issuers located in countries throughout the world representing developed and emerging markets, excluding securities of U.S. issuers. This index is a free float adjusted market capitalization index designed to measure the performance of small capitalization securities.

The MSCI AC (All Country) World Small Cap Index is an unmanaged index and includes reinvestment of all dividends of issuers located in countries throughout the world representing developed and emerging markets. This index is a free float adjusted market capitalization index designed to measure the performance of small capitalization securities.

The MSCI U.K. Small Cap Index is designed to measure the performance of the small cap segment of the U.K. equity market. The index represents approximately 14% of the free float adjusted market capitalization in the United Kingdom.

You cannot invest directly in these or any indexes.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Wasatch Global Investors

505 Wakara Way, 3rd Floor

Salt Lake City, UT 84108

© 2021 Wasatch Global Investors. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc. WAS005451 10/30/2022

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits