Economic Commentary: Brexit, Restaurants, Boeing and Airbus

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIN THIS ISSUE:

- Brexit: A Midyear Update

- Food For Thought

- Boeing and Airbus: Clear For Takeoff

The Summer Olympics are just around the corner, with four new sports (karate, skateboarding, sport climbing and surfing) set to make their Olympic debuts. Kicking cans down a road is not an Olympic sport; but if it were, the United Kingdom (U.K.) and member nations of the European Union (EU) would have fought for gold. The ongoing dispute between them is leaving the respective economies behind the pack.

Five years on from the Brexit referendum and six months since the U.K. left the EU, the two sides are still trying to finalize several important conditions of the divorce. Since their separation, relations between Britain and the rest of Europe have become increasingly complex: tensions have arisen over Northern Ireland, fishing rights, financial services and vaccine exports, among other things.

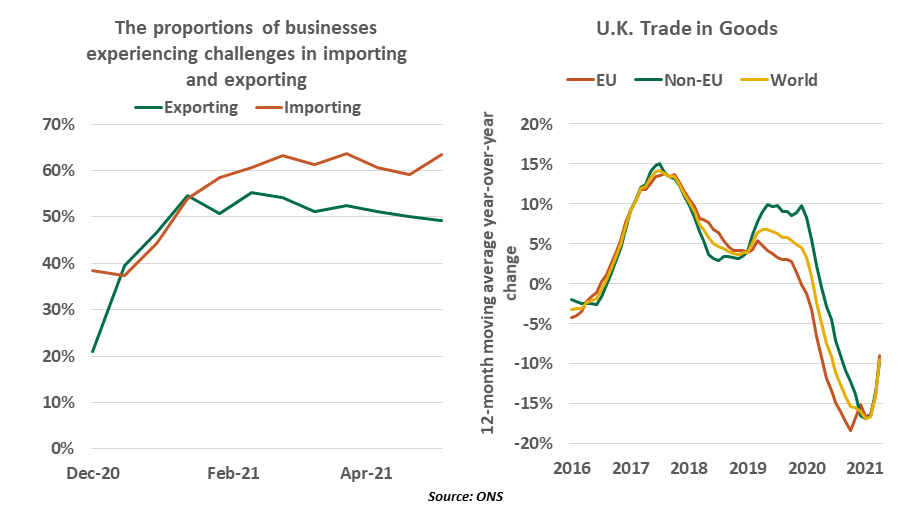

Brexit has created barriers to trade and cross-border mobility, causing disruptions in supply chains. Goods entering the EU from the U.K. must comply with new customs declarations, rules of origin, product safety standards and inspections. According to Britain’s revenue authority, new import and export declarations will likely cost U.K. firms £7.5 billion per annum. While commerce between Britain and the EU is tariff-free, an analysis by the University of Sussex found that British businesses have paid to £3.5 billion in tariffs to the EU since the start of the year; many exporters simply weren’t prepared to file for the relief available to them.

In February’s IHS Markit/CIPS survey, British manufacturers reported a near-record increase in supply chain disruption and rising costs. Some of this was due to COVID-19, but Brexit also played a heavy hand. With no time to transition (since the exit agreement was struck just a week before exit), businesses have been hit hard.

Delays of goods at borders are more tangible, but services have also suffered from Brexit. A study by researchers at Aston University concluded that Brexit shrank the U.K.’s service exports by £113 billion between 2016 and 2019. More than £900 billion in bank assets, equivalent to about 10% of the British banking system, are moving out of the country. Insurance firms and asset managers have transferred more than £100 billion in assets and funds. British businesses, particularly in industries like hospitality, are struggling to recruit employees.

A recent scuffle illustrates how unstable post-Brexit conditions have become. Europe is presently pursuing legal action against Britain for unilaterally delaying the enforcement of sanitary standards on foods entering Northern Ireland from the U.K. The affair has been playfully dubbed “the sausage war,” but there is nothing humorous about it.

|

Trade issues surrounding Northern Ireland remain very much unresolved. |

Because of close economic ties between the Republic of Ireland and Northern Ireland, the two agreed to have equivalent trade rules. (French President Macron recently observed, provocatively, that Northern Ireland was not part of the U.K. for purposes of trade.)

This required changes to inspection standards, which would place Northern Ireland at odds with the rest of the U.K.

An official request has been made by the U.K. seeking an extension to the compliance timeline, but the EU has grown impatient with delays. There is wonderment in Brussels if the U.K. ever intended to abide by the terms of the withdrawal agreement. A considerable amount of commerce between the two Irelands hangs in balance, as does the fragile peace along the border that separates them.

A unilateral abrogation of the withdrawal agreement by the U.K. could worsen economic ties, possibly beyond repair. In line with the agreed terms of the Brexit deal, the EU will not take legal action initially, but will target British goods and financial services exports through import surcharges and additional customs restrictions.

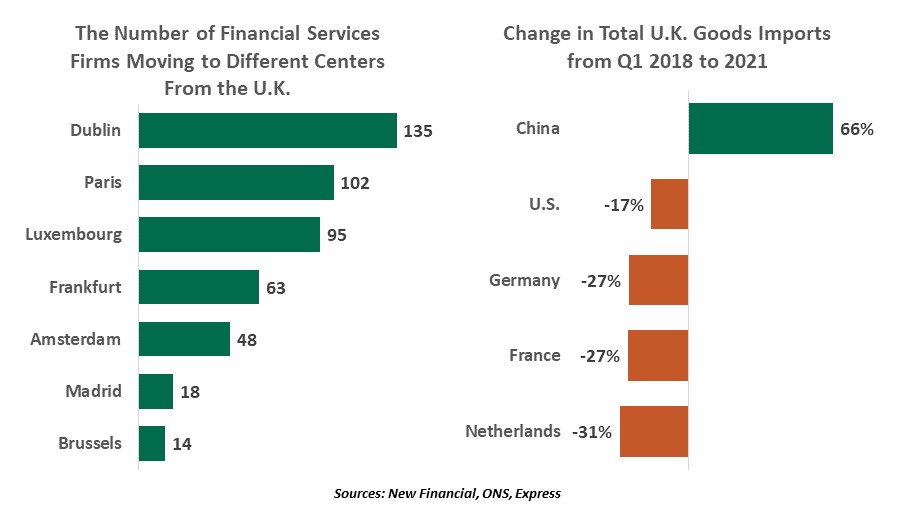

London’s dominance of international finance has largely been due to its success at attracting foreign investors, but Brexit has diminished that standing. The U.K. has come second to France as the most popular European destination for foreign investors for two years in a row. For financial services firms, Dublin has emerged as popular choice for a new English-speaking foothold within the EU. Paris, Luxembourg, Frankfurt, and Amsterdam have also gained at the U.K.’s expense.

Brexit has also had a significant impact on the geography of U.K. imports. China has replaced Germany as the U.K.'s biggest single import market, to the detriment of EU members. But owing to the U.K.’s export dependency on the EU, there is little doubt that Britain has more to lose from worsening ties than their counterparts across the English Channel. According to the European Commission, Brexit will likely cost the Bloc around 0.5% of gross domestic product by the end of 2022, as compared to a 2.3% hit to the U.K. economy.

With an objective to diversify its trade, the U.K. has been pursuing trade deals with countries like the U.S. and New Zealand. The U.K. and Australia have announced an “agreement in principle,” the first deal negotiated from scratch since Brexit. (The free trade agreement reached between the U.K. and Japan last September was simply a roll-over of terms of Japan’s treaty with the EU.)

Westminster has trumpeted this success, but still has a lot of work to do to replicate the fluidity of international commerce it enjoyed under EU auspices.

|

Britain is making some progress on new trade deals. |

While the U.K. enjoys the ability to strike new trade deals and diverge from European regulatory standards, it will have to tread carefully. Significant deviation from shared rules in areas like workers' rights and environmental protection could lead to the introduction of tariffs by the EU.

This is not the first, and probably not the last time, that the U.K. and the EU face a tight timeline for reaching compromise. Just like the numerous occasions in the past, kicking the can down the road looks the most probable outcome. We just hope that resolving all of the issues related to Brexit won’t linger until the next Summer Olympics.

No Reservations

Carl looks at the economic recovery through his favorite lens: food.

Prior to COVID-19, my wife and I would typically dine out once a week. We’ve always enjoyed exploring cuisines and the cultures behind them. Spending time at a table with others is a great way of making and maintaining connections. Unfortunately, the pandemic put our palates on hold.

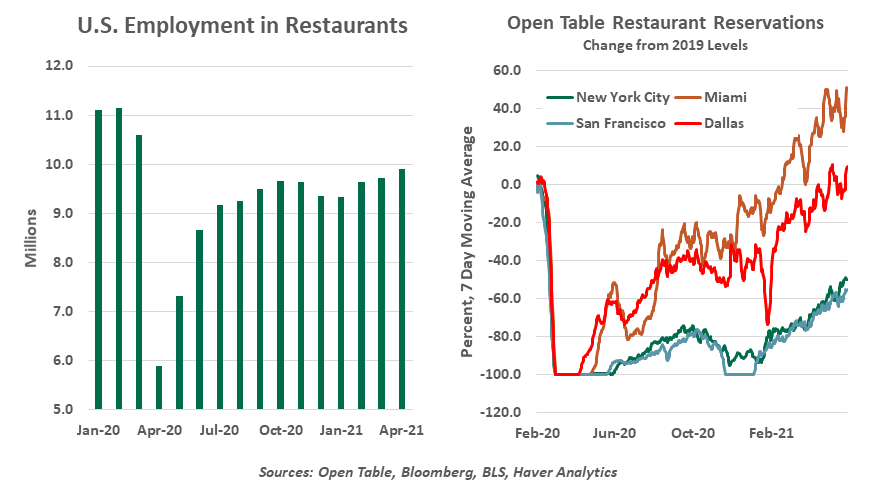

Like many, we’ve tried to support our favorite kitchens during the past year by carrying out. We’ve found that some dishes (like ma po tofu) travel very well, while others (arancini) suffer silently in their plastic enclosures. Despite the collective best efforts of diners, however, the National Restaurant Association estimates that 110,000 eateries closed last year. The ripple effects of these closures were felt throughout the food industry; nearly half of all restaurant workers in the United States, more than five million people, lost their jobs in the early months of the pandemic.

In-person dining has been reopening to various degrees for some time. But for most of last year, dining rooms were subject to strict capacity limitations. And before vaccination, many diners hesitated to visit their favorite cafés. The recession in the restaurant industry was far worse than it was for the economy overall.

Both proprietors and patrons have therefore been cheered by the success of the American vaccination program and the consequent reduction in public health risks. Crowds are returning to restaurants, and we have been among them. It has been a pleasure to peruse a menu again, and to enjoy a meal freshly prepared a professional kitchen.

But I couldn’t prevent myself from doing some economic surveillance in the process. During our recent meals out, it has been abundantly clear that demand exceeds supply. There were large clusters of people waiting for tables; staff seemed insufficient and overwhelmed; some entrees arrived at less than their peak, likely the result of timing challenges in the kitchen.

A root cause is labor. As we’ve discussed, some workers have been slow to return to the labor force, which leaves hiring managers scrambling to find help. Overall, employment in the restaurant industry is still more than one million below pre-pandemic levels. Further, a record percentage of Americans quit their jobs during the month of April, moving to accept better opportunities. That kind of churn makes it difficult to sustain table service.

While it would appear on the surface that there are people available to help prepare and serve food, geographic mismatches complicate the situation. Restaurants in some parts of the country are as busy or busier than they were prior to COVID-19, while others are just starting to rebound. It may not be feasible or economical for a server who lives in San Francisco to relocate to Miami.

It has also seemed to us as if the offerings on menus have been pared back. Purveyors had to divert their output to grocery stores when the pandemic started, and are only now re-establishing supply lines for fresh food to restaurants. I suspect that reversing the food chain is taking time.

|

Demand for restaurant meals is well ahead of supply. |

And finally, it has seemed as if the price of a meal has gone up. The cost of food at full-service establishments jumped by 7% in the most recent month, bringing year over year inflation in the sector to more than 4%. It does not seem likely that restaurants will be able to push through price increases of that magnitude indefinitely, though. As the months progress, we expect supply and labor market conditions to normalize, which should bring prices back under better control.

Restaurants are on the front lines as we monitor the surging U.S. economy. The supply chain, labor, and safety issues they currently confront are emblematic of what is being experienced in other sectors. Their progress of the industry in dealing with these challenges will be a bellwether in the months ahead.

We’re looking forward to doing our part in the recovery process. The search for the perfect plate is back on; while I hope we make progress, I also hope that the quest never ends.

Exiting Turbulence

Gone is the push for trade deals. Instead, we have entered an era of “cooperative frameworks.”

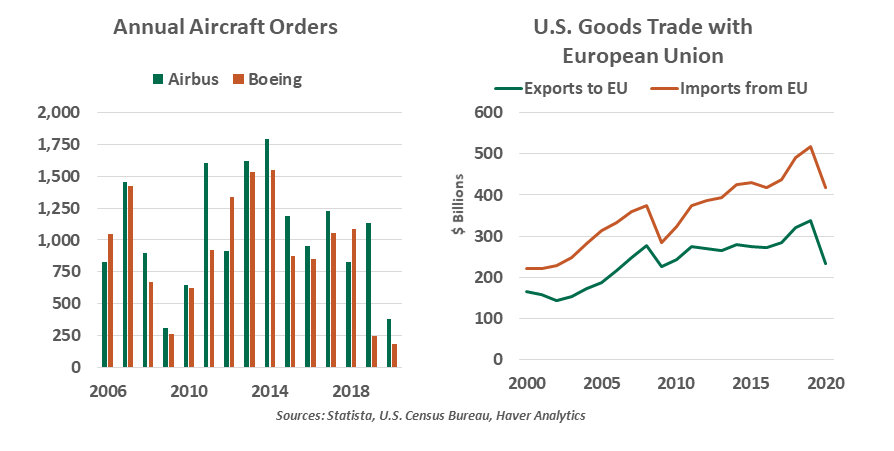

This month, the Office of the U.S. Trade Representative announced détente with the European Union and U.K. in the long-running Boeing-Airbus competitive dispute. Boeing first accused Airbus of receiving anticompetitive state subsidies in 2004. Airbus is owned in part by a consortium of European governments, which offers the company “launch aid” loans to fund the high cost of new aircraft development. These loans carry interest rates well below the typical cost of corporate debt, a subsidy to Airbus. But Airbus fired back, pointing out the substantial government payments Boeing receives through its defense contracts.

Both allegations had merit, and years of negotiation and litigation could not break the stalemate. The conflict reached its height as the U.S. enacted tariffs and European nations retaliated in 2019, affecting goods ranging far beyond aircraft, from French cheese and Scotch whisky to American motorcycles.

While the new framework does not end the dispute, it should cool it. Both sides have agreed to establish a working group to continue discussions. To satisfy the U.S., the agreement calls for aircraft investments to be financed on market terms; to placate Europe, Boeing’s research and development funding and outputs will be more transparent. All sides agreed to a five-year suspension of tariffs stemming from this dispute.

|

Ending the aircraft dispute is a welcome development, but will not be a model for other industries. |

An agreement to keep negotiating is preferable to interminable litigation. Both sides understand their fight was a costly distraction from more substantial trade issues, such as competition from China. Better for all to acknowledge that a large, important market like aircraft will always have some government participation, and no one gained from unrelated and unproductive tariffs.

The framework is a welcome shift toward cooperation. Unfortunately, the unique characteristics of the large aircraft duopoly mean this is unlikely to set a model for the U.S. to resolve its other disputes. U.S. tariffs on steel and aluminum were a unilateral action under the guise of protecting a domestic industry essential to national security; tariffs on China’s exports are specific to China’s trade practices. The Biden administration may yet find a way forward on these matters, but they will require more substance than a cooperative framework.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All