In this Issue:

- The Pandemic Will Limit Economic Growth For Years To Come

- Travel and Tourism Prospects

- Bankruptcies: Calm Before the Storm?

It used to be that something headed upward on a steep path was said to be “going to the moon.” That may be too modest for the present day. There are currently three separate missions surrounding Mars: two in orbit and one (NASA’s Perseverance rover) on the ground. The new benchmark for celestial aspiration is mirrored in the financial markets, where some asset prices have pushed further and further into the stratosphere.

Closer to home, however, other trajectories are getting shallower. Long after vaccination is complete, the pandemic will still be placing downward pressure on the path of economic growth. As much as we’re looking forward to life after COVID-19, the consequences of what we’ve been through will be with us for a long time.

For the past four months, many have been breathing a sigh of relief at the prospect of a post-pandemic future. Vaccination programs are moving forward, and populations of major developed countries are expected to reach high levels of immunity in the second half of this year. Visions of indoor restaurant dining, pleasure trips and concert attendance are dancing in our heads. Life will finally, we hope, get back to normal.

But just as many COVID-19 survivors endure lingering medical difficulties, economies around the world may struggle to regain full health. The pandemic has not only hindered growth over the past year; it has hindered the ability of economies to expand over the much longer term.

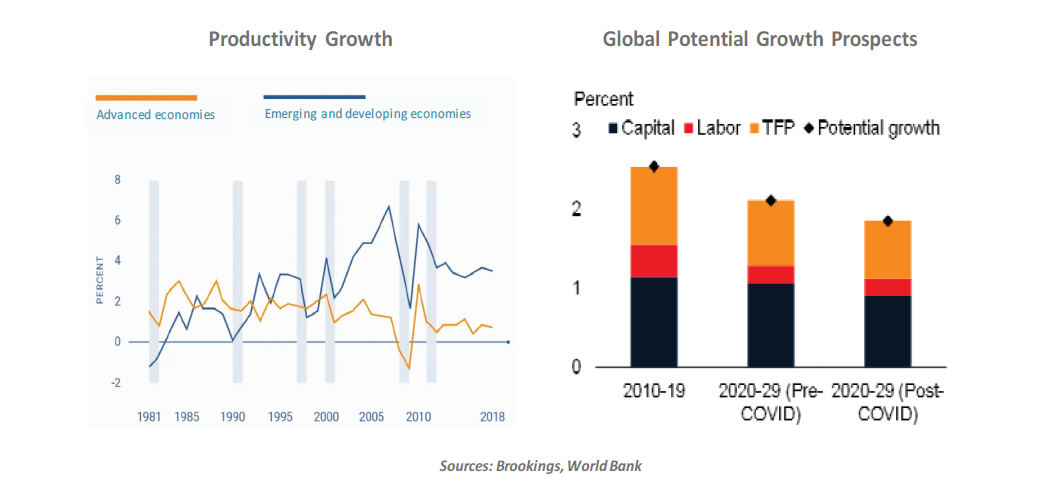

Potential economic growth is the combination of labor force growth and productivity growth. Both were moderating prior to the pandemic; aging societies and insufficient investment were to blame. And both will be impaired further in the post-COVID world.

Reopening after the pandemic is not going to happen suddenly, and it is not going to occur at the same time in all places. (As we discussed last week, uneven application of vaccinations is one reason why.) Global surveys suggest workers will take time to regain comfort with returning to crowded surroundings even after high levels of immunity are achieved. So, interactions within and across countries may remain hindered for a while.

Global supply chains are currently operating well below peak efficiency, and remain vulnerable to disruption if outbreaks recur in component countries. In addition, the pandemic has produced huge problems for global shipping, raising costs to a prohibitive level. Components and finished goods are not moving as quickly or as freely as they were two years ago, and it will take a long time for the system to run smoothly again.

|

COVID-19 will take a lasting toll on labor force growth and productivity growth.

|

With the virus still at large, and risk of contraction still present, workplaces will have to continue accounting for safety concerns. Plant floors, loading docks and cubicle farms will be structured accordingly, which may not be optimal from an output perspective.

These logistical problems will take time to solve, but they should be manageable. What may not be as manageable are the long-term impacts of the pandemic on productivity. Many students around the world have been attending school remotely for most of the past year, and the quality of distance education has ranged from passable to poor.

Some primary school children have checked out, due to a lack of structure or connectivity. At a higher level, reports indicate that nearly 17 million U.S. college students stopped their studies last year, at least temporarily. For some, the quality of remote learning did not match the prices being charged for it.

Losing a year of educational progress is not a minor issue. The formation and enhancement of human capital is central to invention and productivity. It is not clear how we can make up for the learning deferred by COVID-19.

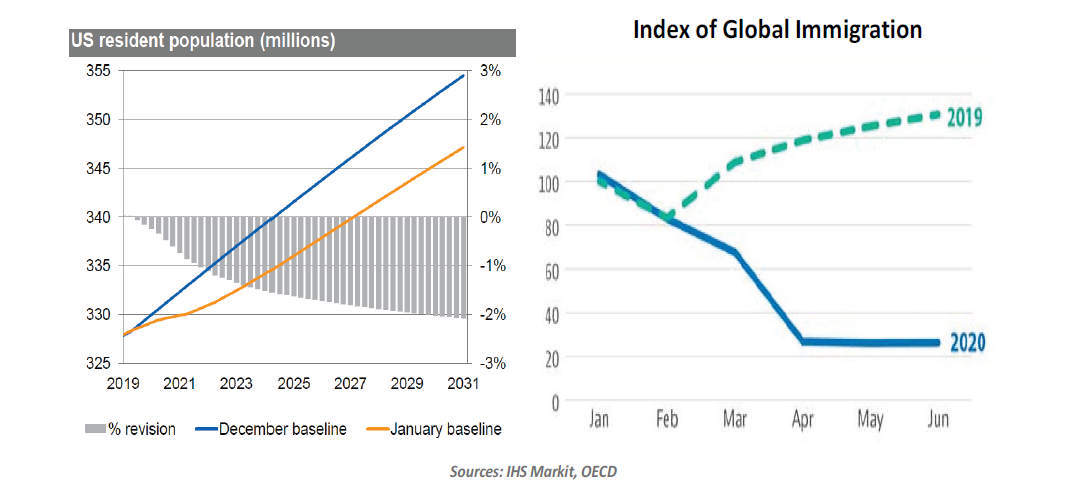

The pandemic has also taken a toll on labor forces around the world. About 2.5 million lives were lost during the first year of the pandemic, and an estimated 10% of those who have recovered are still dealing with lingering after-effects. Life expectancy has declined in many countries, and the pandemic has produced a baby bust. Projections of future population growth are being adjusted downward.

Immigration, a source of both labor force renewal and economic innovation, has been severely curtailed. Populist movements in many developed countries had led to diminished immigration prior to COVID-19, but the need to maintain public health during the pandemic made borders even less permeable. Reopening those borders may take a while, as countries seek to put their own citizens back to work and avoid re-importing new strains of the virus.

|

As expensive as pandemic support has been, more may be needed to limit long-term damage.

|

Another more subtle challenge to long-term economic growth is the increased difficulty in making public investments in human and physical capital that may result from two years of massive government deficits. Calls for austerity are already rising in many world capitals, even before the pandemic has been contained. As an example, the infrastructure initiative expected from U.S. President Joe Biden may not get a fair hearing amid the concerns over reflation. Failing to make productive investments will bound an economy’s ability to progress.

In sum, long-term growth prospects have suffered lasting damage during the pandemic. As a result, standards of living may not improve as expected, and debt may not be as sustainable. Markets that are growing more slowly may not attract the same level of inbound investment, which could further hinder prospects.

Studies of past pandemics routinely show negative effects that can last for decades afterwards. Growth and employment take a long time to recover, even when policy responses are generous. It seems unlikely that we can escape these consequences after COVID-19 is conquered.

The missions to Mars illustrate the apogee of human achievement. But back on Earth, the pandemic threatens to limit the altitude of economic performance. Persistent support from policy makers will be needed to overcome the gravity of the situation.

Grounded

As COVID-19 vaccines started rolling out, a profound sense of enthusiasm followed, especially among those of us who love to be on the road for business or leisure. Visits to travel websites increased, and the industry grew hopeful. But that optimism quickly faded: numbers of infections kept growing, new variants of the virus emerged, and immunizations got off to a slow start. Many governments have kept their borders and economies closed.

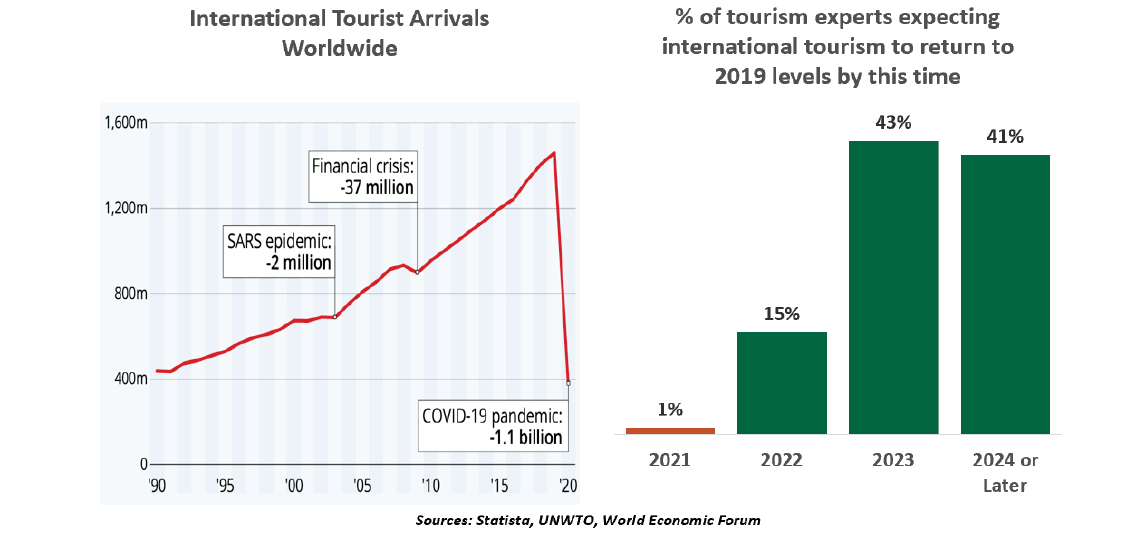

The pandemic has hit few industries harder than tourism. In the first half of 2020, tourist arrivals fell globally by more than 65%, compared with a decline of 8% during the global financial crisis and 17% during the SARS epidemic.

Outside of a brief recovery last summer, the industry has been struggling for the past year. Persistent travel restrictions have pushed the industry back to traffic levels last seen about three decades ago. International tourist arrivals declined by 74% year-over-year in 2020, a fall of 1.1 billion travelers. This translated to an estimated $1.3 trillion loss in tourism revenue globally.

The outlook for tourism remains difficult. According to multilateral institutions and industry experts, the industry will need up to four years to return to pre-pandemic levels of international tourist traffic and receipts. Though vaccines are promising, they are not an overnight cure for the broad challenges of COVID-19. As we wrote last week, vaccine nationalism is one factor. Uncertainty about the effectiveness of vaccines against new variants, as well as changing quarantine guidelines upon both arrival and return, will also keep travelers at bay.

As the market for travel reopens, leisure trips will rebound well ahead of business travel. This is a mixed outcome for airlines. Leisure travel accounts for the majority of airlines’ passenger volumes, but business travel is twice as profitable. According to the World Travel & Tourism Council, business travelers spent $1.4 trillion in 2018 on airlines, hotels, ground transportation, food and other services, with the U.S. and China alone accounting for half and Europe one-fifth of the remaining business travel spend. At best, business travel will recover slowly as employers stay cautious about endangering employees and receiving visitors. Demand may permanently decline as businesses adapt to virtual meetings and conferences.

|

It’s going to be a long road to recovery for the tourism industry.

|

Over the past decades, travel and tourism have grown in economic importance. Tourism activity is now a major source of employment and a key component of service exports. Among G20 nations, the travel sector accounts for about 10% of employment and gross domestic product on average. In some cases, the dependency is well above one-fourth of national output. Many island nations in the Caribbean and southeast Asia are almost entirely reliant on tourism. Several European economies, like Italy, Spain, France and Greece, will struggle to recover without a rebound in this vital sector.

According to research by the International Monetary Fund, a six-month severe disruption to hospitality and travel services would reduce the GDP by 2.5%-3.5% in G20 countries. The predicted losses to low- and middle-income economies were also significant.

The slower the recovery of tourism, the more lasting the damage to tourism-led communities and economies. Strong coordination among countries, including digitalization of COVID-19 screening and vaccination checks, will be essential to getting everyone back on their way.

Kicking the Bankruptcy Can

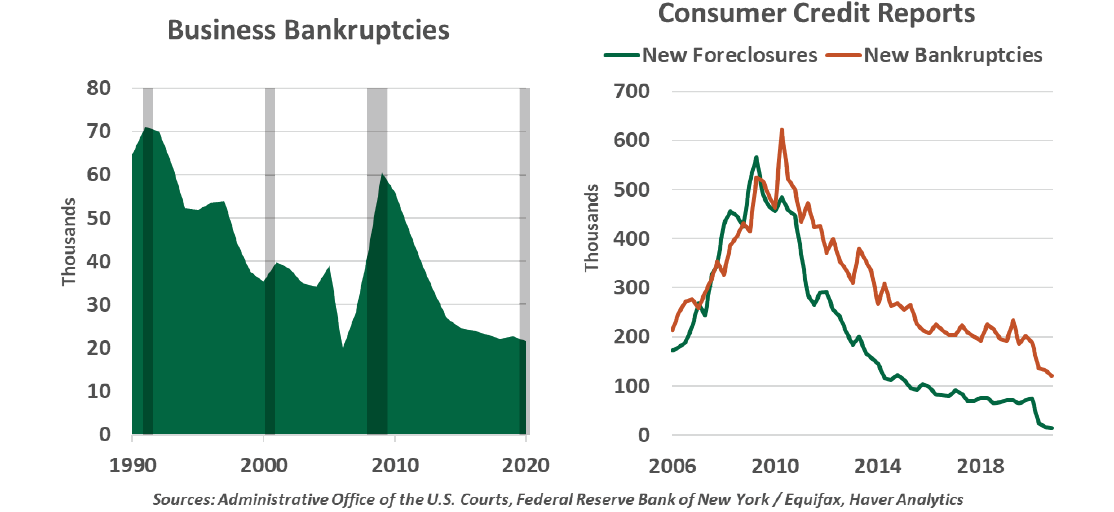

Recent policy interventions have been aimed at preventing the temporary disruption of COVID-19 from causing permanent economic damage. Some losses of revenues and payrolls have been inevitable, but that did not need to lead to lasting harm. By the measure of U.S. bankruptcy filings, these interventions have helped to stave off the worst outcomes, at least for now.

Bankruptcies provide a legal means for a debtor to move on from unaffordable obligations. Filings for individuals will curtail a consumer’s ability to borrow money for years to come, but will expunge most or all current liabilities. Corporate bankruptcies can mean a total liquidation that ends a business (chapter 7) or a reorganization in which debts are renegotiated (chapter 11), which can allow the business to survive.

Recessions predictably led to cyclical increases in bankruptcies, until 2020 again broke precedent.

|

Deferred debts will still come due.

|

Personal bankruptcy filings fell by more than 30% from 2019 to 2020 as consumers were given reprieves from financial obligations. Starting with the CARES Act in March 2020, student loan payments were deferred, mortgage payments could be postponed and tenant evictions were halted. These protections have allowed consumers to stay on top of their other obligations, leading to a record

decline in bankruptcy activity.

Business bankruptcies held steady in 2020 despite a volatile year. Some high-profile bankruptcy filings told the story of the recession, with car rental agencies, restaurant chains and brick-and-mortar retailers leading the headlines. However, the effects of the recession were idiosyncratic. Many businesses found themselves on the upward trend of the K-shaped recovery and were never close to bankruptcy.

The crisis is not over. Debts continue to accumulate. More than 5% of mortgage borrowers remain in forbearance and may find themselves unable to pay when these protections expire. The 18% of delinquent tenants will face eviction and lawsuits if they cannot resume payments—assuming their revenue-deprived landlords do not first file bankruptcy themselves. Businesses may yet face bankruptcy if the economy does not normalize as expected this year. The economy remains poised for a strong year ahead, and it will be needed to head off a delayed wave of bankruptcies.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2021 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

More Innovative ETFs Topics >