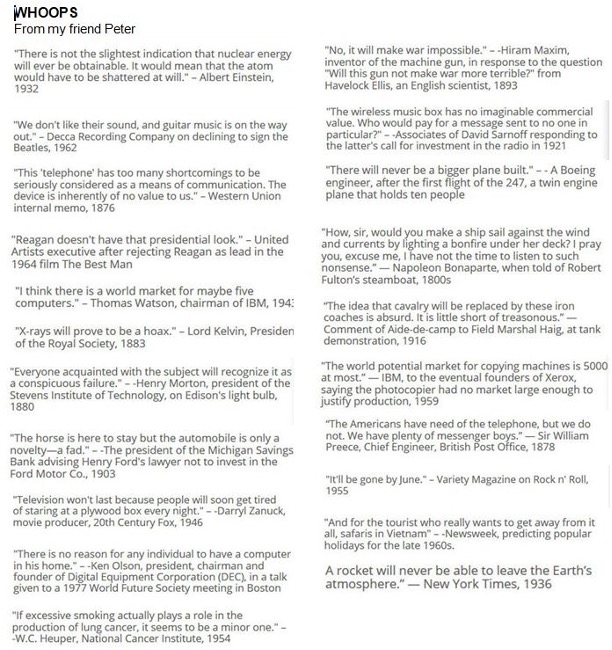

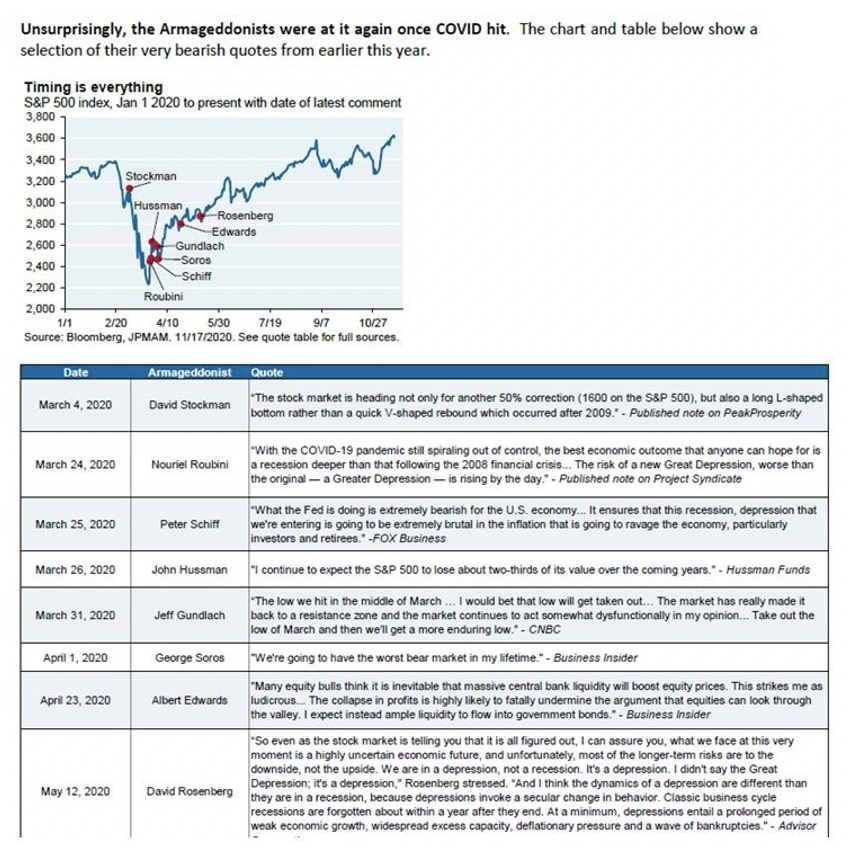

NewsLetter - February 2021

MONTE CARLO

We use Monte Carlo analysis extensively in our planning process. My friend Michael Kitces hit the nail on its head in his recent Newsletter.

“Why I advocate the use of Monte Carlo analysis. ‘I'd rather be vaguely right than precisely wrong.’

– Keynes”

GREAT ARTICLE, AS ALWAYS

In “You Can’t Handle the Truth,” Larry Swedroe once again, in his classic clear and understated style addresses an important investor reality – “over confidence.” For example, he offers the summary of a study “Why Inexperienced Investors Do Not Learn: They Do Not Know Their Past Portfolio Performance” where the authors analyzed the actual performance of the online brokerage accounts of individual investors.

● Investors are unable to give a correct estimate of their own past portfolio performance. The correlation coefficient between return estimates and realized returns was not distinguishable from zero.

● People overrate themselves. Only 30% considered themselves average. Investors overestimated their own performance by an astounding 11.5% a year. And portfolio performance was negatively related with the absolute difference between return estimates and realized returns – the lower the returns, the worse investors were when judging their realized returns. It seems likely investors are unable to admit how badly they have done. While just 5% believed they had experienced negative returns, the reality was that 25% had done so.

● On average, investors underperform relevant benchmarks. While the arithmetic average monthly return of the benchmark was 2.0%, the mean gross monthly return of investors was just 0.5%. And more than 75% of investors underperformed.

He concludes with “my personal favorite story on investor overconfidence. If anyone deserves to be confident of their skills, it seems logical it would be the members of the Mensa (high IQ group) investment club. The June 2001 issue of Smart Money reported that the Mensa investment club returned just 2.5% over the previous 15 years, underperforming the S&P 500 Index by almost 13% per year.” And offers “the moral of the tale.”

“It is important to measure your investment returns and also compare them to appropriate benchmarks. Doing so will force you to confront reality rather than allow an illusion to undermine your ability to achieve your financial objectives.”

You Can't Handle the Truth - Articles

NOT SO “SURE THINGS”

One more item from Larry

“Every January, I start keeping track of the predictions for the upcoming year I hear in the financial media and from advisors and investors. With the arrival of 2021, it’s time for my final review of how the 2020 forecasts played out.

As is my practice, I will give a score of +1 for a forecast that came true, a score of -1 for one that was wrong, and a 0 for one that was basically a tie.

Here is the final review of the nine sure things I was tracking:

1. U.S. economic growth will be durable enough to avoid a recession, but disappointing to those expecting improvement. GDP growth will slow from about 2.3% in 2019 to 1.8% in 2020, according to the Philadelphia Federal Reserve’s 2019 survey of professional forecasters. The coronavirus upended all economic forecasts. Its fourth quarter 2020 survey predicted full-year growth of -3.5%. Score -1.

2. Corporate profit growth will continue to be strong. S&P 500 companies’ earnings will reach a cumulative $178 per share, up from an estimated $162 for 2019, a 10% increase. As of September 24, the consensus forecast for the year was $136, a drop of 16%. Score -1.

3. While P/E multiple expansion is likely behind us, reduced trade tensions, easy monetary policy and strong earnings growth will produce high single-digit returns for U.S. stocks. Demonstrating that the economy and the stock market are very different things, the S&P 500 Index returned 18.4%. Despite the estimated 3.5% decline in GNP and the estimated 16% decline in earnings, the S&P 500 Index more than doubled the forecast. Score -1.

4. Inflation will remain tame. Vanguard’s Joe Davis wrote, “Secular drags, including globalization, technological innovation, and well-anchored inflation expectations have been keeping inflation contained in recent years; and we expect this to persist over the medium and long term.” The consensus forecast of professional economists in the Philadelphia Federal Reserve’s 2019 Survey was for the CPI to increase at just 2.1%. The market certainly agreed, as the spread between 10-year TIPS and 10-year nominal Treasury bonds was only about 1.8%. The Philadelphia Federal Reserve’s Fourth Quarter 2020

Survey forecasted full-year inflation of only 1.24. While the COVID crisis negatively impacted the first two sure things, it helped this one. Score +1.

5. With slowing economic growth and tame inflation, it’s safe to extend maturities. Futures markets show a much greater probability that the Fed funds rate will be lower at the end of the year (52%) than higher (just 2%). This is another forecast that was helped by the coronavirus. The Federal Reserve acted quickly to lower the Fed funds rate to effectively zero. Vanguard Long-Term Treasury Index Fund Admiral Shares (VLGSX) returned 17.7%, outperforming Vanguard’s Intermediate-Term Treasury Index Fund Admiral Shares (VSIGX), which returned 7.7%, and Vanguard’s Short-Term Treasury Index Fund Admiral Shares (VSBSX), which returned 3.1%. Score +1.

6. This sixth sure thing follows from the fifth. The interest rate environment favors REITs. Thus, investors should overweight them. Vanguard’s Real Estate Index Fund Admiral Shares (VGSLX) lost 4.7%, underperforming Vanguard’s 500 Index Fund Admiral Shares (VFIAX), which returned 18.4%. Score -1.

7. Large-cap stocks will continue to outperform small stocks, as they have over the last decade. The authors of the Harvard Business Review article, “The Gap Between Large and Small Companies Is Growing,” explained, “Large corporations are more and more likely to maintain their dominant positions, while small corporations are less and less likely to become big and profitable.” Vanguard’s Small Cap Index Fund Admiral Shares (VSMAX) returned 19.1%, underperforming Vanguard’s Large Cap Index Fund Admiral Shares (VLCAX), which gained 21.0%. Score +1.

8. With concerns over continued growing budget deficits combined with the outlook for accommodative monetary policies around the globe, gold will put in another strong performance. The SPDR Gold ETF (GLD) returned almost 24%. Score +1.

9. Climate change will lead to another year of significant losses to reinsurers. Thus, investors should avoid this asset class. Year-to-date returns have been positive. There are two publicly available reinsurance interval funds. Stone Ridge’s Reinsurance Risk Premium Interval Fund (SRRIX) returned 6.8% and the Pioneer ILS Interval Fund (XILSX) returned 7.4%. Score -1

Our final score was +4/-5. This was my 11th, and final, year of reporting on “sure things,” as the evidence has made the point that economic and market forecasts by gurus should be ignored. In the chart below that depicts the historical evidence, only about one third turned out to be true.

Apparently, sure things are not so sure. Keep this in mind the next time you are tempted to react to some forecast, either yours or anyone else’s. And be especially aware when a forecast agrees with your preconceived ideas, as confirmation bias can be a dangerous condition.

Final Review of 2020 “Sure Things” - Articles - Advisor Perspectives

TIRED OF YOUR CURRENT HOME?

From my friend, Judy

DB asks “DO these homes come with diapers, underpants and new pants?”

YOUR BRAIN ON STRESS

“RUN FOR THE HILLS! GET OUT WHILE YOU CAN! STAY AWAY UNTIL IT’S SAFE!”

“Behavioral finance experts at Oxford Risk, a London-based risk management software firm and consultancy, figured out just how costly it can be to heed the advice of your inner caps-lock voice. They calculated that increasing your allocation to cash can cause investors to underperform their less panicky peers by an average of 4% to 5% per year.

That range is what’s known as the “behavior gap” — the difference between the returns we earn when we make rational investment decisions versus moves driven by emotion, during times of stock market turmoil. Our vision narrows when we face a crisis. We intensely focus on the present and lose sight of the big picture.

On average, the behavior gap costs investors around 1.5% to 2% a year over time. That’s due to our propensity to invest more money when times are good and less when stocks are down. In a decidedly not normal year like we’re having now, the price is a lot higher when you let your feelings take over your trading behavior.”

Food for thought…..

Your Nerves Will Cost You 4% to 5% a Year In Investment Returns

GOBBLEDYGOOK

60/40 BLEND REQUIRES IMAGINATION IN TODAY’S ENVIRONMENT

From an article in Investment Advisor

“Traditional expectations of the 60/40 portfolio may be due for a rethink…Alternatives can provide that improvement without adding more risk.”

As the author is the president of 361 Capital: “We are a leading boutique asset manager focused on alternative solutions that seek to deliver meaningful alpha, manage risk and offer diversification.” Kind of makes one wonder if there might be some bias here.

MORE GURUS

MORE FOOD FOR THOUGHT

BETTER RATCHET UP YOUR GAME

If you believe you can beat the market with your clever trading strategy better keep an eye on the competition. Here’s an excerpt from a Wall Street Journal story.

High-Frequency Traders Push Closer to Light Speed With Cutting-Edge Cables

High-frequency traders are using an experimental type of cable to speed up their systems by billionths of a second, the latest move in a technological arms race to execute stock trades as quickly as possible…

Hollow-core fiber is the latest in a series of advances that fast traders have used to try to outrace their competition. A decade ago, a company called Spread Networks spent about $300 million to lay fiber-optic cable in a straight line from Chicago to New York, so traders could send data back and forth along the route in just 13 milliseconds, or thousandths of a second.

Within a few years the link was superseded by microwave networks that reduced transmission times along the route to less than nine milliseconds…

HFT firms have also used lasers to zip data between the data centers of the New York Stock Exchange and Nasdaq Inc., and they have embedded their algorithms in superfast computer chips. Now, faced with the limits of physics and technology, traders are left fighting over nanoseconds.

INCREDIBLE!

From my friend, Leon. No words to describe it. You just have to watch.

German Wonderland,started by two brothers as a place to show their hobby, began to grow by leaps & bounds. Soon they were joined by other 'Model Railroad Clubs' and other craftsmen. Some were electricians, model makers, carpenters, computer programmers. Their wives would stop by to see what they were doing and usually bring them lunch.

One thing led to another. Three of the ladies had worked at a bakery, several visitors would ask if they had a snack bar. The idea was planted; some of the carpenters came and built a nice restaurant area for the bakery and a kitchen, too. If the fresh coffee smell didn't get you, then the bakery definitely would. Over 400,000 man hours were spent making this dream come true.

EVEN MORE FOOD FOR THOUGHT FOR MARKET TIMERS

Researchers have amassed plenty of persuasive evidence in recent years showing that market timing—or moving in and out of stocks based on where you think the market is headed—often leads to lower returns.

But if that isn’t enough to convince you, perhaps this will: A new study finds that active trading also significantly increases the volatility of a portfolio. That is, market timers actually assume much more risk to get those lower returns, compared with investors who simply buy and hold investments.

A New Reason Investors Shouldn’t Try to Time the Stock Market - WSJ

2020

From my friend, Freddie

GURUS

One more bites the dust

York Capital Management’s hedge funds were flailing.

Its credit hedge fund, which lost $700 million on energy bets gone wrong, was down about 50% since 2018. Other York hedge funds were also in the red.

Longtime partners were leaving the firm and weren’t being replaced. Resentment simmered among some inside the firm that the head of York’s Asia hedge fund, a bright spot the last several years, wanted more money for his team and had threatened to leave, according to current and former employees.

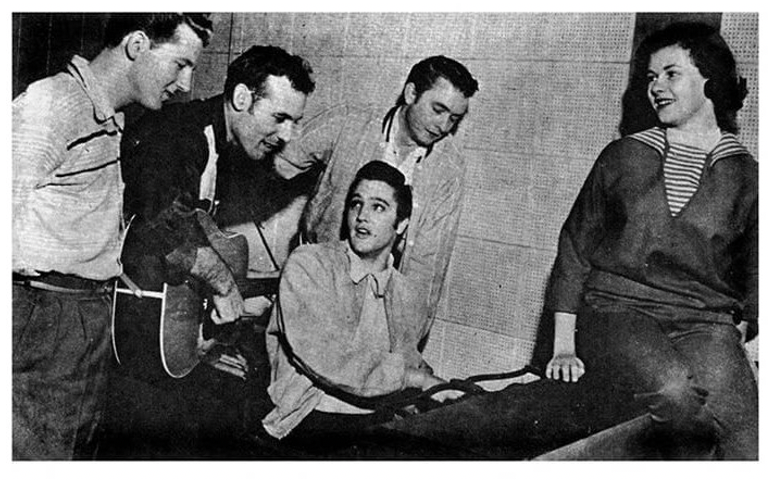

AN AMAZING BIT OF HISTORY

For those of you old enough to recognize the names.

December 4, 1956

Jerry Lee Lewis | Carl Perkins | Johnny Cash | Elvis Presley

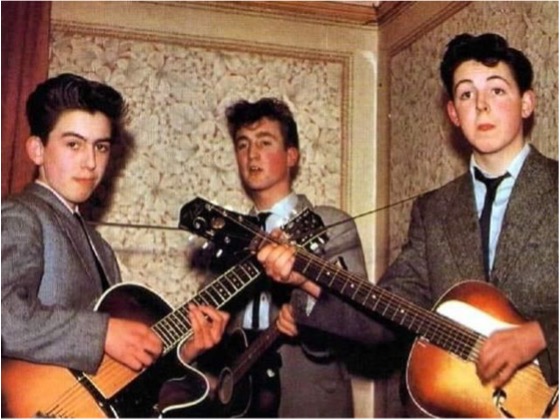

THE QUARRYMEN, 1957.

George was 14, John 16 and Paul 15.

SOOTHSAYER

MORE OLD PEOPLE

From my friend, Peter

George Phillips, an elderly man from Walled Lake, Michigan, was going up to bed, when his wife told him that he'd left the light on in the garden shed, which she could see from the bedroom window. George opened the back door to go turn off the light, but saw that there were people in the shed stealing things.

He phoned the police, who asked, "Is someone in your house?"

He said, "No, but some people are breaking into my garden shed and stealing from me."

Then the police dispatcher said, "All patrols are busy, you should lock your doors and an officer will be along when one is available."

George said, "Okay." He hung up the phone and counted to 30. Then he phoned the police again.

"Hello, I just called you a few seconds ago because there were people stealing things from my shed. Well, you don't have to worry about them now because I just shot and killed them both; the dogs are eating them right now," and he hung up.

Within five minutes, six police cars, a SWAT team, a helicopter, two fire trucks, a paramedic and an ambulance showed up at the Phillips' residence, and caught the burglars red-handed.

One of the policemen said to George, "I thought you said that you'd shot them!" George said, "I thought you said there was nobody available!"

*********************

GETTING OLDER.

A distraught senior citizen phoned her doctor's office. "Is it true," she wanted to know,

"that the medication you prescribed has to be taken for the rest of my life?"

"'Yes, I'm afraid so,"' the doctor told her.

There was a moment of silence before the senior lady replied, "I'm wondering, then,

just how serious is my condition because this prescription is marked 'NO REFILLS'.."

***********************

An older gentleman was on the operating table awaiting surgery and he insisted that his son,

a renowned surgeon, perform the operation.

As he was about to get the anesthesia, he asked to speak to his son. "Yes, Dad, what is it?"

"Don't be nervous, son; do your best, and just remember, if it doesn't go well,

if something happens to me, your mother is going to come and

live with you and your wife... "

********************

When you are dissatisfied

and would like to go back to youth, think of Algebra.

DEPRESSING BUT NOT SURPRISING

Excerpts from S&P’s Persistence Scorecard

Do investment results come from skill or luck? Genuine skill is likely to persist, while luck is random and fleeting. Thus, one measure of active management skill is the consistency of a fund’s performance relative to its peers.

The Persistence Scorecard attempts to distinguish luck from skill by measuring the consistency of active managers’ success. This report shows that, regardless of asset class or style focus, active management outperformance is typically short-lived, with few fund managers consistently outperforming their cohorts.

For example, of the domestic equity funds that finished in the top half in terms of cumulative returns for the period from June 2010 to June 2015, 38.6% replicated that accomplishment during the period from June 2015 to June 2020. In fact, it was more likely for a top-half fund to close its doors or change its style (41.5% combined) than repeat its performance in the top half.

At first glance, there were some signs of performance persistence when narrowing the measurement intervals to consider annual consistency. Of the top-quartile domestic equity funds in June 2018, 35.5% managed to stay in the top quartile annually through June 2020.

However, this persistence was inconsistent and decayed over time. Rewinding the clock two years, just 1.6% of domestic equity funds in the top quartile as of June 2016 maintained that status annually through June 2020.

FRIGHTENING!

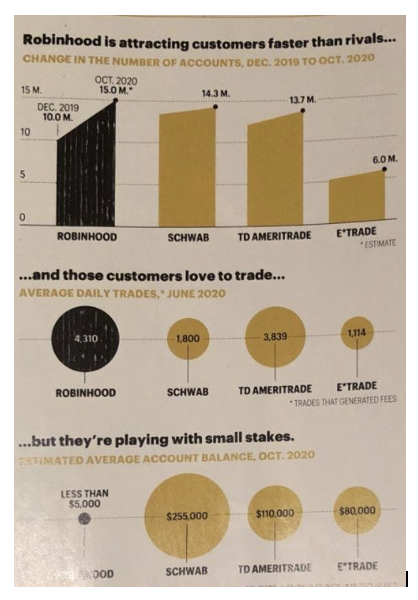

Is Robinhood The Hero That Today’s Investors Need?

Excerpts from an article in Financial Advisor

The investing app says that half of its new users this year have been first-time investors, and the average age of its user is 31.…. It places sophisticated tools like options and cryptocurrencies just a few clicks and swipes away from most users, and the guidance on how to use these more complex securities isn’t easy to find…There are signs that Robinhood’s customers are trading more. The New York Times reported that the app’s users traded 40 times as many stock shares and 88 times as many options contracts as Charles Schwab customers.

Not a “hero” but akin to putting a loaded machine gun in the hands of a toddler. Overconfidence run amuck. As the S&P Persistence Scorecard shows, if professionals have trouble beating the markets, naïve Robinhood investors will be poster children for “a fool and his money is easily parted.”

The only good news (provided by my friend, Taft) is Robinhood “investors” have less to lose.

The bad news is it’s probably their whole nest egg.

MORE ON ROBINHOOD

From my friend, Rick

Excerpts and good common-sense advice

“Robinhood revolutionized the way small and younger investors can buy and sell stocks, options, and cryptocurrency by eliminating minimum purchases and trading fees. The app, with its name implying it takes from the rich and gives to the poor, makes it easy and fun for anyone to invest.

How does a free app make money? Saloons of the 1890s gave away a lunch with every drink purchased. The free food was heavily salted, which resulted in the patrons buying a lot more high-priced beer than they planned.

Similarly, Robinhood used the concept of a heavily salted "free lunch" by using gaming-type experiences that encouraged their customers to trade more frequently and invest in higher-risk investments like bitcoin and options, all of which made the company more money.

Robinhood made much of their money by auctioning off their customer’s trading orders to the firm that would pay them the most money, resulting in the worst deal on pricing for their customers. The SEC said Robinhood’s customers paid over $34 million more than they would have paid with other brokerage firms that charged fees.

What got Robinhood into trouble with the SEC was misleading consumers by not disclosing that customers paid the highest possible prices for the shares they purchased and received the lowest price for those they sold. The company agreed to pay a $65 million fine to settle the charges…

Before you sign on for financial products or services that are "free," clarify how the company or person is making their money. If the answer is not clear and understandable, move on. The chances are that you'll end up with the lowest overall cost by paying a fully transparent and disclosed fee.

Because Grandpa was right. There's no such thing as a free lunch.”

WHERE DID THAT COME FROM?

A SHOT OF WHISKEY

In the old west a .45 cartridge for a six-gun cost 12 cents, so did a glass of whiskey. If a cowhand was low on cash he would often give the bartender a cartridge in exchange for a drink.

This became known as a "shot" of whiskey.

THE WHOLE NINE YARDS

American fighter planes in WW2 had machine guns that were fed by a belt of cartridges. The average plane held belts that were 27 feet (9 yards) long.

If the pilot used up all his ammo he was said to have given it the whole nine yards. SHIP STATEROOMS

Traveling by steamboat was considered the height of comfort. Passenger cabins on the boats were not numbered. Instead they were named after states.

To this day cabins on ships are called "staterooms." OVER A BARREL

In the days before CPR, a drowning victim would be placed face-down over a barrel and the barrel would be rolled back and forth in an effort to empty the lungs of water.

It was rarely effective, hence, if you are over a barrel you are in deep trouble.

HOGWASH

Steamboats carried both people and animals. Since pigs smelled so bad they would be washed before being put on board.

The mud and other filth that was washed off was considered useless "hogwash." HOT OFF THE PRESS

As the paper goes through the rotary printing press friction causes it to heat.

Therefore, if you grab the paper right off the press, it’s hot. The expression means: to get immediate information.

WHAT 2020’S PERFORMANCE SCOREBOARD TELLS US ABOUT THE WISDOM OF SHORT-TERM TRADING

Excerpts from Mark Hulbert’s excellent article. Mark is unquestionably the most credible observer of the performance of investment newsletters having launched his Hulbert Financial Digest in 1980. He is now a columnist for MarketWatch.

The reason I’m asking this age-old question now is that, if trading ever were a good idea, it should show up in 2020’s performance. A trader who got out of equities at the February high and back in at the March low would now be sitting on a year-to-date gain of over 70%. That compares to a gain of “just” 14% for buying and holding…

Of course, this year also presented plenty of opportunities to stumble. A trader who waited until the March low to shift from equities to cash, and who has been out of the market ever since, would be sitting in a greater-than-30% loss position in early December…

To find out how traders actually navigated 2020’s high-risk/high-opportunity environment, I analyzed the numerous investment newsletter portfolios whose track records my firm audits. I wanted to see if these real-world portfolios were ahead or behind where they would have been had they undertaken no trades since the beginning of the year.

To do that, I created a hypothetical portfolio for each of these actual portfolios that was an exact copy as of the beginning of this year—and which made no subsequent changes. If this hypothetical “frozen” portfolio is today worth just as much or more than its corresponding real-world portfolio, then we know its trading didn’t add value.

That turned out to be the case in slightly more than half of the portfolios my firm monitors—52%, to be exact. What conclusion can we draw from this? On the one hand, this percentage is lower than in other years in which I conducted a similar test on investment

newsletters. So to that extent, traders can take some solace that in a year like 2020 there are somewhat increased odds of success. On the other hand, this percentage is still above 50%. That means the odds are still against your being able to add value from your trading.

Taxes

An additional result is relevant to those of you who trade equities in a taxable portfolio. Above and beyond the 52% mentioned above, an additional 17% of the portfolios are ahead of their frozen analogues by less than 5 percentage points. That’s worth mentioning because my firm’s performance calculations do not take taxes into account. So on an after-tax basis, it’s very likely that these additional 17% would be behind where they would have been had they stuck with what they were recommending at the beginning of the year. That would mean that just 31% of the portfolios added value on an after-tax basis through their trading.

It’s also worth remembering that the investment newsletters on whose portfolios I conducted this test have stellar long-term records. That’s not an accident. In 2016, when my performance-tracking firm adopted a new business model in which newsletters paid a flat fee to have their track records audited, only those services with the best long-term returns were interested in participating.

I think it’s telling that, even among the advisers with the very best long-term records, the odds are against them when they try to add value through short-term trading. And this is true even in a year like 2020 in which there is such opportunity for such trading to add value.

What 2020’s performance scoreboard tells us about the wisdom of short-term trading

INTERESTING MAPS

From Judy

INVESTING JUST BEFORE A MARKET CRASH

Courtesy of my associate, Marcos

RETIREMENT PLANNING DURING COVID

An interesting survey from Kiplinger from my friend, Taft

How has the global COVID-19 pandemic changed your confidence about having enough income to retire comfortably?

● My confidence hasn’t changed: 40%

● I’m somewhat less confident: 27%

● I’m far less confident: 16%

● I’m far more confident: 10%

● I’m somewhat more confident: 7%

A number of retirement savers fell even further behind by tapping their retirement accounts for living and other expenses: nearly 60% of respondents took a withdrawal or loan from their retirement accounts in 2020. However, even as the stock market was touching new highs, investment mixes reported in the poll were very conservative. Stocks accounted for just 36% of the average allocation, and cash made up a whopping 24% of portfolios.

How has the pandemic and its financial impact changed your retirement plan?*

● I plan to work longer: 35%

● I plan to save more: 34%

● I plan to curtail travel or other activities I expected to do in retirement to save money: 20%

● I changed my retirement financial projections: 12%

● I will claim Social Security benefits earlier than I originally planned: 8%

● I decided to hire a professional adviser: 7%

● My plan hasn’t changed; I will keep doing what I’m doing: 34% How worried are you about recent stock market volatility?

● Somewhat worried: 47%

● Very worried: 27%

● Not worried: 26%

The poll, conducted in early November, surveyed a national sampling of 744 people ages 40 to 74, none of whom were fully retired, who had at least $50,000 in retirement savings. The median amount saved for retirement among all of the respondents was $188,800. The respondents were equally divided between men and women.

What is the current asset allocation for your investment portfolio or retirement accounts?

● Stocks: 36%

● Cash: 24%

● Bonds: 17%

● Real estate investments: 12%

● Other: 11%

How much did you withdraw from your retirement accounts?

● Less than $25,000: 17%

● $25,000 to $49,999: 27%

● $50,000 to $74,999: 24%

● $75,000 to $100,000: 32%

Which of these statements best describes your response to the bear market early in 2020?

● I did nothing and waited for the market to recover: 54%

● I changed my asset allocation to be more conservative: 19%

● I purchased more stock when prices fell: 13%

● I sold some investments to boost my cash position: 9%

● I sold all my stocks but have since reinvested at least a portion of my assets in the market: 4%

● I sold all my stocks and have not yet reinvested: 2%

A provision in the CARES Act allows people under age 59½ affected by the coronavirus to take a distribution of up to $100,000 from an IRA, 401(k), or similar account without penalty. 31.4% took a distribution from their retirement account, and 27.4% took a loan from their retirement account.

How much did you borrow from your retirement accounts?

● Less than $25,000: 14%

● $25,000 to $49,999: 28%

● $50,000 to $74,999: 27%

● $75,000 to $100,000: 31%

What did you use the money for?*

● Living expenses: 63%

● Medical bills: 41%

● Home repairs: 32%

● Auto: 26%

● College tuition: 23%

● Helping family members: 21%

A Kiplinger-Personal Capital Poll: Retirement Planning During COVID

OUT OF THE MOUTH OF BABES

Thanks to Judy for this

An elementary school teacher had twenty-six students in her class.

She presented each child in her classroom the 1st half of a well-known proverb and asked them to come up with the remainder of the proverb.

It's hard to believe these were actually done by first graders. Their insight may surprise you.

While reading, keep in mind that these are first-graders, 6-years-old, because the last one is a classic!

1. Don't change horses until they stop running.

2. Strike while the bug is close.

3. It's always darkest before Daylight Saving Time.

4. Never underestimate the power of termites.

5. You can lead a horse to water but how?

6. Don't bite the hand that looks dirty.

7. No news is impossible.

8. A miss is as good as a Mr.

9. You can't teach an old dog new math.

10. If you lie down with dogs, you'll stink in the morning.

11. Love all, trust me.

12. The pen is mightier than the pigs.

13. An idle mind is the best way to relax.

14. Where there's smoke there's pollution.

15. Happy the bride who gets all the presents.

16. A penny saved is not much.

17. Two's company, three's the Musketeers.

18. Don't put off till tomorrow what you put on to go to bed.

19. Laugh and the whole world laughs with you, cry and

you have to blow your nose.

20. There are none so blind as Stevie Wonder.

21. Children should be seen and not spanked or grounded.

22. If at first you don't succeed get new batteries.

23. You get out of something only what you see in the picture on the box.

24. When the blind lead the blind get out of the way.

25. A bird in the hand is going to poop on you.

And the WINNER and last one!

26. Better late than pregnant.

SMILES

From Judy & Peter

DON’T BE SCARED

From my friend Professor Sid Mittra’s blog

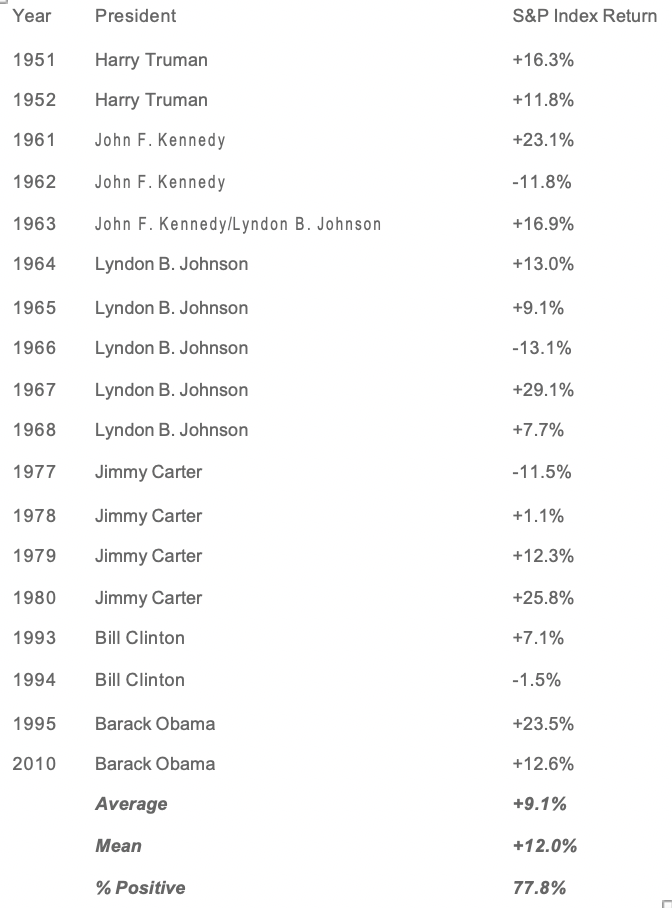

Should A Democrat Presidency Scare Markets? Probably Not

S&P 500 Index Returns When Democrats Controlled The White House and Congress

Source: LPL Research, FactSet 01/06/20 (1950 – Current)

Sid Mittra

THEY'RE BACK!

From my friend, Saby

Those wonderful church bulletins! These sentences actually appeared in church bulletins or were announced at church services:

The Fasting & Prayer Conference includes meals.

Ladies, don't forget the rummage sale. It's a chance to get rid of those things not worth keeping around the house. Bring your husbands.

Don't let worry kill you off - let the Church help.

Miss Charlene Mason sang 'I will not pass this way again,' giving obvious pleasure to the congregation.

Next Thursday there will be try-outs for the choir. They need all the help they can get.

Irving Benson and Jessie Carter were married on October 24 in the church. So ends a friendship that began in their school days.

A bean supper will be held on Tuesday evening in the church hall. Music will follow.

At the evening service tonight, the sermon topic will be 'What Is Hell?' Come early and listen to our choir practice.

Pot-luck supper Sunday at 5:00 PM - prayer and medication to follow.

Low Self Esteem Support Group will meet Thursday at 7 PM. Please use the back door.

The eighth-graders will be presenting Shakespeare's Hamlet in the Church basement Friday at 7 PM. The congregation is invited to attend this tragedy.

Weight Watchers will meet at 7 PM at the First Presbyterian Church. Please use large double door at the side entrance.

And this one just about sums them all up

The Associate Minister unveiled the church's new campaign slogan last Sunday: 'I Upped My Pledge - Up Yours.'

QUESTIONS AND ANSWERS FROM AARP FORUM

Thanks to Leon

Q: Where can single men over the age of 70 find younger women who are interested in them?

A: Try a bookstore, under Fiction.

Q: What can a man do while his wife is going through A: Keep busy. If you're handy with tools, you

menopause?

Q: How can you increase the heart rate of your over-70 year-old husband?

can finish the basement. When you're done, you will have a place to live.

A: Tell him you're pregnant.

Q: How can you avoid that terrible curse of the elderly A: Take off your glasses. wrinkles?

Q: Seriously! What can I do for these crow's feet and all those wrinkles on my face?

Q: Why should 70-plus year old people use valet parking?

Q: Is it common for 70-plus year olds to have problems with short term memory storage?

A: Go braless. It will usually pull them out.

A: Valets don't forget where they park your car

A: Storing memory is not a problem. Retrieving it is the problem.

Q: As people age, do they sleep more soundly? A: Yes, but usually in the afternoon.

Q: Where should 70-plus year olds look for eyeglasses?

A: On their foreheads.

Q: What is the most common remark made by 70-plus A: "Gosh, I remember these!" year olds when they enter antique stores?

LAST MINUTE ADDITION

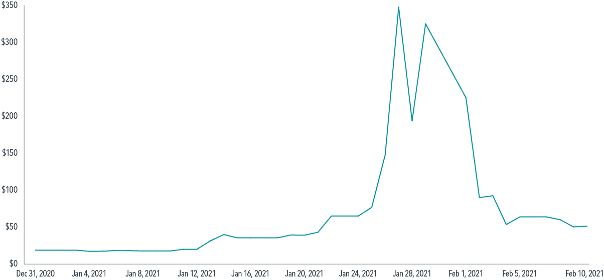

CRAZY WORLD

Market Prices Can Change Rapidly

Closing price of GameStop (GME) from December 31, 2020–February 10, 2021

At its closing peak on January 27, 2021, GameStop had a market capitalization of $24.2 billion, making it larger than over 200 of the constituents of the S&P 500 Index and as large as Whirlpool and American Airlines combined.

I agree with David Booth, Executive Chairman and Founder of DFA. “Think Investing Is a Game? Stop… This is probably a good time to mention that investing and gambling are not the same thing… Investing is a lifelong journey. Making money slowly is much better than making—then losing—money quickly.”

FROM MY COUSIN FRAN

This is what 'I can wait' looks like

Hope you enjoyed it. STAY SAFE!

Harold Evensky Founder

Evensky & Katz / Foldes Financial Wealth Management

Disclaimer:

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz / Foldes Financial Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Evensky & Katz / Foldes Financial Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Evensky & Katz / Foldes Financial Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Evensky & Katz / Foldes Financial Wealth Management client, please remember to contact Evensky & Katz / Foldes Financial Wealth Management, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Evensky & Katz / Foldes Financial Wealth Management’s current written disclosure statement discussing our advisory services and fees is available upon request.

© Evensky & Katz / Foldes Financial Wealth Management