Franklin Small Cap Value Fund Portfolio Manager Steve Raineri discusses why he thinks the near-record underperformance of higher- quality, profitable small-capitalization (small-cap) value stocks relative to lower-quality, unprofitable companies could present a compelling opportunity for longer-term investors as the US economy continues to recover from the COVID-19 pandemic.

During a broad COVID-19 equity market selloff in March and April, US small-cap stocks were hit particularly hard.1 At the time, many investors seemed especially concerned about how these companies would fare in a US economic slowdown.

Since then, many small-cap stocks, as represented by the Russell 2000 Index, have rallied from April’s lows as the US government and Federal Reserve’s rapid response to the COVID-19 crisis helped lift markets. Small-cap stocks especially benefited from the development of multiple vaccines and hopes for fiscal stimulus; quarterly performance was the best on record, allowing the index to reach all-time highs.2 However, lower-quality, less-profitable companies have largely driven it. Given the index’s most recent performance, some investors have asked us for our views on a potential sustained rally in small-cap stocks.

While we remain optimistic regarding the outlook for small-cap stocks, with the returns from unprofitable companies far in excess of profitable ones and near historical extremes3 (see charts under Reason #3), we believe investors should begin to focus on quality at this point in the cycle. Here, we outline five reasons we think small-cap stocks, particularly those with quality characteristics, are worth considering.

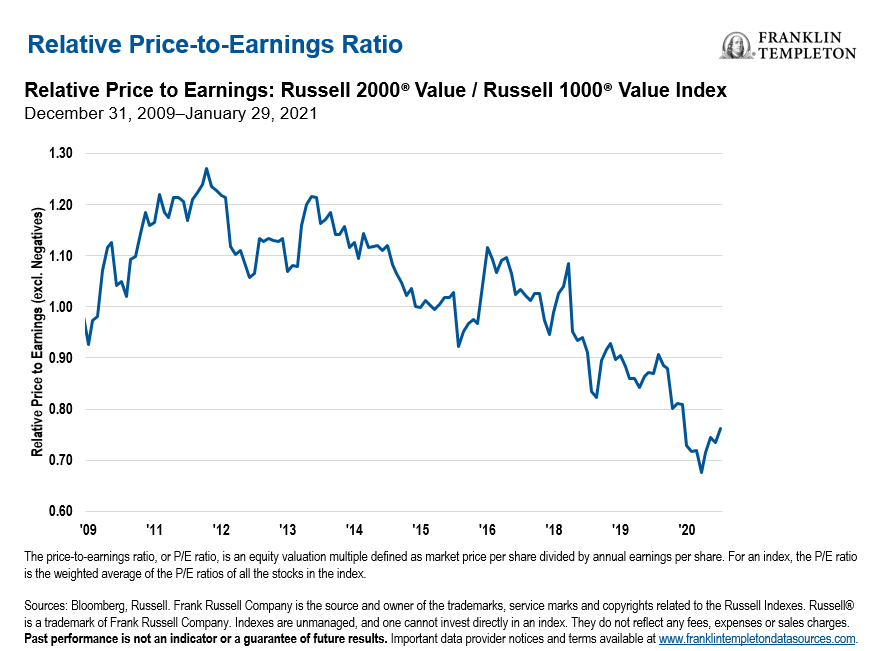

Reason # 1: Compelling Valuations

Despite a bounce off the lows, at the end of January 2021, small-cap value stocks in the Russell 2000 Value Index were trading near their lowest levels in 10 years, compared to the large-cap value stocks in the Russell 1000 Value Index, as measured by price-to-earnings (P/E) ratios.4 See chart below.

We see a few reasons for this difference in valuations, including the belief mentioned above that all small-cap stocks are more susceptible to a US economic downturn. While that’s true for many stocks in the Russell 2000 Value Index, it’s not true for all of them, particularly select small-cap value stocks with higher margins, lower leverage and decent earnings growth.5

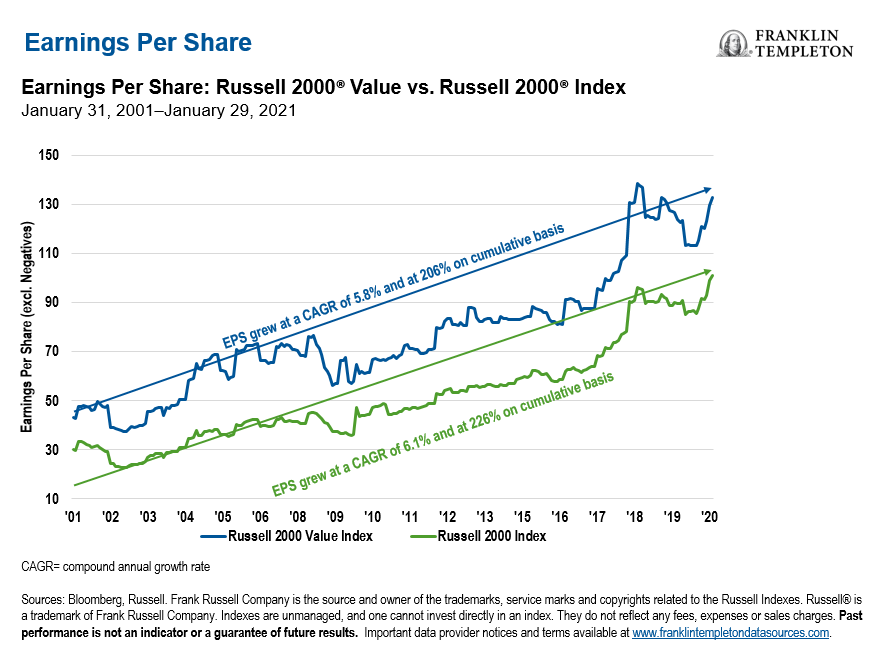

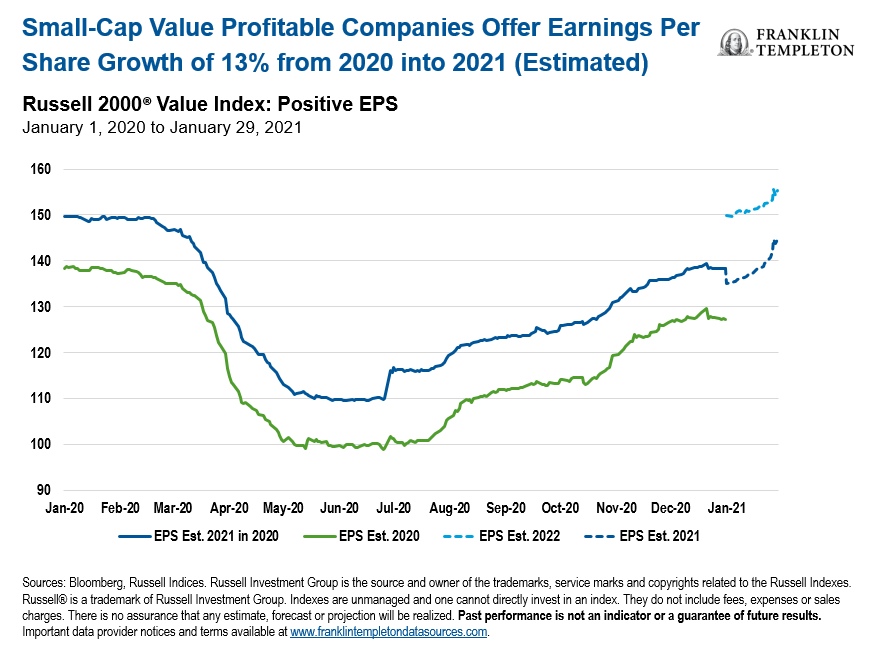

Reason #2: Earnings Growth Potential of Profitable Companies Is Double the Long-term Trend

As value investors, we seek to avoid unprofitable and structurally challenged companies, and look for companies with positive earnings growth potential. Excluding negative-earning companies, earnings per share for companies in the Russell 2000 Value Index grew at a compound annual growth rate of approximately 5.8% for the 10-year period ended January 31, 2021.6 Perhaps more importantly, analysts’ forecasts for profitable companies are expected to be approximately 13% in 2021, more than double the historical trend.7

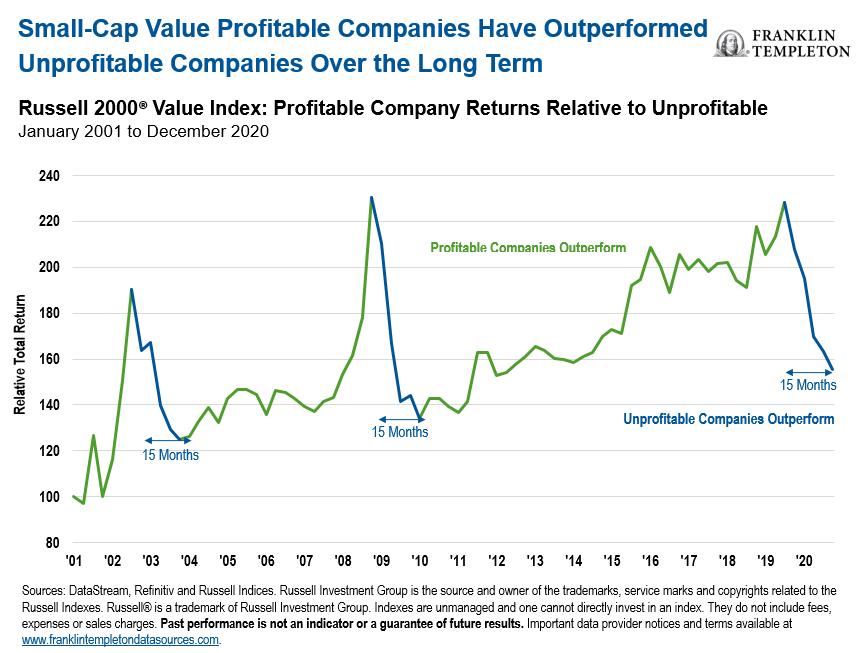

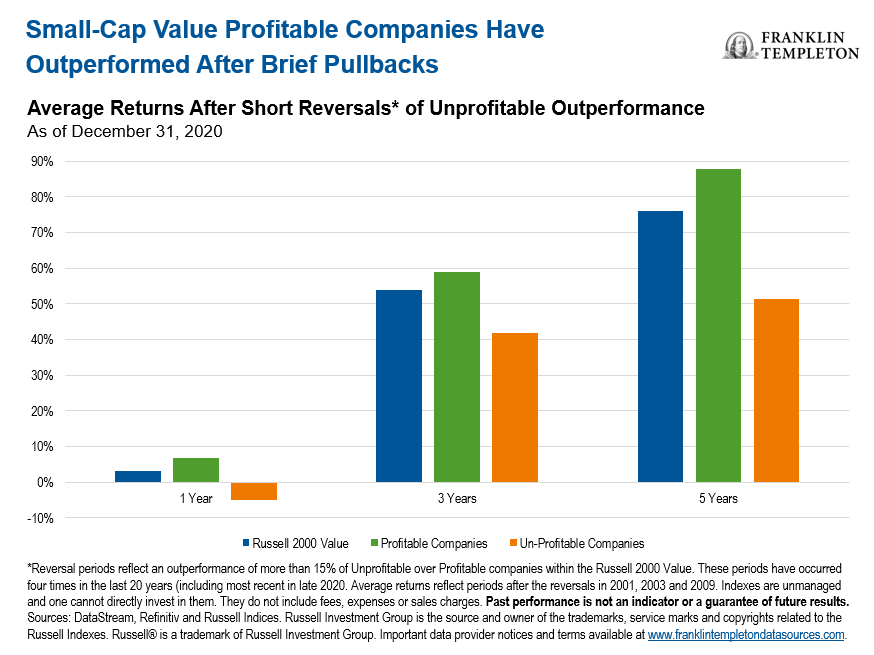

Reason #3: Quality Small-Cap Companies Have Lagged and Are Attractive

Over the past 15 months, quality small-cap companies (as measured below by profitability) have materially lagged negative earners to an extent only seen two other times in the past 20 years. According to our research, based on these prior experiences, returns from purchasing profitable companies have exceeded unprofitable ones by a wide margin and have also outperformed the benchmark.

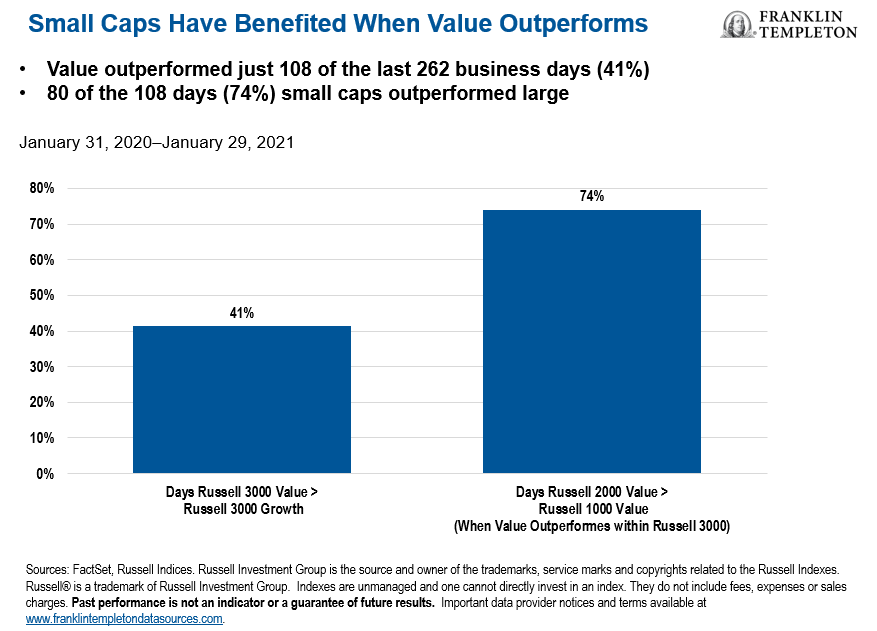

Reason #4: Performance During Value Stock Rallies

According to our analysis of companies in the Russell 1000, 2000 and 3000 indexes, value stocks only outperformed growth stocks 41% of the trading days in the 12 months ended January 31, 2021.8 However, on those days when value stocks outperformed growth, small-cap value stocks have outperformed large-cap value 74% of the time.

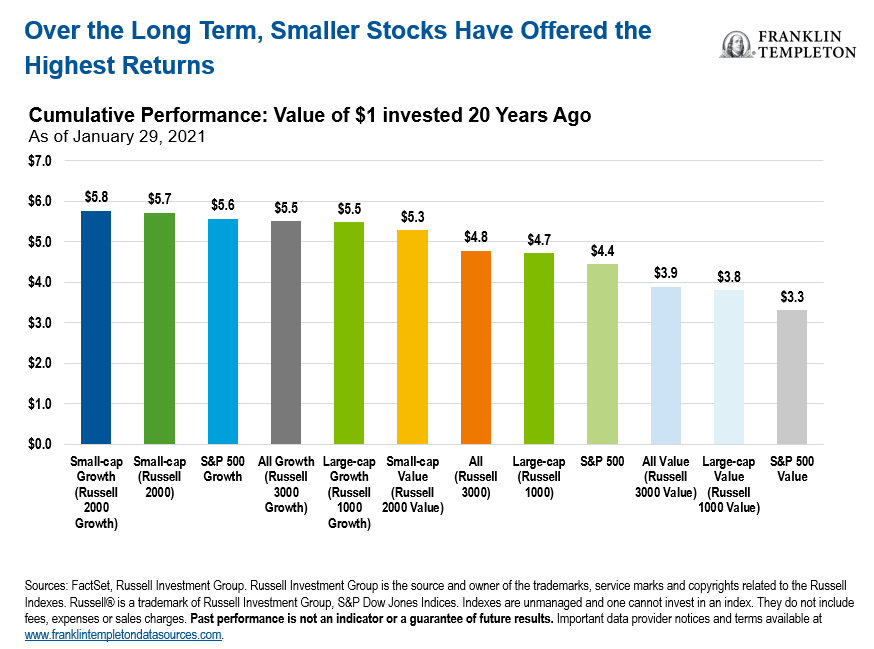

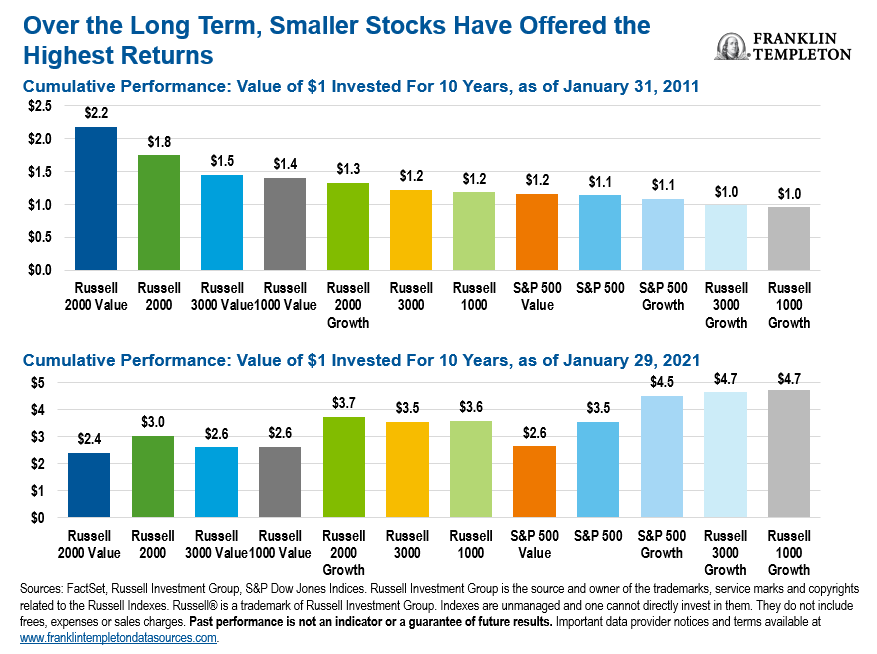

Reason #5: Performance Over Past 20 Years

Despite the record-breaking equity market performance in the fourth-quarter 2020, over the past decade, investors have generally favored large-cap stocks compared to smaller ones. That said, small-cap value stocks have been among the best performers over the 20 years ended January 31, 2021. In addition, if you divide the 20-year period into two 10-year periods, our research indicates that $1 invested in small-cap value stocks would have risen in value during both periods, while $1 invested in the S&P 500 Index for the 10 years ending January 31, 2011, would have resulted in a very modest return.9

Investment Implications

In our view, while market sentiment has favored small-cap value stocks more recently, lower quality, less-profitable companies have driven performance to an extent only seen two other times in the past 20 years. As a result, we believe this is creating a compelling opportunity to purchase higher-quality, historically profitable small-cap value companies at attractive prices, which fits well with our investment philosophy.

Specifically, our approach as a group is to invest in businesses that have a track record of success. We look for companies with shareholder-friendly governance and low leverage, which are trading at what we think are low prices relative to their earnings potential and where we see attractive return potential over the long-run. We believe this investment approach constitutes our competitive advantage and can potentially offer both meaningful upside potential and a degree of downside protection in periods of financial market turbulence.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

This information is intended for US residents only.

What Are the Risks?

Franklin Small Cap Value Fund

All investments involve risks, including possible loss of principal. The fund’s investments in smaller-company stocks carry special risks as such stocks have historically exhibited greater price volatility than larger-company stocks, particularly over the short term. Value securities may not increase in price as anticipated or may decline further in value. Additionally, smaller companies often have relatively small revenues, limited product lines and a small market share. In addition, the fund may invest up to 25% of its total assets in foreign securities, which involve special risks, including currency fluctuations and economic and political uncertainty. REITs may be affected by any change in the value of the properties owned and other factors, and their prices tend to go up and down. These and other risks are detailed in the fund’s prospectus.

Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. Download a prospectus, which contains this and other information. Please carefully read a prospectus before you invest or send money.

1. We define small-cap companies as those with market caps not exceeding either: the highest market cap in the Russell 2000 Index; or the 12-month average of the highest market cap in the Russell 2000 Index. Indexes are unmanaged and one cannot invest in an index. They do not include fees, expenses or sales charges.

2. Past performance is not an indicator or guarantee of future results.

3. Sources: DataStream, Refinitiv and Russell Indices. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. Indexes are unmanaged and one cannot invest in an index. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

4.The price-to-earnings ratio, or P/E ratio, is an equity valuation multiple defined as market price per share divided by annual earnings per share. For an index, the P/E ratio is the weighted average of the P/E ratios of all the stocks in the index. Indexes are unmanaged and one cannot directly invest in an index. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results.

5. Source: Russell Indices. Value stocks represented by the Russell 2000 Value Index. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses and sales charges. Past performance is not an indicator or guarantee of future performance. Additional data provider information available at www.franklintempletondatasources.com.

6. Past performance is not an indicator or guarantee of future results.

7. Sources: Bloomberg, Russell Indices. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. Indexes are unmanaged and one cannot directly invest in an index. They do not include fees, expenses or sales charges. There is no assurance that any estimate, forecast or projection will be realized. Past performance is not an indicator or a guarantee of future results. Important data provider notices and terms available at www.franklintempletondatasources.com.

8. Sources: FactSet, Russell Indices. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. Indexes are unmanaged and one cannot directly invest in an index. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results. Important data provider notices and terms available at www.franklintempletondatasources.com.

9. Sources: FactSet, Russell Investment Group. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group, S&P Dow Jones Indices. Indexes are unmanaged and one cannot invest in an index. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments