Our Fixed Income CIO Sonal Desai shares her investment views and strategies for the post-pandemic recovery. She explains why inflation looks likely to gain steam, and how the balance of fundamentals and valuations become especially crucial today when looking for attractive returns in fixed income. The Franklin Templeton-Gallup Economics of Recovery Study supports her bullish view for the global economy, and highlights how policymakers need to intensify their efforts to boost vaccine acceptance.

Investment strategies have dominated media headlines in recent days, with a twist: it’s all been about social media-driven individual investments in stocks unloved—and shorted—by some major hedge funds. The story has raised strong passions on different sides of the debate: some have seen it as a poetic revenge of “the little guy” against “Wall Street;” some as another dangerous example of mob behavior in the age of social media; and some as simply a manifestation of new dynamics in a financial market where direct individual investment has come to play a bigger role.

But whichever way you look at it, like every discussion on investment strategies, this one also boils down to weighing valuations and fundamentals. And whether you are looking at equities or fixed income assets, for me the starting point must always be an assessment of the overall macro fundamentals. As I have argued in the recent Barron’s 2021 Roundtable, I maintain a bullish view on this year’s economic outlook, especially for the United States. A view informed and supported by the insights we gleaned from our just completed, months-long Franklin Templeton–Gallup Economics of Recovery Study.

Vaccines’ Booster Shot to the Recovery

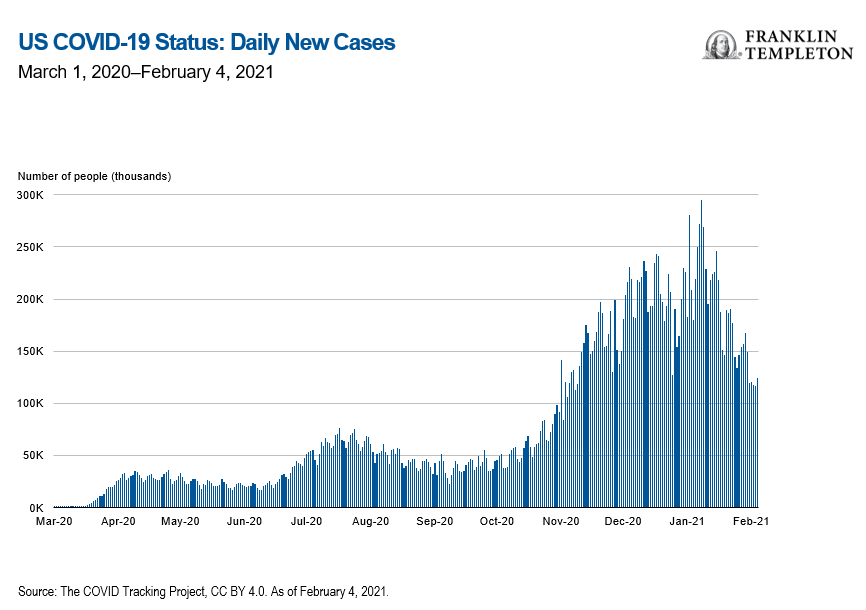

Our study showed that a COVID-19 vaccine would be the single most important factor in giving people confidence to resume normal spending habits.1 Now several vaccines have received emergency approval and their efficacy is higher than was hoped for. Supply chains and distribution are experiencing teething pains, but we’ll surmount them. The key thing is: we now have a vaccine. Moreover, the trend in new cases in the United States had already started to improve considerably at the turn of the year, providing an additional tailwind.

As vaccination programs build momentum, they will pave the way for a broader reopening of economic activity. And in 2020, we have seen that the economy is in strong enough health to bounce back quickly as restrictions on business activities are lifted.

Back to School

School reopenings should provide a further impulse to the recovery. Our Economics of Recovery Study highlighted that reopening schools can give a major boost to labor supply: we found that only 47% of people whose children are in remote learning work full time, compared to 71% of people whose children are in school; and nearly a quarter (24%) of parents with children in remote learning are out of the labor force altogether, vs. only 15% of parents whose children are in school. Compared to those whose children are in school, parents of children in remote learning are twice more likely to be unemployed (11% vs 5%).

Reopening schools will get people back into the labor force and into full-time careers. It will also remove an important cause of inequality: women are hit harder than men by school closures, and so are lower-income parents, who cannot afford to hire tutors or tap other external resources to help their children with remote learning. And since studies have already shown that remote schooling causes a greater setback in learning for children from disadvantaged households, school closures are also entrenching inequality into the future.

US President Joe Biden has targeted reopening schools as one of the goals for his first 100 days, and his Chief Medical Advisor Anthony Fauci also now supports getting children back to school—after cautioning against school reopenings for most of last year. Scientific evidence indicates that young children have an extremely low risk of contracting or transmitting the virus.

Ready, Set, Spend

Fiscal and monetary policy have already provided enormous stimulus, and more is on the way—to the point that even some prominent economists close to the current administration, like former Treasury Secretary Larry Summers and Harvard Professor/Economist Jason Furman, have openly wondered whether Biden’s proposed $1.9 trillion in additional stimulus might lead to overheating.

Household savings rates are extremely high, thanks to timely and generous government support, and so is pent up demand after consumers’ social and economic lives have been heavily constrained for months. The United States economy is primed for a strong rebound.

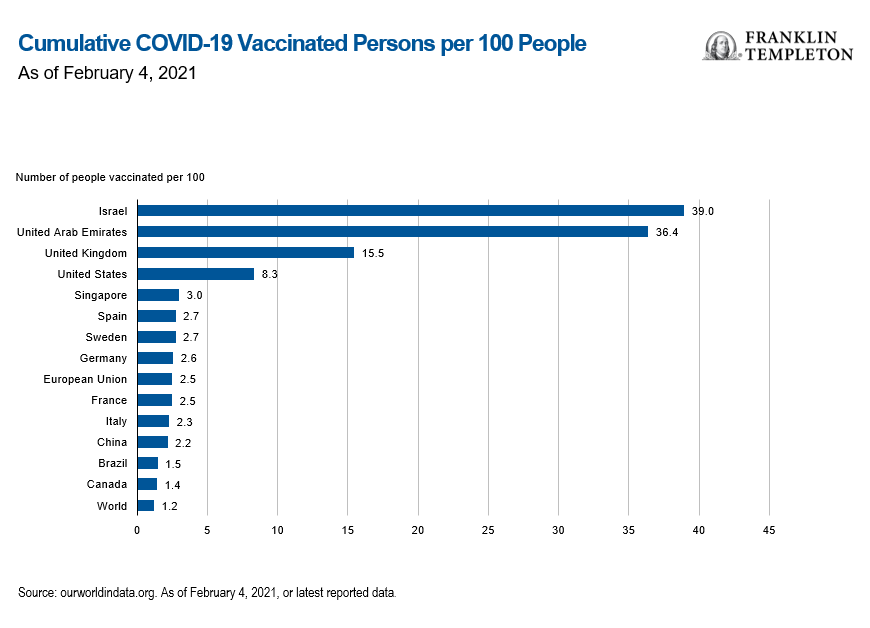

The rebound will be stronger in the United States than in Europe, in my view. When you look across the world, progress in national vaccination campaigns looks very uneven. Israel and a few other smaller nations stand out at the top of the rankings; the United States and United Kingdom are leading the pack of the major advanced economies, whereas the European Union lags behind. This will inevitably be reflected in different speeds of reopening and recovery; countries that move faster on vaccinations will bounce back faster.

Investment Strategy: Low Duration, Gold, Selected High Yield and Emerging Market Bonds

A strong economic rebound coupled with the Federal Reserve’s pledge to keep monetary policy extremely easy should provide a healthy reflationary shock—that’s why our investment strategies focus on limiting duration,2 especially in the United States. That’s also why gold looks attractive to us, and other commodities should also do well, in our view. The massive and sustained policy stimulus in the United States and other major economies implies that aggregate demand will likely recover faster than global supply. Moreover, the fact that some regions and countries lag behind in their vaccination efforts suggests that restrictions on global travel and trade will linger, a protracted headwind to the normalization of supply chains. All this suggests that price pressures will gain steam—and it will not take much for them to exceed the very sanguine market expectations.

The balance of fundamentals and valuations becomes crucial when looking for attractive returns in fixed income at a time when negative-yielding global debt has reached $17 trillion. Based on my positive view on the US recovery, I see US high-yield assets as still attractive, even though their valuations are not cheap. Higher yield comes with higher risk, but I think the recovery outlook makes the risk-reward attractive and allows investors to keep duration low.

Another source of yield is emerging markets debt, which should continue to attract interest and inflows this year, given also that most investors are structurally underweight the asset class. It pays to be selective here, and I would start with Asian markets, since Asia overall has had a more effective approach to the pandemic from the very beginning; and recently India has also shown a marked improvement in COVID-19 trends.

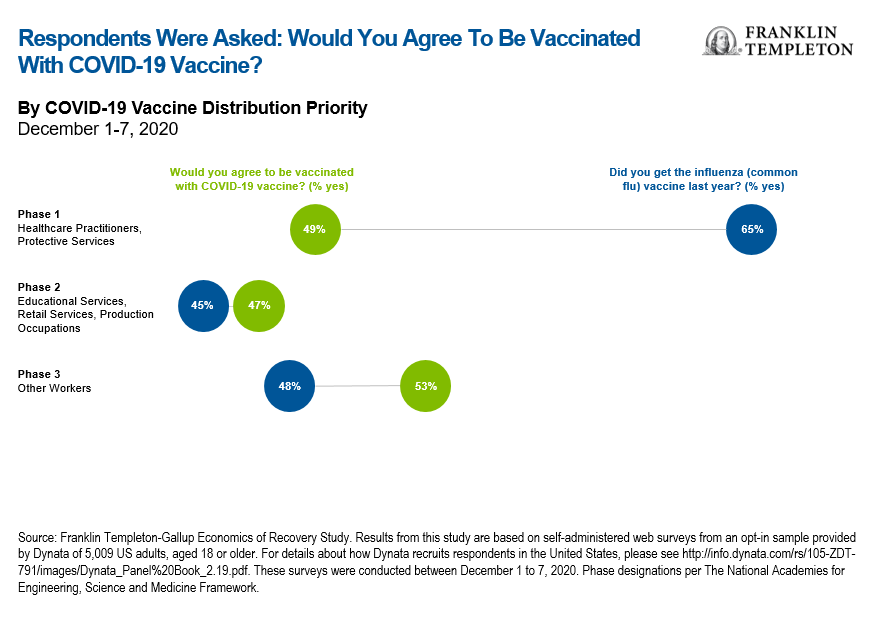

So overall I think 2021 is off to a good start. There’s no shortage of uncertainties and risks, but the improving macro outlook offers some very attractive investment opportunities—and more will arise as the year plays out, which is a good reason to keep some firepower in liquid assets. Among the risks to watch, a key one bubbles up again from our study with Gallup: our latest pulse showed that half of health care workers are reluctant to take the vaccine. A comparison with flu vaccine take-up makes this even more striking; among health care and preventive services workers, the share of those willing to take the COVID-19 vaccine is significantly lower than the share of those who took a flu shot last year. For other workers instead, acceptance of a COVID-19 vaccine is higher than flu vaccination rates.

Our study found that better information boosts the vaccine acceptance rate, so policymakers should intensify their efforts to provide better information on the vaccines’ efficacy and safety to boost the take-up rate among health care professionals and the public at large. Health care is not like finance. In financial markets, sometimes the credible promise of policy action can be enough to avert or solve a crisis—like former European Central Bank President Mario Draghi’s “whatever it takes” pledge to keep the eurozone whole. But to halt a pandemic, it’s not enough that a vaccine exists—we need something closer to an “everyone takes it” approach.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

1. Source: Franklin Templeton-Gallup Economics of Recovery Study. Results from this study are based on self-administered web surveys from an opt-in sample provided by Dynata of 25,033 US adults, aged 18 or older. For details about how Dynata recruits respondents in the United States, please see http://info.dynata.com/rs/105-ZDT-791/images/Dynata_Panel%20Book_2.19.pdf. These surveys were conducted between July and October, 2020.

2. Duration represents the sensitivity of the price of a bond or other debt instrument to a change in interest rates, and is expressed in years.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments