The COVID-19 crisis opened up cracks in the muni market, but we don’t expect those cracks to alter the reality that municipal bonds can be a relatively conservative investment option. Many municipalities are under stress, but that’s not a reason to avoid munis, in our view.

COVID-19 has affected states to different degrees

States that are particularly dependent on the travel and leisure, energy, or service sectors have been “disproportionately affected by the pandemic” and “are generally seeing larger impacts on their economies and tax revenues” according to the National Association of State Budget Officers.1

A good illustration of the uneven impact that COVID-19 is having on states can be seen in their unemployment rates. State unemployment rates range from as low as 3.0% in Nebraska and South Dakota to as high as 9.3% in Hawaii which is closely followed by Nevada at 9.2%.

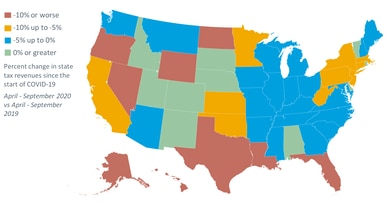

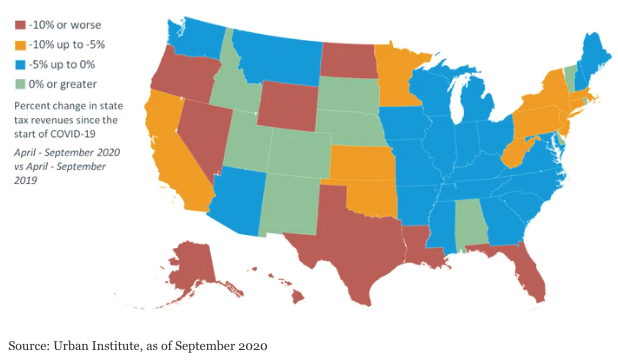

Moreover, some states are bringing in more tax revenues since the pandemic began relative to the same time last year as illustrated in the map below. States that have a higher dependency on sales taxes, as compared to income taxes, are experiencing greater financial pressures.

The COVID-19 crisis has had an uneven impact on state finances

Bankruptcy and default are different

When discussing municipal credit quality, we often hear the concern that municipalities will file for bankruptcy or may default on their bonds. Although often intertwined, a default and a bankruptcy are not the same.

A default is defined by Moody’s Investors Service as a missed interest or principal payment, an exchange where the bondholder received less than was originally promised, or a change in the payment terms. There are also “technical defaults,” where the issuer breaches a covenant, such as minimum debt service coverage, but the bondholder continues to be paid as usual.

A bankruptcy, on the other hand, is a legal process that provides a financially distressed municipality legal protections from creditors while it develops and negotiates a plan for adjusting its debts.

The distinction is important to bondholders because a municipality may default without filing for bankruptcy protection, or it may file for bankruptcy protection but continue to pay some bondholders.

Further complicating matters is that states can’t file for bankruptcy protection, and local governments in 23 states can’t either. The other 27 states that allow local governments to file for bankruptcy protection require the governments to overcome a series of legal hurdles first.

Bankruptcy does not necessarily mean all is lost

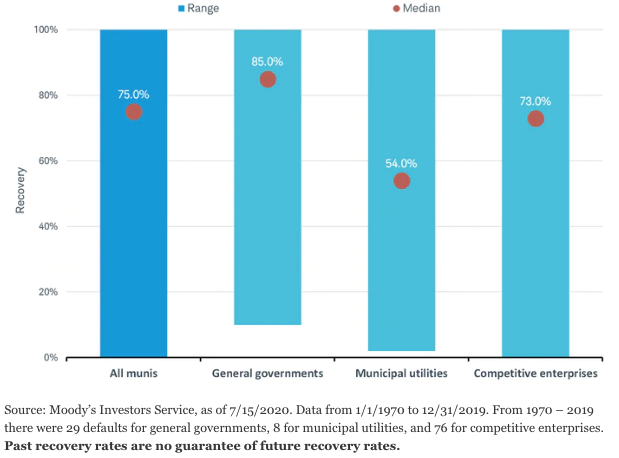

When an issuer defaults, it is essentially declaring that it does not have the financial resources to meets all of its obligations in a timely fashion. However, it may still have some resources to pay back bondholders. On average, bondholders have received about 75% of the amount that was originally owed to them, based on a study of Moody’s-rated bonds going back to 1970.2 Recovery rates, or the amount bondholders receive relative to what they were promised, are usually higher for general governments, which include general obligation bonds of issuers such as cities, states, and local governments, as illustrated in the chart below.

Recovery rates for munis have usually been high, but vary by the issuer type

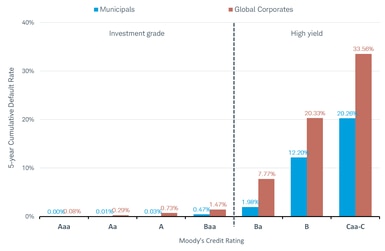

Defaults are relatively infrequent

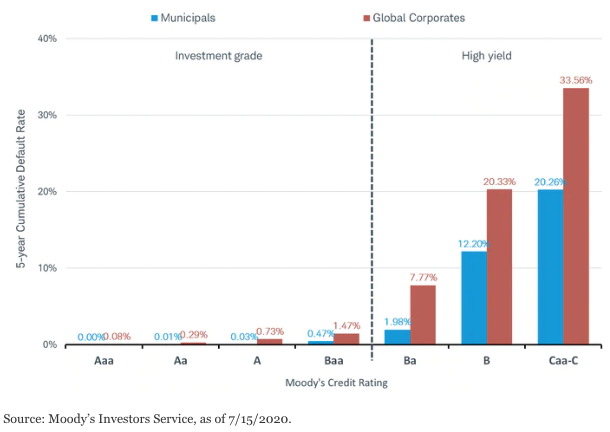

In spite of the recent attention to municipal credit problems, investment-grade municipal bonds historically have defaulted at far lower rates than similarly rated corporate debt, as shown in the chart below. Of those bonds that have defaulted, the vast majority had sub-investment-grade credit ratings or were not rated at all.

Munis historically have defaulted less than corporate bonds of similar maturity

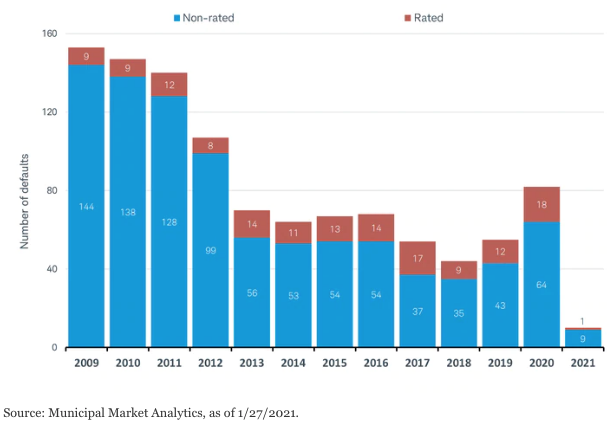

Defaults are most likely among risky issuers

Although defaults are rare in the muni market, they do occur. As illustrated in the chart below, defaults picked up in 2020, but are still well below the levels seen following the 2007-2008 credit crisis. In fact, 82 issuers totaling $5.8 billion of principal defaulted for the first time in 2020, which was the highest since 2012. While this may seem like a large number, it represents less than 0.2% of the $3.7 trillion muni market.

Most defaults are by issuers that were originally unrated, or that operate in an already risky sector. For example, of the 82 issuers that defaulted for the first time in 2020, more than a third were by issuers in the retirement sector, which includes issuers like nursing homes. This was one of the hardest-hit parts of the economy in 2020, due to the pandemic.

Most muni defaults have occurred with unrated issuers

We don’t expect broad muni bond defaults

You may be asking, “but given the declines in revenues that many issuers are experiencing, coupled with a slew of other issues like large unfunded pension plans, won’t that lead to more defaults in the future?” While this is an understandable concern, we don’t think so. One reason is the relatively strong starting point for most issuers prior to the crisis. For example, heading into the crisis, state rainy-day funds were at an average all-time high of 7.6% of general fund expenditures, according to the National Association of State Budget Officers. This provided a cushion to soften the blow of the large decline in revenues.

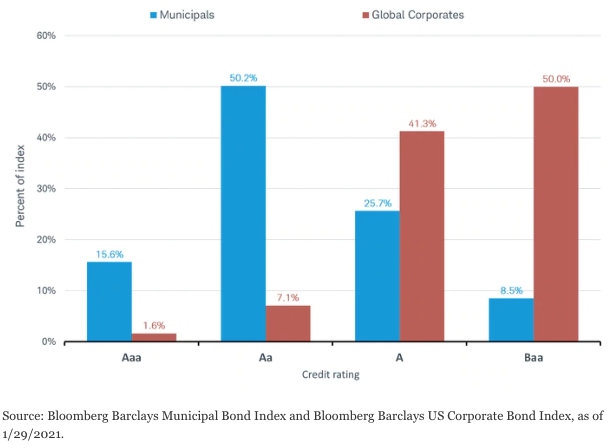

In addition to their relatively strong financial starting point, most municipal issuers operate in a monopolistic structure – meaning they don’t have to compete for “customers” to the same degree that corporate issuers do. For example, most water and sewer issuers deliver an essential service with few or no other alternatives.

Also, many issuers benefit from broad rate-raising ability and expense management. Almost all state and local governments operate on a balanced-budget requirement, meaning revenues must match expenses. They have options to both raise revenues and cut expenses, which is supportive of their strong and stable credit characteristics. The inherent structure of most municipal issuers is a reason why a large portion of the municipal bond market is very highly rated relative to the corporate market, as illustrated in the chart below.

Roughly two-thirds of the muni market is AAA or AA-rated

Fiscal and monetary stimulus have supported the muni market

When the COVID-19 crisis began, Congress swiftly passed the $2.2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) Act, which provided direct aid to states and some transportation issuers, authorized the Federal Reserve to create new facilities to help stabilize the market, and provided a number of other measures to financially support the economy.

The more recent COVID-19 relief package, passed in December 2020, also should provide support for many state and local government issuers. Notably, the recent package didn’t include direct aid to state and local governments, but it did include other measures that should be supportive of economic activity, like enhanced unemployment benefits, direct payments to individuals, the extension of Paycheck Protection Program, and direct aid to airports and transportation providers. Indirectly, this will help the finances of many muni issuers via sales and income tax revenues. The recent package also extended the deadline for states to use the money that was allocated to them under the CARES Act.

We’re cautiously optimistic on the muni market in 2021

We expect issuers to face headwinds in 2021, but they should be manageable. Issuers with greater financial flexibility and revenue sources that are less tied to economic activity should fare better, in our view. We don’t believe investors should avoid munis, which should continue to provide relatively attractive after-tax income and maintain their stable credit characteristics.

1 National Association of State Budget Officers, Summary Fall 2020 Fiscal Survey of States, as of December 23, 2020.

2 Moody’s Investors Service, “U.S. municipal bond defaults and recoveries, 1970–2019, as of 7/15/2020.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.