Will Brexit Lead to Bruin? - The Cost of Absurdity

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe got our fish back. They are now British fish and they are better and happier fish for it.

If you are not British, or you don’t happen to live on these isles, you may not know who Jacob Rees-Mogg is, so let me introduce you. Rees-Mogg is a senior, and a rather controversial, MP for the Conservative Party in Westminster. At one point, he was even mentioned as a possible successor to Theresa May as Prime Minister of the UK – the job that Boris Johnson eventually landed.

The reason I bring him up in the context of this month’s Absolute Return Letter is that he was (and still is) a leading light for the Brexit movement. He was elected chairman of the influential European Research Group – a group of EU-sceptic Conservative MPs – that put immense pressure on Theresa May to pursue a hard Brexit.

In the following, I will look at the pros and cons of life outside the EU, and I will assess whether Britain could end up in ruins as a result, which the little devil in the back of my head keeps telling me. It is admittedly a very emotional topic. I know of entire families here in the UK who have fallen out over Brexit, so I shall do my very, very best to be as clinical as possible in my assessment. That said, I am a European after all, and that fact can only colour my views.

Over dinner the other night, I said to my wife: “Are you aware that there is a link between Brexit and the uncomfortably high UK death toll from COVID-19?” (now in excess of 100,000). “Of course”, she said. “About the worst you can do to the average Brit is to take away his sense of being in control of things. The government did that when they signed up for the EU, and they did it again when putting various lockdown restrictions in place last year. The longer those restrictions lasted, the fewer followed them and, consequently, the more died”. Sad but true.

Now, this month’s Absolute Return Letter is not about COVID-19 but about the (likely) implications of the trade agreement that was entered into five minutes before midnight late last year, so let’s drop the COVID topic for now. It is just very sad to see that the British desire to remain independent has led to a world record in mortalities.

The naked facts

The trade agreement is far too complex to go through in detail (it would probably turn the February Absolute Return Letter into a 1,200 page monster), but let me briefly go through some of the key elements in the agreement (with Politico being my primary source) so that you have a sense what the fuss was all about.

State Aid

State aid proved a sore point during the negotiations. The EU was keen to avoid the UK from gaining an unfair advantage by subsidising British businesses, thus allowing them to undercut EU businesses. This concern was undoubtedly the result of all the talk in Britain about turning it into the Singapore of Europe.

Both sides agree that the resulting compromise is far from the end of the saga. Much work now needs to be undertaken to ensure that what has gone into the agreement is actually workable. Specifically, the UK must now create a body to oversee its own subsidy control regime.

Friction for Flexibility

Throughout January, British newspapers bombarded its readers with horror stories about all the new taxes and paperwork that, at least in some industries, have slowed trading down to a trickle in recent weeks. As a consequence of all the red tape, various shipping companies have announced that they will no longer ship from the EU to the UK and vice versa – at least until some of that red tape has been removed again.

The problem in a nutshell is that Britain demanded the flexibility to strike trade agreements elsewhere (which is understandable). In return, the EU demanded for certain rules to be implemented (which is also understandable).

The other issue which has caused more friction is the fact that the UK declined to follow the EU’s rule set on human rights, animal welfare and disease control. One implication of that is that British farmers now need a vet certificate before they can export their meat to the EU.

Goods vs. Services

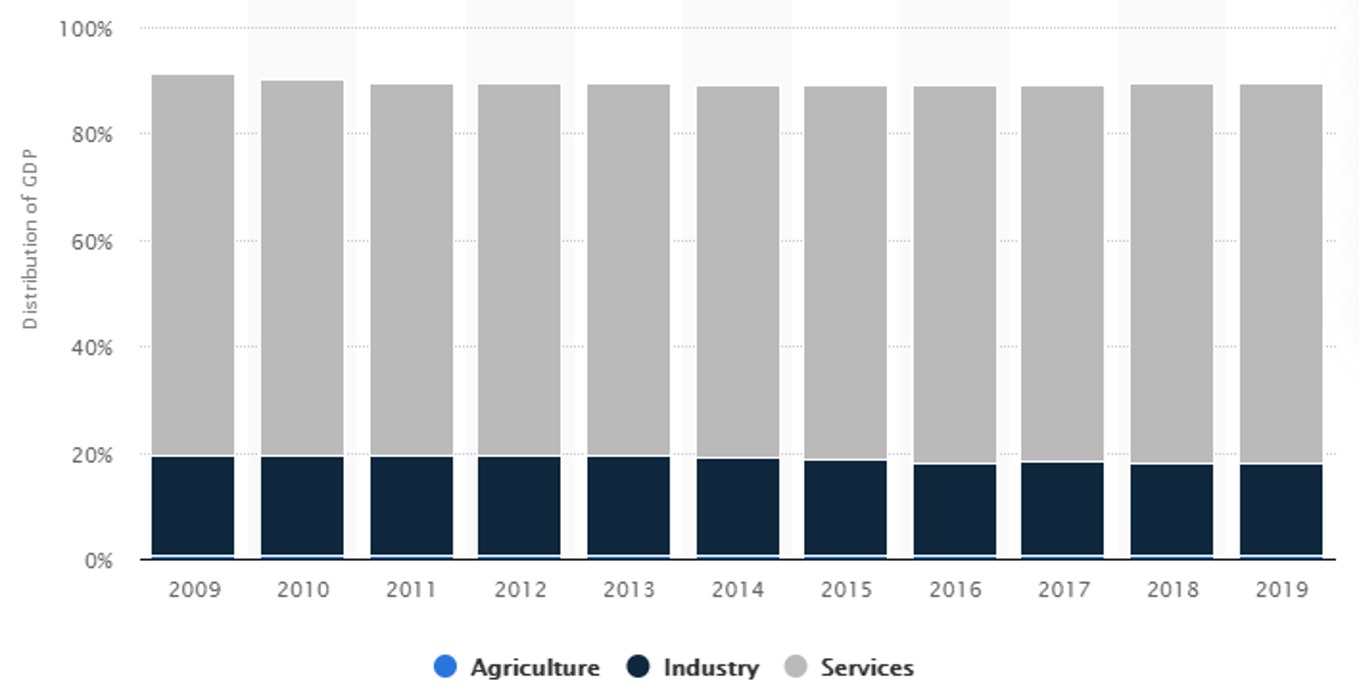

Services, broadly defined, accounted for 71.3% of UK GDP in 2019, whereas manufacturing made up only 17.4% (Exhibit 1). Much of the rest was (and still is) public spending. In the private sector, two industries – farming and fishing – get a disproportional amount of media attention, although they are both largely irrelevant to the overall picture, economically speaking.

Source: Statista

The agricultural industry accounted for 0.6% of GDP in 2019 and the fishing industry for approx. 0.2%. The fishing industry is so insignificant that I have struggled to establish exactly how much it accounts for. In most reports, fishing shows up under “other” but, according to a back-of-the envelope calculation I did, I arrived at approx. 0.2%.

Although services account for nearly three-quarters of UK GDP, the trade agreement is ominously vague on services. Take for example MRPQs (Mutual Recognition of Professional Qualifications), which are critical for doctors, engineers, architect, lawyers and other professionals. The deal now in place offers no more than the EU-Canada trade agreement from 2017. In that context, I note that the EU-Canada trade agreement has not yet led to a single MRPQ. Not one!

As far as financial services are concerned, neither party seemed very eager to enter into an agreement at all. The EU appeared keen for Frankfurt, Paris and Amsterdam to snap up market share from London, and the British government was very much aware that looking after the City boys and girls wouldn’t win them many votes, as large parts of the country think they are a bunch of spoiled brats.

As a consequence, financial services – which is a very important industry to the UK economy – was largely ignored in the final agreement, while an industry that hardly matters (fishing) took centre stage. Having said that, the agreement does contain a clause that states that, by March 2021, the two sides will try and reach an MoU on financial services based on mutual recognition, allowing the financial industry to trade ‘across the border’.

Phasing-In Rules

Japanese car manufacturers are well represented in the UK, and they have been adamant that, without adequate protection, they could be forced to move their production elsewhere – supposedly to an EU country. The good news is that the trade agreement now in place offers at least temporary protection with a six-year phase-in period for the rules governing origin requirements. What will happen at the end of that six-year period, only time can tell.

Labour Mobility

I could go on forever but will mention only one more, as I think the most important parts have now been covered. The last area that deserves a special mention is the new rule set governing the mobility of labour. The UK were keen only to restrain the mobility of labour but not that of goods and services. This was always a non-starter, as it goes straight against the EU’s constitution, the so-called freedom of movement clause. The British government, on the other hand, had little choice but to restrain the mobility of labour, as they would otherwise have lost the support of the European Research Group and thus the majority in Parliament.

The new rule set requires for most to obtain a visa, should they need to work across the border. Admittedly, an exemption for certain professions has been made. Those exempt can work visa-free for up to 90 days but, interestingly, some professions that probably should have been included are not. Take for example musicians. If a British rock band is performing in Berlin for a night or two, a visa is now required. Imagine all the problems that is going to cause.

Source: House of Commons, Briefing Paper 7851

Financial implications

Throughout the rather lengthy negotiations, Brexit supporters maintained – and large parts of the British media bought the argument – that the EU would face a much bigger problem than the UK, in case no deal could be reached, given the considerable, and persistent, EU trade surplus vis-à-vis the UK (Exhibit 2), but that is quite frankly an absurd argument.

When it comes to the impact on the economy, whether there is a deficit or a surplus on the trade balance is irrelevant. What matters is how much is exported to the other side as a percentage of total exports, i.e. what percentage of export jobs are at risk. In 2019, about 43% of total UK exports ended up in one of the EU countries (Exhibit 3), whereas only 4-5% of EU exports of goods and services ended up in the UK.

Note: The EU percentage includes non-EU countries that are members of the single market.

Sources: World's Top Exports, Absolute Return Partners LLP

If trade is affected by all the red tape I mentioned earlier, there is no reason to believe one side will be impacted differently from the other side. The implication of this is that a much bigger percentage of exports, many more jobs (in % of the workforce) and a much bigger slice of the GDP pie will be negatively affected in the UK than in the EU.

Now, if you split the UK-EU trade balance into goods and services, it becomes obvious that, while the UK has a significant trade deficit overall, it actually has a trade surplus with the EU on services (Exhibit 4). This makes it even more puzzling that services were largely ignored in the agreement the two parties entered into just before Christmas. By setting up the agreement this way, not only is a significant number of jobs in UK export industries at risk, but over 70% of the UK economy (services) is left in limbo – not the smartest move by Boris Johnson who obviously cared more about the 0.2% of GDP accounted for by the country’s fishermen (whom he managed to upset anyway).

Source: House of Commons, Briefing Paper 7851

The British government has been adamant that one of the biggest advantages of Brexit is the ability to strike trade agreements with various countries independently of the EU, so let’s spend a couple of minutes on that. In terms of individual countries which form the EU block, the only country with a significant trade deficit vis-à-vis the UK is Ireland (Exhibit 5). In the context of trade agreements, this is relevant because of Joe Biden. He has a certain affinity for Ireland (he is of Irish origin) but, more importantly, he has repeatedly stated that a solid relationship with the EU must be prioritised over and above anything to do with the UK.

Biden is not anti-Britain but is overwhelmingly pro-Europe which makes it very unlikely that he will put a trade agreement with the UK near the top of his priority list. For Biden, it is very much about getting the relationship with all of Europe back on track after four years of Trumpism.

Source: House of Commons, Briefing Paper 7851

Another potentially big winner of Brexit is Canada which has been mentioned in the British media as one of the “obvious ones”, given the close ties between the two countries. In fact, as I write these lines, an agreement has already been signed, so why don’t I get more excited? Problem is that the new agreement is a copycat of the EU-Canada trade agreement from 2017. Thus, leaving the EU does not provide the UK with any advantages over and above those that EU member countries already have.

Having said that, there can be no doubt that, although the trade agreement now in place is far from perfect, it is still better than the alternative, which would have been no deal at all. All future trades between the two would then have had to take place on WTO terms and conditions. According to the UK’s Office for Budget Responsibility (a fiscal watchdog), the deal now in place will result in GDP being 4% lower over the next 15 years than it would have been, had the UK chosen to remain a member of the EU. For comparison, no deal would have translated into a 6% lower GDP over the same timeframe.

The other side of the coin

In all fairness, it is not all bad news. The UK’s strongest card in any upcoming talks is undoubtedly its military power. With Russia playing silly games all over Europe, the rest of Europe cannot afford to upset the British so much that they walk away. Continental Europe needs the UK to be firmly on its side, militarily speaking, and I have no doubts that Putin will test that alliance in the months and years to come.

As far as the new trade agreement is concerned, the deal the two parties have entered into is completely tariff-free. Outside the EEC, the EU has never entered into a trade agreement before where tariffs have been abolished. The price the British paid for that was that they had to drop all ideas about turning the UK into another Singapore. Only if the British agreed to uphold a “level playing field” will the EU continue to accept the terms in the deal according to the small print in the agreement. In practice, this means that the Singapore dream is all but dead, but that some (significant) level of stability has been secured. Therefore, Brexit will most likely not leave Britain in ruins, even if it is not the bed of roses Boris Johnson has portrayed it as.

I should also add that the new agreement has established that the UK is no longer required to follow EU rules and no longer subject to the European Court of Justice. To the British or rather, to the European Research Group and their supporters, this was, and still is, a very important part of the jigsaw.

In Britain, that was presented by Boris Johnson as a major victory (“I have a Christmas present for you”, as he said on national TV). What he failed to say in the same context was that, being outside the European single market means that UK businesses can no longer assume that products authorised by British watchdogs can be sold in the EU. All this red tape is what has caused a slowdown in cross-border trade in January.

The bottom line

Even my pro-Brexit British friends (of which there are a few) have struggled to deliver a positive spin on the new trade agreement. Whilst everybody agrees that it is much better than having no trade agreement at all, I have heard few comments oozing of optimism.

Boris Johnson and his cabinet tried their best to spin a good story, but events over the last few days before a deal was struck speaks a very different language. It was obvious that the British desperately needed a deal. With the UK economy already on its knees from the pandemic, they knew that no deal was the last thing the British economy could afford.

How desperate the UK government was for a deal is best illustrated by the fishing deal they landed. Less than 24 hours before a final agreement was reached, government ministers let it be known that there was no deal to be done unless the EU agreed to a reduction of European fishing rights in British waters of at least 70%. Hours later, a deal was agreed at -25%.

Source: Financial Times

The problem the UK government is up against is the rapid rise in government debt, caused by COVID-19 (Exhibit 6). Running up over £400Bn of new debt in 2020-21 is akin to increasing public debt-to-GDP by approx. 20%. Although it is very cheap to service debt at present, one cannot assume that interest rates will always stay this low. Robust GDP growth is the best medicine against rampant debt accumulation, as that will generate more tax revenue to service the debt with. With the UK now at risk of drowning in debt, Boris Johnson simply cannot afford for the British economy to underperform.

One last point: Given all those negatives, will the UK economy ever perform better than the EU? Yes, and there are two reasons for that. Firstly, the UK economy has already, for many years, performed better than most other EU economies – higher GDP growth, lower unemployment, etc. – and an important reason for that is fewer regulations when compared to most other European nations. Unlike what Brexiteers like to tell the nation, EU membership has never prevented a member state from being less regulated in many areas, as long as certain minimum standards are met, and the British have always taken advantage of that.

The second reason the UK is almost certain to outperform most of Europe for many years to come is much more favourable demographics. Whereas many other European economies will suffer the consequences of very poor demographics, the UK outlook is relatively benign. So, when a future UK government tells you how proud we should all be that we were prepared to leave the sinking ship, they will almost certainly neglect to tell you the true reason why the ship is sinking. That reason is poor demographics – not anything trade agreements can do anything to rectify.

Niels C. Jensen

1 February 2021

Niels Clemen Jensen founded Absolute Return Partners in 2002 and is Chief Investment Officer. He has over 30 years of investment banking and investment management experience and is author of The Absolute Return Letter.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All