Technology’s Rising Importance in Emerging Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhereas commodity production had been a major economic driver in emerging markets, we think technology is now the leading force.

When it comes to technological innovation around the world, semiconductor production is one of the best examples. Among the semiconductors produced in the U.S., many are analog chips—which are often used for power supplies, sensors and wideband signals (e.g., speech, music and video). Applications for digital chips, on the other hand, include computer processing, data storage, logic functions and information management.

Compared to analog chips, digital chips are generally considered much more technologically advanced—and are largely produced in emerging markets, with the leader being Taiwan. Digital chips are necessary to enable e–commerce, mobile payments, fintech, 5G telecom, health–care advances (e.g., telemedicine and drug discovery), remote learning, online entertainment, artificial intelligence, autonomous machines, self–driving cars, supply–chain management, cloud computing and software–as–a–service (SaaS) applications.

SEMICONDUCTOR ADVANCEMENT IS THE “NEW OIL”

Semiconductors have been around for decades. But many of today’s electronic devices depend on the most technologically sophisticated chips, which are extremely difficult to fabricate. So while oil and other commodities were the key economic “lubricants” for emerging markets in the past, we think advanced semiconductors and other cutting–edge technologies will dominate the landscape going forward.

Some observers of emerging markets may take issue with our comparison of oil to semiconductors. After all, oil has a finite supply while semiconductors theoretically can be improved ad infinitum. But we think the reality is that some semiconductor companies are so far ahead of their competitors that supply is in fact a constraint—and therefore a major investment consideration.

EMERGING MARKETS ARE CHANGING

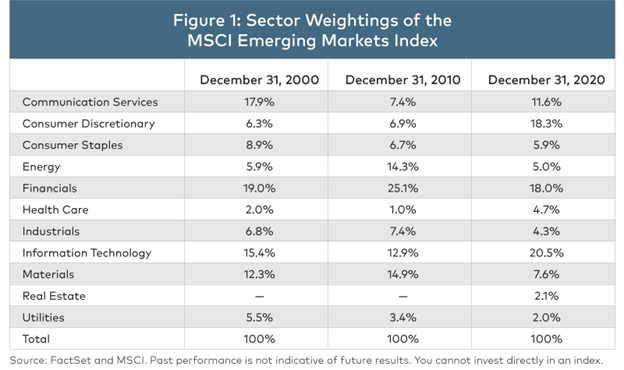

For a better understanding of how emerging markets have been changing over time, refer to Figure 1—which shows the sector weightings of the MSCI Emerging Markets Index in 2000, 2010 and 2020. As you can see, energy and materials rose in importance during the decade ended December 31, 2010 but fell in importance during the most recent decade. Conversely, information technology (IT), communication services and consumer discretionary have seen their roles in emerging markets expand dramatically during the most recent decade. These are the sectors that include, for example, semiconductors, e–commerce and SaaS.

One sector that hasn’t shown as much significance in the Index is health care. But we think this will change dramatically during the coming decade due to the growing utilization of health–care services by people in developing nations and the use of technology to make health care more accessible to these people. For example, China’s Ping An Healthcare & Technology is an online and mobile provider of medical services through the internet–based platform “Ping An Good Doctor.” The platform is used for remote consultations, hospital appointments, health management, wellness services and health–care resource referrals. Ping An’s goal is to improve efficiencies in the allocation of primary–care and hospital resources through the use of innovative technologies including artificial intelligence.

Another example is Wuxi Biologics, which is headquartered in China but operates globally. The company develops antibody drugs and biological medicines and provides value–added services to other pharmaceutical firms. Wuxi has an expanding pipeline of business including involvement in vaccine production for Covid–19.

PERFORMANCE OVER THE DECADES

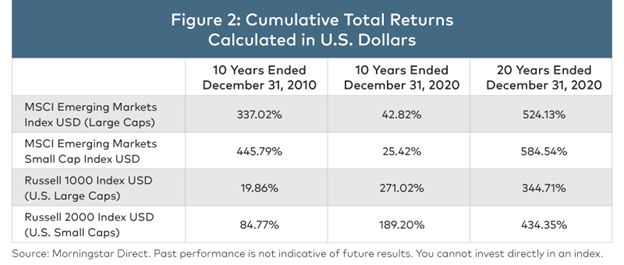

Now that we’ve discussed the sector drivers of emerging markets over the past two decades, let’s look at emerging–market stock performance versus U.S. stock performance broken down by market capitalization. Figure 2 includes the MSCI Emerging Markets Index of large caps, the MSCI Emerging Markets Small Cap Index, the Russell 1000® Index of U.S. large caps and the Russell 2000® Index of U.S. small caps. All of the numbers presented are cumulative (not annualized) total returns calculated in U.S. dollars.

What we see is that over a longer period of time, the 20 years ended December 31, 2020, emerging–market stocks outperformed U.S. stocks. What we also see is that over 20 years—both in emerging markets and in the United States—small caps outperformed large caps. This makes sense to us because emerging–market companies and small–cap companies generally have more headroom for growth, despite their generally higher risk profiles.

Now let’s look at a shorter time period, the 10 years ended December 31, 2020. This period tells a very different story. Emerging–market stocks dramatically underperformed U.S. stocks, and small caps underperformed large caps. However, if we go back further, to the decade ended December 31, 2010, we see outperformance by emerging–market stocks and small caps. What’s more, we believe these areas may be favored by investors once again—as explained below.

LONG-TERM EXPECTATIONS AND CYCLICAL IMPROVEMENTS

Having described the growing importance of technology and the broad performance of stocks over the past two decades, we have some thoughts about what may lie ahead.

Over very long periods of time, we believe there’ll be better opportunities to generate attractive returns in emerging–market stocks and in small caps. The main reason is that greater headroom for growth in these areas generally means that a seemingly higher valuation may be less of an impediment to long–term investment success.

Particularly among emerging–market companies and small–cap companies, we believe investment success comes more from properly assessing business models, management teams and competitive landscapes than from assessing valuations. For our part, business models, management teams and competitive landscapes—among other fundamental factors—are where we concentrate the bulk of our research efforts.

As an example, consider MercadoLibre—a Latin American e–commerce and fintech pioneer. Back in 2010, the company had a market capitalization of about US$2 billion. Since then, the market cap of MercadoLibre has skyrocketed to approximately US$78 billion. Another example is India’s HDFC Bank, which grew from about US$15 billion in 2010 to approximately US$106 billion today.

Still, we understand that cyclical factors also impact market prices. For instance, the most recent decade has been out of sync with what we’d expect over the longer term. In other words, we believe emerging–market stocks and small caps will see cyclical improvements in performance relative to U.S. stocks and large caps. The reasons for such improvements include comparatively attractive prices and the aforementioned headroom for growth and technological advancements—which may create a revolution that would be particularly beneficial for emerging–market and small–cap companies.

Another cyclical factor is the value of the U.S. dollar compared to other currencies. Broadly speaking, during the decade ended December 31, 2020, emerging–market currencies fell relative to the dollar—which created headwinds for emerging–market governments, companies and their stocks. If currency exchange rates generally move the other way in the decade ahead, these headwinds could reverse and spark greater investor interest in emerging markets. As an aside, we believe exchange rates aren’t as important when investing in China, Taiwan and Korea because these countries generally have been able to keep their currencies within reasonable ranges relative to the dollar.

A NEW ECONOMIC PARADIGM

As world–wide economies begin to get back on track in 2021, we think it’s important to keep in mind that “getting back on track” may not be the same as “getting back to normal” because “normal” may have changed. In other words, there may be a new economic paradigm precipitated by the coronavirus pandemic and enabled by technology that has permanently altered the way people live and work—so a seemingly well–positioned company a year ago may now be obsolete.

Based on the recent performance of the Wasatch strategies and funds, which you can access at wasatchglobal.com, we think our bottom–up research process meant we were nicely prepared for this unexpected new paradigm that has favored IT and health–care companies. The continuation of this paradigm will also influence our investment decisions going forward because it may create unforeseen opportunities, as well as accelerate other opportunities we had already expected.

INVESTMENT OPPORTUNITIES IN MAINLAND CHINA

The United States currently considers some mainland Chinese companies to be threats to American security. As a result, the U.S. has banned sales to China of certain critical technologies—including semiconductors. And China is vulnerable to this ban because the country is the world’s largest importer of semiconductors. As a result, we think China may start making major strides to decouple its semiconductor industry from that of the rest of the world.

To better understand this issue, we need to consider what’s going on in Taiwan. According to a recent report from Taiwan’s statistics bureau, the island’s economy expanded during the third quarter at the fastest pace in four years. Much of this growth was driven by exports—with a substantial share coming from Taiwan Semiconductor Manufacturing (TSMC), the country’s largest firm. TSMC’s revenues surged in 2020 as China’s Huawei Technologies stocked up on semiconductors ahead of the U.S.-imposed sales ban, which took effect in September.

Financial markets appear to reflect optimism that the current state of affairs marks a low point in U.S.-China relations. The thinking seems to be, even if relations don’t improve much under Joe Biden’s presidency, they’re unlikely to deteriorate much further. This thesis is reasonable in our view. At the very least, we think the new administration will take a more calibrated approach to China—and place greater emphasis on the interests of American allies such as Taiwan.

Partially due to Taiwan’s strong business ties in the U.S. and Europe, we believe China’s long–term strategy is to invest heavily in building a Chinese–centric infrastructure for semiconductor design and fabrication. However, start–to–finish semiconductor production is a complex process that requires considerable time and effort to develop the necessary expertise. Meanwhile, countries such as Taiwan may find themselves caught in the middle between China’s desire to expand its global economic influence and the U.S.’s desire to contain this influence.

Having said that, trade tensions and other forms of geopolitics have always been inherent risks in emerging markets. Despite these risks, we think there may be good investment opportunities related to the development of China’s semiconductor infrastructure to serve the country’s own needs. These opportunities could go beyond design and fabrication—as semiconductor production also requires many different types of machines, tools and other supplies.

Outside of semiconductor production, which is still in a nascent stage, China already has a large and deep range of investable companies across market capitalizations. Moreover, many of these companies cater to domestic Chinese demand—which is an economic segment we find particularly attractive. Please go to wasatchglobal.com for more information about the new Wasatch Greater China Strategy and Fund.

OPPORTUNITIES IN OTHER EMERGING MARKETS

When emerging markets first became recognized as comprising a separate asset class, investors valued them mainly for their energy reserves, mineral deposits and other natural resources. Extraction of these resources drove many emerging–market economies, which largely depended on exports of commodities to the developed world for growth and hard currency. This mutually beneficial relationship allowed emerging markets to mature well beyond their initial roles as commodity producers.

With technology now accounting for a larger share of emerging–market economies, comments like “tech is ‘eating’ the world” no longer apply just to developed nations. The MSCI Emerging Markets Index also reflects this shift, as indicated in Figure 1 above. For example, in the semiconductor industry, TSMC’s stock has benefited tremendously from the company’s technological superiority over Intel Corp. Having said that, TSMC along with Taiwan as a whole are vulnerable to Chinese interference—at least in the near term.

Outside of Taiwan, Korea may be the largest beneficiary of ramped–up semiconductor production to meet demand from around the world. While Korean companies—similar to Intel in the U.S.—have fallen behind TSMC, they may have some of the best prospects to catch up. Again, beyond design and fabrication, semiconductor production requires many other types of regional companies to be involved in the supply chain. Therefore, semiconductors may contribute to the rise of a new group of “Asian Tigers.”

Elsewhere, although India isn’t yet a powerhouse in semiconductors, technological innovation is nevertheless on full display. For example, India’s human capital is an abundant resource that can be leveraged through technology. A recent article in Bloomberg Businessweek featured nine–year–old fifth grader Shivank Patel, who has been learning to write software code for a year and has already created several apps. Patel’s latest endeavor, which he hopes to publish in the Google Play Store, is designed to help parents and doctors monitor babies born prematurely. Online coding classes for elementary–school children have become popular in India, as concerned parents seek to provide their kids with the tools necessary to land a well–paying job.

For an extensive discussion of India, please visit wasatchglobal.com to find our white paper entitled India’s Virtuous Circle of Amazing Progress. The paper covers what we believe are three megatrends in India: digitalization, financialization and formalization—all of which are enabled by technology.

THE WASATCH OUTLOOK

Clearly, the tensions between the U.S. and mainland China won’t be resolved anytime soon. But while these tensions may be unnerving, we believe they may actually accelerate the development of technologically advanced supply chains—some serving the domestic needs of China and others serving different channels.

The coronavirus pandemic, which caused dramatic shortages of protective gear and pharmaceutical ingredients, also highlighted that countries and companies need to diversify their supply chains and exert more control over production. Low cost can no longer be the primary consideration. For example, Apple is planning to expand iPhone production in India. In addition, Samsung already has its largest smartphone manufacturing facility located in India and will start making TVs there too.

We think new and enhanced supply chains will provide attractive investment opportunities. If you still doubt that companies and their stocks can perform well amid the U.S.-China geopolitical tensions, consider the headline from the cover of the December 14 issue of TIME Magazine, “2020: The Worst Year Ever.” Next consider that most of the Wasatch strategies and funds, which focus on high–quality companies with strong cash flows, were up double–digit percentages in 2020. (See wasatchglobal.com.) Moreover, many of the broad stock indexes around the world did well too.

Over the coming years, we believe thousands of companies will enter—or increase their involvement in—the technologically advanced supply chains running through emerging markets. And with so many companies, especially in China, some will succeed spectacularly while many others will struggle. Therefore, we think active stock picking will be particularly important.

In this regard, we continually add resources to our emerging markets research team. Our latest addition is Neal Dihora, CFA, who comes to Wasatch as a Portfolio Manager from the highly regarded Nicholas Company. Neal was born in Bhavnagar, India and speaks Gujarati.

Wasatch’s experience analyzing innovative, technology–driven companies should be well–suited to navigating the rapidly shifting terrain of emerging markets. Moreover, while some of our strategies and funds focus on small caps, our “select” strategies and funds allow us to invest in mid– and large–cap companies that we believe can continue to grow substantially.

To summarize, within emerging markets, we want to own many of the types of tech–related companies that have brought enormous efficiencies and modern conveniences to developed countries for many years—including during the coronavirus pandemic. Additionally, if we’re correct that the investment cycle and the currency cycle have shifted in favor of many emerging markets, we may have an even stronger wind at our backs.

We think it’s impossible to predict exactly how the dynamics we’ve outlined here will unfold. But by being ready through our continuous due diligence into the prospects of individual companies and by keeping our finger on the pulse of emerging markets, we believe we’ll have an advantage in quickly seizing opportunities as they arise. This is very important because relatively few individual stocks tend to outperform a corresponding benchmark index. And we’re particularly excited that technology, an area in which we consider ourselves to have particular expertise, may have replaced commodity production as the leading force in emerging markets.

With sincere thanks for your continuing investment and for your trust,

Ajay Krishnan, CFA

Head of Emerging Markets Investing

RISKS AND DISCLOSURES

Mutual-fund investing involves risks, and the loss of principal is possible. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets and political and social instability, which are described in more detail in the prospectus.

The Wasatch Greater China Fund is subject to risks associated with investments in China and countries in the greater China region that could affect the value of your investment in the Fund, including government control over currencies, economic conditions, industries and specific issuers, as well as continued strained international relations, uncertainty regarding taxes, and limits on credible corporate governance and accounting standards. Because of its exposure to greater China, including mainland China and China’s special administrative regions, such as Hong Kong, the Fund is subject to greater risk of loss as a result of volatile securities markets, adverse exchange rates and social, political, military, regulatory, economic or environmental developments, or natural disasters that may occur in the China region. The imposition of tariffs or other trade barriers by the U.S. or foreign governments on exports from China may also have an adverse impact on Chinese issuers. The Fund may invest in the securities of Chinese issuers through the China Stock Connect program. Trading through the Stock Connect Programs is currently subject to a daily quota, which limits the maximum net purchases by all purchasers using the Stock Connect Programs each day. While the daily quotas are relatively large, there is the possibility that the quotas could be reduced or exceeded, meaning buy orders for China A-shares would be rejected, affecting the Fund’s ability to efficiently execute on its investment strategy.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit wasatchglobal.com or call 800.551.1700. Please read the prospectus carefully before investing.

Being non-diversified, the Wasatch Greater China Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

The Wasatch Greater China Fund’s investment objective is long-term growth of capital.

Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk.

References to individual companies should not be construed as recommendations to buy or sell shares in those companies.

As of December 31, 2020, the Wasatch Emerging India Fund had 7.6% of its net assets invested in HDFC Bank Ltd.

As of December 31, 2020, the Wasatch Emerging Markets Select Fund had 0.7% of its net assets invested in Ping An Healthcare & Technology Co. Ltd., 5.0% of its net assets invested in HDFC Bank Ltd., 5.6% of its net assets invested in MercadoLibre, Inc. and 3.6% of its net assets invested in Wuxi Biologics Cayman, Inc.

As of December 31, 2020, the Wasatch Frontier Emerging Small Countries Fund had 7.3% of its net assets invested in MercadoLibre, Inc.

As of December 31, 2020, the Wasatch Global Opportunities Fund had 3.5% of its net assets invested in MercadoLibre, Inc.

As of December 31, 2020, the Wasatch Global Value Fund had 3.2% of its net assets invested in Samsung Electronics Co. Ltd.

As of December 31, 2020, the Wasatch Greater China Fund had 1.7% of its net assets invested in Ping An Healthcare & Technology Co. Ltd. and 4.6% of its net assets invested in Wuxi Biologics Cayman, Inc.

As of December 31, 2020, none of the Wasatch strategies or funds held Taiwan Semiconductor Manufacturing Co. Ltd., Intel Corp. or Apple, Inc. Huawei Technologies Co. Ltd. is a privately held company.

Wasatch Advisors, Inc., doing business as Wasatch Global Investors, is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Global Investors.

CFA® is a trademark owned by the CFA Institute.

DEFINITIONS

The “cloud” is the internet. Cloud–computing is a model for delivering information–technology services in which resources are retrieved from the internet through web–based tools and applications, rather than from a direct connection to a server.

Valuation is the process of determining the current worth of an asset or company.

The MSCI Emerging Markets Index is a free float–adjusted market capitalization index designed to measure the equity market performance of emerging markets. You cannot invest directly in this or any index.

The MSCI Emerging Markets Small Cap Index is a free float–adjusted market capitalization index designed to measure the equity market performance of small capitalization securities in emerging markets. You cannot invest directly in this or any index.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non–infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

The Russell 1000 Index is an unmanaged total return index of the largest 1,000 companies in the Russell 3000 Index. The Russell 1000 typically comprises about 92% of the total market capitalization of all listed stocks in the U.S. equity market. It is considered a bellwether index for the performance of large company stocks. You cannot invest directly in this or any index.

The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index, as ranked by total market capitalization. The Russell 2000 is widely used in the industry to measure the performance of small company stocks. You cannot invest directly in this or any index.

The Wasatch strategies and funds have been developed solely by Wasatch Global Investors. The Wasatch strategies and funds are not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the Russell 1000 and Russell 2000 indexes vest in the relevant LSE Group company, which owns these indexes. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license.

These indexes are calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in these indexes or (b) investment in or operation of the Wasatch strategies or funds or the suitability of these indexes for the purpose to which they are being put by Wasatch Global Investors.

©2020 Wasatch Global Investors

Wasatch Funds are distributed by ALPS Distributors, Inc. Separately managed accounts and related investment advisory services are provided by Wasatch Global Investors, a federally registered investment advisor. ALPS Distributors, Inc., is not affiliated with Wasatch Global Investors.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits