From time to time, readers of the Absolute Return Letter ask for my opinion on this or that and, every now and then, I decide to turn my response into a letter. The last few weeks have been no exception. In early December, the extraordinary rise in the price of Bitcoin drove one of our readers to ask what I think of that investment opportunity, and the trade agreement between the UK and the EU, which was entered into just before Christmas, inspired another reader to ask me if I could provide some more colour on that deal.

Whilst I love those sorts of challenges, in this particular case, I am facing a timing problem. As you may or may not be aware, the January Absolute Return Letter is always about the issues that I worry most about, as we enter the New Year. In other words, the earliest I can cover anything else is in the February letter, and we’ll be into March before both of those issues have been covered.

As you can see in Exhibit 1 below, I am not sure my thoughts on Bitcoin should be mothballed that long, and neither should the paper on the Brexit trade agreement, considering how important it is to all of Europe. Therefore, I have made the executive decision to prepare a research paper on Bitcoin, which will be published on ARP+ later this month. You can subscribe to ARP+ here. My thoughts on the trade agreement will then form the base of the February Absolute Return Letter.

Source: coindesk.com

As far as this month’s letter is concerned, for some odd reason – probably because I forgot to bring my crystal ball back to London when I returned from my Christmas break in Denmark last year – there was no mention of COVID-19 in last year’s January letter. I will try and make up for that this year.

Saxo Bank’s outrageous predictions

As I often do in January, I am also going to start this year with a mention of Saxo Bank’s ten (so-called) Outrageous Predictions for 2021. Steen Jakobsen, the CIO of Saxo Bank, and his team rarely disappoint, and this year is no exception. In no particular order, the ten predictions for 2021 are as follows:

- Amazon “buys” Cyprus

- Germany bails out France

- Blockchain tech kills fake news

- China’s new digital currency inspires tectonic shift in capital flows

- Revolutionary fusion design catapults humanity into energy abundance

- Universal basic income decimates big cities

- Disruption dividend creates Citizens Technology Fund

- A successful Covid-19 vaccine kills companies

- Sun shines on silver, which sizzles on solar panel demand

- Next-generation tech supercharges frontier and emerging markets

I am not going to go through every single one, but at least a couple of them deserve a mention. If you want to dig deeper, I suggest you go to Saxo Bank’s website which you can find here.

Let’s start with #3. I wholeheartedly agree that the blockchain technology will do tremendous damage to the existing financial infrastructure. I don’t know about fake news, but blockchain could effectively render commercial banks largely obsolete within the next ten years or so. Online retailers have done immense damage to many brick and mortar retailers more recently, and blockchain may do the same to many commercial banks in the years to come.

The other outrageous prediction I will comment on is #5, mostly because it is not outrageous at all. A lot has happened on the fusion front in 2020, and I am increasingly convinced that we are no more than 10-15 years away from being able to commercialise this revolutionary technology. To illustrate how powerful it is, imagine you go home and fill up your bathtub with water. You then take the lithium from two laptop batteries, and you put it all through a fusion reactor.

The outcome? Enough electricity to cover the needs of an average person in the UK for no less than 60 years! This will reduce the marginal cost of electricity to virtually zero and will have enormous implications on the world as we know it. The main risks are timing and high development costs. A fusion reactor emits no greenhouse gases, it cannot melt down like a fission reactor can, there are no enriched materials which can be used to develop nuclear bombs, and there are only modest amounts of nuclear waste. Does it get much better than that? For those of you keen to get the latest on fusion energy, I suggest you read these articles in Forbes Magazine, Financial Times and Science Alert. I would also recommend part II of our series on Investing in Natural Resources available here on ARP+.

My not-so-outrageous predictions

I am occasionally asked why pandemics don’t feature prominently on our list of risks to worry about, and my answer is always the same. The last pandemic which caused millions of deaths was the Spanish flu in 1918-20, i.e. almost exactly a century ago. If you take all once-in-a-lifetime risks into account, you cannot invest in equities at all. You can’t even buy government bonds. It is so far out on the left-hand side of the risk curve that it is impossible to plan for.

As we enter 2021, there are certainly risks which shouldn’t be ignored. I am not going to mention them all (what about an asteroid hitting Earth?) but, as I see it, three plausible risks stand out:

- The V-shaped economic recovery in 2021, which equity markets are taking for granted, fails to materialise. Either the COVID-19 vaccine doesn’t work as expected or rolling out the vaccination programme takes much longer than expected, turning 2021 into another year which can be largely written off.

- The massive increase in global money supply, which has been part of governments’ response to the health crisis, begins to have a rather unpleasant impact on inflation which financial markets react negatively to.

- For whatever reason (could be as a result of either (1) or (2) above), the runaway bull market in Big Tech finally punctures and retail investors who have dominated the buying of Big Tech for most of the past year panic, leading to a collapse of the (overvalued) US stock market. I think of this risk as a re-run of the collapse of Tokyo Stock Exchange, anno 1990.

As you may have noticed, COVID-19 dominates my ‘ensemble’ of 2021 risks to worry about. Am I suggesting that the pandemic is all we need to worry about as we enter 2021? Not at all, but those three risks stand out as I see things. More on that later.

Before I go there, allow me to briefly mention one or two other risks that I urge you not to ignore. As a colleague of mine often says, “you should always worry when there is nothing to worry about”. He is referring to complacency and how it often finds its way into the human mindset in benign times. We often see it – most recently last spring when, from one day to the next, COVID-19 was suddenly on everybody’s radar screen.

Another risk I am worried about is the state of the American Union – the sad reality that tens of millions of Americans remain convinced that the November elections were rigged despite there being no evidence whatsoever of any improprieties. However, I decided not to add it to my list above, as political incidents rarely have a lasting impact on financial markets. Unless you expect this one to end in civil unrest, perhaps even civil war (the risk of which is tiny in my opinion), it is not likely to have more than a passing effect on financial markets.

One final point before I drop the ball on this topic. The polarisation of American society is not really about Biden vs. Trump. In essence, it is about the fact that the gap between rich and poor is getting bigger and bigger, and the poorest 90%, who have suffered so much in recent years, are now saying that enough is enough. They see the mega-rich getting away with murder (not literally!) and think it is grossly unfair.

In the context of COVID-19, the very expansive monetary policy programme conducted by the Fed in 2020 has only made the difference in wealth bigger. That is due to the very positive impact Fed’s actions have had on financial asset prices – equities in particular. If you never read the September Absolute Return Letter about my old friend TINA, I recommend you do so. You can find it here. The wealthiest, who are always loaded with financial assets, have earned another gazillion in 2020, whereas many of the not-so-wealthy lost their job.

Source: Politifact

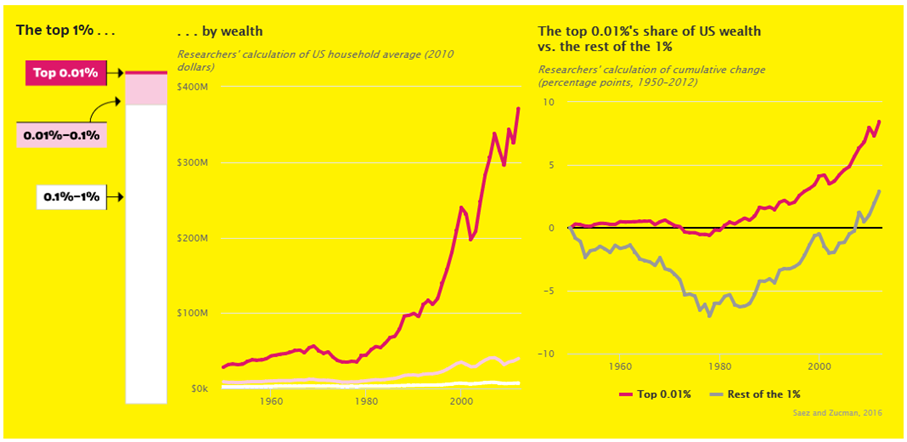

Unfortunately, none of the data I have access to is of recent date, but I can assure you the difference between rich and poor is even bigger today than it was 4-5 years ago when the data in Exhibits 2-3 was compiled. As you can see in Exhibit 2, the bottom 90% of Americans (in terms of wealth) are, at least relatively speaking, getting poorer. The fact that this has happened in a period of exceptional prosperity (2013-16) has turned the poorest 90% against the establishment in Washington DC.

Meanwhile, the top 1% are flying in business class, the top 0.1% in first class, while the top 0.01% take their own private jet. They don’t want to be seen on a commercial airliner! Recent years’ accumulation of wealth amongst the wealthiest 0.01% of Americans is almost obscene (Exhibit 3). Biden has a massive job in front of him if he wants to avoid further polarisation and even bigger problems.

Source: Chicago Boot Review

Risk #1: The V(accine)-shaped recovery fails to materialise

Following recent announcements on the various COVID-19 vaccines that either have been approved already or most likely will be approved shortly, Goldman Sachs upgraded its 2021 and 2022 GDP growth forecasts for various countries (Exhibit 4). The important thing to note here is the big difference between Goldman’s estimates and consensus estimates which, at the time Goldman Sachs released the research paper behind Exhibit 4, did not yet take into account the imminent release of the first vaccine (which has now happened). As you can see, the impact is highly significant, hence why Goldman Sachs chose to call the expected 2021 economic turnaround a V(accine)-shaped economic recovery – an elegant little detail which I have ruthlessly ‘stolen’.

Source: Goldman Sachs Global Investment Research

Now, the risk is that something doesn’t work according to plan. The efficacy of the vaccine may not be as good as early results suggest – either because the virus mutates (which has happened already) and the mutated version is resistant or because all those who are about to be vaccinated turn out to be immune for a few months only. Alternatively, as the vaccine programme has been rushed through, there may be side effects that we are currently not aware of. What is also possible is that the vaccination programme – vaccinating billions of people – proves a much bigger challenge than expected.

2021 could then turn into a another 2020, which has been about as bad as they get economically (see Goldman Sachs’ GDP estimates for 2020 in Exhibit 4 above). Should that happen, I am not sure equity markets will be as forgiving as they have been in 2020.

Risk #2: Inflation is coming

In the national accounts, savings are accounted for by subtracting total consumer spending from national income, and the savings rate is calculated as national savings divided by national income (Exhibit 5).

Source: Statista

As you can see, the US savings rate exploded earlier this year (like it did in many countries), as consumers struggled to maintain their usual spending patterns. What happened to all that money? Most of it was deposited in banks where it still is, despite the savings rate gradually normalising.

Source: MacroStrategy Partnership LLP

In the context of looming inflation, the aspect to focus on is the link between the change in excess bank deposits (the red line in Exhibit 6 below) and consumer price inflation (the blue line). The two are not perfectly correlated but, as is evident, growth in excess bank deposits often lead to a rise in consumer price inflation. The logic is quite simple. Think of bank deposits as consumers’ war chest. When conditions eventually return to normal, consumers have much more between their hands than they have had in a long, long time. How much that will affect CPI, only time can tell.

Risk #3: A collapse of overvalued US equity markets

Retail investors have been a significant driver of the bull market in US equities in 2020. How do I know that? For example, by looking at the volume in out-of-the-money single-stock call options with less than two weeks to expiration which increased dramatically as the year unfolded. Institutional investors rarely buy those sorts of options as they are considered lottery tickets, but many retail investors love them.

Furthermore, stocks favoured by retail investors (Facebook, Tesla, etc.) performed better than those favoured by institutional investors and dramatically better than the overall market. Goldman Sachs recently attempted to quantify that and, as you can see in Exhibit 7, the impact from retail investors was rather dramatic in 2020. When you cannot go shopping, you can always have a bit of fun in the stock market!

Source: Goldman Sachs Global Investment Research

Knowing that retail investors are almost always late to the party, I have an inkling that this could go terribly wrong in the not-so-distant future. What exactly will cause the reversal of fortune is difficult to say – maybe one of the risk factors already mentioned, maybe something entirely different. It is hard to say, but I do not like the fact that retail investors have been in the driver’s seat in 2020.

Concluding remarks

Despite the risks I have just pointed out, my base case for 2021 is still robust – at least for as long as CPI is under control. Strong GDP growth this year and next is likely to lead to robust corporate earnings growth. Thus, expect corporates to perform rather well for a while – both financially and in stock market terms. Having said that, as I pointed out earlier, GDP growth of the magnitude suggested by Goldman Sachs combined with solid corporate earnings growth could have a meaningful impact on inflation.

Sooner or later, CPI will begin to rise. Precisely when and by how much is hard to say but think about it the following way: Fed’s easy monetary policy programme in 2020 has led to a huge jump in US money supply. A jump of that magnitude would under normal circumstances cause inflation to rise almost instantly, but the significant output gap, which is a direct consequence of the pandemic, has pretty much eliminated that risk in the near-term.

In 1990, Goldman Sachs established the so-called GS Financial Conditions Index and, as you can see in Exhibit 8, financial conditions in the US are now the easiest on record. Easy financial conditions imply robust corporate investments and plenty of consumer spending, hence also above average GDP growth. Goldman’s GDP growth estimate for 2021 (5.3%) was established before the latest reading on financial conditions so, if anything, expect some modest upside risk to Goldman’s 2021 GDP estimate.

Source: Goldman Sachs Global Investment Research, Bloomberg

As I just said, a significant output gap is likely to prevent CPI from rising for a while. That said, it ought to be pointed out that (a) the output gap is significantly smaller in the US than it is elsewhere, and (b) GDP growth of the magnitude suggested by Goldman Sachs will eliminate much of the US output gap pretty quickly. Consequently, inflation could begin to rise as we move further into 2021.

Adding to the robust earnings outlook for this year and next, I expect the Fed to continue its very accommodative monetary policy programme. As we learned last year, don’t ever fight the Fed. The combination of an easy Fed and robust earnings growth should lead to benign investment conditions for a while.

Niels C. Jensen

5 January 2021