NewsLetter - December 2020

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFOLLOW-UP DEMENTIA TEST

From my friend Judy. Answers at the end. Don’t peek!!

Something for us seniors, too, to keep those aging gray matter cells active...not that YOU’RE that old. 1. Johnny's mother had three children. The first child was named April. The second child was named May. What was the third child's name? 2. There is a clerk at the butcher shop. He is five feet ten inches tall and he wears size 13 sneakers. What does he weigh? 3. Before Mt. Everest was discovered, what was the highest mountain in the world? 4. How much dirt is there in a hole that measures two feet by three feet by four feet? 5. What word in the English Language is always spelled incorrectly? 6. Billy was born on December 28th, yet his birthday is always in the summer. How is this possible? 7. In California, you cannot take a picture of a man with a wooden leg. Why not? 8. What was the President’s name in 1975? 9. If you were running a race, and you passed the person in 2nd place, what place would you be in now? 10. Which is correct to say, "The yolk of the egg are white" or "The yolk of the egg is white"? 11. If a farmer has 5 haystacks in one field and 4 haystacks in the other field, how many haystacks would he have if he combined them all in another field?

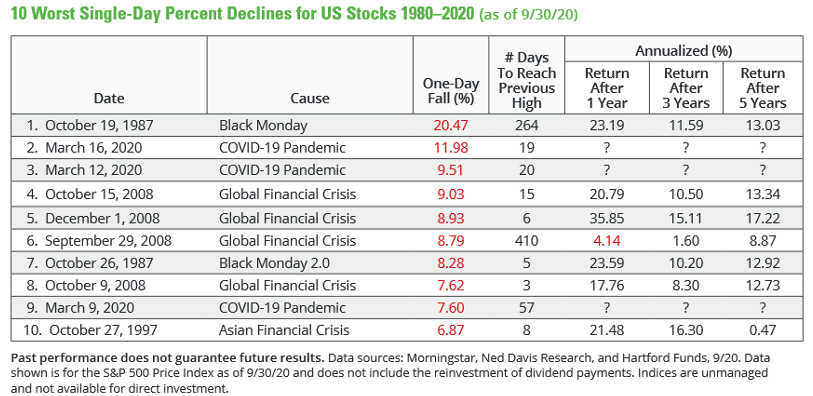

DON’T PANIC

If (rather when) there is a significant market “correction.” Remember it gets dark before it gets light.

SOBERING DATA

From my friend Monty

And remember, this data does not include dividends that, over time, account for 30 – almost 50% of market return. Read More

ALSO SOBERING

From my friend Peter

So, let's get things into perspective...209 seconds that will make you question your entire existence. Watch the video.

FUN PICTURES TO BRIGHTEN A DEPRESSING YEAR

(2020 IN CASE YOU DIDN'T NOTICE)

ONE WHOPPING BIG NUMBER

JPMorgan Admits to Manipulative Trading, Settles for Nearly $1B

The SEC says that JPMorgan and its affiliates have admitted to engaging in manipulative trading for nearly a decade and have agreed to settle charges from the securities regulator, the Department of Justice, and the Commodity Futures Trading Commission for close to $1 billion.

TIME WILL TELL

Wharton’s Jeremy Siegel Makes the Case for Stocks

“While Siegel is not calling the next collapse in tech shares, he believes valuations of many such stocks are totally disconnected from their earnings. And he thinks the vast gap between growth and value stocks, which seems to cycle to extremes, will narrow as investors shift into more core, sound traditional businesses that have yet to fully recover but should as the economy escapes Covid’s grasp…. ‘Value shares are poised to rally in 2021,’ says Siegel…”

AMAZING PICTURE – AMAZING STORY

I ALWAYS THOUGHT ED SULLIVAN WAS FOR THE NEARLY DEAD

Thanks to Alex for correcting me. Watch the video.

SOME INVESTORS TRIED TO WIN BY LOSING LESS. THEY LOST ANYWAY.

Excerpts from an article by one of my very favorite financial reporters, Jason Zweig with the Wall Street Journal.

“The market has a way of soaking people who think they’ve found a way to beat it. The latest case in point: ‘low-volatility’ funds”

An investment strategy for reducing risk in the long-run has raised it in the short run.

Funds holding stocks that fluctuate less than the market as a whole are supposed to do better in bad times while still faring well in good times. Their performance in 2020 has been perverse: Several lost at least as much as the market in February and March, but later lagged far behind when stocks shot up more than 50%.

The low-risk funds put old lessons in high relief: Historical returns often paint a distorted picture, rigid rules have unintended consequences and the market loves to make monkeys out of people who think they’ve solved it….

The low-risk funds are run according to rules, not human judgment. When share prices shatter, the funds generally can’t delete those with the wildest swings and immediately replace them with smoother

alternatives. Instead, the funds tend to make changes on a predetermined schedule—which, in 2020, just so happened to fall at the worst possible time for some….

Managers say these funds aren’t meant to be an investor’s sole or largest exposure to stocks, but rather one part of a diversified approach.

However, Elisabeth Kashner, director of ETF research at FactSet, says such funds often have been promoted as sweeping solutions. “When a product is sold with the implication that it’s going to deliver risk-adjusted outperformance,” she says, “what would it dislodge other than core portfolio holdings?”

It isn’t a mistake to try lowering your risk. It is a mistake, however, to assume that the future will resemble the past, that rules are infallible and that you should dive into any one strategy with both feet.”

A SIMPLE TECHNIQUE TO PROFIT FROM IPOS

Great headline. How could anyone pass up the opportunity to get rich with a “simple technique”?

“Fortunately, it's possible to get your bearings quickly when newly minted issues hit the ticker tape, so let's discuss a simple technique you can use to get up to speed. Just keep in mind that the vast majority of market participants should avoid all IPO exposure, like the plague, because the lack of price points can generate all sorts of dangerous situations.”

Have to wonder why anyone would share this “pot of gold at the end of the rainbow” with the immediate world. I’d recommend staying with “the vast majority of market participants” and “avoid all IPO exposure, like the plague.”

CURIOSITIES OF THE WORLD

From my friend Judy

THOSE WERE THE DAYS

The Fabulous 50’s Number 1 Hits By Year

This was “my time.” My introduction to REAL music was Rock Around the Clock and I still consider it one of the musical classics. I can’t begin to figure out why Deena wouldn’t let us use it for our wedding when she made her entrance.

1950 White Christmas Bing Crosby

1951 Come on-a My House Rosemary Clooney

1952

Unforgettable Nat King Cole

1953 You, You, You Ames Brothers

1954 That’s Amoré Dean Martin

1955

Rock Around the Clock Bill Haley

1956 Hound Dog / Don’t Be Cruel Elvis Presley

1957 Love Letters in the Sand Pat Boone

1958 It’s All In the Game Tommy Edwards

1959 Mack The Knife Bobby Dar

GET REAL!

The Higher You Aim The Worse You Get

From an article forwarded to me by my associate Marcos. A sober warning that unrealistic expectations may be detrimental to your wealth.

“Investors tend to have return goals that are way too high to be realistically achievable in the long run. A study from the Catholic University in Louvain, Belgium, looked at the trading accounts and stated return goals of more than 4,000 retail investors between 2008 and 2012. About one-third of these investors had a target return of 8% or more above inflation. Assuming a 2% inflation rate, that amounts to more than 10% average nominal returns. Another 41% had target returns of 5% to 7% above inflation. Given that a realistic assumption for the equity risk premium above inflation is somewhere around 3% to 7%, this means that three out of four retail investors try to achieve returns that can only be achieved with pure equity portfolios or riskier propositions. …

What the research found was that investors with a higher return target did miss their targets by a wider margin than investors with average return targets. And they did worse in terms of total return achieved.”

MORE SMILES

COVID HUMOR

If we can’t beat it, may as well laugh at it. From my friend Jerry.

- The dumbest, most useless thing I ever bought was a 2020 planner.

- I was so bored I called Jake from State Farm just to talk to someone.

- In 2019: Stay away from negative people. In 2020: Stay away from positive people.

- The world has turned upside down. Old folks are sneaking out of the house and their kids are yelling to stay indoors!

- This morning I saw a neighbor talking to her dog. It was obvious she thought her dog understood her. I came into my house and told my cat. We laughed a lot.

- Every few days try your jeans on just to make sure they fit. Pajamas will have you believe all is well in the kingdom. (Don't believe them.)

- Does anyone know if we can take showers yet ... or should we just only keep washing our hands?

- This virus has done what no woman has been able to do. Cancel sports, shut down all bars, and keep men at home!

- I never thought the comment, “I wouldn’t touch him/her with a 6-foot pole,” would become a national policy, but here we are!

- I need to practice social-distancing from the refrigerator.

- I hope the weather is good tomorrow for my trip to the backyard. I’m getting tired of the living room.

- The analogy "The curve is flattening so we can start lifting restrictions now” is like saying “The parachute has slowed our rate of descent, so we can take it off now.”

- Never in a million years could I have imagined I would go up to a bank teller wearing a mask and ask for money.

- The spread of the coronavirus is based on two things: How dense the population is.… How dense the population is.

SMART NOT BRILLIANT

Balanced portfolios WORK

A GLASS OF CARMEN ANYONE?

Extraordinary! Watch the video.

DIDN’T SEE THAT COMING

Zoom has passed Exxon in market capitalization, with only 1% of its workforce.

FOOD FOR THOUGHT

Before you decide to do your own stock picking or chase exotic investments.

“Harvard’s University’s endowment’s return lagged the U.S. stock market — again. For the fiscal year ending June 30, Harvard’s endowment produced a 7.3% return, versus a 7.5% total return for the S&P 500 (SPX). This marks the 12th year in a row in which the $42 billion portfolio fell behind the benchmark index. Also, as you can see from the accompanying chart, the endowment has lagged the S&P 500 over each of the 3-, 5-, 10- and 20-year horizons.”

AND MORE (RELATED) WISE ADVICE

From Larry Swedroe, one of my favorite thoughtful practitioners.

“…the surest way to win the loser’s game of active investing (trying to pick stocks and/or time the market) is to not play.” Read More

CHEER YOU UP

From my friend Alex

This pretty much condenses life into one minute, 19 seconds. If you don't see yourself in this video at least once, you've been living on another planet. Watch the video.

FOR MY CONTEMPORARIES

MORE FOR OLD FOLKS

- When one door closes and another door opens, you’re probably imprisoned.

- To me “drink responsibly” means don’t spill it.

- Age 60 might be the new 40 but 9:00 p.m. is the new midnight.

- It’s the start of a brand-new day and I’m off like a herd of turtles.

- The older I get, the earlier it gets late.

- When I say ”the other day,” I could be referring to anytime between yesterday and 15 years ago.

- I remember being able to get up without making sound effects.

FOR EVERYONE

From my friend Peter

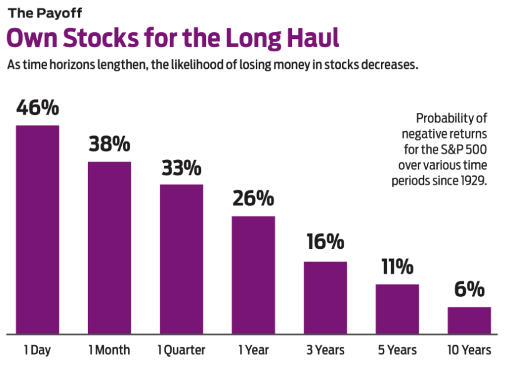

HANG IN THERE

I know you’ve heard of “stocks for the long haul.” Here’s a great graphic from Kiplinger showing why.

AMAZING!

A Murmuration of Starlings

Four Minutes of Sheer Wonder!

From my friend Peter

WHERE ARE THE CUSTOMERS’ YACHTS?

Ever wonder what the main criteria are for hiring a broker? Experience? Credentials? Education? Customer Service? I don’t think so.

Wells Fargo has fired “a sizeable group” of salaried advisors, and more FAs are expected to be terminated…Wells Fargo’s strategy is “to focus on a highly productive team of advisors and to manage out underperformers,…In short, we continue the trend of hiring larger producers than those who leave,” the spokesperson says.

DEPRESSING

From my friend Bob Veres’ newsletter.

I’ve been in this business a LONG time and you’d think by now nothing would surprise me, but this did. The moral is, READ the disclosures carefully and protect yourself. Insist your advisor sign the Committee for the Fiduciary Standard Oath.

Do LPL Clients Pay More for Mutual Funds?

“In response to the SEC’s Reg BI, the giant independent BD says, on the disclosures of its Strategic Asset Management platform “expressly waive LPL’s duty of best execution with respect to the price of its mutual fund share classes.” The firm also makes it clear that its reps have incentives to avoid trading charges, and pass them on to clients. There are 19 conflict disclosures on LPL’s website involving mutual funds paying the firm expenses such as marketing, record keeping, and networking fees. Funds pay LPL record keeping payments of up to 0.30% of assets or $25 per client position. Another disclosure says, “Client understands that the share class offered for a particular mutual fund through LPL’s program in many cases will not be the least expensive share class that the mutual fund makes available. In certain cases,” it continues LPL picks the share class based on “compensation for the administrative and record-keeping services” provided by the fund. (p. 31)”

SAME SONG SECOND VERSE

I thought I’d add an excellent suggestion from my friend Nikolaus. He suggested that I remind my readers that they should leave short term predictions to the gurus. Of course, they usually get it wrong, hence our focus on investing for the long term. Any funds needed for the next 5 years should be in liquid vehicles (e.g. money market), so it won’t matter what the short-term impact of a new administration turns out to be and to not fret so much.

So, in that vein, I thought I’d remind everyone of reality and provide an excerpt from an earlier newsletter on a similar theme.

OCTOBER 2015

GREAT QUOTE

From an executive at a tech company when asked about the future of the computer business.

“I’m too smart and I’m too dumb to predict the future.” I think I’ll use it next time a reporter asks me about my prediction for the market next year.

A MIDYEAR BUCKET PORTFOLIO CHECKUP

Christine Benz (Christine is the Director of Personal Finance at Morningstar)

A Bucket Strategy Review Before we delve into the Bucket portfolios' performance, let's first review what the Bucket approach is designed to do. As pioneered by financial planner Harold Evensky, the Bucket strategy for retirement portfolios centers around an extraordinarily simple premise: By holding enough cash to meet living expenses during periodic weakness in stock or bond holdings–or both–a retiree won't need to sell fallen holdings. That leaves more of the portfolio in place to recover when the market eventually does.

GOOD ONES

From my partner Michael’s dad.

- Going to church doesn't make you a Christian any more than standing in a garage makes you a car.

- Light travels faster than sound. This is why some people appear bright until you hear them speak.

- If I agreed with you, we'd both be wrong.

- War does not determine who is right – only who is left.

- Knowledge is knowing a tomato is a fruit; wisdom is not putting it in a fruit salad.

- Evening news is where they begin with ”Good evening,” and then proceed to tell you why it isn't.

- To steal ideas from one person is plagiarism. To steal from many is research.

- How is it one careless match can start a forest fire, but it takes a whole box to start a campfire?

- Dolphins are so smart that within a few weeks of captivity, they can train people to stand on the very edge of the pool and throw them fish.

- Whenever I fill out an application, in the part that says "In an emergency, notify:" I put "DOCTOR."

- I didn't say it was your fault; I said I was blaming you.

- Why does someone believe you when you say there are four billion stars, but check when you say the paint is wet?

- Why do Americans choose from just two people to run for President and 50 for Miss America?

- A clear conscience is usually the sign of a bad memory.

- You do not need a parachute to skydive. You only need a parachute to skydive twice.

- Always borrow money from a pessimist. He won't expect it back.

- Hospitality: making your guests feel like they're at home, even if you wish they were.

- I used to be indecisive. Now I'm not sure.

- I always take life with a grain of salt, plus a slice of lemon, and a shot of tequila.

- When tempted to fight fire with fire, remember that the Fire Department usually uses water.

- You're never too old to learn something stupid.

- Nostalgia isn't what it used to be.

- A bus is a vehicle that runs twice as fast when you are after it as when you are in it.

- Change is inevitable, except from a vending machine.

APPLES DON’T TASTE LIKE WATERMELONS

Decade's top-performing actively managed funds with over $1B in AUM

“The 20 top-performing active products with at least $1 billion in assets under management have generated an average 10-year annualized return of more than 20%, Morningstar Direct data show.. .By comparison, the SPDR S&P 500 ETF Trust (SPY) and the SPDR Dow Jones Industrial Average ETF Trust (DIA) posted 10-year returns of 13.69% and 12.52%, respectively.”

ABSURD! Of the 20 funds listed, 13 were sector funds and of those 10 were technology. The remaining were high growth. Not one was remotely related to an investment in the S&P 500 or the DOW. For goodness sake, when considering an investment in a “hot” fund, ignore the marketing hype and misleading financial pornography. Compare the fund performance to an appropriate benchmark; i.e., an investment that plays in the same sandbox. Best bet is to look for a comparable ETF. Also, be sure and use after-tax returns (unless in a sheltered account) and risk-adjusted returns (e.g. Sharpe Ratio). Read More

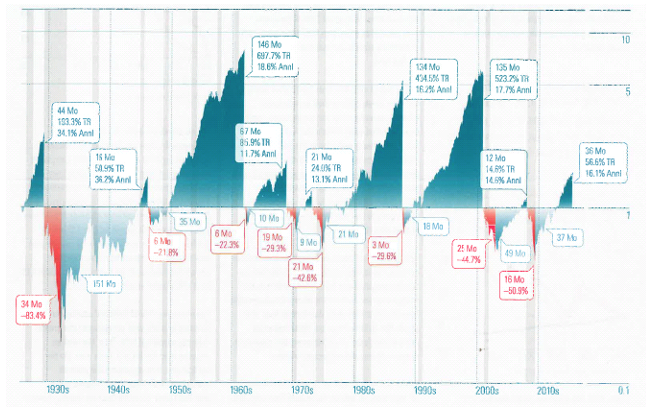

HISTORY OF BULL MARKETS

From Morningstar Markets Observer

IT PAINS ME TO SAY THIS

But sometimes Jim Cramer gives good advice

Jim Cramer's Investing Rule 7: No One Made a Dime by Panicking

Action Alerts Plus portfolio manager and TheStreet's founder Jim Cramer always tells investors not to freak-out when the market tanks. That's why Rule #7 of his 25 Investing Rules is a big reminder that no one makes money by panicking!

OH MY

“People are spending over three times more money ‘gambling’ on hot stocks than at casinos and on lottery tickets and sports betting.”

According to just-completed research, gambling in the stock market is far more prevalent than previously imagined. The study’s authors — all finance academics — calculate that the dollar value of the gambling is at least three-and-one-half times the combined global total of activities at casinos, online gambling, gaming machines, bingo/keno, lotteries, horse tracks, and sports betting.

The study, titled “Only Gamble in Town,” was conducted by Alok Kumar of the University of Miami, Huong Nguyen of the University of Da Nang in Vietnam, and Talis Putnins of the University of Technology in Sydney, Australia.

DECEMBER 2017 WORTH READING

These excerpts from Thinkadvisor.com’s “Navigating Uncertain Rewards and Certain Risks” by Bob Seawright, CIO for Madison Avenue Securities, are a bit long, but I thought it was worth devoting the space. The bold highlights are mine.

Equity investing offers uncertain rewards but certain risks, no matter how beautiful the weather or calm the seas. These risks are often opaque to us. There is no way to know if and when those risks will bite and what the extent of the damage will be.

Yet investing in stocks is crucial for investors to reach their financial goals because of the returns they provide. Risk and reward are inherently connected. Suppose, for example, back in 1928 you had invested in stocks (the S&P 500). Bonds (10-year U.S. Treasury notes) and cash (three-month U.S. Treasury bills) and held through the end of 2016.

Over that period stocks averaged 11.4% annual returns, bonds 5.2% and cash 3.5%. In other words, if you had invested $100 in each of those categories, at the end of 2016 you would have had $1,988 in the cash account, $7,110.65 in the bond account and an astounding $326,645.87 in the stock account — over that period stocks earned 165 times more than cash and 46 times more than bonds.

Risk & Returns

Unfortunately, however, that enormous benefit comes with drawbacks of risk. Stocks suffered enormous losses of more than 20% six times between 1928 and 2016, and in 23 of the 89 years — roughly one in four — provided negative returns…

What to Do?

The best advice most of the time is to accept that drawdown risk is the price paid for the returns stocks provide compared with bonds and cash. Other possible investments, despite the latest financial engineering techniques, cannot measure up in performance either. For example, when analyzed on an asset-weighted basis, as Simon Lock has documented, if all the money that has ever been invested in hedge funds had been invested in U.S. Treasury bills instead, the overall results would have been twice as good…

The current long bull market may have lulled investors into a false sense of security, thinking that there are no risks lurking beneath the surface. Smart investors will prepare for inevitable drawdowns before they happen. Reality may bite, but it need not eat you.

MURGATROYD!

How many of you remember that word? Would you believe the spell-checker did not recognize the word Murgatroyd? Heavens to Murgatroyd! (“Heavens to Murgatroyd” is American in origin and dates from the mid 20th century. The other day a not so elderly (I say 75) lady said something to her son about driving a jalopy; and he looked at her quizzically and said, "What the heck is a jalopy?" He never heard of the word jalopy!! She knew she was old.... but not that old. Well, I hope you are hunky-dory after you read this and chuckle.

Some old expressions have become obsolete because of the inexorable march of technology. These phrases include: “Don't touch that dial.” “Carbon copy.” “You sound like a broken record.” “Hung out to dry.”

Back in the olden days, we had a lot of moxie. We'd put on our best bib and tucker, to straighten up and fly right. Heavens to Betsy! Gee whillikers! Jumping Jehoshaphat! Holy moly! We were in like Flynn and

living the life of Riley, and even a regular guy couldn't accuse us of being a knucklehead, a nincompoop, or a pill. Not for all the tea in China!

Back in the olden days, life used to be swell, but when's the last time anything was swell? Swell has gone the way of beehives, pageboys, and the D.A., of spats, knickers, fedoras, poodle skirts, saddle shoes, and pedal pushers. Oh, my aching back! Kilroy was here, but he isn't anymore. We wake up from what surely has been just a short nap, and before we can say, “Well, I'll be a monkey's uncle!” or, “This is a fine kettle of fish!” we discover that the words we grew up with, the words that seemed omnipresent as oxygen, have vanished with scarcely a notice from our tongues and our pens and our keyboards.

Poof, go the words of our youth, the words we've left behind. We blink, and they're gone. Where have all those great phrases gone? Long gone: Pshaw. The milkman did it. Hey! It's your nickel. Don't forget to pull the chain. Knee-high to a grasshopper. Well, fiddlesticks! Going like sixty. I'll see you in the funny papers. Don't take any wooden nickels. Wake up and smell the roses.

It turns out there are more of these lost words and expressions than Carter has liver pills. This can be disturbing stuff! We of a certain age have been blessed to live in changeable times. For a child, each new word is like a shiny toy, a toy that has no age. We at the other end of the chronological arc have the advantage of remembering there are words that once did not exist and there were words that once strutted their hour upon the earthly stage and now are heard no more, except in our collective memory. It's one of the greatest advantages of aging. Leaves us to wonder where Superman will find a phone booth...See ya later, alligator! Oki-doki!

WHY I LIKE RETIREMENT

Question: How many days in a week?

Answer: 6 Saturdays, 1 Sunday.

Question: When is a retiree’s bedtime?

Answer: Two hours after falling asleep on the couch.

Question: How many retirees does it take to change a lightbulb?

Answer: Only one, but it might take all day.

Question: What is the biggest fight of retirees?

Answer: Not enough time to get everything done.

Question: Why don’t retirees mind being called Seniors?

Answer: The term comes with a 10% discount.

Question: Among retirees, what is considered formal attire?

Answer: Tied shoes.

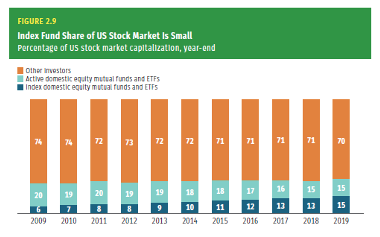

IGNORE THE NONSENSE

Often hyped in the financial pornography that index funds will lead to a market collapse. Turns out they’re not that big a player after all.

EVEN FOR MY OLD GEEZER READERS

Like me…..

The older I get, the earlier it gets late.

I finally reached the Wonder Years:

I wonder where I parked the car?

I wonder where I left my phone?

I wonder where my glasses are?

I wonder what this is?

HERE ARE THE ANSWERS: (NO PEEKING!)

- Johnny’s mother had three children. The first child was named April. The second child was named May. What was the third child's name?

Answer: Johnny, of course.

- There is a clerk at the butcher shop; he is five feet ten inches tall, and he wears size 13 sneakers. What does he weigh?

Answer: Meat

3 Before Mt. Everest was discovered, what was the highest mountain in the world? Answer: Mt. Everest; it just wasn't discovered yet. [You’re not very good at this are you?]

- How much dirt is there in a hole that measures two feet by three feet by four feet?

Answer: There is no dirt in a hole.

- What word in the English language is always spelled incorrectly? Answer: Incorrectly

- Billy was born on December 28th, yet his birthday is always in the summer. How is this possible? Answer: Billy lives in the Southern Hemisphere.

- In California, you cannot take a picture of a man with a wooden leg. Why not? Answer: You can't take pictures with a wooden leg. You need a camera to take pictures.

- What was the President's name in 1975? Answer: Same as is it now – Donald Trump.

- If you were running a race, and you passed the person in 2nd place, what place would you be in now?

Answer: You would be in 2nd. Well, you passed the person in second place, not first.

- Which is correct to say, "The yolk of the egg are white," or "The yolk of the egg is white"? Answer: Neither, the yolk of the egg is yellow. [Duh]

- If a farmer has 5 haystacks in one field and 4 haystacks in the other field, how many haystacks would he have if he combined them all in another field?

Answer: One. If he combines all of his haystacks, they all become one big one.

Hope you enjoyed it. STAY SAFE!

Harold Evensky

Founder

Evensky & Katz / Foldes Financial Wealth Management

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz / Foldes Financial Wealth Management), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Evensky & Katz / Foldes Financial Wealth Management. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Evensky & Katz / Foldes Financial Wealth Management is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. If you are a Evensky & Katz / Foldes Financial Wealth Management client, please remember to contact Evensky & Katz / Foldes Financial Wealth Management, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. A copy of the Evensky & Katz / Foldes Financial Wealth Management’s current written disclosure statement discussing our advisory services and fees is available upon request.

© Evensky & Katz/ Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits