Schwab Market Perspective: Watching the Wheels

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEncouraging news about COVID-19 vaccines has boosted hope for stronger economic growth, kicking off a rotation in stocks and equity sectors as investors look to a brighter future. However, near-term volatility is possible, as we’re not yet out of the coronavirus tunnel.

Nonetheless, investor focus has shifted toward more-cyclical sectors that tend to perform well when the economy is improving, such as Financials, Energy, Information Technology and Consumer Discretionary. Investors also have begun to move beyond the “big five” stocks (by market capitalization) in the S&P 500—Apple, Microsoft, Amazon, Facebook and Alphabet/Google—which outperformed during the earlier pandemic period.

Globally, emerging-market stocks have begun to outpace international developed stocks and U.S. stocks, another sign of rotation and a possible signal of things to come in 2021. A similar turning has been seen in the fixed income market, where emerging-market and high-yield bonds have outperformed U.S. Treasuries in recent months.

U.S. stocks and economy: A broad market rotation

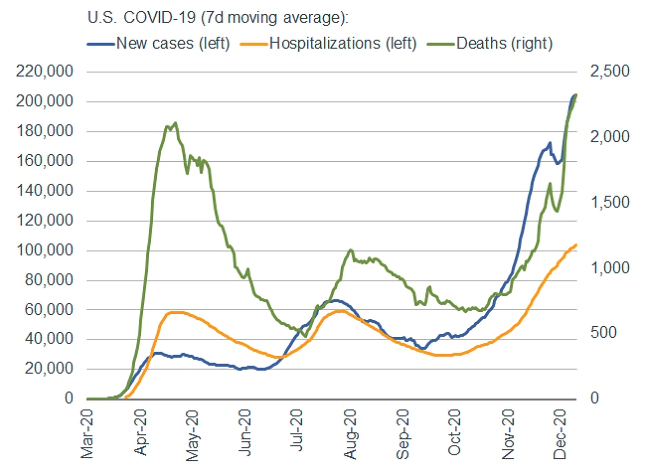

Despite brighter days on the horizon, as we approach the end of the year, the economic recovery has narrowed and economic growth in the near term is likely to struggle. The coronavirus continues to spread at a rapid pace, with an increase in hospitalizations and deaths unfortunately following close behind. As you can see in the chart below, the third wave has pushed the United States to fresh records for all three.

COVID-19 cases, hospitalizations, and deaths are still rising

Source: Charles Schwab, Bloomberg, as of 12/9/2020.

The reported success of vaccine trials by Pfizer, Moderna, and Oxford/AstraZeneca has boosted enthusiasm about a sooner-than-expected rebound in economic growth (and subsequent return to normal activity). However, various manufacturing and logistical issues still threaten an effective rollout of the vaccine, not to mention the difficulty in forecasting the public acceptance and true effectiveness of each vaccine.

While expectations for a more robust recovery have grown, the spread of the virus remains the largest issue in the near term. Mass shutdowns aren’t likely to go back into effect, but regional restrictions have been reintroduced in some states and cities.

The positive vaccine data and attendant uptick in forward growth expectations have supported U.S. equities to an incredibly large degree since the beginning of November. As major indices climbed to new highs, more traditional cyclical sectors—such as Financials and Energy—led the market higher, with participation among stocks broadening out. Moving into December, investors continue to favor names outside of sectors that fared the best during the pandemic—namely, Information Technology and Consumer Discretionary.

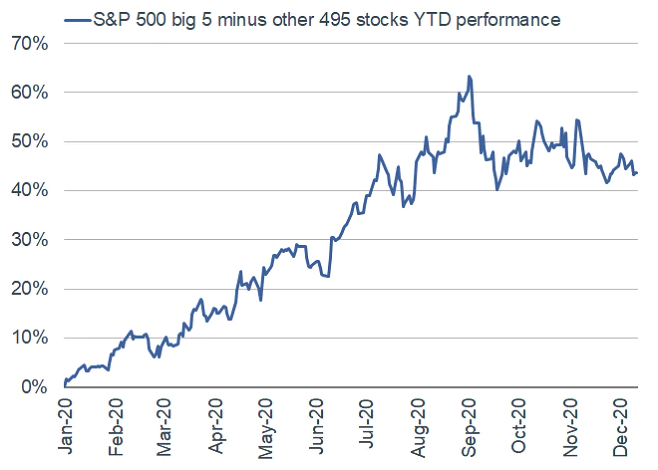

With that has also come a bias away from the “big five” stocks in the S&P 500, and outperformance of the other 495 stocks, as you can see in the chart below. You can also see that as the market climbed to its September 2nd highs, the former cohort outpaced the latter by 62 percentage points on a year-to-date basis (the “big five” were up 65% and other 495 stocks were up 3% at that point). That trend has since reversed, modestly, as the big five have since fallen by 7%, while the other 495 have risen nearly 7%.

Big five stocks are losing leadership status

Source: Charles Schwab, Bloomberg, as of 12/9/2020. Big 5 stocks include Alphabet, Amazon, Apple, Facebook, and Microsoft. Past performance is no guarantee of future results.

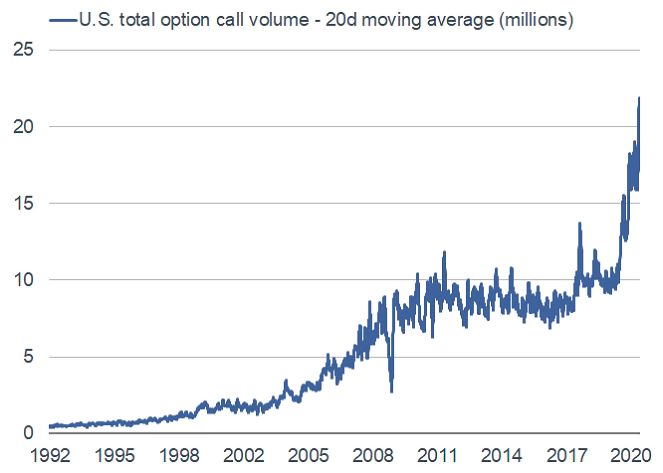

The five largest companies have seen their dominance wane in terms of performance lately, but they still represent more than a fifth of the index in terms of market cap—and unfortunately, frothy sentiment has not eased. A larger risk for stocks in the near term is the buildup in excessive optimism, now pervasive within both behavioral and attitudinal measures of sentiment. Particularly within the options market, you can see that speculation has spiked considerably: Call option volume across all U.S. exchanges (measured on a 20-day moving average) is averaging more than 21 million contracts. (A call buyer gains the option to buy an asset at a specified price, and the buyer typically profits if the underlying asset increases in price.)

Call option frenzy confirms rampant speculation

Source: Charles Schwab, Bloomberg, as of 12/9/2020.

Stretched sentiment itself doesn’t portend an immediate reversal for stocks, but it does suggest the market may be more vulnerable to negative catalysts. Given the nature of this crisis, those would likely come in some form of virus- or vaccine-related news. Regardless of the murkiness associated with the pandemic, however, we continue to encourage discipline around diversification and rebalancing.

Global stocks and economy: Emerging market leadership

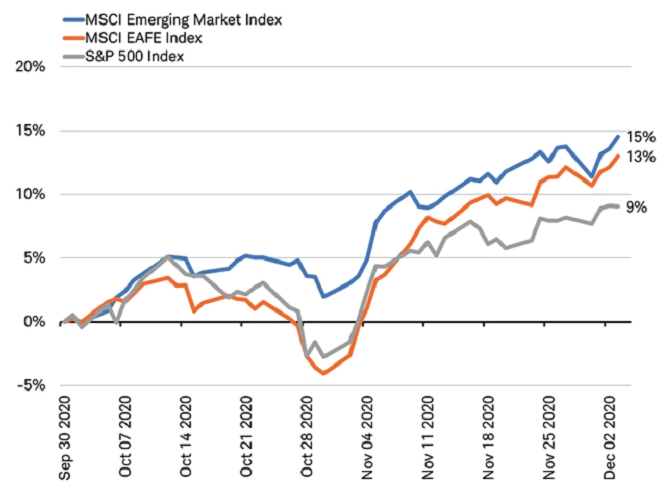

The fourth quarter has been a powerful one for global stocks, with the MSCI World Index posting double-digit percentage gains through December 3. Optimism over vaccines and the fading of much of the uncertainty around the U.S. elections helped drive the market. Emerging market (EM) stocks led the gains, posting a 15% rise compared to 13% for international developed stocks and 9% for U.S. stocks, as you can see in the chart below. We believe this performance may foreshadow things to come in 2021.

Fourth quarter performance has been strong

Source: Charles Schwab, Bloomberg data as of 12/3/2020. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Although China has led the recovery in the global economy and markets in 2020, fourth-quarter outperformance by EM stocks was concentrated elsewhere. In fact, Chinese stocks (measured by the MSCI China Index) lagged their EM and international developed peers; tracking closely with the S&P 500, they increased by 9.3%. This may be because Asia has less to gain from a vaccine, as the virus is largely under control in much of the region. China’s economy is already growing rapidly after fully recovering from the pandemic, with the EM Asian region having benefited from a pandemic-related boom for its exports.

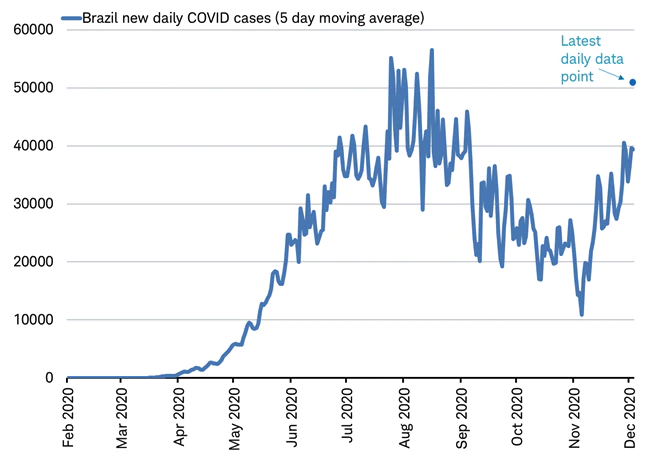

EM stocks’ strong performance came from countries outside Asia: Latin America, Eastern Europe, Africa, and the Middle East. Latin America, led by Brazil, has posted a 30% gain so far in the fourth quarter, measured by the MSCI Brazil Index in U.S. dollars. Equities have remained resilient despite the backdrop of Brazil (and the broader Latin America region) experiencing rising new daily COVID cases and securing a much smaller amount of vaccine doses relative to population size compared to Europe or the United States.

Brazil daily new virus cases on the rise again

Source: Charles Schwab, Bloomberg data as of 12/3/2020.

These gains are supported by rising prospects for a global recovery in travel and transportation in 2021, which are in turn powering a shift to leadership for the Energy and Materials sectors in the fourth quarter—lifting commodity-sensitive EMs in Latin America, Eastern Europe, Africa and the Middle East regions.

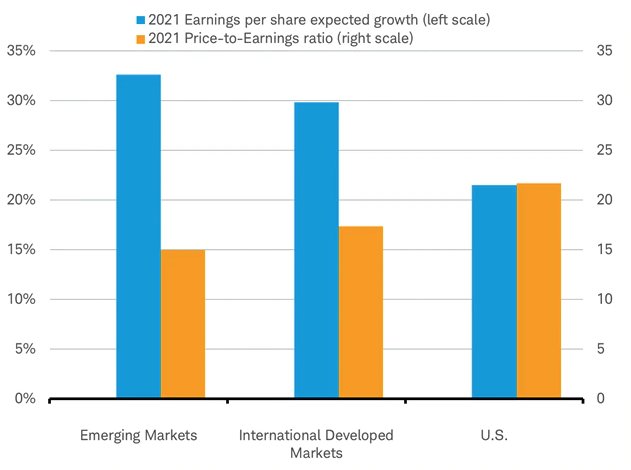

Even if vaccine immunization programs in EMs significantly lag those in developed markets, the next chart shows the recovery in global demand may drive earnings of EM companies to exceed those of both the U.S. and international developed markets next year, according to Wall Street analysts’ 2021 consensus estimates. Significantly lower valuations seem to be boosting the potential for EM outperformance. Although EMs often offer lower valuations than developed markets, the gap is wide compared to the historical average.

2021 expected earnings growth and price-to-earnings ratio by region

2021 price-to-earnings ratio is defined as current price divided by 2021 expected earnings per share.

Source: Charles Schwab, FactSet data as of 12/4/2020.

With lower valuations, stronger earnings expectations, and the potential for a weaker dollar, EM stocks’ outperformance in the current quarter may signal a similar outcome for 2021.

Fixed income: Time for caution

In early December, bond yields rose to the highest levels since the onset of the COVID-19 crisis, fueled by optimism about future economic growth. With vaccines on the way, markets are overlooking the near-term ongoing damage to the economy and pricing in stronger growth for the second half of 2021. The 10-year Treasury yield is approaching 1% for the first time since March and the yield curve (the difference between short and long-term yields) has steepened.

The 10-year Treasury yield is nearing 1%

Source: Bloomberg. 10-year Treasury yield (USGG10Y Index). Daily data as of 12/7/2020. Past performance is no guarantee of future results.

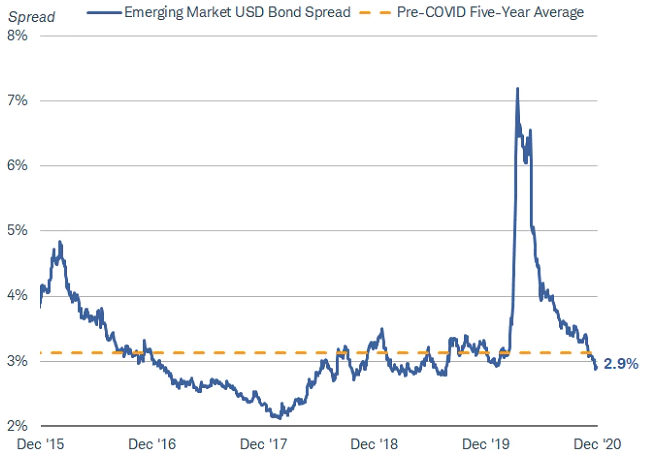

Higher risk segments of the market, such as high-yield and emerging-market bonds, have outperformed Treasuries over the past few months—another sign that investors anticipate stronger growth in 2021. Yields for sub-investment-grade bonds have fallen to record lows and the yield spread between emerging-market bonds and Treasuries has fallen back to near pre-pandemic levels.

EM bond spreads are back near the pre-COVID average

Source: Bloomberg. Bloomberg Barclays Emerging Market U.S. Dollar Aggregate Option Adjusted Spread Index (EMUSOAS Index). Daily data as of 12/7/2020. Past performance is no guarantee of future results.

The optimism about the longer-term prospects for the economy is consistent with our views. In our 2021 outlook, we suggest that 10-year Treasury yields will likely trade in a range of 1% to 1.6% while short-term interest rates will remain anchored near zero. We see the next year as one where investors will need to focus on earning coupon income rather than investing for price gains. That suggests taking some form of credit risk.

However, now that the consensus view has moved toward optimism and the extra yield you get for investing in riskier bonds is shrinking, we believe investors need to tread cautiously. Both monetary and fiscal policy may come in short of expectations.

Market expectations for further easing from the Federal Reserve are vulnerable to disappointment. Many investors expect the Fed to hold down long-term interest rates by increasing the amount of long-term bonds it buys. While that’s an option available to the Fed, we don’t expect it to happen at the upcoming December meeting, based on comments from various Fed officials. Any disappointment from the central bank could be a source of volatility.

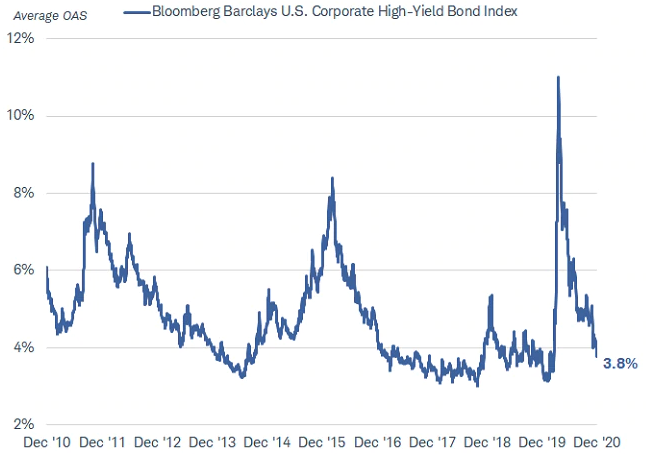

The terms of a potential fiscal relief package are still very much up in the air, but may not be enough to help some industries and companies survive through the winter. Consequently, defaults may rise in the high-yield bond market. With prices high, the market is susceptible to a setback. We suggest investors focus on higher-rated bonds within the high-yield market (BB rated) to mitigate some of the risk. Similarly, Congress may not allocate enough funds to state and local governments to avoid some downgrades in areas experiencing the most stress on budgets. In the municipal market, we favor bonds rated AA or above.

High yield spreads have continued to fall

Source: Bloomberg. Bloomberg Barclays US Corporate High Yield Average OAS (LF98OAS Index). Monthly data as of 11/30/2020. Past performance is no guarantee of future results.

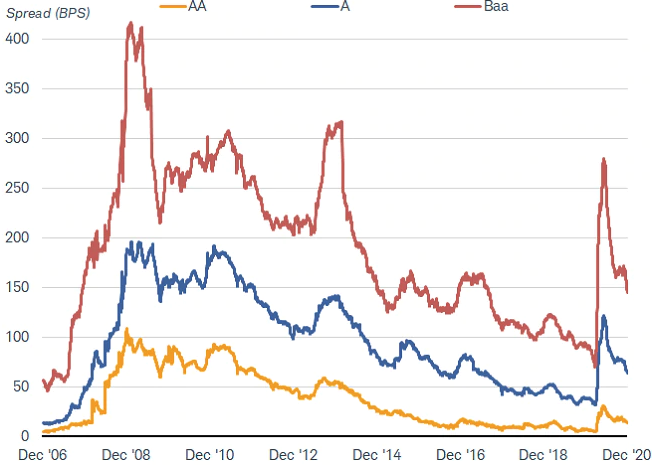

Spreads on munis have come back from their previous highs

Source: Bloomberg Barclays AAA, AA, A, and Baa Municipal Bond Indexes. As of 12/4/20. Difference in yields over time may be due to different index characteristics such as durations, average coupons, or other characteristics. Past performance is no guarantee of future results.

Among the riskier segments of the market, we believe emerging-market bonds still offer an opportunity to invest for yield in an improving global economy. However, the immediate path could be rocky due to potential setbacks to the global recovery. Overall, while we’re still optimistic about the long-term outlook, we suggest caution in the near term.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Currencies are speculative, very volatile and are not suitable for all investors.

Options carry a high level of risk and are not suitable for all investors. Certain requirements must be met to trade options through Schwab.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

All corporate names are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits