The Franklin Templeton–Gallup Economics of Recovery Study has heralded some interesting results in regard to the attitudes and behavior of Americans in response to the ongoing pandemic—and what developments could change both. Our Fixed Income CIO Sonal Desai shares her thoughts on the latest wave of survey findings, including the value of trusted advice in navigating financial and investment concerns.

In this post, I want to focus on another set of insights that emerged from the fourth pulse of our Franklin Templeton-Gallup Economics of Recovery Study (there were too many to fit them all in my prior post!)

Uncertainty and information have emerged as two recurrent key themes in our study. Uncertainty—both about COVID-19 and the economy—has a major impact on our attitudes and behaviors, and we know that uncertainty tends to depress both consumption and investment. Getting the right information is a key antidote to uncertainty, but our very first pulse showed that getting the right information is no easy task. You need to find expert advice that you can trust.

Our latest poll shows that equity investors with financial advisers are much more likely to feel “very confident” in their investment strategy compared to those without advisers—by a full 20 percentage points.1 This confidence-boosting impact works across income levels: working with a financial adviser gives greater confidence to investors with lower incomes as well as to wealthier ones.

One might object that this should not be too surprising: once you have decided to take more active control of your financial future and engaged professional help to shape your investment strategy, you should feel more confident in it. True enough, but I see three important implications here.

First, in an era dominated by skepticism toward “the experts,” it’s reassuring to see that about half of all investors (48% in our poll) turn to expert advice to secure their financial future and feel good about it. Maybe this points to a difference between the “headline-grabbing” experts and those who work in the trenches to help people.

Second, in my mind it confirms the importance of an active approach to investment management. I have emphasized in previous posts that I believe active investment management will prove a winning strategy in the coming quarters and years, because the ability to pick the right industries and credit names will provide crucial added value. Yes, working with a financial adviser is also consistent with investing mostly in passive strategies, but it can probably be especially helpful in guiding an active investment strategy.

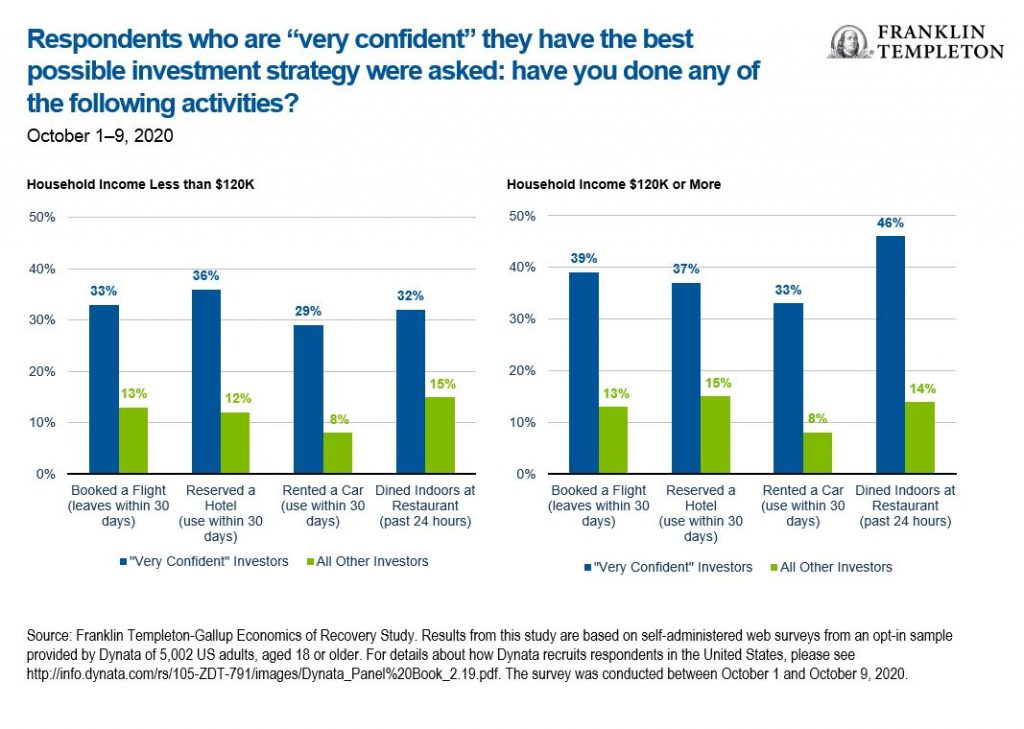

Third and most important, our pulse reveals that confidence in one’s investment strategy and financial future gives people greater confidence to engage in a broad range of economic activities that will prove crucial to the recovery, such as booking a flight, renting a car, reserving a hotel room and dining at a restaurant. People who feel very confident in their investment strategy are 2-3 times more likely to engage in these activities than other investors, according to our poll.

Financial advisers have always helped educate investors about their investment options, but our latest poll results show that their steady hand is also correlated with a stronger sense of control and confidence by investors in their financial future, which translates into broader engagement in consumer activity that the economy needs now. By laying the groundwork for investor confidence, advisers’ work is enabling the type of consumer confidence needed to stimulate further economic recovery.

This contribution by financial advisers could soon trigger a virtuous circle with the other key factor highlighted by our latest pulse: a COVID-19 vaccine.

In early results from our survey project, 70% of Americans said the development of an effective vaccine would have an important impact on their willingness to go back to normal spending habits.2 But our latest survey pulse showed that how and when the vaccine is brought to the public will be crucial; as I noted in my previous post, the results indicated that Democrats would be much more willing to take a vaccine (by eight percentage points) if it were brought to market in early 2021 rather than in 2020. This suggested that a significant number of people would have lower confidence in a vaccine if it were launched under the sitting administration. We also found that many more Americans would be ready to take a vaccine found to be 100% effective rather than just 50% (the threshold which is one of the conditions for US Food and Drug Administration approval).

Over the past several days we have seen two relevant developments: Joe Biden has clinched the US presidential election—though the results are not yet official—and a COVID-19 vaccine developed by pharmaceutical company Pfizer has been declared to be 90% effective. If both of these results are confirmed, a vaccine might hit the market sooner rather than later, and under conditions that would facilitate a broader and faster take-up in the population. As our polls have indicated, this would encourage a majority of people to return to normal economic behavior. At the same time, this would likely have a positive impact on stock prices (this has indeed been the knee-jerk response to the vaccine announcement), which would boost the greater sense of financial confidence nurtured by financial advisers, and have a further positive impact on people’s willingness to engage in consumption activities.

What about the implications for interest rates? If, as seems to be the case at the time of writing, we head into 2021 with a divided Congress, the scale of further fiscal stimulus will likely be smaller than many people expected in the case of a “blue sweep” mirroring the 2016 outcome. On the other hand, the early deployment of a vaccine could mean that even a smaller fiscal stimulus would suffice to give an important boost to the economy; meanwhile, the Fed has clearly indicated it will maintain a very accommodative stance for quite a while longer.

All this would skew the odds in favor of a faster pick-up in inflation. Nothing dramatic, but as I have mentioned in the past, it would not take much to exceed the very sanguine consensus inflation expectations. And our latest pulse has also shown that since the pandemic started, most consumers have experienced price rises on the goods and services they consume. Long-term yields have already moved sharply up on the latest news about the vaccine, confirming that risks remain tilted towards higher rates. I expect this trend will be confirmed in the coming months.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Actively managed strategies could experience losses if the investment manager’s judgment about markets, interest rates or the attractiveness, relative values, liquidity or potential appreciation of particular investments made for a portfolio, proves to be incorrect. There can be no guarantee that an investment manager’s investment techniques or decisions will produce the desired results.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com – Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

_________________________________________

1. Source: Franklin Templeton-Gallup Economics of Recovery Study. Results from this study are based on self-administered web surveys from an opt-in sample provided by Dynata of 5,002 US adults, aged 18 or older. For details about how Dynata recruits respondents in the United States, please see http://info.dynata.com/rs/105-ZDT-791/images/Dynata_Panel%20Book_2.19.pdf. The survey was conducted between October 1 and October 9, 2020.

2. Source: Franklin Templeton-Gallup Economics of Recovery Study. Results from this study are based on self-administered web surveys from an opt-in sample provided by Dynata of 5,002 US adults, aged 18 or older. For details about how Dynata recruits respondents in the United States, please see http://info.dynata.com/rs/105-ZDT-791/images/Dynata_Panel%20Book_2.19.pdf. The survey was conducted between July and October, 2020.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments