Despite the COVID-19 pandemic, emerging markets have shown a continued appetite for structural reforms that could lay the foundation for lasting economic recoveries, according to our Emerging Markets Equity team. Here are some highlights of news and events driving emerging markets during the month of October, and where the team sees opportunities today.

Three Things We’re Thinking About Today

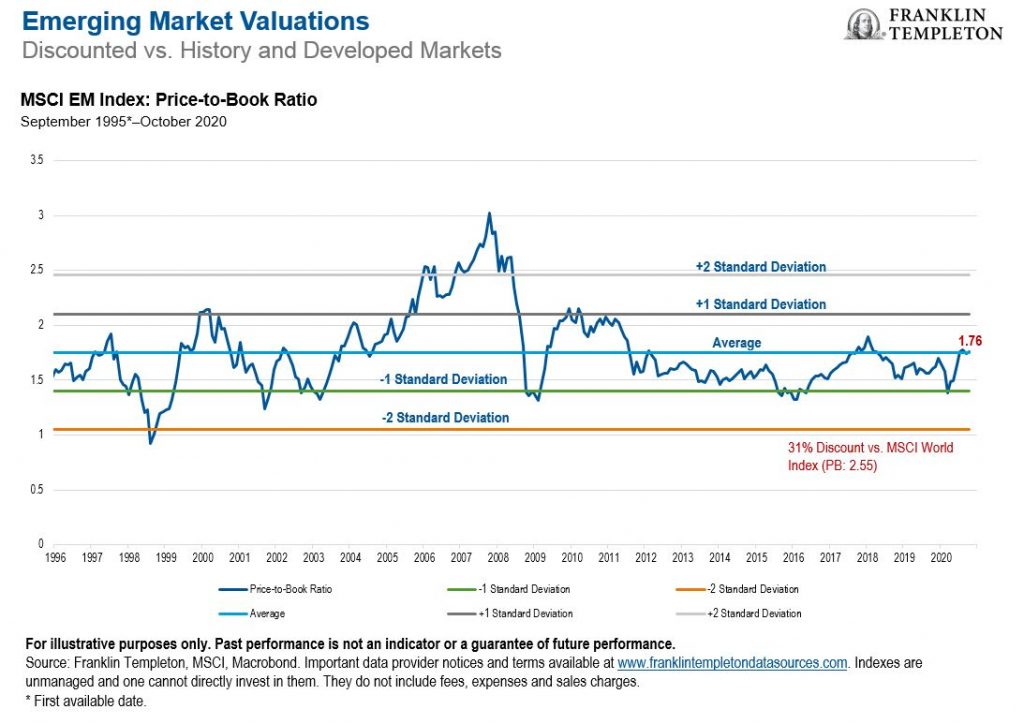

-

Emerging market (EM) small-capitalization (small-cap) stocks outperformed their large-cap counterparts over the last six months. A catchup from the sharp underperformance in the first quarter was a key driver of the stronger EM small-cap recovery. EM small caps have attracted less investor attention due to the growing market concentration of performance in a handful of mega-cap companies, as disruption from the COVID-19 pandemic drove interest in technology giants. But as we see normalcy return more rapidly in key EMs, this should enable broader economic and market recovery, as evidenced by the recent outperformance of EM small caps. We believe that the long-term structural story for EM small caps is not undone and remains compelling, underpinned by domestic economic drivers and the consumption growth story. As such, we believe that dedicated small-cap exposure should be viewed as complementary to large caps.

- Despite the COVID-19 pandemic, EMs have shown a continued appetite for structural reforms that could lay the foundation for lasting economic recoveries. China, for example, has stayed true to its longer-term goal of making domestic consumption a major economic engine—and a source of potential ballast during external demand shocks. The government’s recent moves to boost local luxury consumption tie in with this ambition as officials relaxed duty-free shopping rules, igniting a surge in duty-free sales in China. We see China’s domestic travel and duty-free industries heading for a boom in the next few years. India’s sizable fiscal deficit has limited the government’s ability to spend on shoring up its economy. We expect privatizations and other economic reforms to offer more support by attracting investments. The country’s “Make in India” initiative, aimed at growing the manufacturing sector, appears well placed to benefit from several trends. Brazil has also continued to pursue structural reforms despite economic disruptions and political noise. Officials recently passed new rules for the natural gas and sanitation industries in a bid to unlock hefty investments in the coming years.

- The recent weakening of the US dollar relative to EM currencies can be attributed to the continued challenge of containing COVID-19 in the United States, the unprecedented level of US fiscal stimulus and dovish monetary policy, and market expectations of subsequent fiscal stimulus. The weakening of the US dollar comes off the back of a prolonged period of US dollar strength relative to most currencies. We expect some reversal of this previous trend of US dollar strength, but view it unlikely for the US dollar to give up all its gains relative to EM currencies in the near to medium term given global economic uncertainty, low US inflation expectations and the continued importance of the US dollar as the global reserve currency. The weaker US dollar is generally beneficial for EM equities—and especially Asian equities— with many companies domestically oriented. As such, earnings should improve in US dollar terms. A weaker dollar also gives emerging economies more leeway for fiscal measures.

Outlook

We have seen increased differentiation within EMs amid rapid changes brought about by various economic, social, and exogenous shocks such as the pandemic. As a whole, EM equities have been resilient, though this masks wide divergences across countries and sectors. As a region, emerging Asia has outperformed. By industry, the narrow leadership of internet, technology, consumer and other “new economy” companies thriving amid COVID-19 has been apparent.

Technology- and consumer-centric companies that have dominated their fields with the help of durable competitive advantages look attractive to us. In our view, innovation and technology have been the driving forces behind EMs’ recovery amid the COVID-19 fallout. Social distancing especially has supported the growth of e-commerce, remote working, online learning and entertainment streaming. We also remain optimistic about the longer-term potential for consumption growth, whether through a rising penetration of goods and services or a “premiumization” in demand.

While developments from the US presidential election—and their potential impact on US-China relations—could spur market volatility, our focus remains on individual companies that could fare well over the longer run. We see resilience in technology leaders that have become integral to supply chains globally and are likely to weather changing geopolitical dynamics, as well as companies capitalizing on strong domestic and secular drivers of growth.

Emerging Markets Key Trends and Developments

EM equities finished a volatile month higher, while developed market stocks declined. Recovering economic momentum in emerging Asia cushioned EMs’ performance against renewed recession fears in Europe as mounting COVID-19 infections pushed several countries back into lockdowns. Rising coronavirus cases in the United States, plus uncertainty around additional fiscal stimulus and the presidential election, also drove market caution. The MSCI Emerging Markets Index increased 2.1% during the month, while the MSCI World Index declined 3.0%, both in US dollars.1

The Most Important Moves in Emerging Markets in October 2020

Asian equities defied market routs globally to deliver gains. Stocks in China rose as its economic resurgence gained pace, with industrial production and retail sales beating growth expectations in September. Taiwan’s market advanced; investors welcomed strong corporate earnings and the economy’s third-quarter rebound on the back of robust technology exports. Indonesian equities surged as the government relaxed coronavirus curbs in Jakarta and passed a job creation law aimed at reducing regulations and boosting investments. Conversely, Thailand’s market fell amid continued pro-democracy protests. In Malaysia, political tussles weighed on the country’s stocks.

In Latin America, Brazil’s stock market and its currency, the real, weakened. Concerns around the country’s fiscal health overshadowed its current account surplus and a strong rebound in its economic activity. Stocks in Peru retreated amid political uncertainty as lawmakers re-attempted to impeach the country’s president. Conversely, Mexican equities rose, with the Mexican peso’s appreciation adding a boost. The government announced an infrastructure program underpinned mostly by private investments.

Emerging European markets pulled back as a fresh wave of COVID-19 infections in Europe brought on tighter mobility restrictions. A faltering outlook for economic momentum and energy demand drove oil prices lower. Against this backdrop, Russian equities fell. Turkey’s equities and currency lost ground. The central bank’s decision to not raise its key policy rate amid heightened inflation undercut investor sentiment, as did geopolitical tensions surrounding the country. In the Middle East and Africa region, South African stocks gained, thanks to strength in the South African rand.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. Smaller and newer companies can be particularly sensitive to changing economic conditions. Their growth prospects are less certain than those of larger, more established companies, and they can be volatile.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

1. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments