Volatility swept across US markets over the last several days as fear and uncertainty surrounding the coronavirus as well as the US presidential election continue to take hold, causing the Nasdaq Composite to post its worst week since March. In Europe, many countries have once again been placed on lockdown with even tighter restrictions in place due to rising cases of COVID-19, including France and Germany. Here in the US, confirmed case numbers have also begun to rise again, sparking alarm that we may now be entering the third wave of coronavirus outbreaks. This negative news has investors on edge, especially as we start to head into the fall and winter months where social distancing will inherently become more of a challenge with no real end in sight, barring a vaccine. While this week’s action jolted tech and mega-cap stocks like the infamous FAANGs, we also saw many of the reopening-related names once again take a hit. Reopening names include those companies that rely on a fully operating, “normal” economy and are also referred to as the BEACH stocks (Bookings, Entertainment, Airlines, Cruise/Casino, and Hotels). These stocks mostly come from the broader consumer cyclicals sector, which remains a high Relative Strength (RS) area of the US equity market that currently ranks second in the Nasdaq Dorsey Wright Dynamic Asset Level Investing (DALI) tool. However, when we look below the surface of the cyclicals sector, we find that not all areas are participating in the upside, including some of the aforementioned BEACH-related stocks.

|

BEACH-related Stocks |

|||||||

|

SYMBOL |

NAME |

PRICE |

TECH ATTRIB/SCORE |

DWA SECTOR |

OVERBOUGHT/OVERSOLD |

||

|

American Airlines Group Inc. |

11.16 |

0 |

Aerospace Airline |

|

|||

|

Allegiant Travel Company |

137.57 |

3 |

Aerospace Airline |

|

|||

|

Alaska Air Group Inc |

36.78 |

1 |

Aerospace Airline |

|

|||

|

Booking Holdings Inc. |

1630.26 |

1 |

Internet |

|

|||

|

Carnival Corporation |

12.98 |

0 |

Leisure |

|

|||

|

Choice Hotels |

86.56 |

3 |

Leisure |

|

|||

|

Caesars Entertainment Inc. |

46.10 |

2 |

Gaming |

|

|||

|

Delta Air Lines Inc. |

30.76 |

1 |

Aerospace Airline |

|

|||

|

The Walt Disney Company |

121.54 |

3 |

Media |

|

|||

|

Expedia Group Inc. |

95.22 |

3 |

Leisure |

|

|||

|

Cedar Fair L.P. |

25.52 |

1 |

Leisure |

|

|||

|

Hyatt Hotels Corp. |

54.58 |

0 |

Leisure |

|

|||

|

Hilton Worldwide Holdings Inc |

86.51 |

2 |

Leisure |

|

|||

|

Southwest Airlines Co. |

39.57 |

2 |

Aerospace Airline |

|

|||

|

Las Vegas Sands Corp. |

47.84 |

1 |

Gaming |

|

|||

|

Live Nation Entertainment Inc. |

49.67 |

2 |

Leisure |

|

|||

|

Marriott International, Inc. |

93.33 |

1 |

Leisure |

|

|||

|

MGM Resorts International |

21.29 |

2 |

Gaming |

|

|||

|

Vail Resorts Inc |

233.84 |

5 |

Leisure |

|

|||

|

Norwegian Cruise Line Holdings Ltd. |

15.77 |

3 |

Leisure |

|

|||

|

Penn National Gaming Inc |

55.74 |

4 |

Gaming |

|

|||

|

PARK HOTELS & RESORTS INC |

9.96 |

4 |

Real Estate |

|

|||

|

Royal Caribbean Cruises Ltd. |

53.83 |

2 |

Leisure |

|

|||

|

Six Flags Entertainment Corporation |

20.91 |

2 |

Leisure |

|

|||

|

United Airlines Holdings Inc. |

33.57 |

1 |

Aerospace Airline |

|

|||

|

Marriott Vacations Worldwide Corporation |

96.53 |

1 |

Leisure |

|

|||

|

Wyndham Hotels & Resorts Inc |

46.83 |

4 |

Leisure |

|

|||

|

Wynn Resorts, Limited |

72.19 |

0 |

Gaming |

|

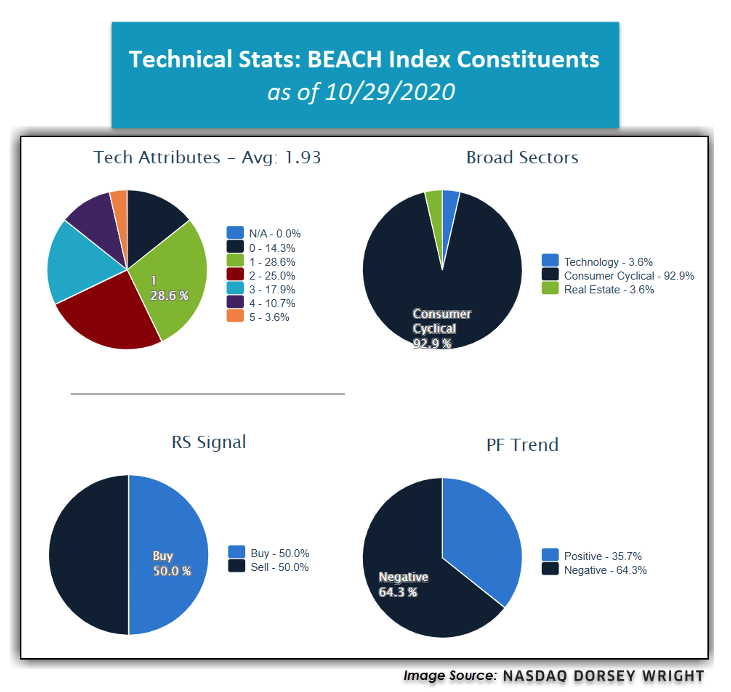

Using the stocks listed in the table above, we created a custom equal-weighted index via FactSet consisting of 28 BEACH-related names to track the group’s performance over time. Currently, from a technical perspective, this group of stocks has a weak average attribute rating of 1.93, an average year-to-date loss of over -32%, and an average overbought/oversold (OBOS) reading of -27.18% oversold.

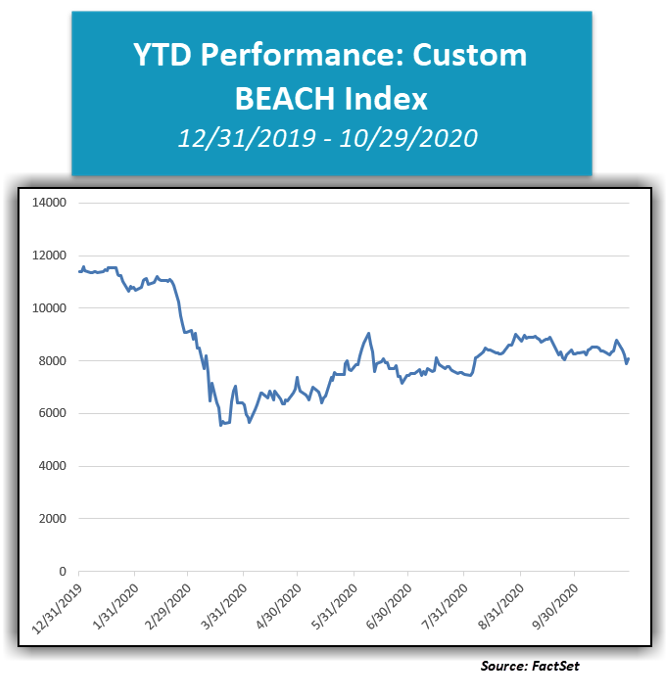

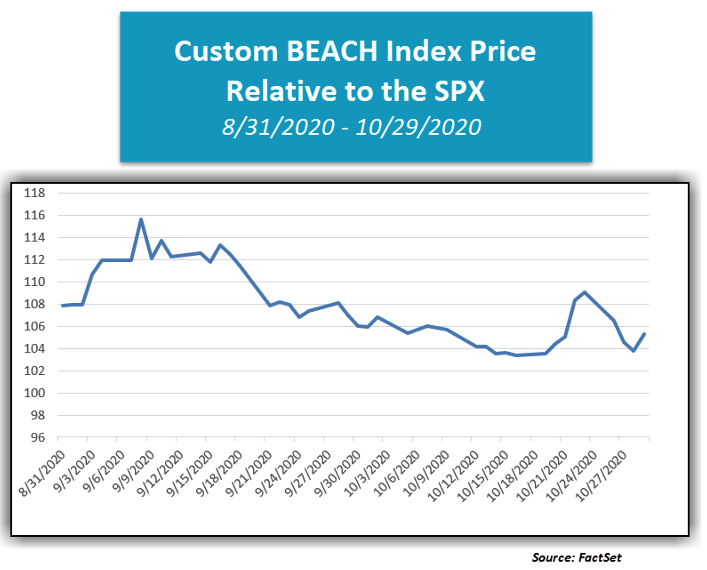

Since the market bottom on March 23, our custom BEACH index has gained 42.78% and has managed to stay in step, relatively speaking, with SPX’s return of 47.94%. However, we have started to see some divergence between the two, which is shown in the chart below comparing the price of our custom BEACH index relative to that of the S&P 500 Index since August 31. Over the last two months alone, our custom BEACH index has posted a loss of -10.34%, significantly underperforming the S&P 500 Index SPX’s loss of -5.64% over the same period due to growing coronavirus concerns and increasing lockdown restrictions. Furthermore, on a year-to-date basis, our custom BEACH index is down -28.72%, significantly underperforming SPX’s gain of 2.46%.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

The returns above are not inclusive of transaction costs. Investors cannot invest directly in an index or a model portfolio. Indexes and models have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss. The relative strength strategy is not a guarantee.

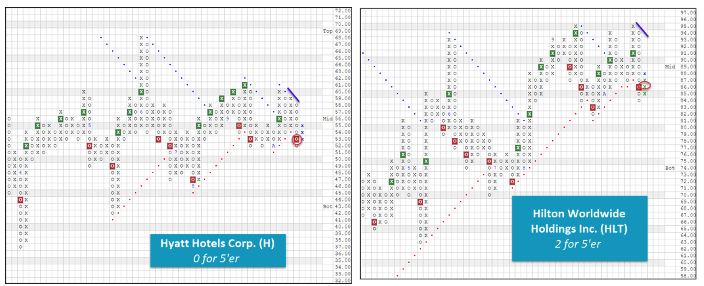

What we found was that many of these reopening names have attempted to recover after being hit hard in March, however, despite their best efforts, most have not been able to maintain any sort of momentum and have once again turned lower. Take Hyatt Hotels Corp. H and Hilton Worldwide Holdings Inc. HLT, for example. Each of these global hotel chains briefly moved back into overall positive trends in the first week of October as they saw their respective stock prices generally move higher. However, on Wednesday, October 28, both stocks fell enough to violate their respective bullish support lines and have therefore returned to negative trends. As a result, H and HLT are both weak attribute names with respective TA ratings of 0 and 2, making them names to avoid.

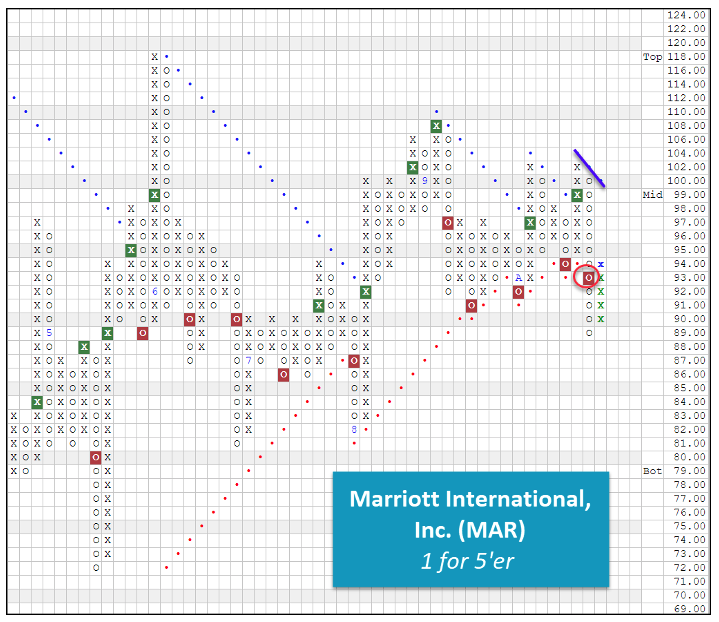

Marriott International, Inc. MAR, another major hotel chain, also started to show some signs of life when it moved into a positive trend on Thursday, October 22. Like H and HLT, MAR fell back into a negative trend this past Wednesday on negative virus news and has just 1 attribute in its favor at this time. When all was said and done, it only took six trading days for MAR to violate its newly established bullish support line, and over that brief period, the stock posted a loss of -10.76% while SPX was down -5.28%. We do note that H and HLT have earnings announcements scheduled for November 4, while MAR expects earnings on November 6.

With uncertainty and fear surrounding the coronavirus’s timeline skyrocketing and the technical strength of many BEACH-related names tumbling, we recommend steering clear of the weakening stocks within this cyclicals sub-group until they’re able to prove themselves with at least consistent upside follow through and positive trends. If looking for individual ideas within the broader consumer cyclical sector, be sure to focus on those sub-groups that have proven to be winners in the current “corona-conomy”, including, but limited to, computers and electric retail, homebuilding, internet, direct marketing retail, and footwear.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

The Dorsey Wright Sector Indexes are non-investable, equal weighted baskets of stocks including the largest and most liquid names from within each sector. The indexes are rebalanced daily and do not include the reinvestment of dividends. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Unless otherwise stated, the performance information included in this article does not include dividends or all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.