Too Much: Market Succumbed Again to Trifecta of Virus, Fiscal Relief and Election Uncertainty

Key Points

-

Last week’s decline was the worst since last March; while it’s the third meaningful pullback since the March 23 low.

-

Election uncertainty, the lack of a fiscal relief package and resurgent COVID-19 virus cases nationally were the catalysts for the latest reversal in fortune for U.S. stocks.

-

Some speculative excess has been wrung out; but we may not be out of the woods yet.

For the third time since the COVID bear ended its short havoc, U.S. stocks went into pullback mode—culminating in the worst week since March. The virus itself continues to be a culprit; with another surge in cases and hospitalizations; although not for deaths, at least not yet. The lack of a fiscal relief package and heightened election uncertainty are also to blame.

Three-peat

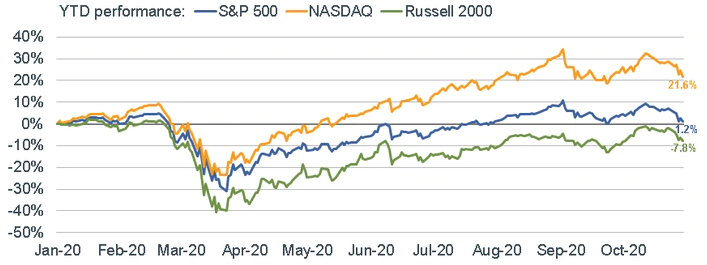

For the S&P 500, the 9% decline since October 12, is reminiscent of June’s quick 7% decline and September’s near-10% decline. As you can see in the chart below, among the major averages, on a year-to-date basis, the technology-heavy NASDAQ is leading the pack, up nearly 22%; with the S&P 500 barely positive, and the small cap Russell 2000 remaining in the red, down nearly 8%. According to Evercore ISI data, last week’s factor performance leaned toward risk-off; with earnings quality and accelerating sales performing well, and earnings risk and price volatility noticeably weak.

NASDAQ Remains on Top

Source: Charles Schwab, Bloomberg, as of 10/30/2020. Past performance is no guarantee of future results.

Big 5 not immune

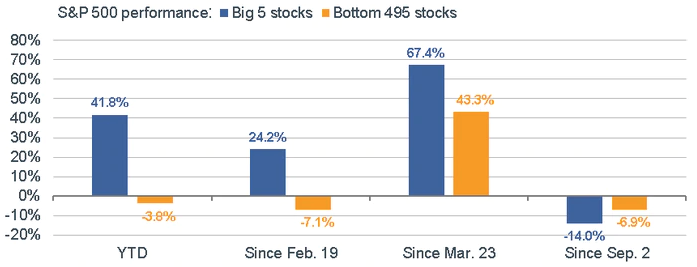

Much ink has been spilled—including by yours truly—on the performance dominance of the “Big 5” stocks within the S&P 500: Apple, Microsoft, Amazon, Google and Facebook. They are often lumped together as “tech” stocks; but the reality is, they span three S&P 500 sectors: Apple and Microsoft are in the Technology sector; Amazon is in the Consumer Discretionary sector; and Google and Facebook are in the Communication Services sector. I’ve been calling them “techie” stocks. On a year-to-date basis, the Big 5 stocks’ average return has crushed the average return of the remaining 495 stocks within the S&P 500 index, as you can see in the left pair of bars in the chart below. The chart also shows performance since the pre-pandemic high on February 19, since the bear market low on March 23, and since the most recent all-time high on September 2.

Big 5 vs. Bottom 495

Source: Charles Schwab, Bloomberg, as of 10/30/2020. Performance is based on market cap-weighted average of the 5 largest and 495 smallest S&P 500 stocks. Past performance is no guarantee of future results.

As shown above, the performance story of the Big 5 stocks vs. the other 495 stocks started a possible new chapter when the S&P 500 hit its all-time high on September 2. Since that point, the Big 5 stocks have underperformed the other 495 stocks by more than seven percentage points. It has become a rotational market; however, the narrative around which stocks are being sold in favor of which stocks are being bought has not been consistent. For the past two months, we have seen “fickle rotations” from “techie” stocks to non-techie areas; from defensive sectors to cyclical sectors; from growth to value; and from large cap to small cap.

Fickle rotations

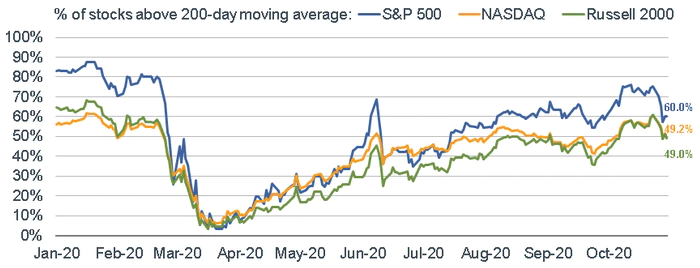

Throughout this most recent period of fickle rotations, we have seen a noticeable deterioration in breadth; with a declining percentage of stocks trading above their 200-day moving averages, as seen below. For both the NASDAQ and Russell 2000, less than half their component stocks continue to trade above their 200-day moving averages. The S&P 500 is faring better, at 60%; but that’s well down more than 75% earlier in October.

Weaker Breadth

Source: Charles Schwab, Bloomberg, as of 10/30/2020. Past performance is no guarantee of future results.

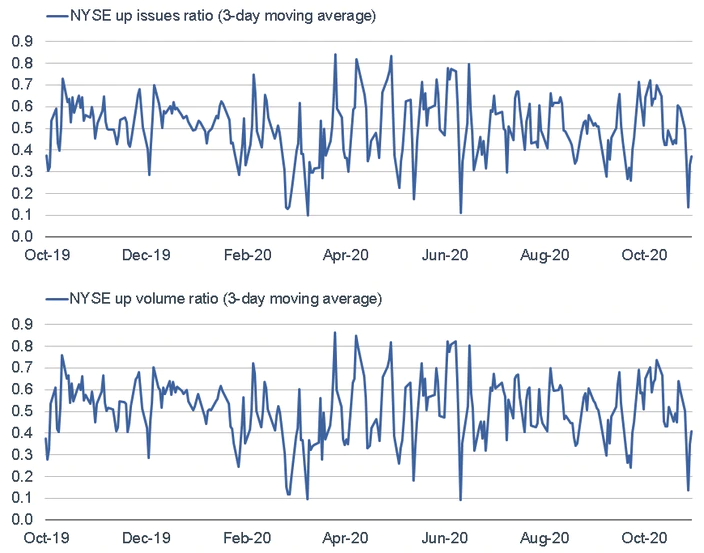

Last Monday and Wednesday, selling pressure was overwhelming enough that most securities fell—and most of the volume on the New York Stock Exchange (NYSE) was focused on those issues. According to SentimenTrader (ST), at the recent low, the three-day average of NYSE up issues and up volume both dropped to below 20%. That shows wholesale, get-me-out selling pressure. Often, there are a lot of down issues, but not a lot of volume. Sometimes there is a lot of volume flowing into relatively few declining stocks. However, early last week, it was both.

Get-Me-Out Selling Pressure Last Week

Source: Charles Schwab, Bloomberg, as of 10/30/2020. For Illustrative purposes only.

Thursday was a better day last week; and even Friday brought some recovery from the lows intraday. It was enough to push those averages back above 20%; showing a potential recovery, though longer-term measures haven’t fully reached oversold territory. Similar periods historically showed a tendency for the S&P 500 to continue to have weak patches shorter-term, but more consistent rallies over the medium-term.

Volatility spike easing

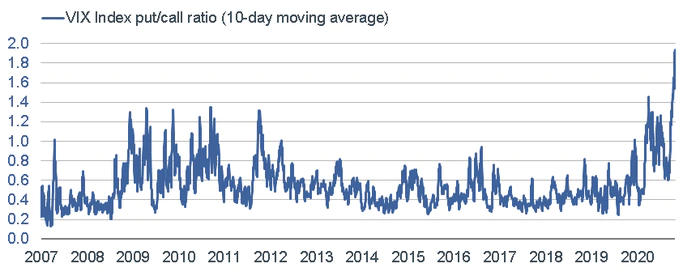

Volatility spiked last week as well; and an increasing number of traders are betting that it’s likely to reverse. As you can see below, the 10-day average of the VIX Put/Call Ratio recently spiked to its highest level in more than 13 years, according to ST data. That means that on an average day, 50% more puts are being traded than calls. It’s not known whether the underlying trades are betting on increasing or decreasing volatility; the assumption is that heavy put volume reflects bets that the VIX will decline (and historically, that’s what typically occurred). We can only hope that once the election this week is over (and decided) that volatility might ebb.

Betting on Volatility Decline

Source: Charles Schwab, Bloomberg, as of 10/30/2020.

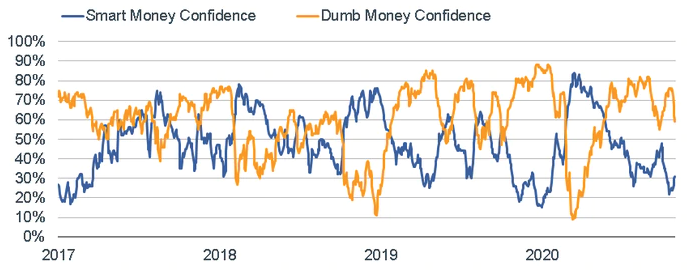

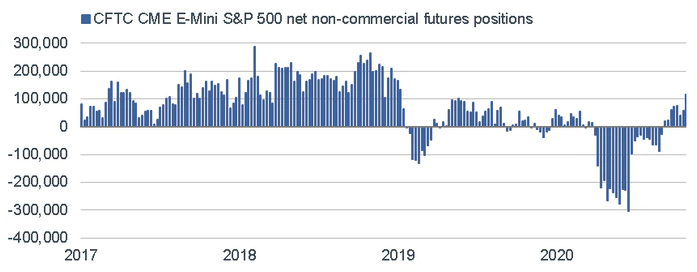

Finally, the weakness last week did aid some convergence in ST’s “Smart Money” and “Dumb Money” Confidence measures, as you can see in the first chart below. As a reminder, these are real money gauges of what the typically-non-contrarian (at extremes) “smart money” large investors/speculators are doing, and what the typically-contrarian (at extremes) “dumb money” small traders/speculators are doing. They remain far from the extreme divergence the February 19 to March 23 bear market brought about; but some convergence is welcome from a contrarian sentiment perspective. In fact, as you can see in the second chart below, larger speculators’ bullish wagers in S&P 500 futures for last week were the greatest since January 2019.

Convergence in Confidence

Source: Charles Schwab, SentimenTrader, as of 10/30/2020. SentimenTraders’ Smart Money Confidence and Dumb Money Confidence Indexes are used to see what the “good” market timers are doing with their money compared to what the “bad” market timers are doing and are presented on a scale of 0% to 100%. When the Smart Money Confidence Index is at 100%, it means that those most correct on market direction are 100% confident of a rising market. When it is at 0%, it means good market timers are 0% confident in a rally. The Dumb Money Confidence Index works in the opposite manner.

Speculators Getting More Optimistic

Source: Charles Schwab, Bloomberg, as of 10/27/2020. The Commitments of Traders (COT) reports provide a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the Commodity Futures Trading Commission (CFTC).

Catalysts vs. causes

The aforementioned forces putting downward pressure on stocks—including election uncertainty, the lack of a fiscal relief package, and of course the rising trajectory of virus cases—have probably been catalysts more than causes. Perhaps that’s an exercise in semantics; but sentiment had gotten stretched, with rampant signs of speculative froth. Speculative fervor can persist alongside a rising market for an extended period. Remember what John Maynard Keynes once said: “markets can remain irrational longer than you can remain solvent.” However, they can’t (and historically don’t) stay irrational forever; and we can “thank” the resurgence in virus cases for aiding in the reversal in some concerning indicators of rampant speculation.

Discipline, diversification and periodic rebalancing remain key in these uncertain times.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Options carry a high level of risk and are not suitable for all investors. Certain requirements must be met to trade options through Schwab.

Investing involves risks, including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

(1120-0S8P)