When many fixed income investors think about the November US election, they tend to focus on how the presidential and congressional race outcomes could affect national policies. However, our municipal bond team delves into state and local government elections, too. Here, they share their analysis of how election outcomes at all three levels of government could affect muni bonds.

We always follow election outcomes as part of our research activities. In most years, we are focused primarily on state and local elections. But in years with presidential elections, we take a deeper dive into how the national election could impact state and local governments.

When looking at elections at all levels, spending time trying to predict election outcomes isn’t our focus. Rather, we look to understand sentiment changes, sense political priorities and prepare for the outcomes so we can take advantage of any potential opportunities that arise in the market.

One global issue that will face leaders at all three levels of government will be the ongoing challenge of the COVID-19 pandemic. We think the pandemic will preempt leaders’ ability to tackle many issues they would otherwise address. Maintaining public health, opening the economy, and ultimately managing a vaccine distribution will come ahead of other policy priorities.

State and Local Elections

State and local elections are important because some types of bonds require voter approval. Many state and local governments put tax measures on the ballot and, of course, elected officials govern state and local governments, approving budgets and providing government services. Therefore, we learn a lot from state and local elections. First, we look at voter-approved bond measures and whether they succeed or fail. We factor this information into our analysis of a government’s leverage.

Part of our analysis focuses on how an issuer can raise taxes. If tax changes require voter approval, which varies by state, we can learn a lot about the electorate by watching elections, which can be important to understanding future credit challenges or opportunities.

That said, it isn’t just the quantitative election outcomes that are important. We closely follow trends to understand what a community’s appetite is for tax increases (either through the issuance of more debt or actual tax-rate increases), which can be just as important.

As an example, in the year leading up to the COVID-19 pandemic, we started to see more and more California cities put sales tax or parcel tax measures on their ballots to deal, in large part, with spending constraints from growing pension requirements. Over this period, we saw several very high-profile measures defeated, a trend which we viewed as an important consideration: if these tax measures were being declined 10 years into one of the country’s strong economic expansions on record, what would it mean when the next economic cycle happens and cities need more money? That situation is here now, with nearly all states and locals seeing reduced tax revenues from COVID-19-related shutdowns.

Tax measures can have other impacts on municipal bonds. While not related to a municipality’s credit, higher taxes increase the value of tax-exempt municipal bonds. So, while tax increases can potentially improve credit (not all tax increases do, however), they can also improve the demand for these products.

Political risk is also an important component of our analysis, as the political party makeup of the executive and legislative branches can have a large impact on municipal bonds. As an example, political risk can rise when different parties dominate the executive and legislative branches. When coupled with a recession, we tend to see more infighting over revenue assumptions and spending priorities and more frequent budget delays. The economic and financial impacts from the COVID-19 pandemic are creating that type of situation. In crafting fiscal year 2021 (FY21) budgets, the ability of many states to come to agreements was encouraging to us. However, we are concerned that FY22 could increase political risk if economic growth is still weak, as most of the “low hanging fruit” was used to help balance the FY21 budgets.

National Elections

Any presidential election year introduces a number of new questions. This year is no different, and perhaps even more so given the division and backdrop of COVID-19. One hotly debated topic leading up to the election is additional funding tied to the pandemic. For munis, this largely focuses on additional support (stimulus) for municipal issuers, specifically revenue replacement aid for state and local governments, and for transportation.

We think it is unlikely we’ll see any additional aid ahead of the election, but post-election we think the potential rises, particularly if Democratic nominee Joe Biden wins in the US presidential race. The size of additional aid is most likely contingent on party control. However, both parties have provisions for aid to airlines, while mass transit would receive aid under congressional Democratic control.

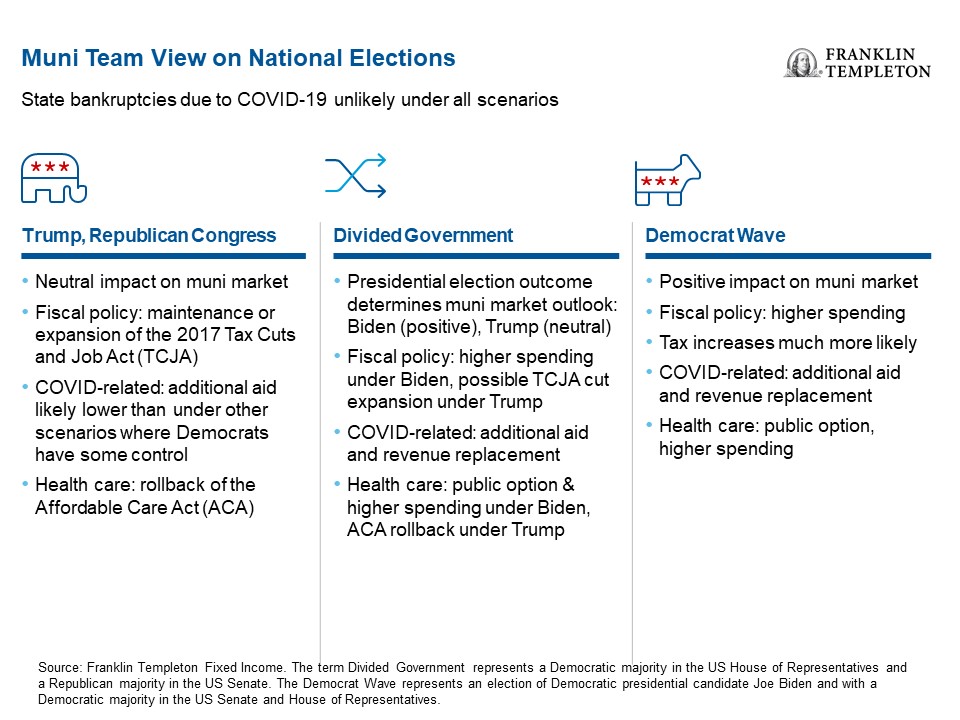

The graphic below identifies the consequences we see stemming from various potential election outcomes. In general, we view all of these scenarios as neutral to positive for munis. However, under scenarios where there is less federal aid, we believe state and local governments will likely increase taxes.

If Biden wins, we anticipate higher spending, tax increases, state and local COVID-19-related aid and a public option for the uninsured. If Biden wins, but the House and Senate remain divided, we anticipate some increased spending, but not as much as under a situation where the Democrats control both chambers of Congress.

If Trump wins and Republicans gain control of both branches of Congress, we expect a continuation of many recent policy themes, but to an even greater extent. For example, not only would the tax cuts passed in 2017 likely remain in place, but we would also see increased potential for additional cuts. We think there could be some additional COVID-19-related aid, but it probably comes at lower levels and with liability protection. If Trump is re-elected and Congress remains divided, we don’t expect much change from current policy.

Bottom Line

Regardless of the November election outcome, we are prepared to take advantage of any changes to the muni bond market where we see potential investment opportunities. Over time, our team has navigated many different election cycles across various economic and interest-rate environments, and we’ve learned elections are unpredictable and the muni market is dynamic. However, we believe analyzing various post-election scenarios at the local, state and national levels can help us better prepare for the challenges and opportunities ahead.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as of publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own investment professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com—Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton’s U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton Investments