Investors Need Some Accurate Evidence!

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe have a light economic calendar with important data on home sales, jobless claims, and durable goods orders. None of these is likely to stimulate higher heartbeats.

I expect politics and the election to get plenty of attention in the financial media, especially with an open Supreme Court seat as a new issue.

These are important long-term issues, but the answers (which no one knows anyway) shed little light on key questions we all face right now.

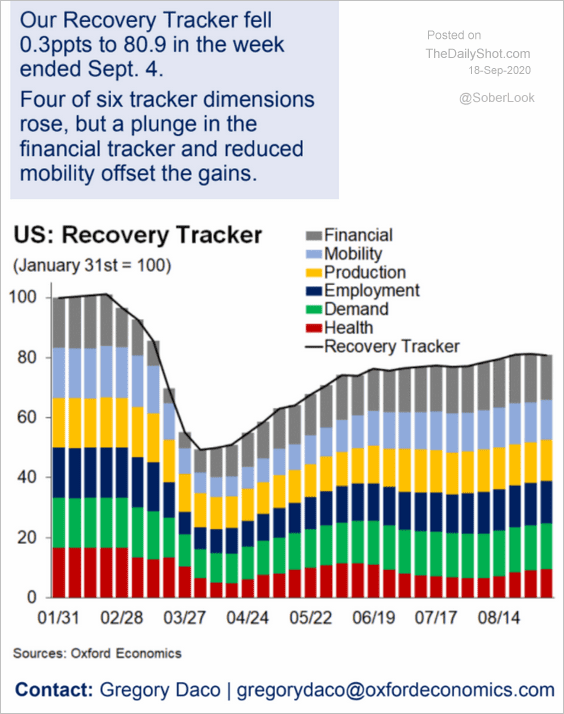

Investors need an evidenced-based assessment of the economic rebound.

And then they need to ask if their portfolios are aligned with the answer.

Last Week Recap

In my last installment of WTWA, I took note of market declines and considered whether this might be the “start of something big.” We still do not know, but it is worth paying attention to the most important indicators.

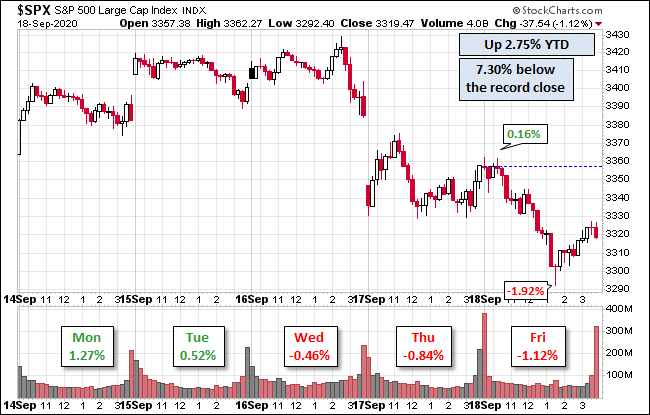

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version of the prior week. The callouts also show the range of Friday trading.

The solid start to the week deteriorated beginning Wednesday afternoon. This coincided with Fed Chairman Powell’s press conference, viewed by many as the cause.

The market declined 0.7% on the week. Despite the choppy look of the chart, the trading range was only 3.0%. I provide regular updates of historical and expected volatility in the Indicator Snapshot (below).

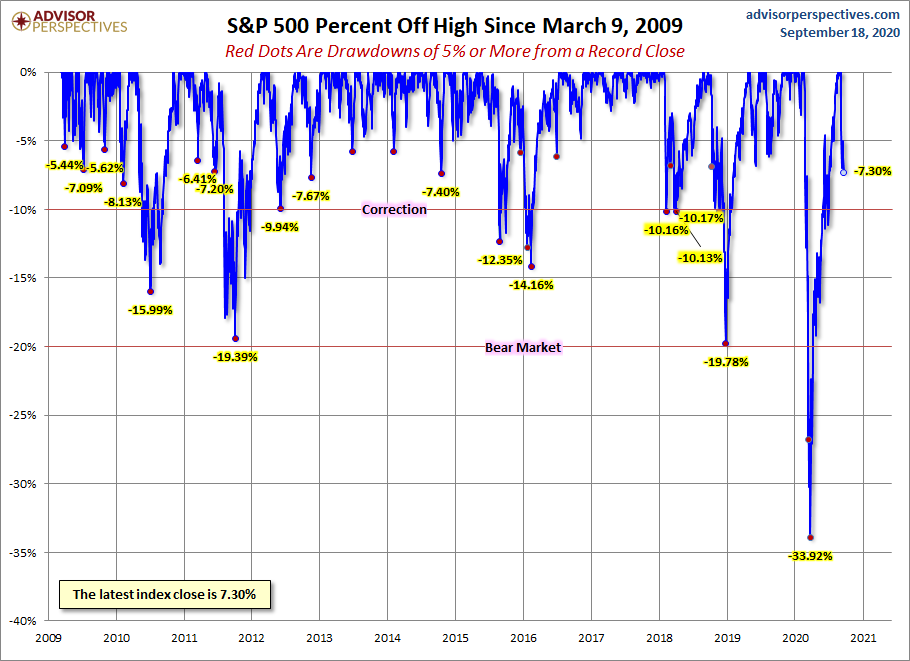

A second chart from Jill helps to maintain our perspective on the current drawdown.

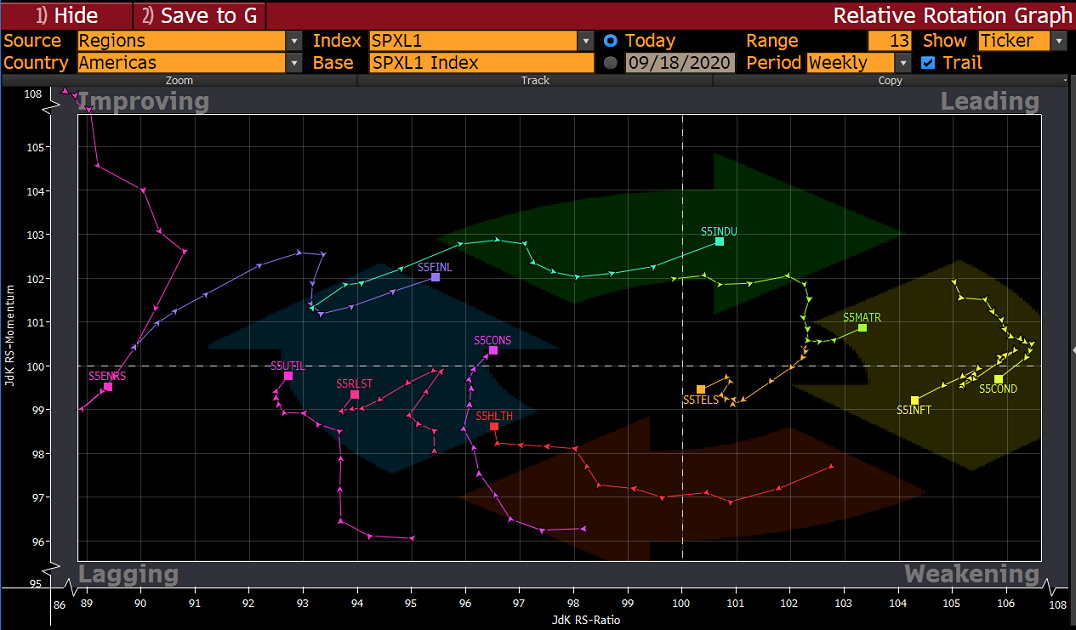

The weekly sector chart shows the sources of the action.

I have promised some commentary on this chart from Juan Luque, the member of our trading team who works most closely with these trends. Here is his update:

The Relative Rotation Graph serves as a visual representation of the rotation of instruments around a benchmark. For our regular post we chose the S&P 500 index as the benchmark to see how its sectors outperform or underperform it and to see the direction of the trends in each sector. In today’s graph we can see the industrials strength as it moves into the leading quadrant and the financial sector towards it. It also seen how the construction, info tech, and communication services have continued to weaken and investors might worry in those sectors. It is quite interesting to see energy sector dropping from the improving quadrant to the lagging one instead of moving towards the leading one as all sectors tend to move in a clockwise manner.

(The sector names are here. The Bloomberg symbols add “S5” at the start of the name).

Noteworthy

For the last two weeks I have been worrying about my West Coast friends. They have avoided the worst results of lost homes and costly evacuations, but many have suffered from deadly reductions in air quality. I studied the AQI and found this excellent description form the Visual Capitalist. Read this guide and you will be able to interpret the air quality maps the way I have been.

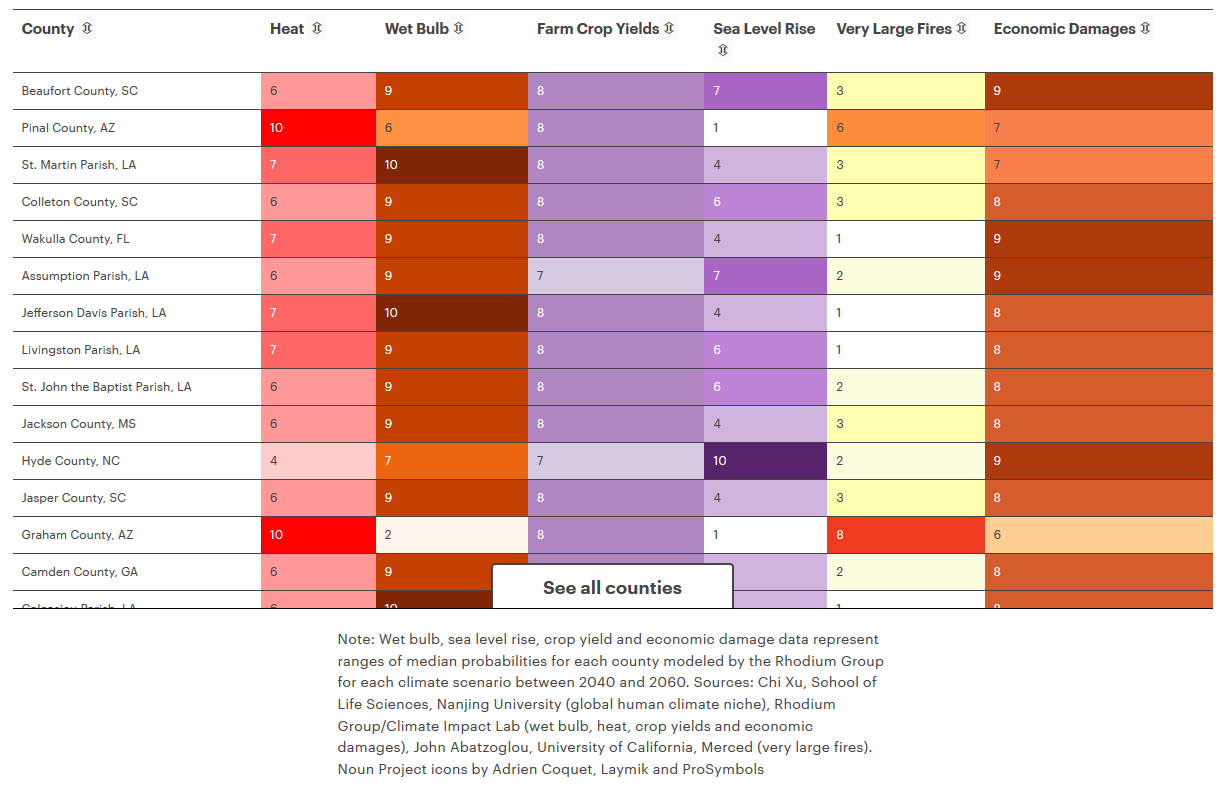

So many candidates for my Noteworthy section cannot be demonstrated properly in WTWA. The interactive version of this post draws upon several solid sources to look a few decades into the future and look at the impact on various regions. The example in this chart can be sorted by each field. If you choose “Heat” for example, you will see that my new home rates a “10.”

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

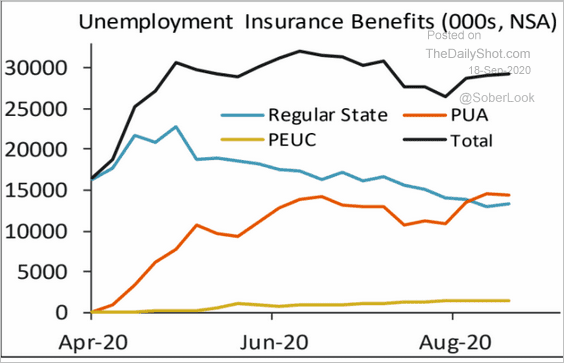

New Deal Democrat’s high frequency indicators are more important than ever. As we look for turning points and the sustainability of the rebound, these are the earliest clues. His latest update shows all three of his time frames remain in positive territory. He expects consumer spending to weaken with the loss of Congressional emergency aid. They key element of change? More action against the coronavirus could lead to a firm expansion next summer.

The Good

- Homebuilder sentiment for September was 83, well above the 78 reading for August, which was also the value expected by economists. Calculated Risk writes about the record high in this diffusion index.

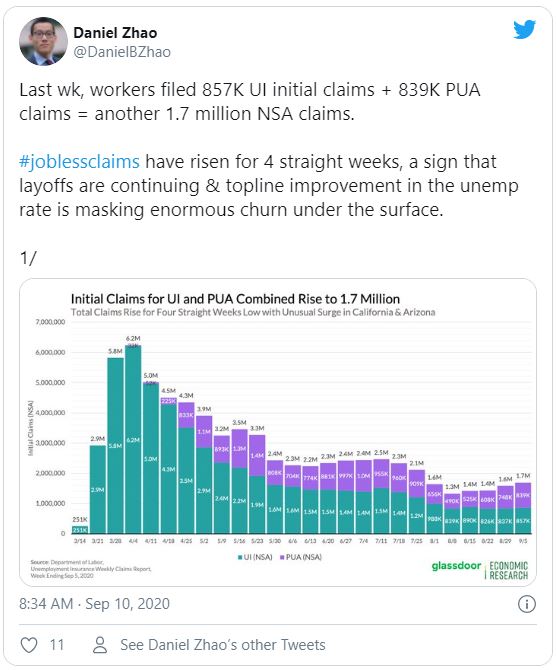

- Initial jobless claims decreased to 860K from the prior week’s upward revised 893K, but missing expectations of 830K.

- Continuing claims declined to 12.628M from the prior week’s downwardly revised 13.544M

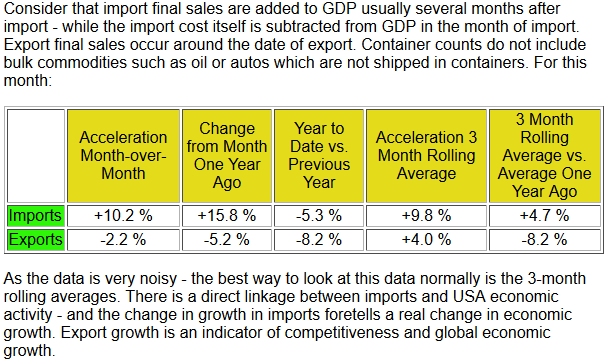

- Sea container imports are at record levels. Steven Hansen (GEI) considers the data from various angles and provides this highlight:

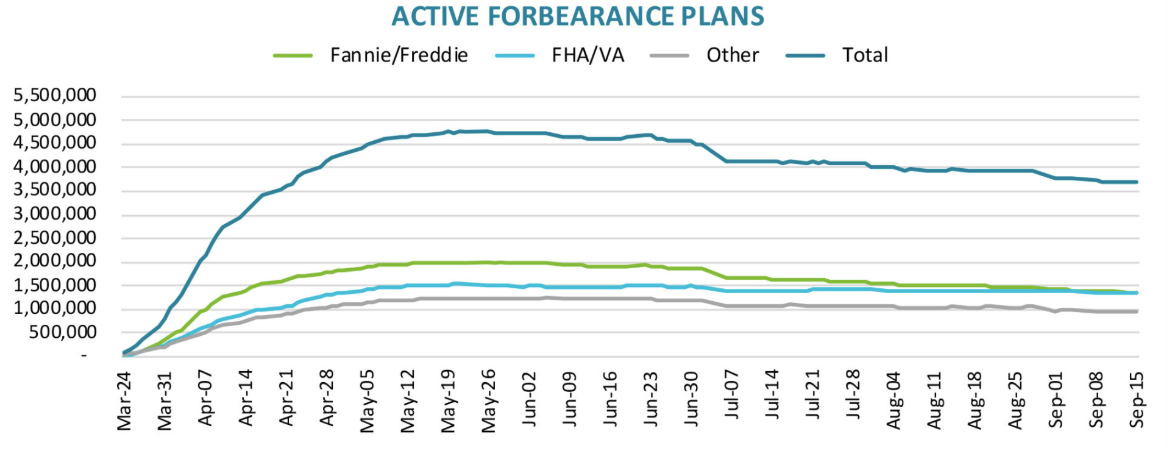

- Homeowners in Forbearance Plans due to COVID-19 declined, as of mid-September. Calculated Risk shows the significant improvement since the peak in May.

- University of Michigan sentiment (Sep. preliminary) was 78.9, beating expectations of 77.0 and much better than August’s 74.1. Jill Mislinski has the best chart on this series.

The Bad

- Industrial production for August increased only 0.4%, missing expectations of 1.0% and weaker than July’s (downwardly revised) 0.9%.

- Mortgage applications declined 2.5% versus the prior week’s gain of 2.9%.

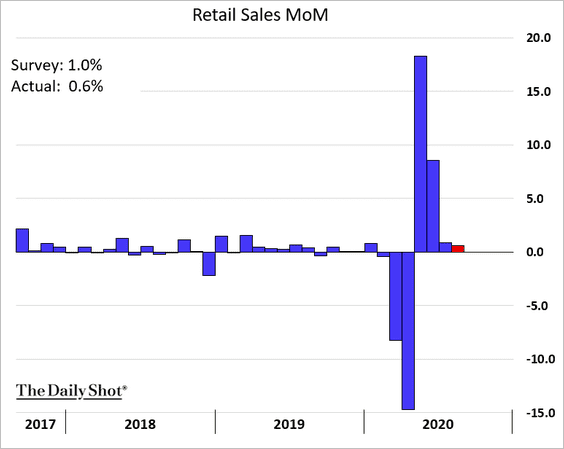

- Retail sales for August increased 0.6%, below the expectations of 1.0% and July’s downwardly revised 0.9%.

The control group removes the most volatile sales components.

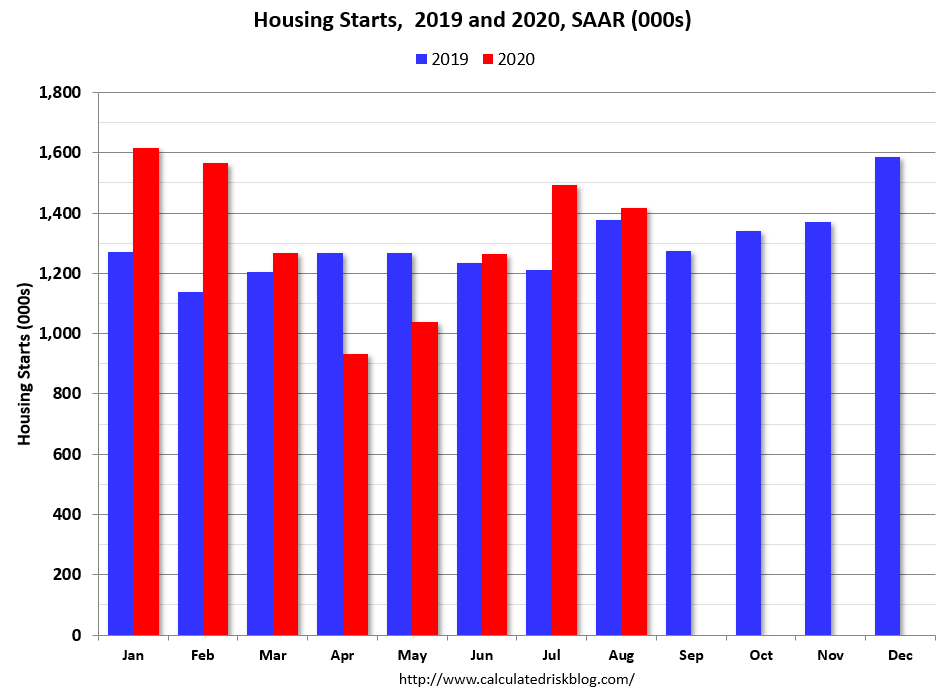

- Housing starts for August registered a SAAR of 1416K, missing expectations of 1489K and lower than July’s 1492K. Calculated Risk observes that YTD starts are up 5.2% compared to 2019. He expects stable but slowing growth. The monthly comparison for 2019 and 2020 is interesting.

- Building permits for August recorded a SAAR of 1470K, slightly lower than July’s downwardly revised 1483K and expectations of 1520K.

- Leading indicators for August increased 1.2%, missing expectations of 1.4% and lower than July’s 2.0%, revised up from 1.4%.

The Ugly

The election homestretch. I have spent some time recently discussing election ideas with friends from both parties. Taking a passive role, I tried to draw out their reasoning and view of the facts. All of these friends are very intelligent and well-read. I had a general sense of what to expect but was still surprised.

Each sounded like a partisan spokesperson! There was not even agreement about basic facts, with raw disbelief for any contrary interpretation. I’ll spare you the details.

Political scientists (of which I am a card-carrying member, although the card is a little dusty) have long known that the most informed voters decide early. There are very few “thoughtful independents” who weigh evidence until they actually vote. That is especially true this year. The election will be decided by the least informed voters, the group that is most readily influenced by the ugly attack adds that everyone pretends to deplore. [Mrs. OldProf mutes them on a non-partisan basis. As new residents of a battleground state, we are big targets].

The Conversable Economist has a nice post, Misperceptions and Misinformation in Elections Campaigns. There is a good summary of factual misperceptions from a scholarly article by Brendan Nyhan. The disciplined method is interesting.

To be clear, Nyhan describes misperceptions as “belief in claims that can be shown to be false (for example, that Osama bin Laden is still alive) or unsupported by convincing and systematic evidence (for example, that vaccines cause autism).” Thus, he isn’t talking about issues of shading or emphasis. Nyhan writes: “Misperceptions present a serious problem, but claims that we live in a `post-truth’ society with widespread consumption of `fake news’ are not empirically supported and should not be used to support interventions that threaten democratic values.”

Here is another good example to encourage you to read the entire post:

An underlying pattern that comes up in this research is that if people are exposed to an concept many times (an example is the false statement “The Atlantic Ocean is the largest ocean on Earth”), they become more likely to rate it as true. The underlying psychology here seems to be that when a claim seems familiar to people, because of repeated prior exposure, they become more likely to view it as true. An implication here is that while those who marinate themselves in social media discussions of news may be more likely to think of themselves as well-informed, they are also probably more likely to have severe misperceptions. Indeed, people who are more knowledgeable are also the same people who have become aware of how to deploy counterarguments so that they believe their misperceptions even more strongly.

This long-term trend has been exacerbated by technology and social media. I have featured “fake pictures” in this section on several occasions, so this latest example should be no surprise. It happens to be an attack on Biden, but there are others with a big variety of targets. Feel free to post other examples.

The other big election factor is turnout. Both parties have solid organizations to identify supporters in advance and encourage them to vote.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

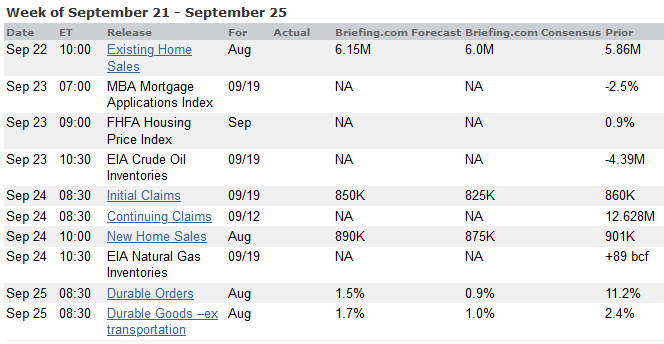

We have a modest economic calendar featuring home sales and prices, jobless claims, and durable goods orders. Only the claims data provides a true progress report.

Like it or not, expect a bombardment of political commentary and ads. This does not seem to have much market effect, and it probably should not.

There are also regular updates about vaccine progress, with knee jerk reactions to each.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

In normal times the week’s story would be mostly about housing and employment. Instead, prepare for a high-volume blast of political commentary. This may be interesting and important, but the relevance to our near-term investment decisions is small. Investors should be asking:

What is the state of the economic rebound? And please – provide evidence.

Background

A big problem is the second part of the question. We have entered what I call a Quagmire of Sophistry where most sources begin with the conclusion and adduce cherry-picked evidence. At this critical investment juncture, much more is required. My mission this week is to review the key issues and the current state of the evidence.

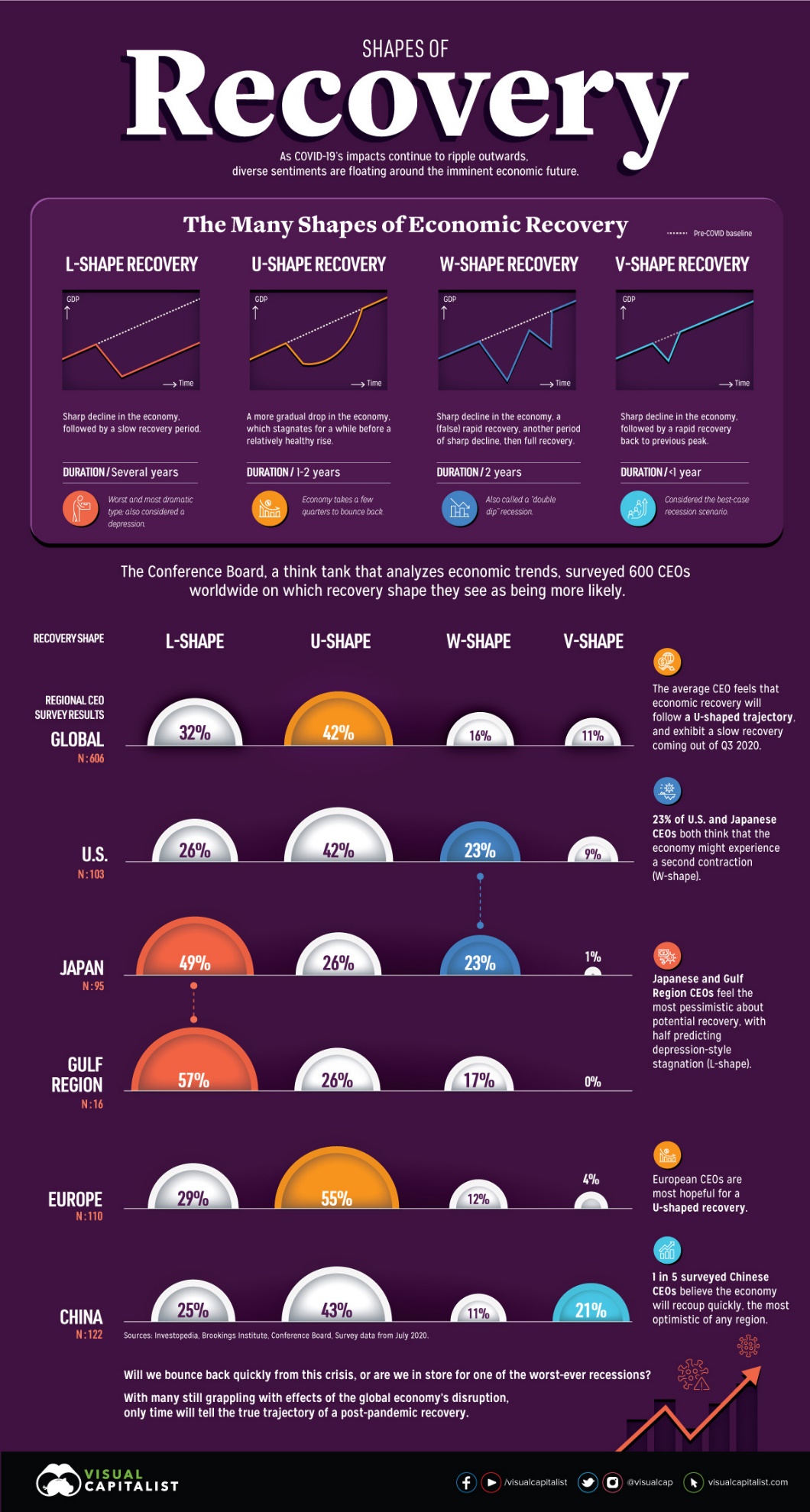

The Visual Capitalist provides information on how global CEOs see the shape of the recovery. The key takeaway is that about half see some type of near-term recovery. Will their current feeling prove accurate?

Our wise sources see various conclusions.

Paul Schatz (a normally bullish observer) opines, Market Bottom Still Ahead.

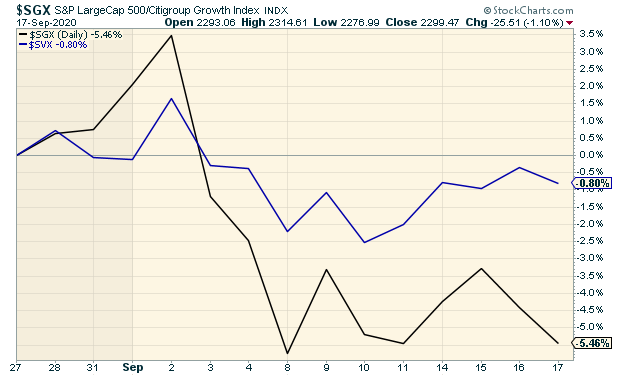

Eddy Elfenbein is encouraged by the shift from growth stocks to value stocks.

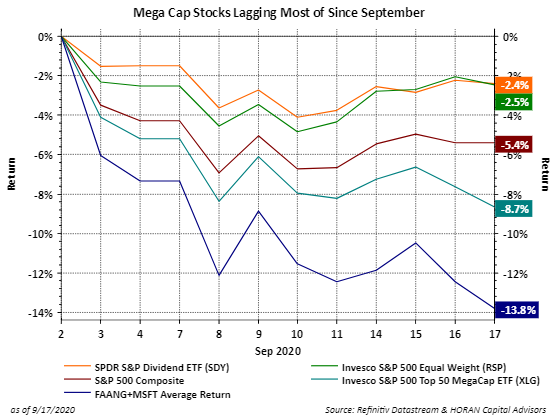

David Templeton (HORAN) also takes note of the mega cap stocks, without comment on the implications for the broader market.

Shift to Value (At Last)

James Picerno takes a longer view and reaches a different conclusion.

[JEFF] I LOOK FORWARD TO THE ROTATION TO VALUE, BUT I DO NOT EXPECT TO SEE IT SOON. THIS WILL BE A BIG THEME AFTER THE GREAT RESET.]

Snowflake

Also relevant to the market sentiment is the reaction to the Snowflake (SNOW) IPO. Tech expert Beth Kindig drilled down on the data, business model, and competitors. She looks at the company’s September 8th filing and the potential pricing of $75 – $85 per share. She looks at this 30 forward price-to-sales ratio and concludes that it would be the first high growth company with positive earnings to sustain this valuation, even briefly.

So what happened? From Barron’s – The offering range moved higher and was eventually priced at $120. But the average investor could not get that price. The first trade price was $245! It traded up to a high of $319. The implied market cap is greater than 87% of the stocks in the S&P 500. That is 150 times current year estimated sales. Forget about earnings.

[Jeff] Some would see this as a sign of a frothy market.

Employment

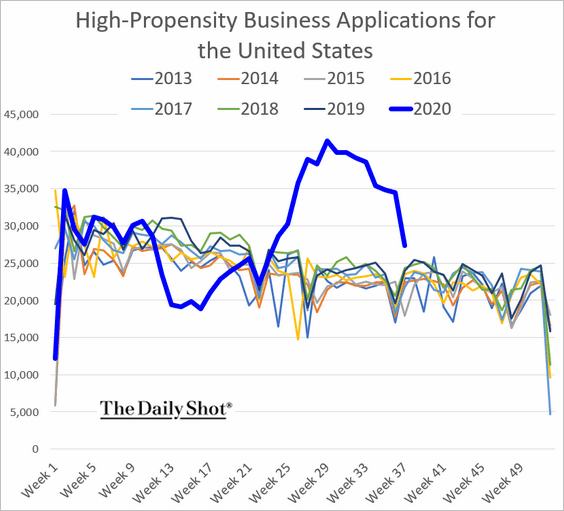

The numbers do not add up. The BLS nonfarm payroll method assumes business openings to match the number of closed, non-reporting businesses. Since no one seems to realize this (despite my data-based efforts) the overall perception of the economy has an optimistic bias. That has influenced Congress and the Fed, which may make matters worse.

The business application data is pretty soft with a lot of uncertainty in the term “high propensity.” Mostly it requires a statement that the business is hiring and includes a planned date for starting to pay wages.

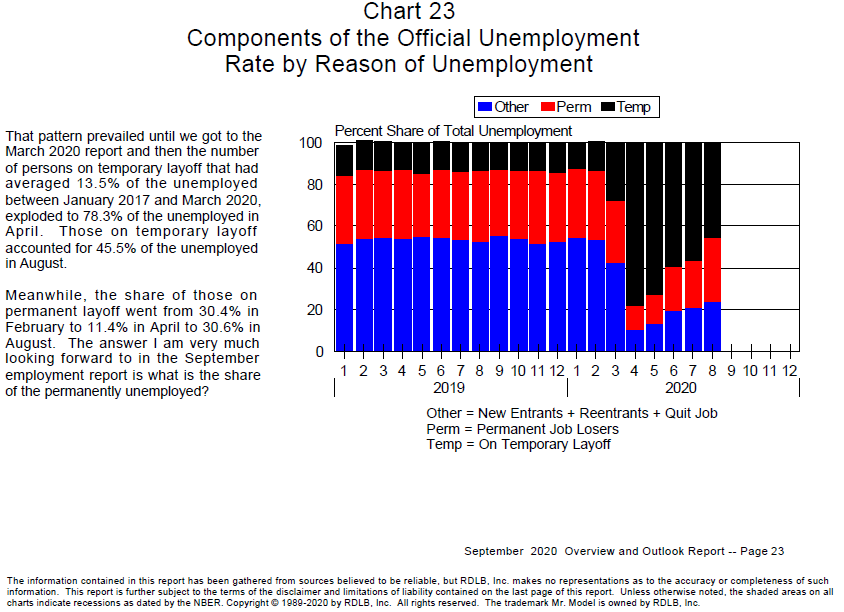

As usual, Bob Dieli has a first-rate analysis of the unemployment data. His full report provides much more chart-supported analysis, including the stability of this data series before the pandemic.

[Jeff] We know that there were classification errors in this series related to permanent unemployment versus temporary layoffs. I agree with Bob’s focus on the number in the permanent category.

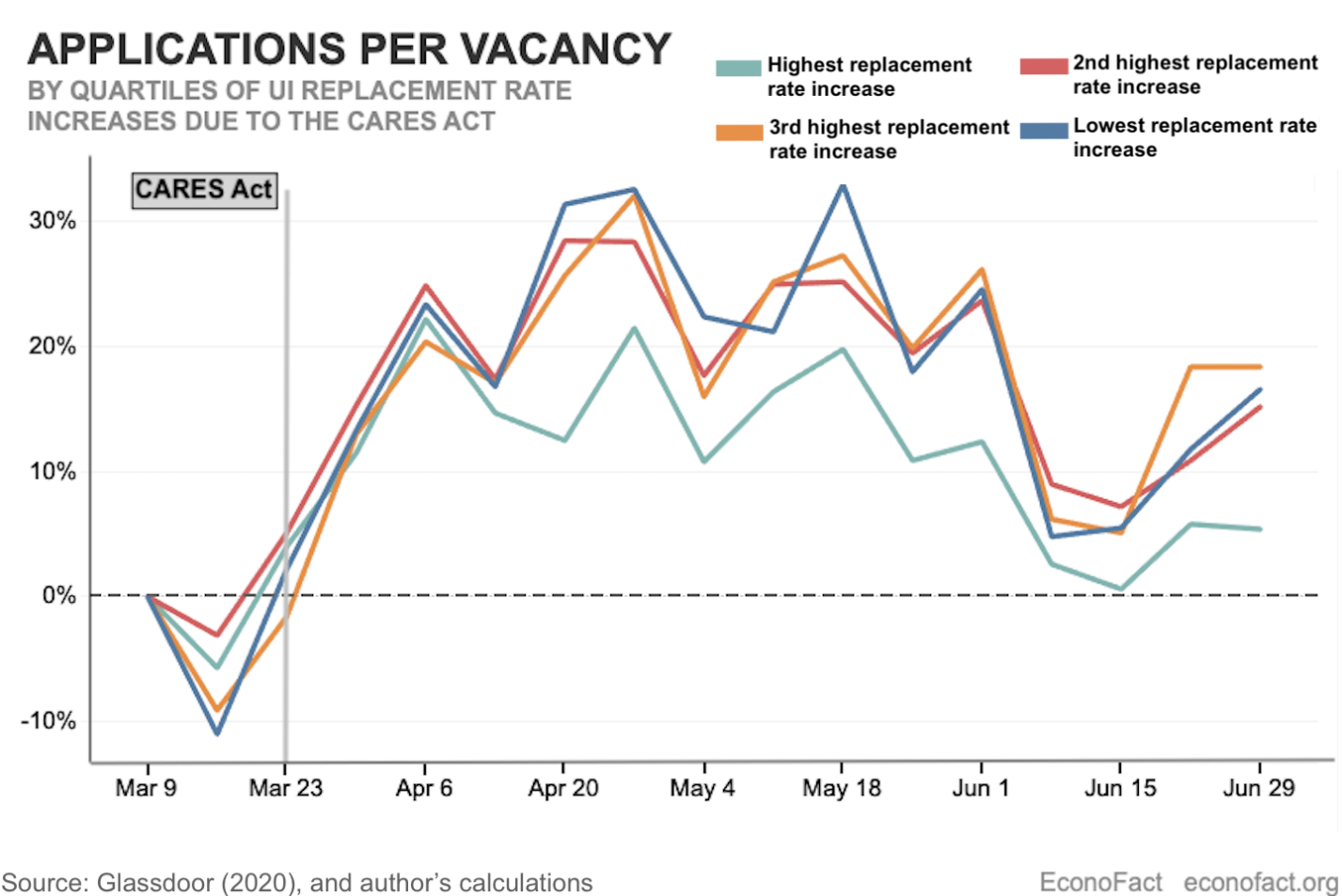

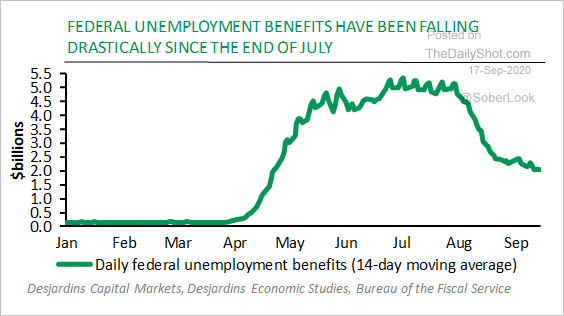

Another key question is: Have Enhanced Unemployment Benefits Discouraged Work?

This carefully evidenced paper concluded as follows:

The results of our study, as well as other emerging work, suggest there was not a significant effect of the expansion in unemployment benefits created by the CARES Act on overall employment. The vast majority of employment loss was due to a decrease in job opportunities rather than a decrease in the willingness to work. This does not mean that incentives are erased. When people report anecdotes about some workers not wanting to go back to work, it does reflect their reality. But at the same time, there are so many people who DO want to go back to work despite the benefits, and there are so few jobs, that the disincentive effects of very generous unemployment benefits turn out not to be a problem for the aggregate employment level. When there are too many applicants per job, one person not applying makes no material difference to the job being filled.

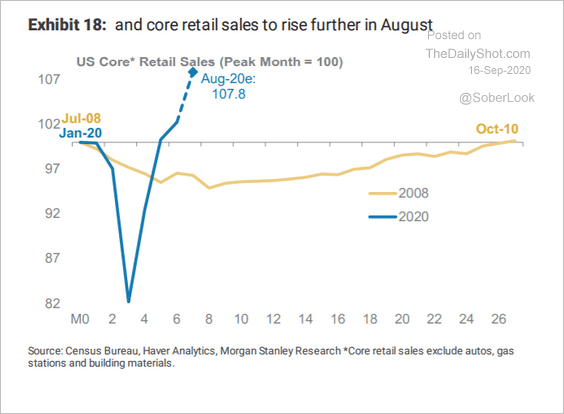

Street Expectations

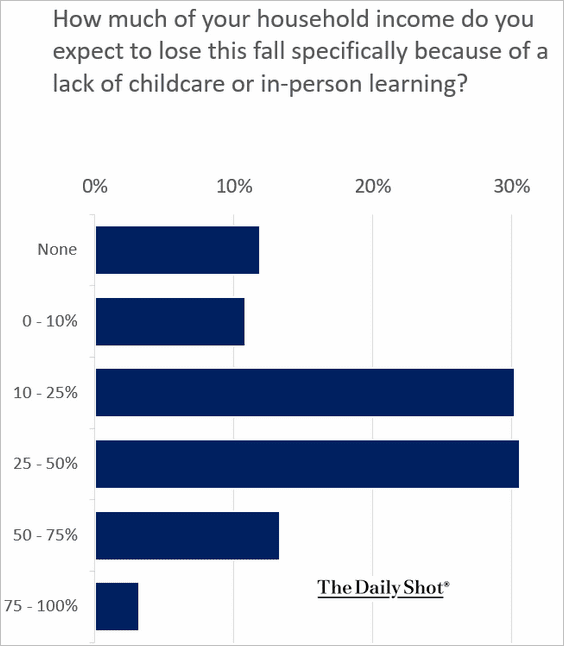

Analyzing potential market reaction always includes the “What is baked in?” question. We often have no good answer. That makes this chart quite interesting.

We should ask if this assumption is realistic?

[Jeff] Avoid blind acceptance of reports from analysts. Unless you know their assumptions and methods, just take a pass. In this case it is a revealing insight into a questionable conclusion about future consumption].

The Fed

Markets were reassured by the original Fed decision and statement. Selling began during Chairman Powell’s press conference. As usual, leading Fed observer Prof. Tim Duy provides the real scoop. Fed Doubles-Down on Zero Rates Despite Economic Gains. He draws upon the data that demonstrate the differences between now and the 2007-09 recession, before emphasizing this key Fed conclusion:

Despite these improvements, all the Fed see are downside risks:

The path of the economy will depend significantly on the course of the virus. The ongoing public health crisis will continue to weigh on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term.

And then finally this important observation about future Fed policy:

Bottom Line: The Fed is committed to zero-rates for the foreseeable future. They are not committed in the same way to the pace of asset purchases. The Fed though is not inclined to shift its current stance very easily. The bar is high for a rate hike. I suspect it is not nearly so high for the Fed to pull back on asset purchases. In the near term, that isn’t going to happen because the Fed is wedded to the bearish risks for the economy. If the forecast changes, the Fed will change with it. But they may be slow to change, and then change abruptly.

Callum Keown draws upon a range of market and economic observers in this excellent report: Stock markets have now seen the ‘peak of Fed stimulus’ unless these two things happen.

My conclusion? Those who see markets through the prism of QE are destined to be disappointed.

Corporate Earnings Expectations

The ultimate question for markets is the impact on expected corporate earnings. I regard the regular reports from Brian Gilmartin as among the most important indicators to watch. He updates forward earnings, sector analysis, and rates of change. Best of all, he shares data allowing readers to verify his conclusions. Here is his most recent post, providing the strongest support for a bullish argument. SP 500 Forward EPS Estimates Still Increasing

I have a few additional observations in today’s Final Thought.

Ideas for Investors

I have switched the investor section to a separate post. I hope to run it nearly every week, calling it Investing for the Long Term. It has turned out to be more comprehensive than it was as a part of WTWA, and more difficult to do. It is important to include the Great Reset concept as well. I may not be able to do this weekly, and it might be a bit shorter.

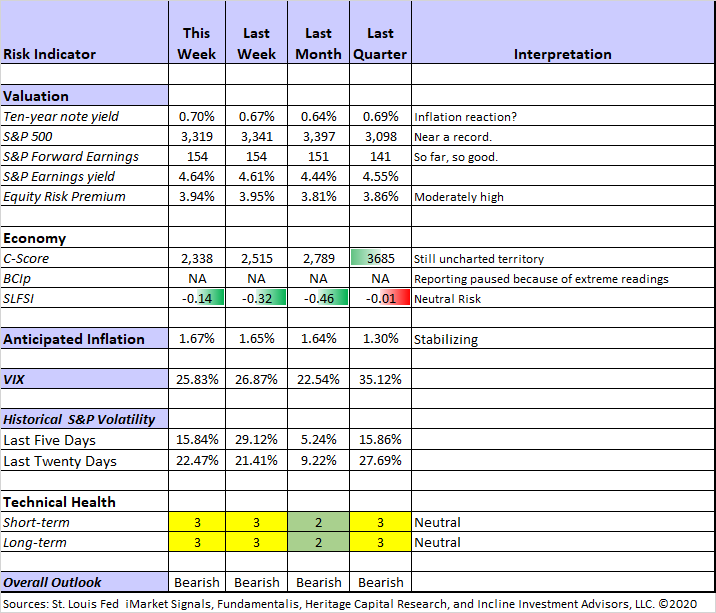

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

For a description of these sources, check here.

The technical indicators remain neutral and close to support levels.. My overall rating of “Bearish” is based on expectations for long-term investors. My key risk avoidance method is lightening up positions when I expect a recession. Hello? That is where we are. It is not a time for aggressive action by long-term investors.

The C-Score remains at levels never before seen. It is combining the sharp economic rebound with pandemic effects. When we are able to separate the two, a current mission of Dr. Dieli (who is making progress), it will provide more guidance on the timing and extent of the recovery.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies. This week Brian also takes note of the improvement in corporate credit spreads.

David Moenning: Developer and “keeper” of the Indicator Wall.

Georg Vrba: Business cycle indicator and market timing tools.

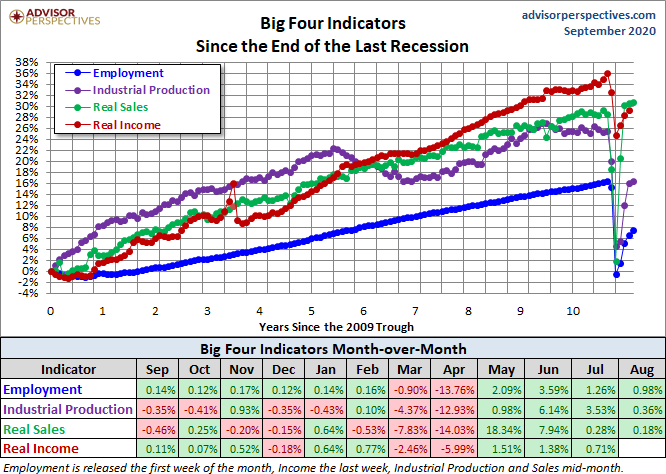

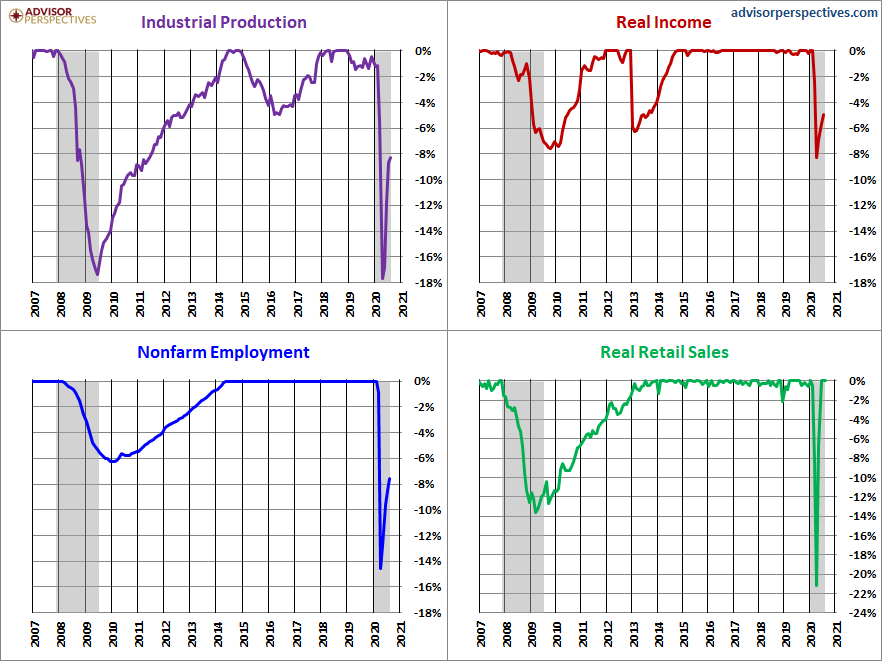

Doug Short and Jill Mislinski: Regular updating of an array of indicators. The most important are summarized effectively in the Big Four.

It is also helpful to consider the factors individually.

The strength of retail sales stands out. Will this continue in the face of the decline of unemployment benefits?

Retail sales showed sharp increases in May and June and very small increases in July and August.

Guest Commentary

Allan Roth offers 2 Reasons Stocks Recovered. Our interest at the Quant Corner is on #1. The key point:

This is to say that lower cash flows are worth more, because discount rate declined by more than the cash flow projections. The same is true for the stock market as a whole. Overall long-term earnings projections haven’t increased; they have merely shifted from companies like brick-and-mortar retailers to Amazon.

This argument is popping up in various quarters, but the explanation I am citing is easy to understand.

Final Thought

Several themes stand out in this complicated market.

- The economic data, which I have watched closely for decades, can be split into indicators that show current relative direction and those that show level. The former pointed upward after the stimulus. The Big Four, for example, reflects the level of activity. The response has been less positive. (And even that may be overstated if I am correct about the employment data).

- Too many market participants have a Fed fixation. For years this was viewed as the only reason markets rose. It became an element of Wall Street Truthiness. Somehow the fed asset purchases were magically transformed into direct support for stocks. No one succeeded in describing the causal factor behind this effect, but the belief persists. Those investors are about to be disappointed.

- The market rallies on any positive virus news. Expectations for a successful vaccine, production, distribution, willingness to use it, percentage of participants — none of that is discussed. Algorithms do not think this through, but investors can.

- The economic rebound from reopening has hit a stall zone. Our political leaders seem unready to act, so the data will probably go from slowing to getting worse.

How can an individual investor fight back against the quagmire of sophistry? My friend Rob Martorana has some excellent advice using important current examples. His list of biases is accurate and helpful.

And finally, what about the Supreme Court? As always, let us put aside our personal feelings about Justice Ginsburg and the current choices. Instead, what is likely to happen and how will it affect us as investors?

For now, my only comment is that my frequent statement about low investor impact from a Democratic sweep depends upon the Senate filibuster. The votes are not there to implement the so-called “nuclear option” to end this rule. It is a long-honored tradition and a change would not be supported by several Democratic Senators. If a Trump nominee is confirmed before the election, we should expect procedural retaliation from Democrats if they ever get majority Senate control.

You may choose to avoid politics and social issues. You cannot avoid investment decisions. Doing nothing is a decision! It might be the most important one you will ever make.

A Special Opportunity

Whenever there is an especially important issue, I generate a white paper. Last week I focused on finding and measuring portfolio risk. I think you will find my method to be helpful. Please also consider joining the Great Reset group. This drives my own investment analysis, and (I hope) inspires others. Join in my Wisdom of Crowds surveys. I need more wise participants! The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

There is no charge and no obligation for either the Portfolio Risk paper or the Great Reset Group. Just make your request at my resource page.

I’m more worried about

- The election. Not the outcome, but the process. Smooth transitions have been a staple of the U.S. government, but some are raising serious questions about this one.

- Cooperation on needed policies like more unemployment help and aid to local governments.

I’m less worried about

- Stock buybacks. Those worried about management manipulation should read this excellent analysis from Timothy Taylor. Key conclusion: Buybacks do indeed increase debt and leverage, but for corporate purposes. Management incentives have moved on from the short term.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits