"If most traders would learn to sit on their hands fifty percent of the time, they would make a lot more money." Bill Lipschutz

TINA revisited

Spending almost three weeks in Denmark this summer, I finally got to see friends and family I hadn’t seen since last Christmas, which was fab. On top of that, when your great friends from California (who are also Danish) happen to be there at the same time, it only gets better.

Jesper used to be a client of mine. Now, Anne and I have to settle for his and Louise’s friendship. If you know them, you will know what a great trade that is. Sitting in our Danish holiday home one evening in early August, enjoying one of Anne’ spectacular dinners, Jesper suddenly asked: “What do you make of Tina?” Being the fool I am, I thought he was referring to a former colleague of his, whom I also used to do business with, so I fell right into his trap: “Tina? Are you still in touch with her?”, I asked. Jesper laughed. “I am not talking about Tina but about TINA – There Is No Alternative”.

Suddenly the penny dropped. All evening, we had made regular references to the (perceived) insanity of the ongoing bull market in equities, and I suddenly realised what he was referring to – the extraordinary low yields that bonds offer at present, and how that has driven investors to buy equities despite the rather lofty valuation levels.

Considering the extraordinarily difficult circumstances for almost all corporates apart from a small number of tech giants that stand to benefit greatly from the current mayhem, it is hard to understand that logic for somebody like me who wants to apply a reasonable amount of fundamental analysis to the investment process.

Exhibit 1: Probability of US recession as currently priced in by various asset classes Source: J.P Morgan.

That I am not the only one scratching my (thinning) hair is evident every morning when I open the newspaper. The chart above (Exhibit 1) was sent to me last week and, as you can see, J.P. Morgan is now of the opinion that investors are pricing the S&P 500 as if the probability of a US recession is nil. Quite extraordinary!

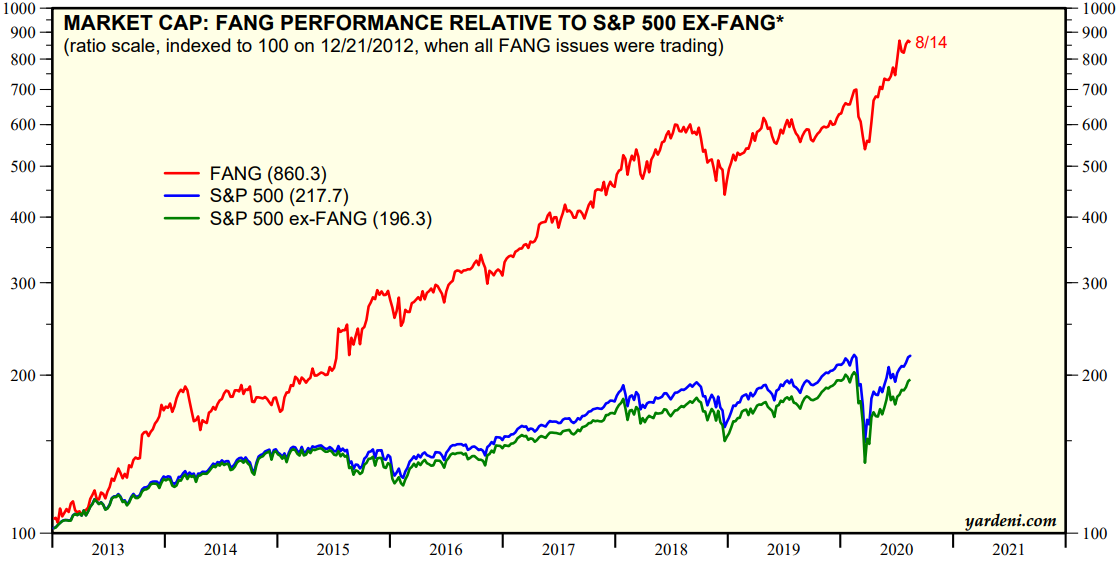

The worst example of mis-pricing I have ever experienced was the Japanese bull market of the late 1980s which ended in tears. That this one will also end in tears I have no doubt about, but there is a fundamental difference. Whereas the Japanese bull market in the late 1980s was very much driven by rising valuations in various service industries and an extraordinary bull market in real estate, especially in Tokyo, the US bull market of more recent times is driven by big tech (Exhibit 2).

Exhibit 2: FANGs vs. S&P 500 ex. FANGs* Note: The term “FANG” to be defined below. Source: Yardeni Research Inc., Standard & Poor’s.

Whilst the upswing in Japanese fortunes in the 1980s had no effect whatsoever on productivity and only caused even more capital to be misallocated, the bull market in big tech now is very much about increased digitisation and the productivity improvements that can be derived from that (although US valuations, as Japanese valuations in the 1980s, are also rising fast). For that reason, it will probably not be as tearful in the US as it was in Japan, but there will be tears nevertheless.

The link between starting multiples and long-term equity returns

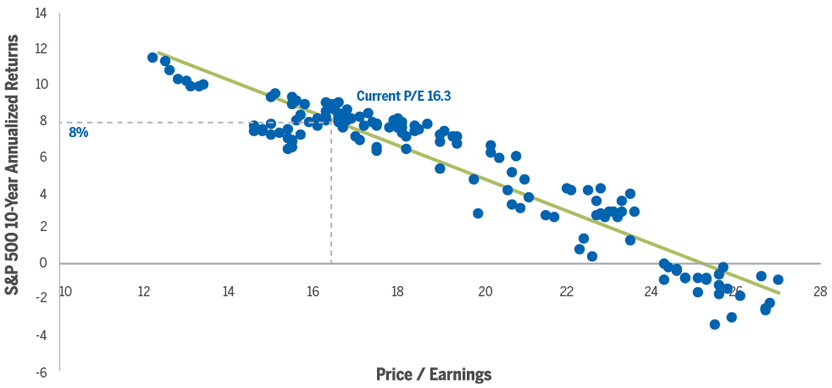

One of the most reliable predictors of long-term equity returns is the starting earnings multiple. History suggests that, when earnings multiples are in the low 20s, the best you can hope for over the next ten years is low single digit annual returns (Exhibit 3). As you can see, 10-year returns turn negative when the starting multiple is about 25 or higher. The R2 is a massive 0.8945, suggesting a very robust link between the two variables. Just don’t expect this technique to work well over shorter periods of time – it doesn’t.

Exhibit 3: Starting P/E Multiple on S&P 500 vs. Ensuing 10-Year Returns Notes: R2 = 0.8945. Data from January 1995 to September 2016. The chart was produced in late 2016 so ignore the suggestion that the current multiple is 16.3. Source: Alger.

Now to the bad news. Although earnings multiples are currently all over the place due to the extraordinary level of uncertainty at present, everybody agrees multiples are currently very high. Depending on whether you look at 2020 or 2021 earnings estimates, and depending on how optimistic (or pessimistic) the strategist in question is, the multiple on S&P 500 earnings is everywhere from the mid-20s well into the 30s. I suggest you plot those numbers in to Exhibit 3 and see what the ensuing 10-year return is likely to be.

Recent events

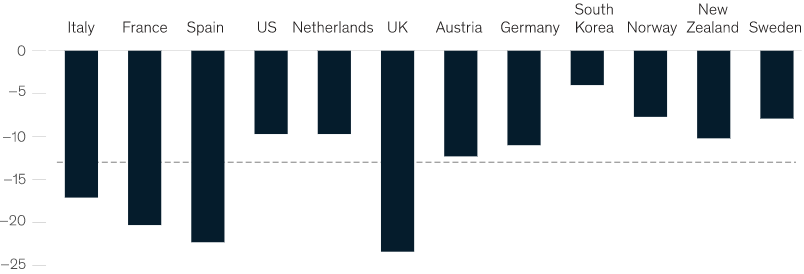

Exactly a year ago, the S&P500 closed at 2,926.44. On the last trading day of August, it closed at 3,500.31. In other words, over the last 12 months, which has been a period of unheard-of drama and uncertainty, the S&P 500 is actually up 20%. The story only gets better when looking at the Nasdaq index, up a massive 48% over the last 12 months. It is therefore only fair to ask – what on earth is going on? With the global economy in a virtual meltdown (Exhibit 4), how come equity investors have chosen to ignore that?

Exhibit 4: Change in Real GDP 2Q20 vs. 4Q19 Note: As reported by country statistical agencies as of 12th August, 2020. Netherlands, New Zealand and Norway are based on 2Q20 estimates from Oxford Economics. Source: McKinsey & Company.

A variety of reasons have driven equities, and particularly big tech in the US, higher, but TINA is fairly high on my list of valid explanations. In the interest of full disclosure, I should also mention the virtual limitless support from the Federal Reserve Bank during the crisis and, more recently, the move by the Fed to allow higher inflation, which is good for (most) corporates.

Adding to that, the Coronavirus pandemic has highlighted the necessity for a more robust digital infrastructure. With more people working from home, and with many of those likely to continue to work from home when the outbreak finally comes under control, many countries offer a hopelessly inadequate digital infrastructure. From an investment point-of-view, that is an opportunity, though.

In my holiday home in Denmark (in a very rural part of the country), I recently upgraded from 300MB download speed to 500MB for an extra £2.50 per month and still pay less than I pay for 5MB (on a good day!) in my primary residence only 30 miles from central London. The British had better get their act together unless they want to fall further and further behind!

The extraordinary performance of the Nasdaq index over the past 12 months is explained by a combination of these factors. One group of tech companies have done particularly well – the so-called FANGs (Facebook, Amazon, Netflix and Google (Alphabet)). The FANGs are sometimes referred to as the FAANGs (the FANGs + Apple), and Goldman Sachs always call them FAAMGs (Microsoft replacing Netflix). Just to confuse you, more and more frequently, you come across the term FAANGMs, which includes all six of the above-mentioned companies. To be fair, your choice of acronym shouldn’t change your conclusions much. They all deliver very similar results.

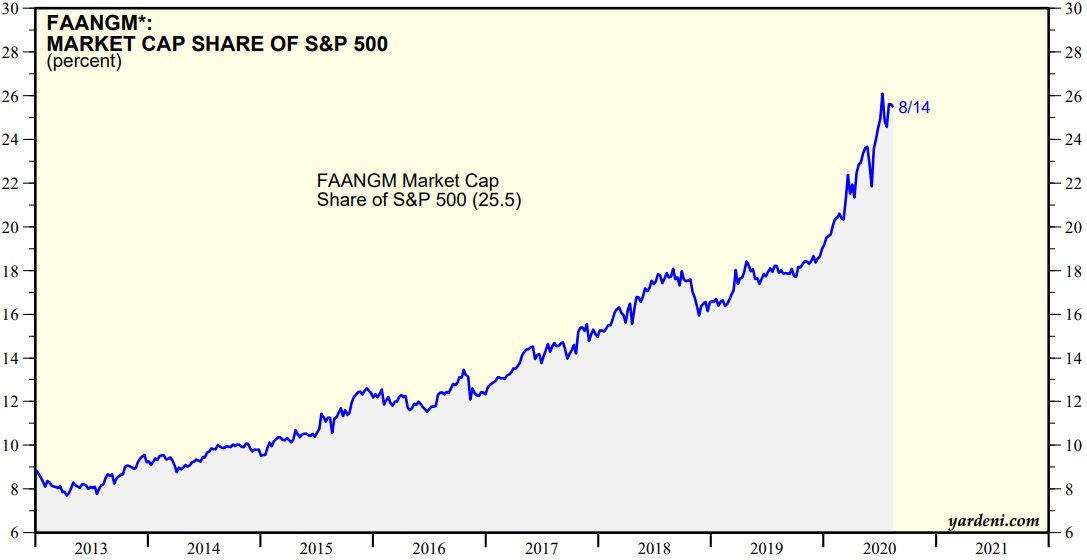

As the digital infrastructure improves, and as consumer habits change accordingly, the companies in FAANGM (just to make sure they all get a mention) stand to benefit immensely. It is therefore no wonder they have all performed so well more recently. Just how well is clear if you take another look at Exhibit 2. How dominant this handful of companies have become is obvious when you look at Exhibit 5 below. Less than eight years ago, the FAANGMs accounted for no more than 9% of total market capitalisation of the S&P 500. As you can see, the corresponding number today is 26-27%.

Exhibit 5: FAANGMs share of market capitalisation in S&P500 Source: Yardeni Research Inc., Standard & Poor’s.

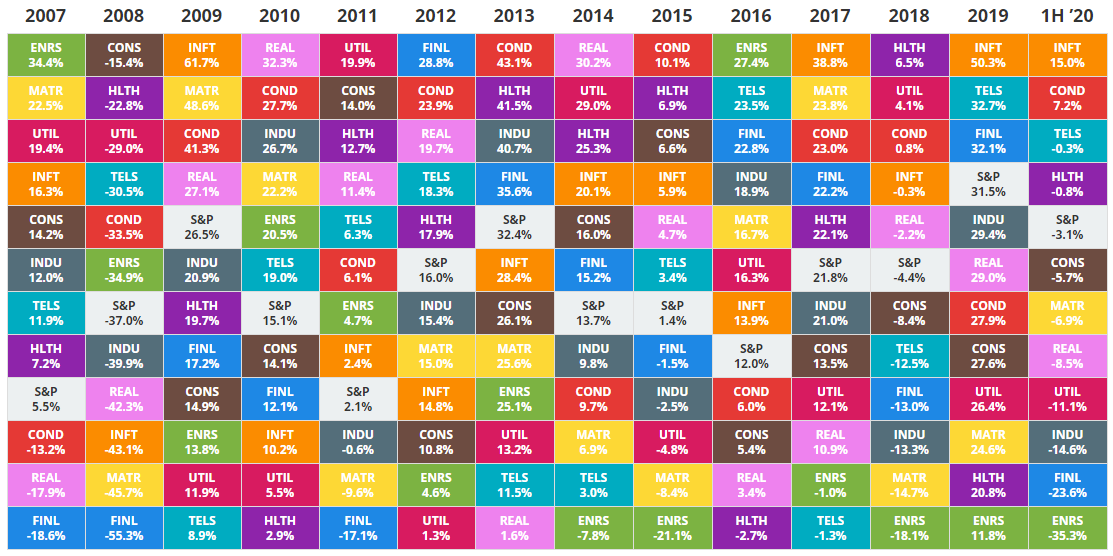

One last point before I move on. If the FAANGMs have managed to increase their share of the S&P 500 that dramatically over the past few years, there must have been some serious laggards. As you can see in Exhibit 6 below, energy stands out. In five of the last seven years, energy have been the worst performing sector in the S&P 500. Under normal circumstances, I would probably argue that now may not be a bad time to take a look at energy companies but, given the desire all over the world (ex. Trump’s camp) to phase out fossil fuels, I wouldn’t touch them with a barge-pole.

Exhibit 6: S&P 500 Performance by Sector Source: Novel Investor

Are we on a slippery slope?

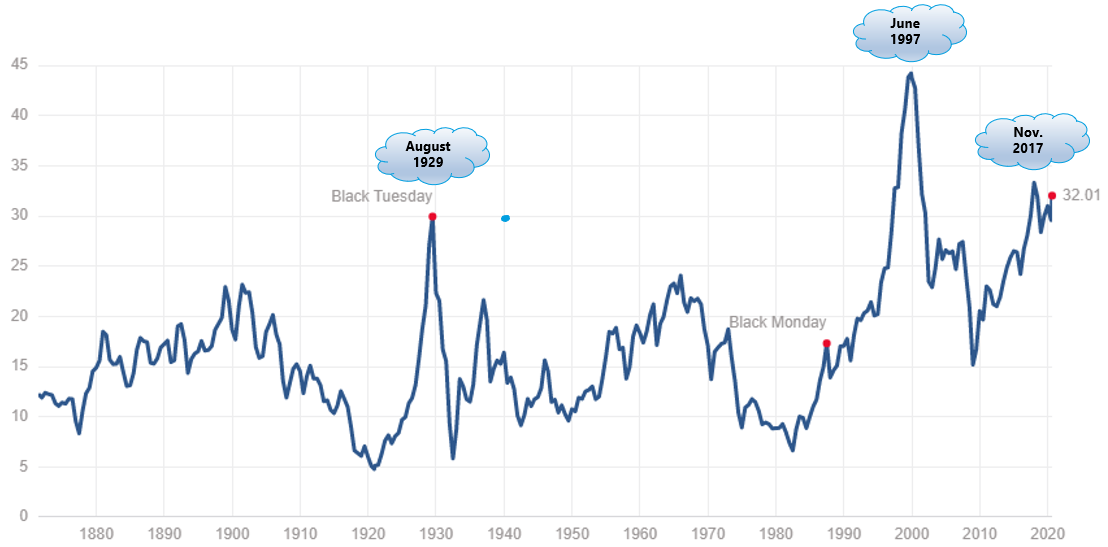

Obviously, when the economy is in a dark hole (as it is now), earnings suffer and, when earnings suffer, earnings multiples skyrocket, but that is not necessarly representative of the true earnings power over an entire economic cycle. To address this problem, Robert Shiller, Professor at Yale University, developed the cyclically adjusted P/E ratio or CAPE ratio for short. It is also known as the Shiller P/E ratio.

The CAPE ratio is calculated as the share price divided by 10-year average, inflation-adjusted earnings. By using earnings over ten years rather that just one, you smooth out the ups and downs that are a natural part of the economic cycle. As you can see in Exhibit 7 below, even if you cyclically adjust P/E ratios, US equities now trade at a massive 32x earnings. Over the past 150 years, they have been this high only three times before.

Exhibit 7: S&P 500 CAPE ratio since 1872 Source: multpl.com.

Past experience suggests that when the CAPE ratio is above 20x, one should switch the amber warning light on. When it goes above 25x, the amber light should turn red and, when it exceeds 30x, everybody should run for the hills. With the CAPE ratio now at 32x, now is not the time to take much risk in equities. That is at least the case in the US. Elsewhere, valuations are less steep, so you cannot necessarily draw the same conclusion all over the world, although a bear market in the US will have a meaningful impact on equities elsewhere.

The problem with big tech

As I mentioned earlier, one can indeed argue that the recent increase in the valuation of the FAANGMs is justified as a future with fewer brick and mortar retailers and fewer office workers travelling into town every morning can only benefit the FAANGMs but, at the same time, there is a much darker side to the tech story which I will share with you now.

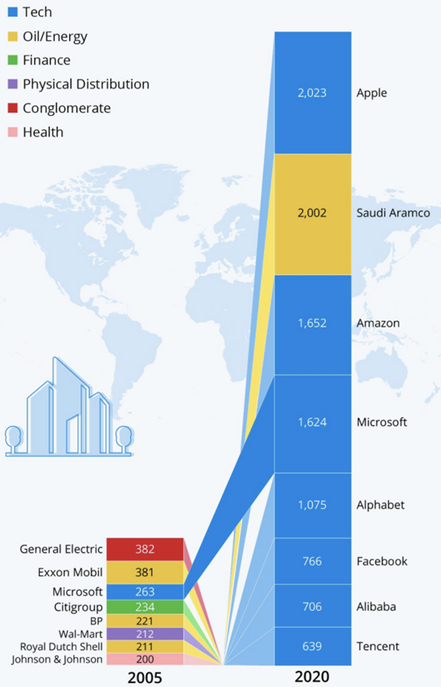

Exhibit 8: Companies with largest market capitalisation, 2020 vs. 2005 Source: Statista.

The question is a relatively simple one – are the FAANGMs getting too big for their own boots? Allow me to paraphrse Andrew (a colleague of mine) who said to me the other day that SMEs are the heart and soul of US business, and that a combination of the Covid-19 crisis and big tech is in the process of sucking that heart out (see for example this article in the Financial Times).

One could argue that big tech should be worried, should Biden win on the 3rd November but, equally so, one should worry about the heart and soul of US business, should Trump win. It is (sort of) a heads I win, tails you lose proposition. Just how big and powerful big tech has become is illustrated in Exhibit 8 above.

As you can see, seven of the eight largest companies in the world are now tech companies. 15 years ago, only one (Microsoft) was in the top eight. What you cannot read out of Exhibit 8, is that the composition of lists like this change dramatically from one decade to the next. I have seen similar lists going back to the 19th century, and there has hardly been a decade where well over half the names weren’t new.

Imagine we had the list for 2035 in our hands right now. I would be genuinely surprised if at least five of the eight names on the list above hadn’t dropped out. Nothing lasts forever; neither will the dominance of big tech.

What the 3rd November is really about

Going back to my opening statement about TINA, it is therefore likely that, sometime over the next few years (I have no idea precisely when), TINA will have to go shopping for plenty of Kleenex, such will be the need to wipe tears off the faces of lots of unhappy investors. Whether that will happen sooner or later will to a significant degree be dictated by who will be the next occupant of the White House.

Nobody yet knows precisely how ruthless the Biden & Harris team will be on Big Tech, but we do know that Kamala Harris in her job as District Attorney of San Francisco could be very tough. We also know that, more than once, Biden has talked about closing tax loopholes that Big Tech benefit from.

On the other hand, should Trump win, the United States of America (as a single country) might not survive another four years of his divisive policies. It is therefore far more than a ‘simple’ presidential election on the 3rd November. It is a vote for or against USA as a homogenous union and a vote for or against some very basic democratic principles.

Niels C. Jensen 2 September 2020

Niels Clemen Jensen founded Absolute Return Partners in 2002 and is Chief Investment Officer. He has over 30 years of investment banking and investment management experience and is author of The Absolute Return Letter.

In 2018, Harriman House published The End of Indexing, Niels' first book.