Key Points

- New All-Time Highs for SPY and QQQ

- Treatment and Vaccine Potential Provide Another Datapoint for the Bulls

- Will They or Won’t They on the Next Round of Fiscal Stimulus?

- Breadth Divergences are on Our Radar

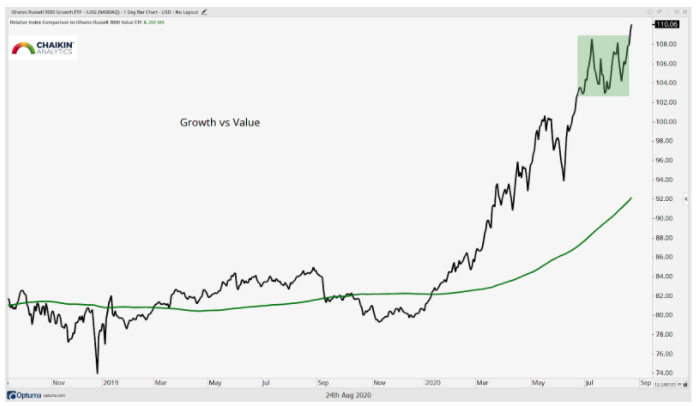

- Growth Breaks Topside From the Consolidation vs Value

Action Plan

This week, we continue with a bullish tilt toward equity positioning as the SPDR S&P 500 ETF (SPY) and the QQQ Trust (QQQ) trade at new all-time highs. Within the context of this bullish view, we highlight the re-emergence of Growth over Value as the ratio between the two has moved up and out of the short-term consolidation (in line with our prevailing views). Investors should continue to focus on ideas in the growth theme for long exposure either through ETFs or individual equities.

We have also been highlighting certain cyclical areas of the market that are beginning to perk up: Materials and Industrials in particular. It is important to understand that having a bullish view on growth does not preclude investors from also looking for ideas in the cyclical sectors, especially if those sectors are showing relative improvement, they are not mutually exclusive. While we are not believers in the wholesale shift to cyclical / value, we do want to continue to find the best opportunities across the investment landscape.

In the fixed income space, we see opportunity in the investment grade corporate debt as a way to take advantage of diversification as well as the rising inflation theme. The iShares Iboxx Investment Grade Corporate Bond ETF is a compelling idea to leverage this theme.

We remain bullish on precious metals but are closely watching the recent consolidations in Gold and Silver to determine which way they break and if we have to reevaluate our current views.

Commentary

US Equities

The trend for equities in the US remains in place with the SPDR S&P 500 ETF (SPY) and the QQQ Trust (QQQ) closing at all-time highs last week (in line with the thesis that we have been laying out for weeks / months). The iShare Russell 2000 ETF (IWM) has not yet reached a new high but does remain in an uptrend from the March 23rd lows. All three of these funds carry a Very Bullish (QQQ) or Bullish ETF Rating and all three sport Power Bar Ratios that are bullish.

Two weeks ago, we wrote that QQQ remained our favored exposure in the equity landscape and the fund has not disappointed as it has seen a resurgence of it’s relative strength vs SPY.

Leadership on the part of QQQ has played out as growth has broken topside from a near-term consolidation relative to value. Much was made in the press and by some well-known investors about the rotation from growth to value. We remained steadfast in the view that this was not a rotation but simply a pause in an uptrend that had become extremely extended. We have made the case over and over that this relationship would likely resolve to the upside and we were proven correct last week.

The bull case for equities may see an added boost this week with the president considering fast-tracking the coronavirus vaccine being developed by Oxford University and AstraZeneca for use in the US ahead of the November election. At the same time, the FDA has granted emergency use authorization of plasma treatment for coronavirus.

As our thesis and our bullish stance on the market continue to play out, we are not becoming complacent. It is always a good idea to have a sense of what is lurking around the corner that can derail the uptrend (note that “have a sense of” does not mean sell / become bearish). The first concern is on the policy front where the government has yet to arrive at a new fiscal relief package. Over the weekend both parties took the opportunity to blame the other for lack of progress on a bill. Investors are currently taking the stance that a bill is a matter of “when” not “if” and giving the benefit of the doubt to the prevailing trend in the market.

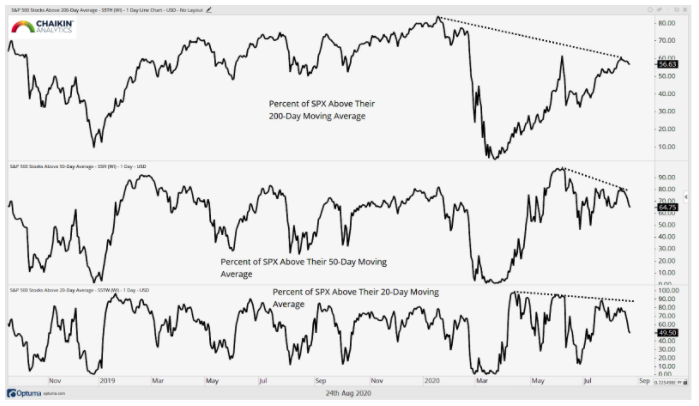

The other “elephant” in the room that has been getting much attention is breadth in the marketplace. First I want to make a distinction between participation and performance. Participation has to do with the number of stocks in the market that are moving in concert with the major averages. We can see here in the NYSE Advance / Decline Line that participation has been strong with the line making a new high on August 12th, ahead of the S&P 500, before turning lower last week (a small divergence).

Performance has to do with which stocks are leading. Here is where the breadth bears show their teeth. They call out the fact that only a handful of stocks (think FAN-MAG) are driving the gains. And in this regard, they are correct. The largest stocks have been leading from a performance perspective. So we have solid participation but the best performance is concentrated in a small group of stocks. The case can be argued in both directions.

The bigger “concern” from a breadth perspective centers on the divergences at the trend level. Across time-frames, these metrics have made a series of lower highs as the S&P 500 and the Nasdaq have moved to all-time highs. The chart below shows the percentage of stocks in the S&P 500 above their respective 200, 50 and 20-day moving averages.

Again, these are not sell signals but they do serve as a caution flag and investors should ensure that their risk management process is firmly in place.

Fixed Income

We have long been of the view that investors should have fixed income exposure as a diversifier to equity portfolios. We have largely expressed this view in the ETFs that are tied to treasuries but we now see an opportunity to add exposure in high grade credit, while swapping out of a portion of treasury exposure. The iShares Iboxx Investment Grade Corporate Bond ETF (LQD) has a Bullish ETF rating and is now oversold based on our indicator. During the recent consolidation, LQD found support at the rising long-term trend line, setting the stage for the uptrend to resume.

Commodities and Currencies

Dollar debasement remains the name of the game as the Invesco DB Dollar Bullish ETF (UUP) remains in a downtrend below the key $26 level. This has helped the commodity complex maintain a steady move to the upside as the inflation portion of our thesis plays out as well. We note that the move higher in the commodity complex extends beyond Gold and Silver. Crude Oil has seen a strong move from the April lows and many of the agricultural commodities have done the same. Finally, the price of Lumber has moved from ~$260 in April to nearly $850 this week.

The precious metals remain the way that we are expressing a bullish view on this theme, however we are mindful of the recent weakness in the group and will continue to monitor to determine if this exposure should be pared back in the near-term.

Dan Russo, CMT

Chief Market Strategist

Disclaimer

PortfolioWise is a product by Chaikin Analytics, LLC. Chaikin Analytics, LLC, is not registered as a securities Broker/Dealer or Investment Advisor with either the U.S. Securities and Exchange Commission or with any state securities regulatory authority. This information does not represent a recommendation to buy or sell ETFs, stocks or any financial instrument nor is it intended as an endorsement of any security or investment. The information, analysis, and opinions presented in our reports include the confidential and proprietary information of PortfolioWise and may include data provided by your financial representative which cannot be verified by PortfolioWise. This report is supplemental literature and does not take into account an individual's specific financial situation. Reports are solely for investment research and the user bears complete responsibility for any trading decisions. Users should consult with their financial advisor before making buy/sell decisions. For more information, see www.portfoliowise.com/disclaimer