I realized that it’s been so long since I started my NewsLetter, most of you won’t know its origins. To bring you up to date, here’s the intro to the first one.

In the fall of 2007, I started doing a NewsLetter for our firm’s professional friends (e.g., accountants and attorneys). Not exactly a traditional “Newsletter”; more a compilation of tidbits and commentary on a potpourri of items I find interesting. I called it a NewsLetter to emphasize that my goal is to provide succinct but interesting, fun and potentially useful “news.” To my pleasant surprise, the response of recipients has been very positive and a number of clients who don’t fall into the “professional” category but have been shown a copy by their accountants or attorneys have asked “How about us?” Good question. The model for my NewsLetter came from a friend who had designed his own letter for professionals. Now, having been asked to expand my audience (compliments always work for me), I’ve decided to experiment with a more general version in which you don’t have to wade through selected IRS code sections or recent court rulings.

So, welcome to the current version. Hope you enjoy.

I’M SHOCKED!

The Department of Labor published a notice indicating that it was sending a new fiduciary rule to the White House’s Office of Management and Budget, the standard step required for a regulatory review before it’s released to the public for comment. Entitled “Improving Investment Advice for Workers & Retirees Exemption” [right!], the new rule is expected to take a step back from the prior DOL fiduciary rule that was vacated in 2017, and instead to hew closely to the SEC’s own Regulation Best Interest rule. Not a big surprise as the current Department of Labor Secretary Eugene Scalia was one of the attorneys leading the industry’s lawsuit against the prior fiduciary rule. Don’t forget to have your adviser sign the Fiduciary Oath that I’ll paste to the end of this musing.

Thanks to Michel Kitces’ excellent Weekend Reading for Financial Planners for the update.

https://www.reginfo.gov/public/do/eoDetails?rrid=130634

http://www.thefiduciarystandard.org/wp-content/uploads/2015/02/fiduciaryoath_individual.pdf

MAY TAKE A WHILE

It’ll be a while before customers see them, but changes there will be …

Charles Schwab says that the Department of Justice has closed its investigation into its planned acquisition of TD Ameritrade. Schwab and TD Ameritrade’s stockholders have approved the deal.

BUYER BEWARE

From a recent OnWallStreet article …

Fidelity Magellan echoes glory days by trouncing benchmark

The stock-pickers are shining again at Fidelity Investments.

Fidelity Magellan, the mutual fund made famous in the 1980s by Peter Lynch, is trouncing its benchmark and peer group this year. Magellan returned 6% through Wednesday while the S&P 500 index lost 2.5% with dividends reinvested. The $19 billion fund was beating 95% of its competition as of Tuesday, according to data compiled by Bloomberg.

As always, don’t just buy the headlines; do your homework. The place to start is the benchmark the story is referencing—check out if it’s relevant for the investment. As is all too often the case, it’s not. Fidelity Magellan is a large cap growth fund, NOT a core S&P 500.

Take a look at the S&P 500 ETF (IVV) vs. the S&P 500 Growth (IWV) for the year through 6/5, the date of the article.

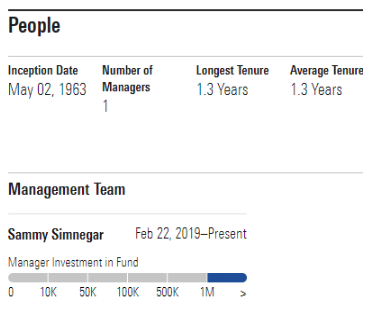

Now let’s add Fidelity Magellan (FMAGX) starting with manager tenure.

Simnegar was co-manager in February—relative performance since 2/22/2019.

How about year to date (Simnegar took over full management at the end of 2019)?

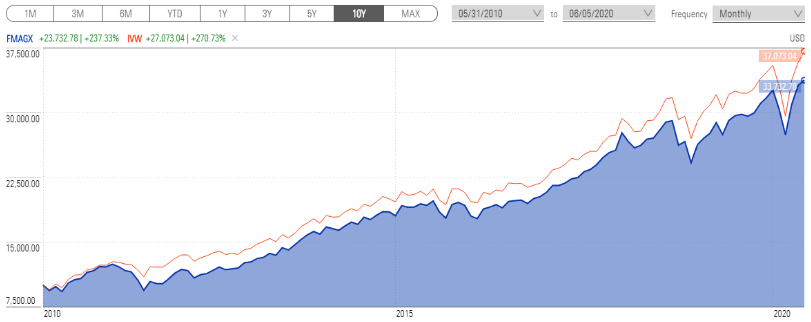

Now take a look at 10 years …

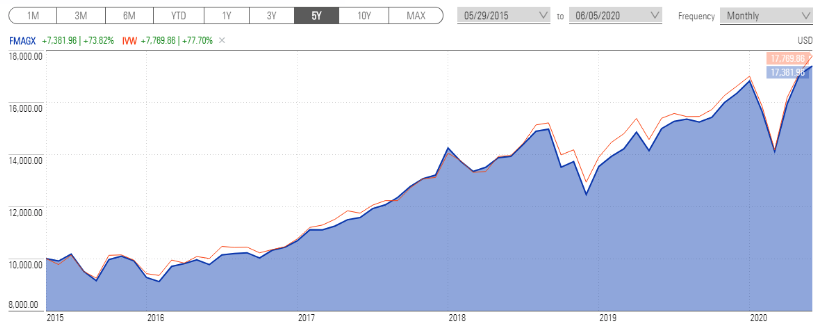

And the last 5 years …

Not exactly trouncing an APPROPRIATE benchmark. Much more of an index clone.

https://onwallstreet.financial-planning.com/articles/fidelitys-magellan-fund-echoes-glory-days-by-trouncing-benchmark?utm_campaign=onwallstreet-tw&utm_source=twitter&utm_medium=social&utm_content=socialflow

FOR OLD FOLKS LIKE ME

From my friend Alex …

TWELVE COMMANDMENTS FOR SENIORS

#1 – Talk to yourself; there are times when you need expert advice.

#2 – “In style” are the clothes that still fit.

#3 – You don’t need anger management; you need people to stop pissing you off.

#4 – Your people skills are just fine; it’s your tolerance for idiots that needs work.

#5 – The biggest lie you tell yourself is “I don’t need to write that down; I’ll remember it.”

#6 – “On time” is when you get there.

#7 – Even duct tape can’t fix stupid—but it sure does muffle the sound.

#8 – It would be wonderful if we could put ourselves in the dryer for 10 minutes, then come out wrinkle-free and three sizes smaller.

#9 – Lately, you’ve noticed people your age are so much older than you.

#10 – Growing old should have taken longer.

#11 – Aging has slowed you down, but it hasn’t shut you up.

#12 – You still haven’t learned to act your age, and hope you never will.

YOU CAN’T MAKE THIS STUFF UP

- The Arizona sheriff who tested positive for COVID-19 prior to a planned meeting with President Donald Trump still says he has no plans to wear a mask in public or enforce any future orders requiring one to do so.

https://www.usatoday.com/story/news/nation/2020/06/21/pinal-county-sheriff-mark-lamb-positive-covid-19-enforce-mask/3232821001/?for-guid=242ed6ca-6c81-11ea-a70f-129880492251&utm_source=usatoday-Coronavirus%2520Watch&utm_medium=email&utm_campaign=baseline_greeting&utm_term=newsletter_greeting

- “They Just Dumped Him Like Trash”: Nursing Homes Evict Vulnerable Residents

Nursing homes across the country are kicking out old and disabled residents and sending them to homeless shelters and rundown motels.

https://www.nytimes.com/2020/06/21/business/nursing-homes-evictions-discharges-coronavirus.html?referringSource=articleShare

- Ex-Morgan Stanley diversity chief sues for alleged race discrimination

https://onwallstreet.financial-planning.com/news/morgan-stanley-sued-for-discrimination-by-ex-diversity-chief-marylin-booker?utm_campaign=onwallstreet-tw&utm_medium=social&utm_source=twitter&utm_content=socialflow

- Trump urges slowdown in COVID-19 testing, calling it a “double-edged sword”

U.S. President Donald Trump on Saturday told thousands of cheering supporters he had asked U.S. officials to slow down testing for the novel coronavirus, calling it a “double-edged sword” that led to more cases being discovered.

https://www.reuters.com/article/us-health-coronavirus-trump-testing/trump-urges-slowdown-in-covid-19-testing-calling-it-a-double-edge-sword-idUSKBN23S0B4

CAVEAT EMPTOR

Shaking my head. These are not my observations (although I agree with them); they come from recent publications.

DOL Throws 401k Investors to the Wolves

https://www.forbes.com/sites/edwardsiedle/2020/06/13/dol-throws-401k-investors-to-the-wolves/#5f78302d7edd\

Labor Department Quietly Offers Up 401k Plans to Private Equity Vultures:

Leading U.S. Retirees “‘Like Lambs to the Slaughter”

With the American public’s attention consumed by the COVID-19 pandemic and mass protests against police brutality, the U.S. Labor Department earlier this month quietly gave corporate sponsors of retirement plans something they’ve been agitating over for years: a government green light to invest workers’ savings into funds managed by notoriously predatory private equity firms.

The move, announced on June 3 by Labor Secretary Eugene Scalia, allows large managers of 401(k) plans and individual retirement accounts (IRAs) to put workers’ retirement savings into private equity investments that offer the possibility of huge returns—and devastating losses.

https://www.alternet.org/2020/06/trump-labor-department-quietly-offers-up-401k-plans-to-private-equity-vultures-leading-us-retirees-like-lambs-to-the-slaughter/

Trump Administration Move

Could Add “Significant Risks” to Retirement Accounts

When it comes to a 401(k) account, most savers simply choose a target date fund and leave it at that.

Now, thanks to a rule change from the Trump administration, those retirement vehicles could soon get a lot more complicated. It’s likely to lead to new risks (and perhaps new rewards) for savers.

Managers of 401(k) plans now have the ability to invest in private equity. In other words, your 401(k) could soon take stakes in private companies.

The goal, according to Labor Secretary Eugene Scalia, is to allow investors to “gain access to alternative investments” and “ensure that ordinary people investing for retirement have the opportunities they need for a secure retirement.” The Department of Labor laid things out in a letter that says putting 401(k) money into private-equity funds would not “violate the fiduciary duties” of certain retirement plan sponsors.

But some experts see a big downside.

Barbara Roper, Director of Investor Protection at the Consumer Federation of America, said the “significant risks” associated with private equity investments haven’t been adequately addressed.

“By the Department of Labor’s own admission, these are investments that are more complex, more opaque, less liquid, more difficult to value, with often higher costs than the investments that are traditionally offered through retirement plans,” Roper said in an interview with Yahoo Finance.

https://finance.yahoo.com/news/trump-administration-move-could-add-significant-risks-to-retirement-accounts-115443201.html

Excerpts from The Regulators’ Conflicts of Interest by Tamar Frankel, professor of law emerita, Boston University Law School and one of the country’s most respected authorities on fiduciary issues.

Wide acceptance among federal regulators and the financial industry of conflicts among and a rejection of the principles contained in the Advisers Act is startling. It should especially worry investment advisers.

This rejection of the Advisers Act means that:

- Government is politicized. Conflicts are neither prohibited nor prevented directly.

- This is corrupting money managers and government personnel as well.

- We may “return” to darker days in history such as the early 1900s, the deterioration in trust and honesty and the financial disasters of the late 1930s that drove new regulations in 1933, 1939, and 1940.

This return to darker days will contaminate the financial system—advisers, brokers and dealers, money managers, and those who work for them—and also touch those who are subject to conflicts of interest.

The description above of the SEC’s ruling and the Labor Department’s behavior and approach demonstrates this observation. The SEC’s ruling leaves everything not specifically prohibited as potentially permitted.

FEE-BASED ADVICE HELPED INVESTORS SAVE $5.8B IN 2019: MORNINGSTAR

I know I’m prejudiced as a fee-only adviser, but I do like this headline …

https://financialadvisoriq.com/c/2777403/341973/based_advice_helped_investors_save_morningstar?referrer_module=emailReminder&module_order=10&login=1&code=YUdWMlpXNXphM2xBWldzdFptWXVZMjl0TENBeE1EY3hNVEE1TXl3Z01UUTBNamt4TVRJME1BPT0

GO FIGURE

NBC News

“So, we're officially in a recession. Market response? Dow rises, S&P erases losses, Nasdaq hits record high.”

https://www.nbcnews.com/business/markets/so-we-re-officially-recession-market-response-dow-rises-s-n1227761

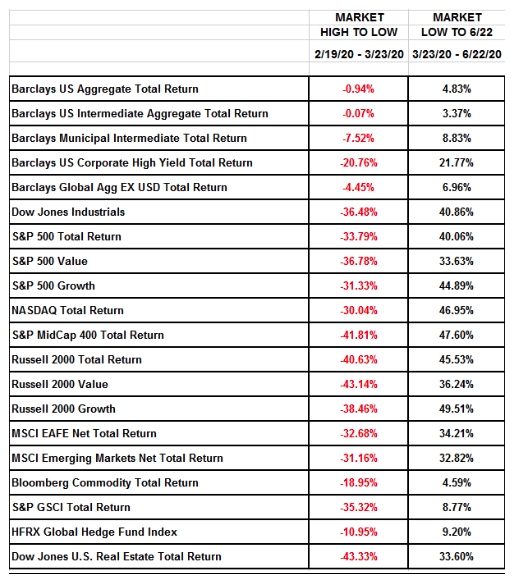

FOOD FOR THOUGHTFrom tables prepared by my partner Michael Walsh …

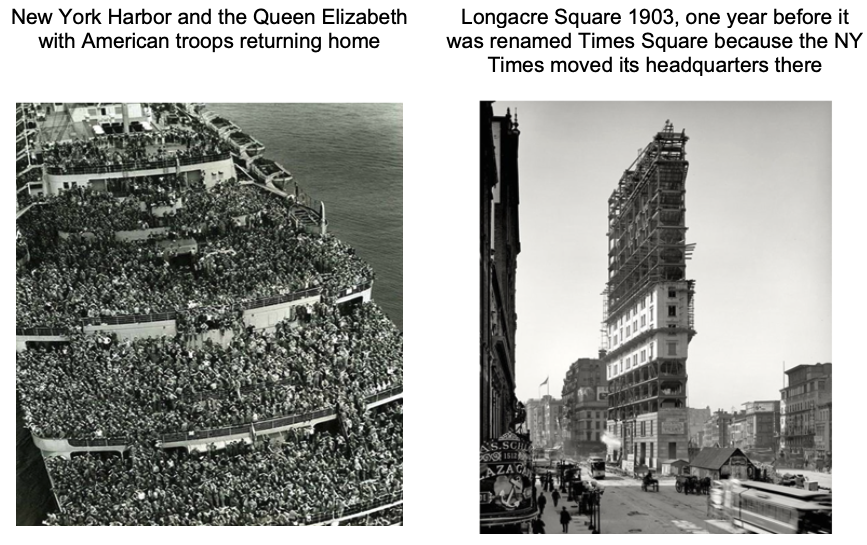

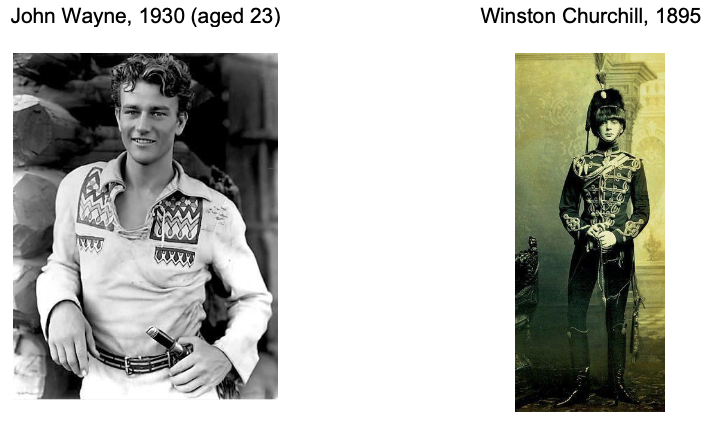

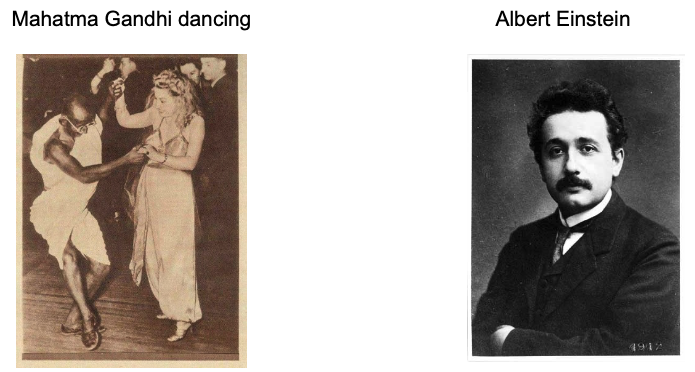

MORE AMAZING PICTURES FROM HISTORY

From my friend Alex …

A BILLION HERE, A BILLION THERE

A billion is a difficult number to comprehend, but one advertising agency did a good job of putting that figure into some perspective.

- A billion seconds ago, it was 1959.

- A billion minutes ago, Jesus was alive.

- A billion hours ago, our ancestors were living in the Stone Age.

- A billion days ago, no one walked on the earth on two feet.

SITTING DUCK

From a recent story in a professional publication.

If you occasionally feel like a sitting duck and get the feeling that an investment recommendation may be driven by something other than your interest, you may be right. There’s a reason that brokerage firms charge and product companies are willing to pay these outrageous fees to target brokers. It’s a win-win for everyone but the client.

Wells Fargo Raises Some Revenue-Sharing Fees for Asset Managers

“Wells Fargo Advisors has raised the upper limit of fees that third-party asset managers pay to get access to brokers who sell mutual funds and ETFs on its advisory platforms,” according to a regulatory filing.

The wirehouse has raised the ceiling on fees for “data agreements” that help asset managers target individual brokers interested in particular fund products to $650,000 from $550,000, it says. The minimum fee remains at $450,000.

Morgan Stanley, for example, charges as much as $600,000 per year for allowing fund salespeople to market to its financial advisors at branch offices and conferences, with payments rising for firms that agree to reimburse brokers for expenses, according to a revenue-sharing disclosure document on its website.

Morgan Stanley garnered headlines two years ago when it stopped selling Vanguard Group funds, known for their low management expense ratios, because of the money manager’s refusal to pay for “shelf space” and “access to the brokers.”

All the more reason for investors to insist on and get a signed copy of the Committee for the Fiduciary Standard’s Fiduciary Oath - http://www.thefiduciarystandard.org/wp-content/uploads/2015/02/fiduciaryoath_individual.pdf

https://advisorhub.com/wells-fargo-raises-some-revenue-sharing-fees-for-asset-managers/

BE INFORMED

Hope you enjoyed this issue, and I look forward to “seeing” you again.

Harold Evensky

Founder

Evensky & Katz / Foldes Financial Wealth Management

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz / Foldes Financial Wealth Management (“EK-FF”), or any non-investment-related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from EK-FF. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. EK-FF is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of EK-FF’s current written disclosure Brochure discussing our advisory services and fees is available upon request. Please Note: If you are an EK-FF client, please remember to contact EK-FF, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. EK-FF shall continue to rely on the accuracy of information that you have provided.

© Evensky & Katz/ Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management