Want to read more by PortfolioWise? Visit their Featured Firm page here

Key Points

- SPY Puts the February Highs in Sight as the Uptrend Persists

- Small Caps Continue to Improve; Shifting to Leadership?

- QQQ is Remains With a Bullish Rating and Near Record Highs

- Industrials Follow Materials with Emerging Cyclical Strength

- Earnings Exceed Low Expectations

Action Plan

This week we drill down on the trends in the US equity market as the SPDR S&P 500 ETF (SPY) puts the February highs in its sights. The trends across the major market ETFs remain to the upside.

The bull case centers on the implicit and explicit support of the Federal Reserve in conjunction with the prospect for further fiscal stimulus putting more capital in consumers’ pockets. Additionally, earnings reports in the second quarter have exceeded an extremely low bar. It is clearly the bull case that is in focus for investors now and that lines up with what has been our prevailing view since the April time frame.

If we wanted to make the bear case, it would largely center on what is well understood at this point. The risk that a new round of stimulus is not passed (we can debate the President’s executive order some other time). We can point to the still dismal employment numbers. We can call out percolating (simmering?) tensions between the US and China. I’m sure I am missing some but you get the point. Yes these are concerns but until the market cares, why would we? This is why having a solid risk management process is so important. If and when the market decides to pay attention to these or some other bearish factor, risk management will push cash levels higher.

We continue with a bullish stance on the equity market in the US (in line with the prevailing trends). Other trends on which we are bullish (but do not feature in this week’s note as they have not changed) are exposures to US Treasuries (slowing growth theme); exposures to precious metals (inflation theme, stretched in the near-term). At the same time we are becoming more bullish on trends outside the US with an emphasis on growth (EFG) and emerging markets where we are looking for oversold conditions to present a compelling opportunity.

Commentary

US Equities

Equities in the US have done a fairly good job of following the script that we have laid out over the past few months. The SPDR S&P 500 ETF has held above important support levels (which we have gradually been moving higher) and is now in a position to take on the February highs, which has been our base case.

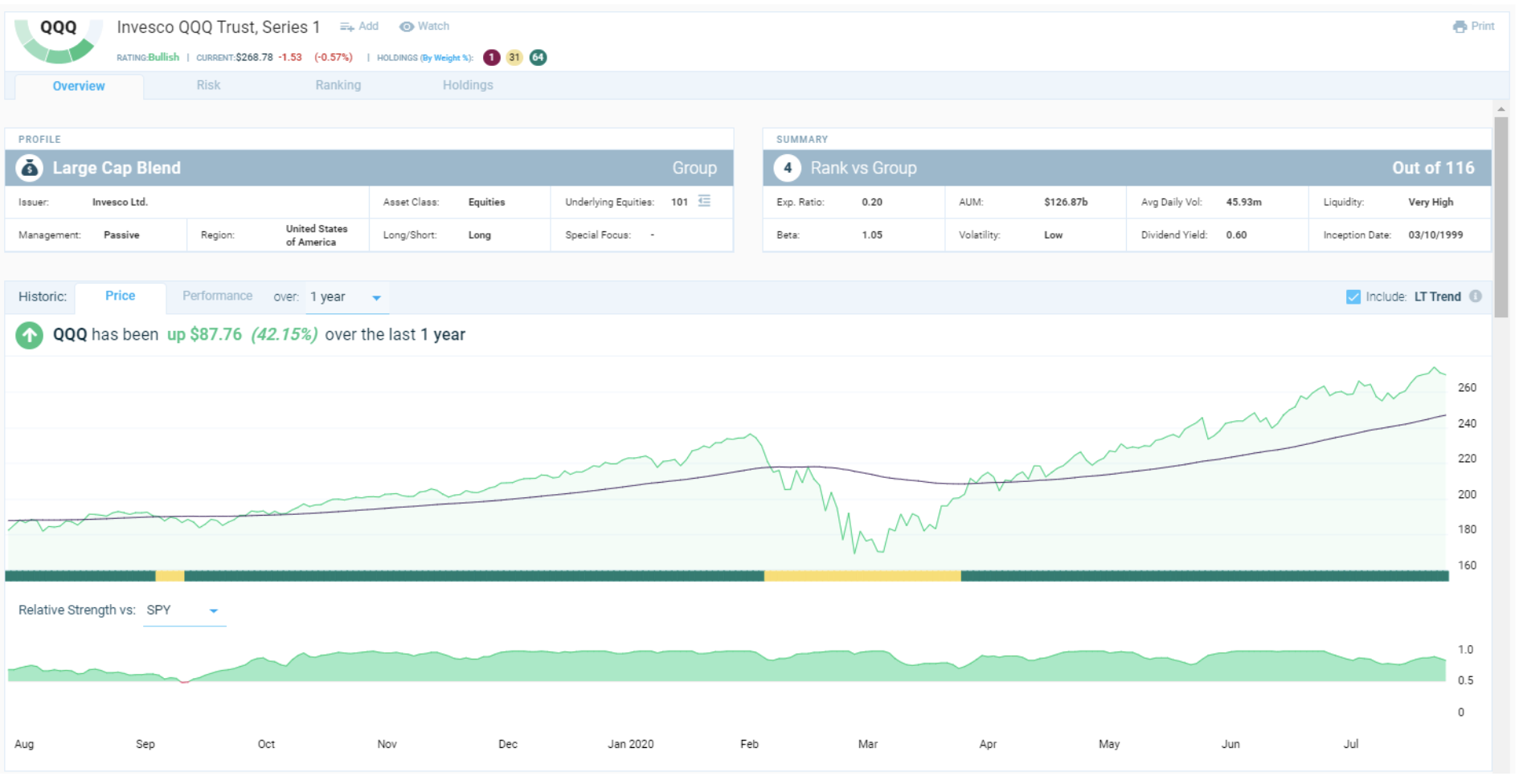

Not to be outdone, the Nasdaq QQQ Trust has been making new highs consistently since the beginning of June. This has been and remains one of our favored exposures in the market. Note that of the three main market ETFs, QQQ is the only one with a Bullish rating.

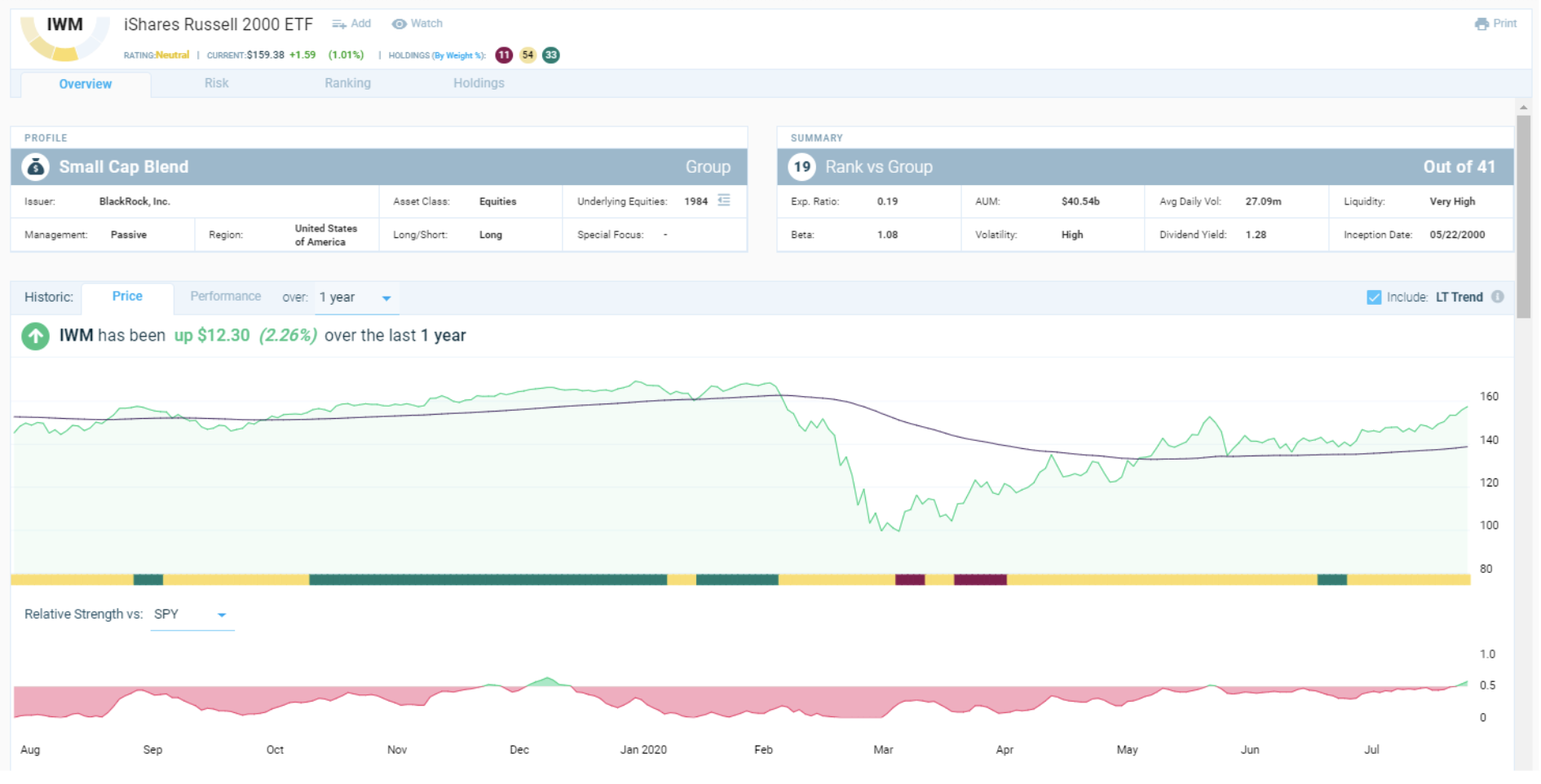

The one that we have missed is small caps. The iShares Russell 2000 ETF (IWM) has seen its relative strength steadily improve since making a low in March. Despite the fund being overbought in the near-term, we can no longer justify a bearish stance on this group.

The one negative that we can call out on the major market ETFs at this point in time is simply that all three are overbought based on our indicator, but let's put this in context, they are all overbought within uptrends from the March 23rd low.

The uptrends have persisted as earnings season has progressed. Companies are surpassing low bars based on overly conservative estimates from analysts who were left completely in the dark when management teams pulled guidance due to the lack of visibility from COVID-19. As of August 7th, 89% of the companies in the S&P 500 have reported with 83% reporting positive earnings surprises, which is the highest percentage beat rate since Fact Set began tracking the data in 2008. But we note that the trends in price were already well established which speaks to the importance of price over the prevailing narrative.

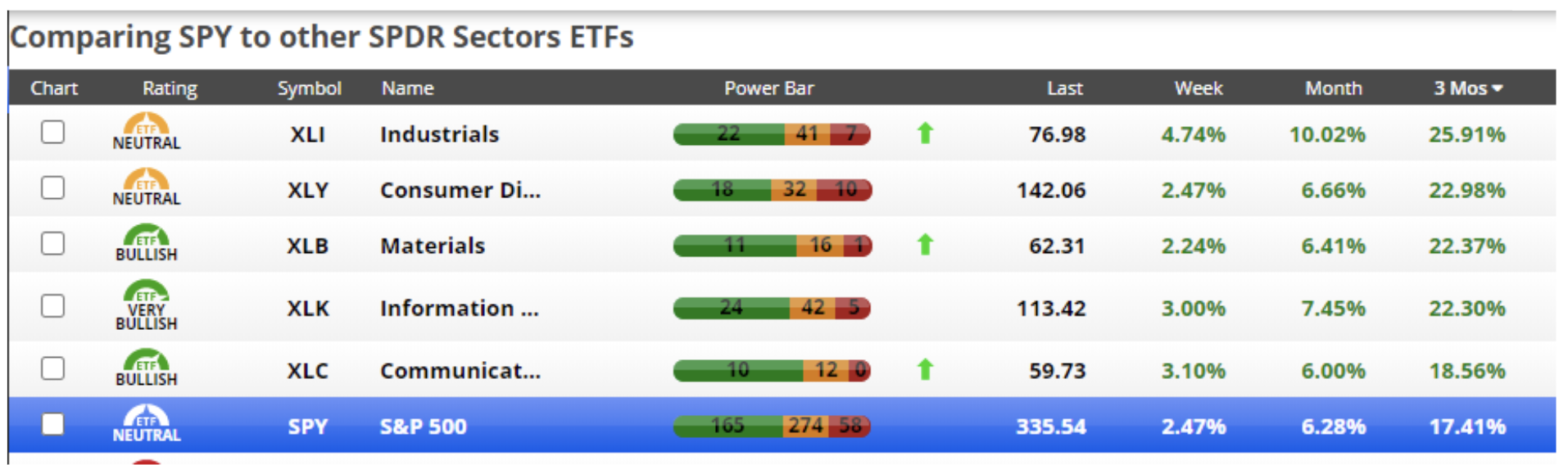

A few weeks ago, we began to see signs of life in the Materials sector as investors moved into the mining stocks, especially the names that were leveraged to the bullish precious metals theme. We are now beginning to see a similar dynamic at play in the Industrials sector. The Industrial Select Sector SPDR Fund (XLI) is on the verge of breaking above near-term resistance and Chaikin Money Flow has spiked to the upside as the long-term trend line has acted as support for the past few months. On a relative basis, the fund remains a laggard. However, we note that over the past three months, XLI is the best performing sector fund. The group is now on our radar as a possible leader in the weeks and months ahead.

The trend in the equity market in the US remains bullish despite many reasons called out in the bearish narrative. While we continue to view the “rotation” as a temporary pause in the outperformance of growth over value, we are mindful of the shifts playing out at the sector level and have recently begun to highlight the emerging bullish trends in areas such as Materials and Industrials.

Dan Russo, CMT

Chief Market Strategist

Disclaimer

PortfolioWise is a product by Chaikin Analytics, LLC. Chaikin Analytics, LLC, is not registered as a securities Broker/Dealer or Investment Advisor with either the U.S. Securities and Exchange Commission or with any state securities regulatory authority. This information does not represent a recommendation to buy or sell ETFs, stocks or any financial instrument nor is it intended as an endorsement of any security or investment. The information, analysis, and opinions presented in our reports include the confidential and proprietary information of PortfolioWise and may include data provided by your financial representative which cannot be verified by PortfolioWise. This report is supplemental literature and does not take into account an individual's specific financial situation. Reports are solely for investment research and the user bears complete responsibility for any trading decisions. Users should consult with their financial advisor before making buy/sell decisions. For more information, see www.portfoliowise.com/disclaimer