Want to read more by Smead Capital Management? Visit their Featured Firm page here

Everyone who owned common stocks in the U.S. went through hell in the first quarter of this year. The 36% decline in the S&P 500 Index in February and March was the fastest 36% decline of my lifetime. This hell was especially damaging to those of us who have a positive view of the U.S. economy over the next ten years.

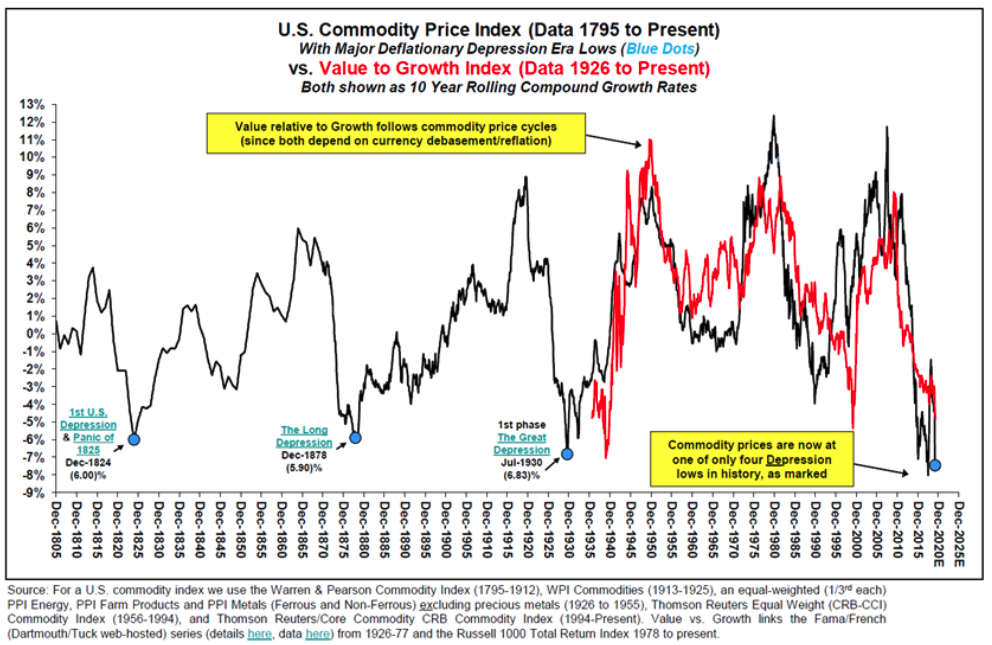

The decline hit economically sensitive stocks much harder than even the index reflects. Commodities, which are usually a pretty good reflection of economic strength, came out of the decline as depressed versus common stocks as they have been in the last 215 years (see chart below):

Source: Stifel, Macro & Portfolio Strategy, April 5, 2020. 12/1/1805 – 12/31/2019. Data for time period 12/1/2020 – 12/31/2025.

The complete collapse in economic optimism, due to the COVID-19 pandemic quarantines, translated into vicious declines of share prices in certain sectors and industries. Energy stocks, retailers/malls, airlines, general travel and other in-person consumer discretionary companies were battered as much as we had seen in 2007-2009 and in the 1987 stock market crash. We are huge fans of Warren Buffett and Charlie Munger, but it is unlikely they have been more scared by economic circumstances in my lifetime than they were in March through May. Buffett tried to put a positive spin on America in his virtual Berkshire Hathaway Annual Meeting, but his positive spin only stretched to mindlessly investing into the S&P 500 Index.

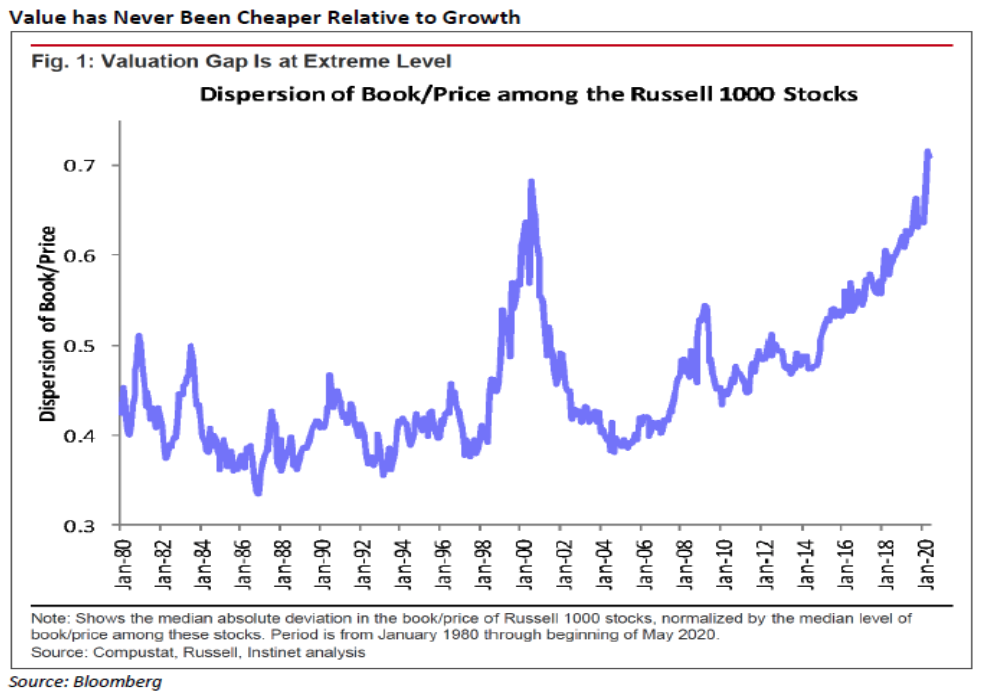

Therefore, with the most brilliant value investors of all time sidelined in fear and trapped out by size considerations, value investments reached epic underperformance levels versus the index and especially to growth stocks as a category (see the chart below):

Source: Cypress Capital Market Outlook, May 29, 2020. Data for the time period 1/1/1980 – 1/31/2020.

Therefore, the “opportunities” in hell were closely tied to smaller capitalizations, deep value pricing and in industries which made you nauseous to even think about making an investment. So, we pulled out our eight criteria for common stock selection and began tacking our portfolio toward companies at the epicenter of COVID-19 fears and in the middle of the burning flames. We replaced Occidental Petroleum (OXY) with Chevron (CVX), which was a massive balance sheet upgrade. We bought into Simon Properties (SPG), the most powerful mall owner in the U.S., after watching the founder and the CEO buy millions of dollars of the stock in the $55-$60 per share area.

We bought into Credit Acceptance Corporation (CACC) at fire-sale prices when used auto prices scared the hell out of its existing investors. You think quite a few credit-worthy car buyers might have a besmirched credit score the next time they need a car? We nibbled on Ulta (ULTA) and Carter’s (CRI) in the retail world. Lastly, we got started in Amerco (UHAL), because we think the great intra-country migration of millennials is being triggered by COVID-19.

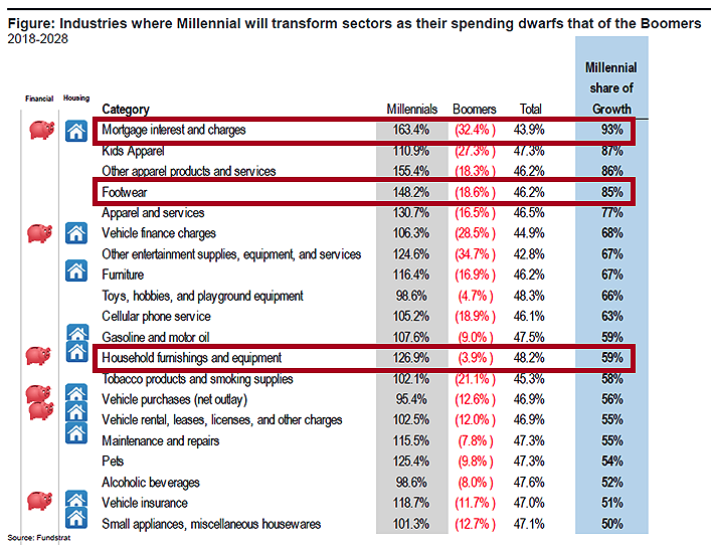

In all, we were busier in the first half of 2020 than we had been since 2008’s version of hell. The good news for our long-term investor base is the depressed prices that the 2008 hell provided us and offered years of wealth creating share ownership. These hellish circumstances result in more companies meeting our eight criteria for stock selection. Many of them are in the sweet spot of where the 30-45-year-old millennial group will take their spending in the next ten years.

Source: Fundstrat, “The Long Game,” 2019 Strategy. Data as of 12/31/2018 and projected through 12/31/2028.

We like Carter’s (CRI) because kid’s apparel could rule the next ten years. We like the home builders to satisfy an enormous demand for new homes to offset the COVID-19 destruction of the supply of existing homes (which won’t happen in the aftermath of nursing home problems). The baby boomers are likely to stay in their home and call Tom Selleck for a reversible mortgage to pay for in-home care.

We are underinvested in energy, because Chevron (CVX) seems to be the only financially strong company which will fill the need. We believe that the major banks are being massively underestimated, as they own the millennial depositors and provide superior mobile banking.

The one big upside to COVID-19 in our portfolio is that it exposed how valuable our pharma/biotech companies are. Amgen (AMGN) and Pfizer (PFE) are leaders in potential vaccines and have the financial muscle to act quickly. Merck (MRK) looks very undervalued as well, even though numerous cancer patients’ lives have been endangered by quarantines.

Lastly, the shortages created by quarantining exposed how attractive some of our companies are. Target (TGT) was allowed a near monopoly as an essential business and still looks very attractive when clothing shopping rebounds. Home Depot (HD) became the go-to place for bored folks quarantined at home. Houses and yards have probably never looked better. eBay (EBAY) found six million new buyers, numerous new sellers and is seeing a virtual renaissance in their marketplace business. Isn’t it interesting how much more profitable it is being an exchange, rather than being an online retailer? Amazon can have the glory; we will take the profit.

Many people have asked us what would create heaven (significant and prolonged outperformance versus the S&P 500 Index) for investment disciplines like ours. First, the economy would be substantially better the next ten years than the media and prognosticators think it will be. As an economist, we see a huge increase in 30-45-year-old homeowners, children born into average to above-average income households and grandparents starving to spoil them. The circumstances post-COVID are giving them cheap gasoline, historically low mortgage rates, and a healthy skepticism.

Second, the psychological setup is very favorable. The maximum enthusiasm for stocks is in the misery-laden glamour tech stocks, who seem to have gained favor from the quarantines. The psychology going forward is not in economic enthusiasm (see the chart below):

Source: Barron’s, “Growth’s Edge Over Value May Finally Be Nearing Its End” written July 3, 2020.

Third, interest rates would rise gradually as the economy recovers and millennial home and car buyers begin to dominate. The rising interest rates depress growth stock price-to-earnings ratios going forward:

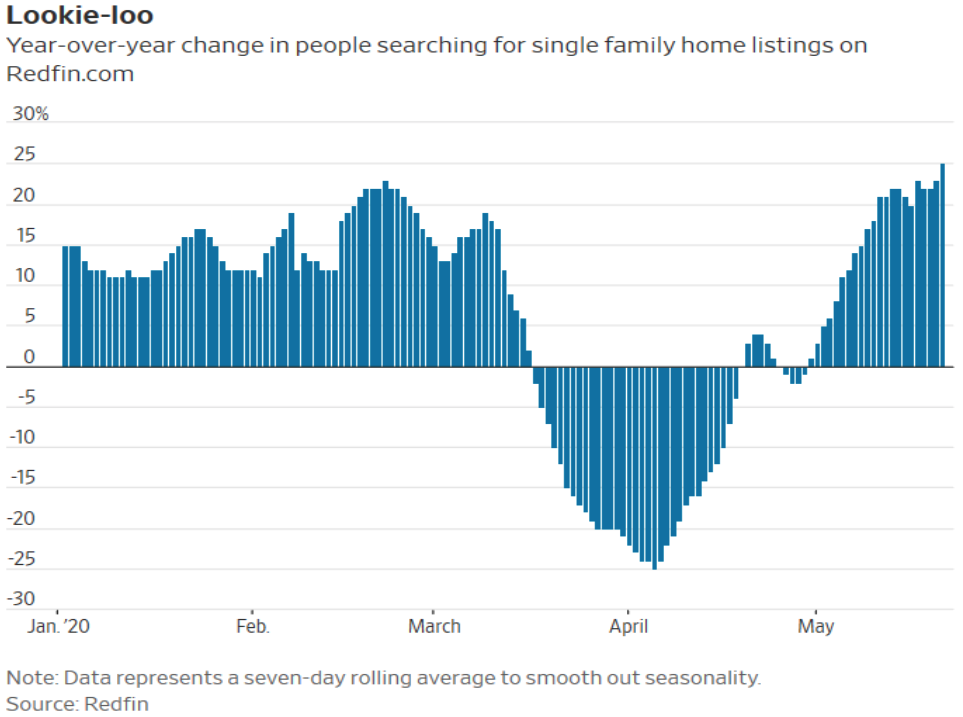

Source: https://www.wsj.com/articles/remote-work-could-spark-housing-boom-in-suburbs-smaller-cities-11590843600. Data for the time period 1/1/2020 – 5/31/2020.

We know we have a lot of work to do to win back the full confidence of investors. One thing stands in our way currently: the extreme popularity of the largest technology companies. Their ability to suck up capital at the margin might even give the dotcom bubble disaster a run for its money (see the chart below):

Source: Barron’s, “Growth’s Edge Over Value May Finally Be Nearing Its End” written July 3, 2020.

Financial euphoria episodes always last longer than people expect because “the market can stay irrational longer than investors can stay solvent!” To quote John Kenneth Galbraith from his great book, A Short History of Financial Euphoria:

The only remedy, in fact, is an enhanced skepticism that would resolutely associate too evident optimism with probable foolishness and that would not associate intelligence with the acquisition, the deployment, or, for that matter, the administration of large sums of money. Let the following be one of the unfailing rules by which the individual investor and, needless to say, the pension and other institutional-fund manager are guided: there is the possibility, even the likelihood, of self-approving and extravagantly error-prone behavior on the part of those closely associated with money. Let that be the continuing lesson of this essay.

A further rule is that when a mood of excitement pervades a market or surrounds an investment prospect, when there is a claim of unique opportunity based on special foresight, all sensible people should circle the wagons; it is the time for caution.

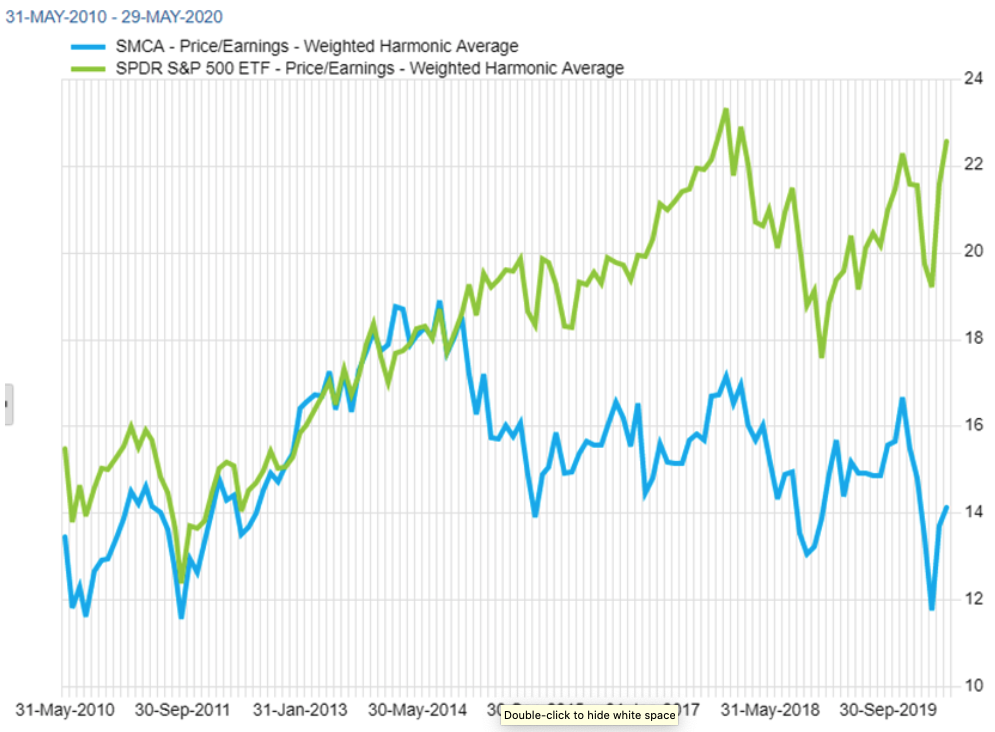

Our portfolio is the cheapest relative to the stock market on a price-to-earnings and dividend yield basis it has been since we started this strategy in 2008.

Source: FactSet. Data shown is for Smead Capital Appreciation vs. S&P500 ETF for the time-period 5/1/210 – 5/31/2020.

We look forward to seeing whether that plays out in long-term index outperformance, because we believe Galbraith, who last revised this book in 1993, will be spot on again. Thank you for your ongoing support and capital commitments.

Smead Capital Management, Inc.(“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Arizona. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Registered investment adviser does not imply a certain level of skill or training.

This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the publications.

For additional information about SCM, including fees and services, send for our disclosure statement as set forth on Form ADV from SCM using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

© 2020 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap