Market Scout - International and Emerging Markets Opportunities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsHigh-quality companies outside the U.S. look especially attractive to us. And their stocks have underperformed recently, possibly giving them greater upside potential.

On June 22, 2020, we issued a paper entitled Opportunities Outside the United States—which assesses the status of small- and mid-cap companies in international developed and emerging markets. Our conclusion is that stocks in these markets have generally underperformed their U.S. counterparts for more than five years. But we believe business-quality measures are generally better outside the United States.

Moreover, we think the four Wasatch international and emerging markets strategies that are discussed in the paper stack up especially well in terms of quality. This combination of modest performance in the recent past and attractive business-quality fundamentals gives us optimism for these strategies going forward.

In this Market Scout, we summarize the main points from Opportunities Outside the United States. For the full paper, please visit the News & Insights section at wasatchglobal.com. We begin with the performance of stocks as categorized by various benchmark indexes. Then we present what we consider to be one of the most important measures of business quality—EBIT ROA. We also show how the four Wasatch international and emerging markets strategies compare to their benchmarks in terms of EBIT ROA.

STOCK PERFORMANCE DURING THE PAST SEVERAL YEARS

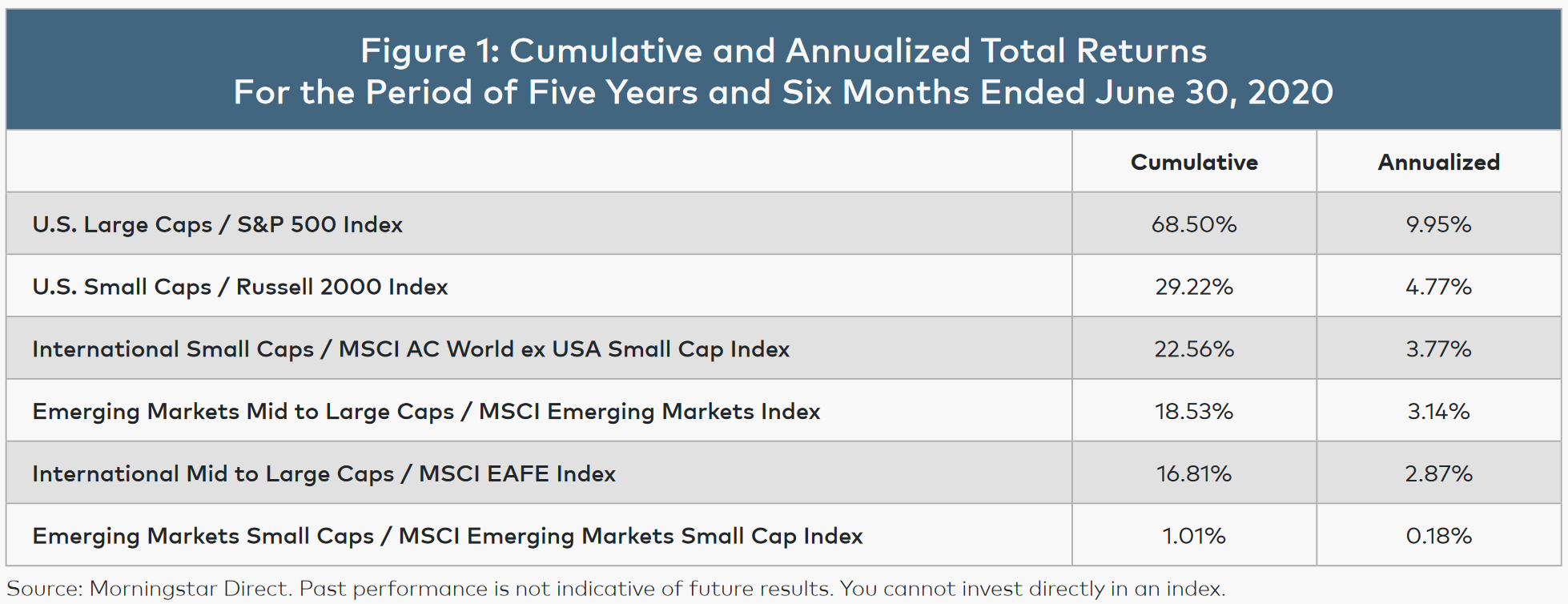

Starting with the United States, we note that U.S. small caps (as represented by the Russell 2000® Index) have underperformed U.S. large caps (as represented by the S&P 500® Index) during the past several years. This underperformance is evident in Figure 1 below.

Figure 1

Not only have U.S. small caps lagged U.S. large caps, but they’ve experienced the worst of both worlds—generally performing less robustly in the rising environment before the Covid-19 pandemic and more poorly in the falling environment after the pandemic began. For the 2020 year-to-date period through June 30, U.S. small caps were still lagging large caps—even after the rebound from the trough of the Covid-related selloff.

Like U.S. small caps, international small caps have shown disappointing returns. Among the other categories of stocks presented in Figure 1, the returns have been progressively worse: emerging markets mid to large caps, then international mid to large caps, and finally emerging markets small caps trailing them all. For the entire period of five years and six months—leading up to and including the Covid-19 pandemic—Figure 1 shows the respective cumulative and annualized total returns in order of best to worst.

Think about these numbers for a moment. In this span of five years and six months, emerging markets small caps, for example, have made only about 1% cumulatively—which is less than 0.2% on an annualized basis.

HAS HISTORICAL STOCK PERFORMANCE BEEN JUSTIFIED BY COMPANY FUNDAMENTALS?

At Wasatch Global Investors, we’ve always been quick to acknowledge that it often makes sense to hold onto stocks that are performing well if the underlying company fundamentals continue to show the potential for strong performance going forward. In other words, it has been our experience that the stocks of companies with great management teams and with headroom for growth often have risen nicely for years on end. Having said that, it’s just as important to identify when company fundamentals may no longer point to strong stock performance ahead.

We also believe there are circumstances in which solid company fundamentals are underappreciated by investors—and are poised to be recognized. We think this type of underappreciation may be present among many companies in international developed and emerging markets.

MEASURES OF QUALITY

In our paper Opportunities Outside the United States, we look at several measures of quality: estimated long-term earnings per share (EPS) growth, long-term debt to capital, return on equity (ROE), return on assets (ROA) and EBIT ROA.

U.S. small caps, for their part, have reasonably strong scores on these measures of quality—which is one reason for our optimism on the U.S. small cap category. What we see in the paper is that international developed and emerging markets also include companies with attractive scores on these measures of quality. More importantly, the four Wasatch international and emerging markets strategies exhibit even better scores.

RETURN ON ASSETS (ROA) AND EBIT ROA

Of all the measures of quality, return on assets (ROA) is particularly useful when analyzing companies with larger amounts of assets and/or debt on their balance sheets. Furthermore, we look at EBIT ROA to compare companies based on operating earnings without the influence

of financing differences and taxes. This is calculated as earnings before interest and taxes (EBIT) divided by total assets. EBIT ROA is a gauge of management’s efficiency in utilizing all of a company’s assets—not just the capital of the ownership base—to create profits. For example, a company might be able to maintain a high ROE by issuing debt, but such a move would be reflected in the company’s EBIT ROA. As shown in Figure 2 below, the overall EBIT ROA for each Wasatch strategy discussed here is higher than for the category/benchmark index.

Figure 2

An important caveat is that our emerging markets strategies tend to have more significant holdings in financial companies, which we think are particularly vital for the progress of less well-established nations. Since financial companies inherently employ larger amounts of debt, our emerging markets strategies show lower overall EBIT ROAs than would otherwise be the case. Nevertheless, we believe our financial companies are some of our most attractive investments because of the companies’ strengths compared to competitors and because of the enormous growth opportunities as individuals and businesses increasingly take advantage of financial services. Incidentally, when we look at EBIT ROAs across companies, we’re more interested in making comparisons within a single industry or sector—rather than evaluating a bank versus a tech company, for example.

“PAYING UP” FOR GROWTH

Measures like EPS growth, long-term debt to capital, ROE, ROA and EBIT ROA are all independent of a company’s stock price. In other words, these measures tell us something about the management expertise and the competitive position of a company—but the measures don’t tell us what investors should be willing to pay for that company.

A common measure of the perceived expensiveness of a company is the price/earnings (P/E) ratio, which is simply the stock price divided by earnings per share. The P/E ratio can be calculated in a number of ways—for example, based on trailing earnings or based on projected future earnings. We think most investors would agree that a high-quality company deserves to sell at a greater P/E ratio than a lower-quality company. The question is, “How much greater?”

At Wasatch Global Investors, we often invest in companies with significantly larger P/E ratios than the ratios for companies in the benchmark indexes. Our reason for this is that we believe the high-quality characteristics we emphasize will allow our companies to grow sales and earnings much faster than the average index constituent. In other words, we’re not afraid to “pay up” for growth if, for example, we think a company can double in size within the next five years or so. Moreover, we believe high-quality companies are often better able to maintain operations during periodic downturns and emerge well-positioned for the long term—even if their stocks are priced somewhat more richly in the short term.

Another point regarding “paying up” for growth is that it doesn’t necessarily result in higher volatility of a portfolio’s performance. Beta is a measure of volatility compared to a benchmark index. And the Wasatch strategies generally have had lower betas than their benchmarks, as you can see at wasatchglobal.com.

WASATCH OUTLOOK AND POSITIONING

At Wasatch Global Investors, we’ve always tried to devote our research efforts to those areas where we see the most opportunities. For decades, we’ve found exciting businesses among U.S. small and micro caps—and we still do. But when we look at the global landscape, our preferred measures of business quality seem most attractive outside the United States.

In fact, when we consider the quality measures referenced above, the numbers appear to us as strikingly better for the categories/benchmark indexes representing international developed and emerging markets. So if stocks in these markets had performed extremely well over the past several years, we might conclude that the prices had already been bid up in response to the fundamentals. But we don’t believe that’s been the case. As Figure 1 shows, international developed and emerging markets have lagged their U.S. counterparts over the past five years and six months.

In light of these circumstances and the opportunities we see, how are we choosing our investments outside the United States? First, even though we’re willing to “pay up” for growth, we’re focusing on high quality in our international and emerging markets strategies.

Second, similar to our U.S. strategies, we favor profitable, industry-leading companies that are generally able to self-fund their growth without much debt and, if possible, without high fixed costs. We believe these companies may be situated to deal with periodic Covid-related challenges relatively well and emerge from the pandemic in reasonably strong competitive positions. We also generally like companies that are focused on domestic economies. We believe these companies may have fewer challenges if the coronavirus disrupts global supply chains and world-wide demand for an extended period.

Third, we’re aware of currency values. Just as U.S. stocks have generally led world exchanges during the past several years, the U.S. dollar has been exceptionally strong. If that currency trend moves the other way, international developed and emerging markets could have an additional wind at their backs. A weaker dollar and recently lower interest rates in the United States could redirect the flow of investor capital—at least to some extent—away from the U.S. and toward international developed and emerging markets. Moreover, a weaker dollar could benefit companies serving their home-country consumers—rather than companies exporting to the United States.

INTERNATIONAL DEVELOPED MARKETS

The Wasatch International Small Cap Growth strategy, as its name implies, invests in growth-oriented small caps located mostly in international developed markets and to a lesser extent in emerging markets. The Wasatch International Select strategy is a high-conviction strategy focused exclusively on developed markets. While we look for companies of any capitalization, we’ve found the sweet spot to be in mid caps. Currently, for both of these strategies, Japan and the United Kingdom are among the most heavily weighted countries—with significant positions in information technology, industrials, health care and consumer names.

Japan is a country we see as being particularly resilient. We believe it has worked steadfastly to emerge from years of relatively slow growth. The government has implemented many shareholder-friendly reforms that have led to better corporate governance and to higher growth rates along with improved ROEs and ROAs for many businesses. Japan is also home to leading companies involved in medical devices, pharmaceuticals and health-care information. In addition, the country has now fully embraced internet-based technologies for a host of industries. And from our vantage point, Japan has one of the most vibrant small-cap marketplaces in the world.

As for the United Kingdom, some observers may find our optimism surprising—especially given the challenges regarding Brexit and the significant impact of Covid-19 on the country. But based on our fundamental research, we’ve invested in several U.K. companies involved in the use of cloud-based software for automation, procurement, communications, entertainment, and the retail and wholesale distribution of goods and services. We’ve also invested in companies making cutting-edge industrial products and components used for manufacturing, business construction and homebuilding. In addition, our U.K. holdings include innovative medical-device and health-care-research companies and specialty retailers with interesting competitive advantages.

While Australia isn’t always a large weighting in our strategies, we like the country’s entrepreneurial spirit. Our current holdings include a scientific-research company that develops and markets medical implants. We also hold Australian companies that are delivering software solutions online and companies that are enhancing sales and marketing efforts with internet-based tools.

EMERGING MARKETS

The Wasatch Emerging Markets Small Cap strategy invests almost exclusively in small caps located in emerging markets. The Wasatch Emerging Markets Select strategy invests in fewer stocks, often in the mid- to large-cap range. These two strategies have significant investments in India, Taiwan and Brazil—with sizable positions in information technology, financials, industrials and consumer names.

Although stay-at-home measures to contain the spread of Covid-19 in India have been among the world’s strictest and have tempered economic growth temporarily, India remains our most favored emerging market for the long term. We believe the Indian economy has tremendous room for expansion and will continue to benefit from a virtuous circle of progress based on digitalization, financialization and formalization. This virtuous circle, which we’ve written about extensively, is supported by India’s relatively young population and the embrace of technology, transparency and the rule of law.

Moreover, because India imports approximately 80% of the oil it uses, Brent crude’s significant decline this year should help to improve the nation’s current-account balance, support its currency and keep inflation in check. Easing inflationary pressures and increased currency stability may also give India’s policy makers additional scope to stimulate the country’s economy.

Taiwan is home to some of our strongest-performing companies recently. Our Taiwanese investments include a manufacturer of high-performance mixed-signal and analog integrated circuits used in a wide array of electronic devices. We also hold a fabless designer of integrated circuits specializing in areas that include server management and audio-visual extensions. Both companies have benefited as businesses and individuals around the world have increased their use of online platforms and data transfers amid the coronavirus pandemic.

Regarding Brazil, we have investments in a pharmacy chain, a provider of medical and dental care, and an online platform for businesses and individuals in Latin America to buy and sell a wide variety of products. While Brazil continues to face political uncertainty, we believe our companies there have world-class management teams and robust business models. In addition to serving large markets for local customers, we think some of our Brazilian companies have strong demand from other countries—without being overly dependent on the United States.

ADDITIONAL INFORMATION

In closing, we’d like to emphasize that Wasatch got its start in U.S. small- and micro-cap investing by focusing on high-quality companies generally with healthy, low-debt balance sheets. We’ve always looked for great management teams that we believe are able to grow sales and earnings at rates significantly better than the growth rates for companies in the benchmark indexes. This same focus guides us in managing our international and emerging markets strategies.

Currently, as described above, we favor companies that are generally focused on their home countries. We think these companies may be less vulnerable to business disruptions if Covid-19 lingers around the world longer than expected.

With sincere thanks for your continuing investment and for your trust,

Ajay Krishnan, CFA Portfolio Manager

Ken Applegate, CFA, CMT Portfolio Manager

CFA® is a trademark owned by the CFA Institute.

RISKS AND DISCLOSURES

Mutual-fund investing involves risks, and the loss of principal is possible. Investing in small-cap and micro-cap funds will be more volatile, and the loss of principal could be greater, than investing in large-cap or more diversified funds. Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets, and political and social instability, which are described in more detail in the prospectus.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit wasatchglobal.com or call 800.551.1700. Please read the prospectus carefully before investing.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

Wasatch Global Investors is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Global Investors.

DEFINITIONS

Beta is a quantitative measure of the volatility of a given stock relative to the overall market. A beta above one is more volatile than the overall market, while a beta below one is less volatile.

Brexit is an abbreviation for “British exit,” which refers to the June 23, 2016 referendum whereby British citizens voted to exit the European Union. The referendum roiled global markets, including currencies, causing the British pound to fall to its lowest level in decades.

The “cloud” is the internet. Cloud-computing is a model for delivering information-technology services in which resources are retrieved from the internet through web-based tools and applications, rather than from a direct connection to a server.

Earnings per share or EPS is the portion of a company’s profit allocated to each outstanding share of common stock. EPS growth rates help investors identify companies that are increasing or decreasing in profitability.

EBIT (earnings before interest and taxes) is a measure of a firm’s profit that includes all expenses except interest and income tax expenses. It is the difference between operating revenues and operating expenses. EBIT is also called “operating earnings,” “operating profit,” or “operating income.” EBIT ROA is the ratio of EBIT to the total capital invested in operating assets.

Long-term debt to capital is a company’s debt as a percentage of its total capital. Debt includes all short-term and long-term obligations. Total capital includes the company’s debt and shareholders’ equity, which includes common stock, preferred stock, minority interest and net debt.

The MSCI AC (All Country) World ex USA Small Cap Index is an unmanaged index and includes reinvestment of all dividends of issuers located in countries throughout the world representing developed and emerging markets, excluding securities of U.S. issuers. This index is a free float-adjusted market capitalization index designed to measure the performance of small capitalization securities. You cannot invest directly in an index.

The MSCI EAFE Index is an equity index which captures large- and mid-cap representation across 21 developed-market countries around the world, excluding the United States and Canada. With 902 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization in each country. You cannot invest directly in an index.

The MSCI Emerging Markets Index captures large- and mid-cap representation across 26 emerging-market countries. With 1,385 constituents, the Index covers approximately 85% of the free float-adjusted market capitalization in each country. You cannot invest directly in an index.

The MSCI Emerging Markets Small Cap Index includes small cap representation across 26 emerging-market countries. With 1,641 constituents, the Index covers approximately 14% of the free float-adjusted market capitalization in each country. You cannot invest directly in an index.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non-in-fringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, with-out limitation, lost profits) or any other damages. (www.msci.com)

The price/earnings (P/E) ratio, also known as the P/E multiple, is the price of a stock divided by its earnings per share.

Return on assets (ROA) measures a company’s profitability by showing how many dollars of earnings a company derives from each dollar of assets it controls.

Return on equity (ROE) measures a company’s efficiency at generating profits from shareholders’ equity.

The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index. The Russell 2000 is widely used in the industry to measure the performance of small company stocks. The Russell 3000 Index seeks to track the entire U.S. stock market. You cannot invest directly in an index.

The Wasatch strategies have been developed solely by Wasatch Global Investors. The Wasatch strategies are not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the Russell 3000 and Russell 2000 indexes vest in the relevant LSE Group company, which owns these indexes. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license.

These indexes are calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in these indexes or (b) investment in or operation of the Wasatch strategies or the suitability of these indexes for the purpose to which they are being put by Wasatch Global Investors.

The S&P 500 Index includes 500 of the United States’ largest stocks from a broad variety of industries. The Index is unmanaged and is a commonly used measure of common stock total return performance. You cannot invest directly in an index.

©2020 Wasatch Global Investors

Wasatch Funds are distributed by ALPS Distributors, Inc. Separately managed accounts and related investment advisory services are provided by Wasatch Global Investors, a federally registered investment advisor. ALPS Distributors, Inc., is not affiliated with Wasatch Global Investors.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits