The economic calendar is modest, and many market participants will probably extend their long weekends. The ISM Non-Manufacturing Index and jobless claims data will be the most important.

Credit for today’s theme goes to Satchel Paige, one of the greatest pitchers of all time.

Don’t look back; something might be gaining on you.

Picture Courtesy of Simpson Street Free Press, where you will also find a nice article by Patricia Cazares, age 13.

Last Week Recap

In my last installment of WTWA, I described the fragile state of the economic recovery and asked whether it could be sustained. Bloomberg apparently thinks that I was on the right track, since they ran this story on June 29th: Coronavirus Resurgence Threatens Fragile U.S. Economic Recovery. Check it out and compare the information from the three article authors with WTWA!

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Investing.com’s version. This is just the static chart, but a visit to the post will enable you to explore the news callouts and much more.

The market ignored record numbers of new COVID-19 cases to post a strong week. The market gained 4.0% with a trading range of 5.5%. My weekly indicator snapshot monitors the actual volatility as well as the VIX (see below).

Noteworthy

Statista tracks the current stall in state reopenings.

In my new home state of Arizona, we face possible new restrictions from Sonora. Health officials there want to restrict border crossings from our COVID hot spot into Mexico.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators have always been a valuable part of my economic review. They are especially important as we all try to monitor the economic recovery. His three time frames all show some improvement – positive in the long-term, newly positive in the short-term, and “less awful” in the nowcast. NDD remains cautious about the willingness of people to accept growing cases in the pandemic.

The Good

Pending home sales registered a blowout gain of 44.3% versus expectations of 18.0% and April’s -21.8%. (Calculated Risk).

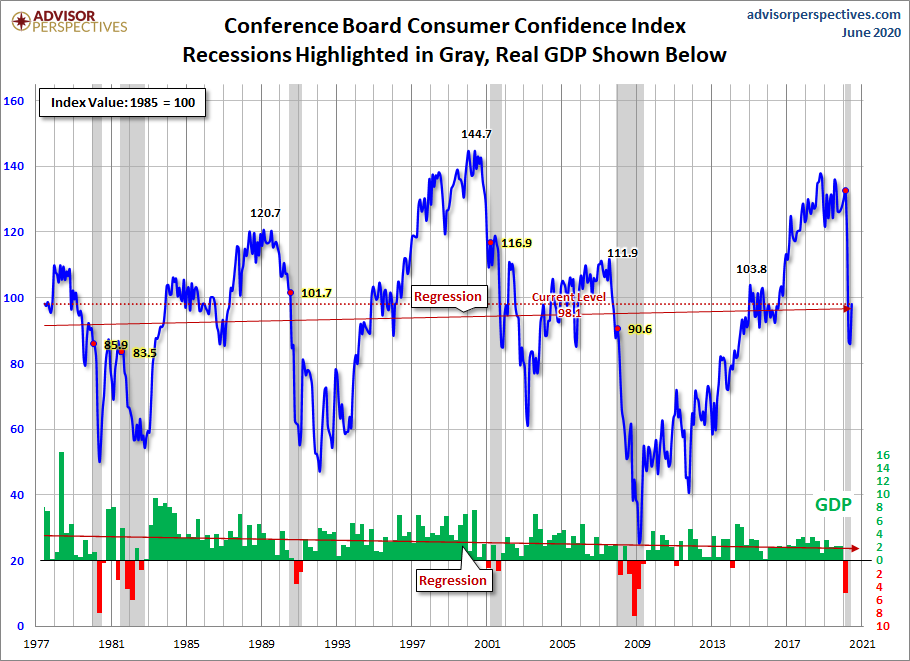

Consumer confidence for June came in at 98.1, beating expectations of 92.0 and last month’s 85.9. As always, Jill Mislinski has excellent coverage of this indicator as well as the best chart.

The ISM Manufacturing Index for June registered 52.6, beating estimates of 49.2 and May’s 43.1.

Factory orders for May increased 8.0%, better than expectations of 7.2% and much better than April’s 13.5% decline.

More fiscal stimulus is coming – at a cost, of course.

The Employment situation report for June showed a net increase of 4.8M jobs, much better than the expected 3.5M and May’s 2.7M.

Unemployment declined to 11.1%, better than the expected 12.6% and last month’s 13.3%. The news looked very good, although some cautioned that the rebound still has far to go. Others wondered whether current slowing in the reopening might have an effect next month. This chart is interesting.

The Bad

MBA Mortgage Applications declined 1.8%, but still look very healthy.

Construction spending for May declined 2.1% missing expectations of a 1.1% gain but better than April’s 3.5% decline.

Initial jobless claims registered 1.427M, higher than the expected 1.355M. Continuing claims were about the same at 19.29M.

ADP’s private employment change was an increase of 2.369M versus expectations of 3.75M. May’s report was adjusted upward by over 5.8M jobs.

Most states are constitutionally prevented from running budget deficits.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

We have a very light economic calendar with many, no doubt, extending vacations. Jobless claims continue to be important. The ISM Non-Manufacturing Index will get attention as will the JOLTS report. Neither can really provide any fresh information. PPI is similarly uninteresting.

There is no calendar for COVID-19 news, but it will compete for attention with the economic data every day.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

The economic news, once again, got better, and pandemic news, once again, got worse. The market rose nicely, reassuring many investors. Instead of looking at the modest economic rebound, investors should be paying attention to Satchel Paige:

Don’t look back; something might be gaining on you.

For many reasons, our attention is currently focused on the “now” and the recent past. How can investors best look forward?

Underlying Factors

There are several important forces creating a challenge for those who do objective analysis.

Questionable Data. In normal times I depend upon economic data and earnings reports to provide a grounding for investment choices. These sources are not very helpful since none of the economic indicators mean much. Those based upon the diffusion method, including the ISM indexes, PMIs, and the various Fed indexes, tell us about the direction of change, but not the size. Survey data is good for a current snapshot but tells us little about prospects. Most other reports are distorted by extreme events related to the pandemic. The agencies creating the reports are doing an honest and unbiased job. Their tools are not geared to the extreme situations we are now seeing. I have studied both the indicators and the methodology for many years, and I do not trust the current results.

Government Intervention. Government actions have changed nearly every indicator. The Fed is active on more of the yield curve. People have income without jobs while others have jobs but low income. Special purpose loans are helping particular recipients and sectors. This is not a judgement on the wisdom of the policies. It is a factual statement emphasizing the impact on data.

Psychological Traits. Many of the most powerful are currently in evidence, creating a witch’s brew for trouble.

Collective action. Collective goods (e.g. police, national defense, education) are underfunded when dependent upon contributions. At the moment we are reliant upon voluntary cooperation to halt the spread of COVID-19.

Counterfactuals. People readily see and believe what is in front of them. They are not good at imagining what would have happened if circumstances were different. Progress has been made in many places at reducing the COVID-19 spread. Would the same progress have occurred without restrictions on movement and behavior?

First-order impacts. People believe what they can see. This is why a dramatic video sways public sentiment more than years of analysis backed by data. When we see people socializing in bars or on the beach, it is tempting to think that all is well. Determining the effects of this behavior is challenging and usually ignored.

Confirmation bias. This is the strongest of the behavioral economics effects. It affects what we see, whom we believe, and how we interpret evidence. It also affects the experts who have “skin in the game” for economic, political, or reputational reasons.

Facts and sources. Experts often disagree. Highlighting the areas of dispute puts a shadow on findings that represent a broad consensus. Many of the most popular sources disseminate misleading information, often taking quotations out of context.

These factors interact. Why would I help someone else avoid disease if experts say it is not that dangerous? Why should I make sacrifices to fight an exaggerated public threat? Since there are significant measurement problems in identifying cases and effects, why should I believe any reported data? And why would I ever believe a model?

These effects have been fueled by a populist wave that disparages expertise of all types. We are apparently destined to learn in real time whether this particular group of experts was right.

The Result?

Stock values, the knowledge desired by many, are at the top of a pyramid. The foundation layer is expected earnings. The foundation for earnings is the economy.

Now there is a new element to the foundation – the fight against COVID-19. The economic effects will be severe if the virus spreads aggressively but can be significant even if it does not. Governments are already slowing reopening plans.

Even when businesses reopen, some customers will choose not to go.

Those dismissing the pandemic effects as unimportant are underestimating these key relationships.

As usual, I will have a little more in today’s Final Thought.

Ideas for Investors

I have decided to switch the investor section to a separate post. I hope to run it nearly every week, calling it Investing for the Long Term. In the latest edition I expanded my matrix approach for finding long-term value drawn from our most recent Wisdom of Crowds survey. As usual I linked to several of my favorite sources for investment ideas. In each case I added a comment about how I might use the idea and also related it to our Great Reset results. I hope readers will find this valuable and that my colleagues will consider the Great Reset Matrix as part of their selection process.

One of my personal 2020 resolutions was even more emphasis on investor education – not just recommending stocks but learning how to find suitable choices. I have created a resource page where you can join my Great Reset group. You will get updates about what is being studied and can join in the process. There is no charge and no obligation, but I hope you will join in my Wisdom of Crowds surveys. I need more wise participants! The latest survey results are part of my most recent report. The results of our team effort will be published on a regular basis, so you will be joining me in contributing to a greater good.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

The C-Score remains at levels never before seen. It is combining the sharp economic rebound with pandemic effects. When we are able to separate the two, a current mission of Dr. Dieli, it will provide more guidance on the timing and extent of the recovery. I continue my rating of “Bearish” in the overall outlook for long-term investors. We should also keep watch an inflation antcipation. As this increases it affects government policy and our portfolio construction needs.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

David Moenning: Developer and “keeper” of the Indicator Wall.

Doug Short and Jill Mislinski: Regular updating of an array of indicators, including the very helpful Big Four.

Georg Vrba: Business cycle indicator and market timing tools.

Final Thought

One important issue is whether the public is emphasizing health concerns over the economy. This basic concept will be part of my next Great Reset survey.

Regardless of current attitudes, opinion on this topic will shift as we see more data.

I am concerned – for family, friends, and my readers. It is so easy to become too carefree, and we all want to get out and have fun.

I urge you to stay safe in your socializing and to be sure that your portfolio is safe as well.

I’m more worried about

Lack of progress in seeking a balanced solution to the crisis. There is so much polarization, that finding a process for a safe reopening is getting lost.

I’m less worried about

The election. Stories are popping up about economic and market threats from the election. I do not anticipate any outcome that would instantly alter economic prospects, but some are concerned.