Responsible Investing in a Traditional Asset Class

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn the municipal bond market, the issuance of green bonds has provided an attractive solution for investors interested in socially responsible investments while also receiving the tax-exempt income benefit municipal bonds offer. Franklin Templeton’s Municipal Bond team provides an overview of green bonds, including potential benefits and risk considerations.

In November 2008, the World Bank issued the first ever bond that carried the label ”green.”1 This marked the inception of the global green bond market—a market that is now over a decade old. In that bond issue, the World Bank defined its criteria for eligible green bond projects and provided a second party opinion to assure investors the proceeds would address climate change.2

Since 2008, green bonds and climate-aligned bonds have become a growing subset of the global fixed income markets. These bonds are distinguished by their use of proceeds, which must be deployed in a manner consistent with environmental sustainability.

Examples of projects funded by green bonds include investment in infrastructure for water and wastewater systems, renewable energy assets, and Leadership in Energy and Environment Design (LEED) certified buildings. The environmental benefits of such projects include water use efficiency, a reduction in carbon emissions and energy efficiency.

For investors, green bonds provide an opportunity to dedicate capital to projects and programs that have a defined environmental purpose.

Globally, green bond issuers include for-profit corporations and other private enterprises, supranational organizations such as the International Monetary Fund, governments and quasi-sovereign issuers. In the United States, state and local entities, as well as not-for-profit organizations, have increasingly issued green bonds to finance environmentally friendly projects and programs.

The universe of municipal green bond issuers in the United States includes states, cities, municipal water and sewer enterprises, transportation systems, universities, and hospitals, among others. As a result, some municipal green bonds are issued as general obligation bonds, while others are classified as revenue bonds. Green bonds have the same bondholder security features from the issuers as their non-green counterparts.

Similarly, municipal green bonds enjoy the same tax-exempt status as traditional municipal bonds. As a result, environmentally conscious investors have the opportunity to invest in projects that promote environmental sustainability without sacrificing the tax exemption.

Green bonds include sustainability bonds, climate bonds and environmental impact bonds. All three categories are defined by their use of proceeds. Borrowers have a duty to demonstrate that proceeds from issuance of a green bond are used appropriately. Some green bond issuers hire independent parties to verify that proceeds are used for their stated purposes, and all climate bonds require independent verification. We will take a closer look at standards of issuance and verification later in this paper.

Issuance and Market Structure

The Commonwealth of Massachusetts became the first issuer of municipal green bonds by issuing $100 million of green bonds in June of 2013. Issuance has steadily increased since that time, both in terms of the number of issuers and principal amount outstanding. In 2017, gross issuance increased by over 40% from the prior year. What began as a small group of issuers has expanded into a broad collection of municipal entities spanning multiple sectors and geographic regions.

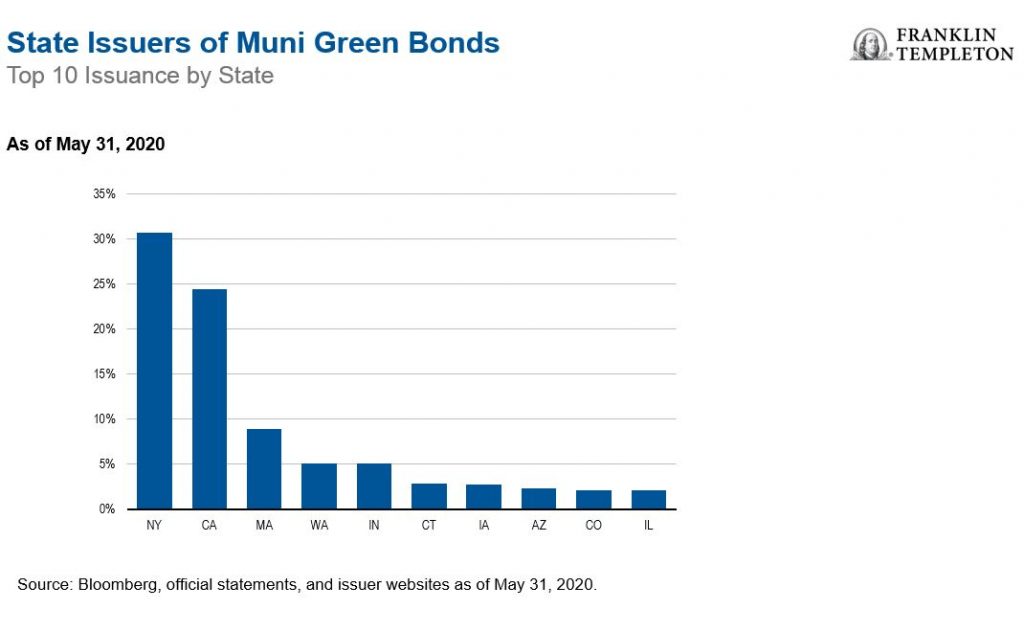

The market for municipal green bonds has continued to grow. As of May 31, 2020, there were over 175 unique issuers of municipal green bonds across 36 US states. The total principal amount issued was $39 billion. Although the geographic reach of municipal green bonds continues to grow, the top 10 states, based on issuance, make up 85% of all outstanding bonds. New York and California are the largest issuers with 31% and 24% of the market, respectively. However, green bonds still represent a small portion of the overall municipal bond market.

While gross issuance remains small relative to the overall municipal bond market, the range of issuers is broad and diverse. There has been at least one green bond issued from 16 different sectors. To date, public, transportation and water-sewer related entities have dominated issuance: combined these two sectors account for over 50% of the market. Increasingly, state-affiliated loan pools are a common issuer of municipal green bonds.

Overall, this growing universe of municipal green bonds allows for the ability to manage a dedicated portfolio in this space.

Analogous to the broader municipal market, green bonds tend to carry relatively long maturities compared to other fixed income sectors. Just as most municipal issuers are generally assumed to exist in perpetuity, environmental initiatives and projects also carry long-term time horizons. As a result, the average maturity of all outstanding municipal green bonds is greater than 15 years.

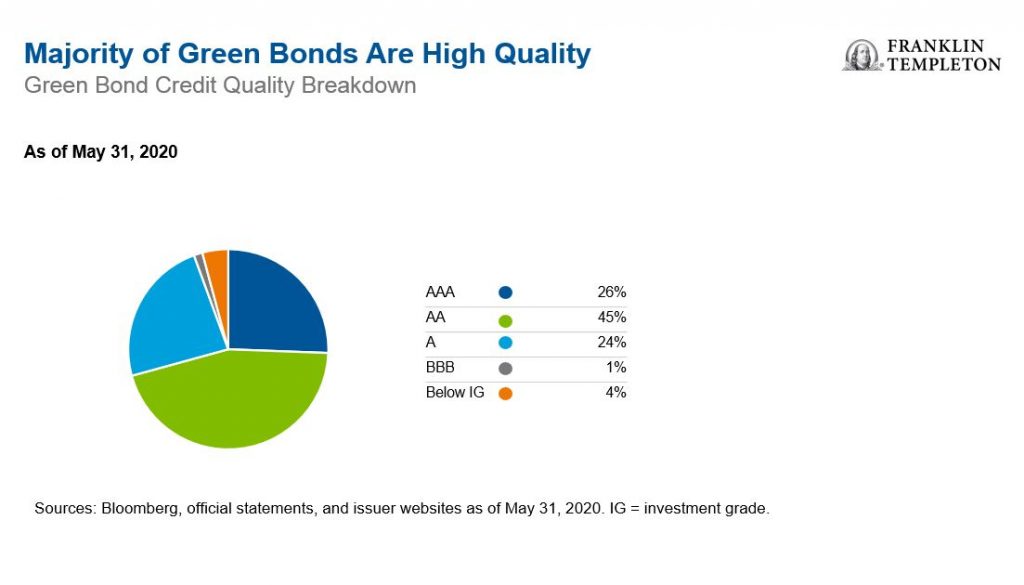

The credit quality of municipal green bonds is also reflective of the broader market. As of May 2020, 71% of outstanding green bonds were rated AAA or AA by Standard & Poor’s, Moody’s or Fitch. By dollar volume, over 95% of supply-to-date has carried investment-grade credit ratings. That said, several non-rated green bond deals offer compelling opportunities for high impact investments. Examples of non-rated green bonds include waste-to-energy and land restoration projects, among others.

The municipal green bond market is young and continues to evolve. Importantly, the number of unique issuers continues to grow. Smaller issuers are increasingly considering green bonds as a potential source of funds. This expanding pool of borrowers allows dedicated green bond investment portfolios to achieve diversification across sectors and issuers.

Municipal Green Bond Examples

In the state of Washington, the Department of Ecology found that the transportation sector is responsible for the majority of the region’s greenhouse gas emissions. The Central Puget Sound Regional Transit Authority (“Sound Transit”) provides rail and bus systems serving the greater Seattle area and is a large issuer of green bonds. Through its Environmental and Sustainability Management Program—financed by green bonds—Sound Transit has made several key accomplishments, including reductions in greenhouse gas emissions, air pollutants, and overall energy use, with a significant increase in renewable energy inputs.3

The largest issuer of green bonds in the United States is the Metropolitan Transportation Authority (MTA) of New York City. The public transportation system most famous for operating New York City’s subway system has engaged the Climate Bond Initiative to certify $11.3 billion of its $24 billion capital program—funding nearly half of its capital investments with green bonds. By only using the green label on bonds that fund environmentally friendly initiatives, the MTA bolsters its credibility as an issuer of green bonds. These bonds are certified pursuant to the Low Carbon Transport Criteria under the Climate Bonds Standard 2.0. This standard provides a scientific framework for determining which projects and assets are consistent with a low carbon and climate resilient economy.

Green Bond Verification

Green bonds are not regulated as a class and their designation is voluntary. As of this writing, there is no legislative body, either domestically or internationally, governing what “green” means—only voluntary standards. This presents the risk of issuers misleading investors by making false claims about the use of proceeds or the management of their proceeds.

Issuers employ a variety of practices to disclose the use of proceeds and describe targeted projects and programs. Some issuers do not provide any meaningful description of the projects or programs funded with green bonds; others hire independent parties to verify that proceeds are used for environmentally friendly purposes. The absence of standard green bond disclosure practices represents an additional challenge to investors. It also highlights the importance of having a thorough process dedicated to identifying authentic green bonds from those issuers that attempt to “greenwash” an issuance by inappropriately self-labeling their bonds as green.

To address the issue of disjointed disclosure practices across issuers, some voluntary organizations have created frameworks for issuing green bonds. The International Capital Market Association (ICMA) publishes the Green Bond Principles (GBP), which classifies environmentally friendly projects and programs, and directs issuers to adopt adequate disclosure practices. The ICMA also publishes the Social Bond Principles (SBP); Sustainability Bonds adopt both the GBP and SBP.

The GBP are generally considered to be the most widely accepted framework for municipal green bond issuance and disclosure. The GBP outline a framework for green bond issuance—the so-called “Four Pillars” of green bond underwriting—as well as 10 eligible use-of-proceeds categories. The Four Pillars are: Use of Proceeds; Process for Project Evaluation and Selection; Management of Proceeds; and Reporting.

Drafted by a consortium of capital markets participants, the GBP do not represent a commercial certification, but rather a framework for green bond issuance available for all interested parties: issuers, underwriters, and investors alike.

In the absence of any centralized regulatory oversight governing green bonds, the GBP have emerged as the authority for green bond issuance within US public finance (as well as in Europe). They serve as a critical form of guidance to help standardize a nascent and growing sector of the international green bond markets.

The Climate Bond Initiative oversees a program through which issuers can sell climate bonds. The Climate Bond Initiative is an independent, international organization committed to promoting a low carbon and climate resilient economy. Climate bond certification requires independent verification that bond proceeds are deployed in a manner consistent with this mission. The CBI is aligned with the Green Bond Principles, and we consider all climate bonds to be part of the broader green bond universe.

Franklin Templeton’s Approach to Evaluating Green Bonds

To address the lack of standards in the municipal green bond market, our research analysts and portfolio managers work together to identify and select authentic green bonds and discard bonds that use the “green bond” label inappropriately or provide inadequate disclosure. Franklin screens all green bonds, sustainability bonds, and climate bonds. In the absence of an official designation, research analysts and portfolio managers can also nominate bonds that have not received any of these labels.

The portfolio managers leverage the large and tenured team of research analysts dedicated to municipal bond analysis to identify authentic green bonds. Municipal bonds are riddled with nuance, a fact that necessitates a deep and experienced team of analysts to portfolio managers to assess the intent and authenticity of an issuer. To aid in that effort, we directly contact the issuers, and often will engage them on various issues related to their green bond program.

The due diligence process for identifying authentic green bonds primarily focuses on the intended use of funds for projects or programs. In our process, we ask a series of questions to help guide our decision-making. In answering these questions, we review offering documents, issuer websites, and other sources of information to verify that the projects or programs in question are adequately described.

Fundamentally, projects being funded with green bonds must align with at least one GBP category. In addition, green bonds without an adequate description of the respective projects are not considered for investment in our green bond strategies. Franklin encourages all green bond issuers to adopt the GBP.

However, alignment with the GBP does not ensure that a bond will be deemed suitable for green bond strategies, and failure to adopt the GBP does not preclude a bond from being purchased in these strategies. We rely on our independent analysis to determine which bonds are suitable for inclusion in our green strategies.

In addition to examining all publicly available information, we often interact with borrowers, bankers, financial advisors and other parties to determine if the projects and programs are intended to generate authentic environmental benefits. In cases where the issuer demonstrates a quantifiable, positive environmental impact, the determination is straightforward. In other cases, we must make the determination based on qualitative factors. To help make this determination, we attempt to answer the following questions:

- Do the projects and programs have clear environmental benefits?

- Do the projects and programs promote sustainability or climate resiliency?

- Does the borrower have a clear sustainability and/or climate resiliency program?

- Has the borrower engaged an independent party to verify that its projects and programs are green?

After all due diligence is complete, green bonds will be placed in one of the following three categories: Not eligible for investment in municipal green bond strategies; Eligible for investment in municipal green bond strategies based exclusively on an internal evaluation of the bond and the borrower; or Eligible for investment in municipal green bond strategies based on an internal evaluation of the bond and the borrower, as well as an external evaluation by an independent party.

We will also conduct ongoing surveillance on all green bonds held in green bond strategies to verify that the proceeds were used for environmentally friendly projects and programs. If an issuer fails to use proceeds as prescribed in its offering documents, or if continuing disclosure is inadequate, we can change the categorization of the corresponding green bonds and attempt to sell them.

Credit Research and Environmental, Social and Governance (ESG) Integration

Green bond strategies leverage the same fundamental, bottom-up research analysis employed by all strategies in Franklin Templeton’s Municipal Bond Department. Each targeted green bond investment is subject to internal credit approval. The research team is organized by sector groups, and there is at least one research analyst covering every sector of the municipal market. Due to the fragmented nature of the market, each sector has its own distinct criteria—both quantitative and qualitative—that analysts use to evaluate the creditworthiness of a given issuer.

As a signatory to the Principles for Responsible Investment (PRI),4 Franklin Templeton has made a firm-wide commitment to integrating an analysis of ESG factors into our core investment process across all investment teams and asset classes. Our Municipal Bond Department has responded by instituting a multi-pronged approach to ESG analysis for every credit we review. For investors seeking to align long-term investment goals with their social values, we believe green bonds offer a compelling solution.

Important Legal Information

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the US by other FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com-Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in lower-rated bonds include higher risk of default and loss of principal. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Municipal bonds are debt securities issued by state and local governments and are generally exempt from federal income tax and also from state and local taxes for residents in the state where the bond was issued. They typically offer income, rather than capital appreciation potential. Corporate bonds are issued by corporations. Bonds with lower ratings and higher credit risk (risk of default) typically offer higher interest rates to compensate investors for the higher risk associated with the investment.

Diversification does not guarantee profit nor protect against the risk of loss.

1. Source: The World Bank, November 2018.

2. Ibid.

3. Source: The Central Puget Sound Regional Transit Authority (Sound Transit), 2016 Green Bond Annual Report.

4. Source: Principles for Responsible Investment (PRI). A consortium of global investment managers and an affiliate of the United Nations. The PRI “works to understand the investment implications of environmental, social and governance (ESG) factors and to support its international network of invest or signatories in incorporating these factors into their investment and ownership decisions.”

© Franklin Templeton Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits