The disruptions of the coronavirus pandemic have hurt small-caps stocks, badly, having fallen more than large-cap stocks. This is not surprising since in the early stages of previous bear markets, small-cap earnings also suffered more on average than their larger siblings.

In the wake of low returns and high volatility, investors may feel compelled to avoid this market. But history suggests they could pay a harsh price if they do. Now is the time to take a hard look at small caps: when assets deliver returns at the low end of the historical range, opportunity may be knocking.

We see great opportunities for active managers to identify differentiating factors and position their portfolios to emphasize the likely winners among small cap stocks.

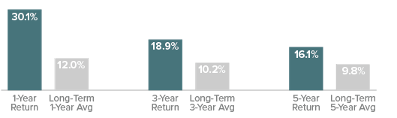

Over the past three years, through the end of April 2020, small-cap stocks posted a modestly negative average annualized return of -0.8%. Negative returns are very rare, occurring in only 49 of 449 (about 10%) of all month-end periods since the Russell 2000 Index’s inception in 1978.

Investors might react adversely to negative returns, yet history suggests exactly the opposite. Performance following three-year negative return periods instead has been unusually strong:

Average Returns Following Negative Russell 2000 3-Year Return Periods vs. Long-Term Averages, from 12/31/78 through 4/30/20. Past performance is no guarantee of future results.

But investors’ risk aversion understandably rises during market storms. Volatility (the VIX) is a useful measure of the intensity of these storms. For April 2020, the daily VIX averaged 41.5% – a remarkably high level, in the highest 10% of all months since the VIX’s inception in 1989.

Following periods of high volatility, small caps often produce high returns: from 1Q 1990 through 3Q 2020, the average one-year return was 28.5%, and the average annualized three-year return was 17.4%. Small caps also tend to bounce back higher after highly volatile periods, beating large caps in 70% of subsequent one-year periods, and 81% of three-year periods.

The world’s economies will recover at different speeds based on their fundamental strengths, how well they were positioned to benefit from secular trends, their cyclical momentum coming into this recession, and the monetary and fiscal steps their governments have taken and will take.

Companies also will vary in their recoveries due to comparable factors, including the steps their managements have been taking in the downturn. Positive and negative investment trends can persist for a while, but they always reverse. Investors should try to position their portfolios now to benefit from these reversals. This is not easy, but we believe a reversal period has begun.

The bulk of the best opportunities are “B2B” rather than consumer facing. Semiconductor and semiconductor equipment companies are good examples, along with related component and device makers, especially those in mobile or communications technology. Many of these stocks have done relatively well through the market’s volatile swings, and they have positive outlooks.

Supply chain and logistics infrastructure businesses also show strength. Widespread disruptions are forcing many companies to reexamine, migrate and invest in their global supply chains. The beneficiaries include suppliers of warehouse and supply chain management software that help businesses rework and efficiently manage their logistics.

Because balance sheet stress is causing many companies to refinance and perhaps even rethink their futures, corporate financial advisory firms with restructuring expertise are also ticking up.

Recreational companies are benefiting from surges in physical-distancing outdoor activities. Consumers are planning alternate vacations or getaways that do not require flying, fueling solid demand for boats and recreational vehicles, and enhancing the stocks of these dealers.

Consumer discretionary areas have been among the hardest hit during the decline and may have the longest roads back: hotels and restaurants & leisure. A third area, specialty retail, was already facing seismic changes when the virus broke out. These are generally not the best opportunities.

Areas that have delivered subpar returns may prove attractive places to look for future returns. So it is with small cap equities in this moment – if investors choose the right stocks.

IMPORTANT INFORMATION

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, guarantee of future results, recommendations or advice. Statements made in this material are not intended as buy or sell recommendations of any securities. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. Information and opinions expressed by either Legg Mason or its affiliates are current as at the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors.

© 2020 Legg Mason Investor Services, LLC. Member FINRA, SIPC. Legg Mason Investor Services, LLC, and Royce Investment Partners are subsidiaries of Legg Mason, Inc.

Read more commentaries by Royce Investment Partners