As the economy reopens from COVID-19 restrictions, a question looms: What will colleges and universities look like come fall? Will students return to a more normal on-campus learning experience, some form of online experience, a combination of both … or will they simply not return? The question is important to municipal bond investors because the education sector accounts for roughly 7% of the investment-grade muni market.

We believe the core of a well-built muni portfolio should consist primarily of general obligation bonds and essential-service revenue bonds. However, for investors who wish to expand their municipal portfolios, another area to consider is higher-education revenue bonds, or bonds that are issued by public or private universities or colleges. But don’t consider just any university or college, especially in a COVID-19 world.

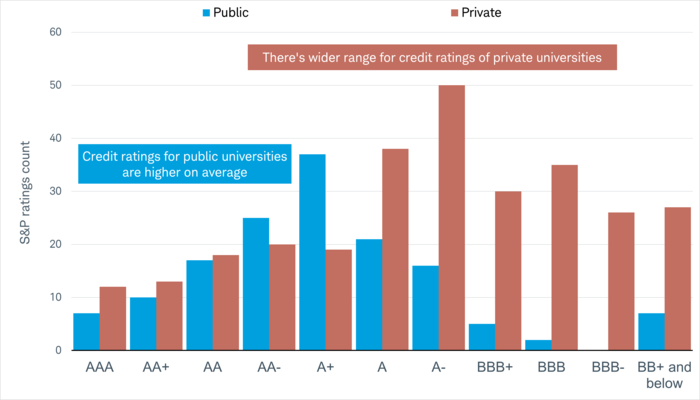

Public institutions, on average, tend to have higher credit ratings than private schools

Not-for-profit higher education bonds come in two major flavors: public and private institutions. Colleges and universities, both public and private, are generally not-for-profit enterprises. As such, interest paid on their bonds is generally exempt from federal income taxes, as well as state income taxes if the bonds are issued in the investor’s home state. From a credit ratings perspective, an issuer can be a standalone school or an entire system, such as the University of California or the University of Texas systems.

Overall the sector is very highly rated, but it’s somewhat bifurcated based on private or public institutions and size. On average, private institutions tend to have lower credit ratings compared to public institutions. But the range in credit quality for private institutions is wider, as illustrated in the chart below. Public institutions tend to have higher credit ratings, on average, because they benefit from state support and generally have economies of scale. The higher-rated private schools tend to be those that are highly selective and household names—like many of the Ivy League schools.

Public university ratings are more clustered compared to private universities

Source: Standard and Poor’s, as of 1/16/2020. For illustrative purposes only; some ratings may have changed since the publication date of the report.

More in-demand schools should have greater flexibility going forward

From a credit perspective, demand is one of the major factors that distinguishes stronger higher-education issuers from weaker ones. The stronger the demand, the stronger the institution’s bond credit quality. This isn’t always the case, of course, but high demand means more flexibility to manage through the issues posed by the coronavirus.

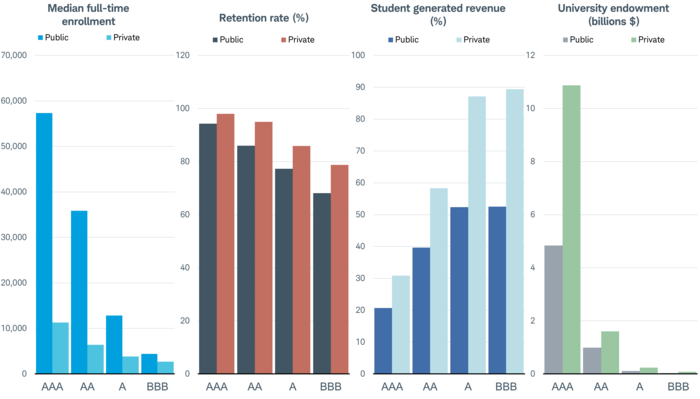

Demand is especially important when looking at private schools, because they generate a larger portion of their revenues from tuition relative to public schools. For example, public universities receive roughly 22% of their revenues from state appropriations and 48% from student-generated revenue. This compares to private schools, which receive 85% of their revenue from students, on average.1

Endowment size tends to be highly correlated with the quality of a university’s bonds, as well. The rules of how much and when a school can draw from its endowment varies, but it usually serves as an important source of financial support in times of economic disruption.

The charts below show that more highly rated institutions tend to have larger student populations and higher student selectivity, which are signs of greater demand and usually larger endowments.

Higher-rated institutions tend to have a larger student population, greater retention rates, larger endowments, and are less dependent on student revenues

Source: Standard and Poor’s, as of 6/25/2019

The coronavirus has the potential to disrupt the sector

Just a few short months ago the term “social distancing” wasn’t common vocabulary and wearing masks in public was extremely rare. Given the higher-education sector’s reliance on large groups of students, the coronavirus will disrupt the sector in the short term and has the potential to alter it in the longer term. Here are some factors that we’re watching going forward:

-

Which schools return to an on-campus learning environment? The general trend for schools is to have students return sometime in the fall and either end the semester early at Thanksgiving or move to an online-learning format. Roughly two-thirds of schools surveyed said they were planning for in-person learning this fall, according to the Chronicle of Higher Education. Eight percent are planning for online, whereas the rest are either waiting to decide, considering a range of options, or proposing a hybrid model of both online and in-person.

-

Will students take a gap year or something similar? The value proposition of a four-year in-person degree is about more than just academics, in our opinion. Many college students are now facing the difficult dilemma of choosing between returning to an environment that may not be the traditional college experience or waiting a year or two before it returns to some form of normalcy. This will be a case-by-case decision for students. However, in an informal poll conducted by Standard and Poor’s, over half the respondents said they expect at least 10% of students will skip fall 2020. This will be more disruptive financially for smaller schools that are more financially dependent.

-

Will states reduce aid to colleges? Forty-nine states have to operate under a balanced budget requirement—meaning that revenues have to match expenses. This is unlike the federal government. According to the National Conference of State Legislatures, revenues are projected to decline for all states that have reported fiscal 2021 projections. Given the anticipated decline in revenues, states will have to either cut expenses or enact other measures.

-

Is additional federal support coming? The CARES Act allocated $14 billion to “each institution of higher learning” based on a series of formulas. This direct aid is supportive of an issuer’s credit quality and should help recipients better manage through the financial disruptions caused by the coronavirus pandemic. However, there are strings attached. The law requires that most of the aid be used to provide emergency financial aid and grants to students or to help offset the costs associated with remote learning. In addition to the CARES Act, Congress is in talks about another round of aid for state and local government; however this may not be finalized until later this summer or may not come to fruition.

One expense they could choose to cut is funding for higher education systems. In fact, the average state spent 16% less per student in 2017 than in 2008, according to the Center on Budget and Policy Priorities. Schools have to make up the reduction in revenue by either cutting expenses or raising tuition. Higher tuition may cause students to question the value proposition of some more-expensive schools.

-

Will high unemployment lead to an increase in enrollment? It may seem counterintuitive to consider high unemployment a good thing, but enrollment tends to increase during periods of high unemployment as some people seek additional education to improve their job prospects when the economy recovers. The Federal Reserve expects the unemployment rate to stay elevated at 5.5% through 2022, which could mean an increase in enrollment in the near term.

-

How will auxiliary revenue bonds fare? Many colleges and universities issue bonds that are backed by a specific revenue source, such as rent for a housing complex or parking fees. We expect these types of revenue sources to come under pressure if fewer students return to campus in the fall. However, these types of bonds often benefit from financial support from the sponsoring school. We suggest focusing on issuers with greater liquidity and strong support from the sponsoring school if you are investing in these types of bonds.

Putting it all together

From a bondholder’s perspective, we don’t think investors should avoid higher-education issuers due to the risks that the coronavirus crisis poses. We suggest focusing on issuers that have higher demand and greater financial flexibility. This tends to coincide with higher-rated issuers. We expect these issuers will be able to better manage through the disruptions caused by the coronavirus crisis.

1 Standard and Poor's, as of 6/25/2019.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market or economic conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Tax-exempt bonds are not necessarily suitable for all investors. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the alternative minimum tax. Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

All names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0620-09MN)

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab