Want to read more by Nasdaq Dorsey Wright? Visit their Featured Firm page here

In many ways large cap, and especially large cap growth, has dominated the story in 2020. The Nasdaq Composite Index and Nasdaq-100 (NDX) rebounded from the Q1 sell-off to recently reach new all-time highs, and through yesterday’s trading (6/15) the S&P 500 Index (SPX) is down just 5% on the year. One size/style category that has largely flown under the radar is small cap value – small cap value ranks last in ranking size and style categories according to the Nasdaq Dorsey Wright Dynamic Asset Level Investing (DALI) tool. And the iShares Russell 2000 Value ETF (IWN) is down more than 24% year-to-date. However, if we look at the time period since the March 23rd bottom, small cap value is actually the most improved size and style category in DALI rankings having gained 31 buy signals over that period, going from 17 to 48. No other category has gained more than seven signals over the same period.

And while the speed and magnitude of the large cap recovery has garnered most of the attention, the iShares Russell 2000 ETF (IWM) has actually outperformed the SPDR S&P 500 ETF (SPY) since March 23rd, with the two funds gaining 41.13% and 37.72%, respectively. Small cap value isn’t far behind as IWN is up 35.67% over the same period.

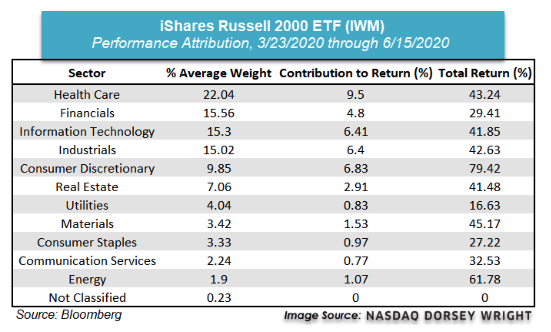

In order to pinpoint which areas within the small cap space have led this improvement, we have taken a look at the performance attribution of the iShares Russell 2000 ETF (IWM) from the market bottom on March 23rd through June 15th. We can see from this breakdown that IWM is overweight healthcare (22%), financials (15%), technology (15%), and industrials (15%), which combine to make up about two-thirds of the total allocation. Healthcare, the largest sector in the portfolio, also accounted for the highest contribution to the total return of IWM during the timeframe examined, making up about 9.5% of the 42.01% gain of the Fund (total return is inclusive of dividends, 3/23 through 6/15). Consumer discretionary saw the second-highest contribution to performance at 6.83% of the return, as the sector is the fifth largest in the Fund but also the best performing on an absolute basis, up over 79%. Communication services saw the least contribution to IWM’s return, just beneath the low contribution of utilities.

Nasdaq Dorsey Wright offers investors a free trial of the NDW Research Platform, which provides turnkey research and analysis for securities selection, portfolio management and asset allocation. Click here for more information. For questions about the NDW strategies, contact us here.

Dorsey, Wright & Associates, LLC, a Nasdaq Company, is a registered investment advisory firm. Registration does not imply any level of skill or training.

Unless otherwise stated, the performance information included in this article does not include all potential transaction costs. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

Nothing contained within the article should be construed as an offer to sell or the solicitation of an offer to buy any security. This article does not attempt to examine all the facts and circumstances which may be relevant to any company, industry or security mentioned herein. We are not soliciting any action based on this article. It is for the general information of and does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any analysis, advice or recommendation (express or implied), investors should consider whether the security or strategy in question is suitable for their particular circumstances and, if necessary, seek professional advice.

Dorsey Wright’s relative strength strategy is not a guarantee. There may be times when all assets are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon to be successful or outperform any index, asset, or strategy.