NewsLetter - June 2020

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAMAZING COUNTRY MUSIC

Even for those who may not be big fans.

SAD BUT NOT SURPRISING

Bankrupt in Just Two Weeks—Individual Investors Get Burned by Collapse of Complex Securities, The Wall Street Journal, 6/1/2020

“When William Mark decided to get back into investing after the 2008 financial crisis, he looked past stocks and bonds. Needing to play catch-up with his retirement portfolio, the piping engineer decided to bet on a complicated product he hoped would deliver double-digit annual returns.

It worked so well—earning him 18% a year in dividends, on average—that he eventually poured $800,000 into the investments, called leveraged exchange-traded notes, or ETNs. When the coronavirus pandemic hit, he lost almost every penny.

‘I’m 67 years old and I’m basically bankrupt in just two weeks,’ Mr. Mark said.” My friend Larry Swedroe, whom I’ve often quoted, hit it on the head:

“Some traders said large asset managers, turned off by the complexity, mixed record, and relatively high fees, hardly ever bought the products.

‘If institutions aren’t buying this, the retail investor shouldn’t be either. Otherwise they’re the sucker at the poker table that doesn’t know it,’ said Larry Swedroe, chief research officer at wealth-management firm Buckingham Wealth Partners. ‘If a product is so complex that you can’t explain it to your partner, then you shouldn’t buy it.’”

PONDERISMS

From my #1 son

- How important does a person have to be before they are considered assassinated instead of just murdered?

- How is it that we put a man on the moon before we figured out it would be a good idea to put wheels on luggage?

- Why is it that people say they "slept like a baby" when babies wake up every two hours?

- Why are you IN a movie, but you are ON TV?

- Why do doctors leave the room while you change? They're going to see you naked anyway.

- Why is "bra" singular and "panties" plural?

- Why do toasters always have a setting that burns the toast to a horrible crisp, which no decent human being would eat?

- Why do the Alphabet song and Twinkle, Twinkle, Little Star have the same tune? Why did you just try singing the two songs above?

- Did you ever notice that when you blow in a dog's face, he gets mad at you, but when you take him for a car ride, he sticks his head out the window?

- How did the man who made the first clock know what time it was?

EQUAL MAY NOT BE EQUAL

“The Problem with All Things Being Equal,” The Wall Street Journal, 3/2013

"The market has a nasty tendency of over relying on the good companies and paying too large a premium [for them] on the tacit assumption that recent success portends long-term future success," says Rob Arnott, CEO of investment firm Research Affiliates LLC.

However, the Journal warned, “Equal-weight indexing has been getting more attention lately. But perhaps it's time investors scaled back their enthusiasm: This niche strategy may not deserve equal billing with traditional index strategies.”

“Cap Weighted Versus Equal Weighted, Which Approach Is Better?” Forbes, 7/18/2016

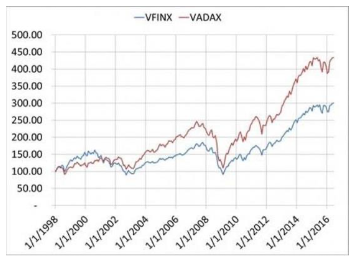

So which approach is better, if there is one? Can we outperform the S&P 500 using the S&P 500, but changing the selection approach? The chart below shows this has been happening.

The blue line is the Vanguard Index 500 Fund (VFINX). The red line is the Invesco Equally Weighted S&P 500 Fund Class A (VADAX). Prices are adjusted for dividends and capital gains. Both prices are set to $100 on Jan. 1, 1998. The graph ends on June 30, 2016. VADAX ended at $440, while VFINX ended at $305. This is even more remarkable given the much lower internal costs at Vanguard.

In March, the S&P Dow Jones Indices Dashboard published an update of the U.S. Equal Weigh

Index versus the traditional S&P Index. The S&P 500 Equal Weight Index underperformed the S&P 500 by 0.8% during February and by 6.8% over the past 12 months.

S&P DJI Commentary [email protected]

A MILLION DOLLARS DOESN’T GO VERY FAR THESE DAYS

From a MarketWatch story, “Here’s how long retirees can afford to live in major U.S. cities on $1 million.”

THESE ARE COOL

Stunning Aerial Footage of F-16s Flying over Arizona Filmed in 8K

Amazing 3-Year-Old

NASA Drops Mind-blowing 1.8 Billion-pixel Mars Landscape Panorama

https://www.cnet.com/news/nasa-curiosity-rover-delivers-insanely-high-res-mars-panorama/

OH MY!

“Administrative costs now make up about 34% of total health care expenditures in the United States – twice the percentage Canada spends, according to a new study published in the Annals of Internal Medicine. These costs have increased over the last two decades, mostly due to the growth of private insurers’ overhead.

MORE THAN WELL DESERVED

“Meet Barron’s 100 Most Influential Women in U.S. Finance Right Now” Barron’s, 3/6/2020

The 100 women on the list were chosen based on their accomplishments and leadership within their organization, influence within their sector, and the capacity to shape their business or the industry in the future.

Christine Benz Director of Personal Finance/Senior Columnist Morningstar

https://www.barrons.com/articles/barrons-100-most-influential-women-in-u-s-finance-51583516036

AND MORE GOOD (AND BAD) NEWS

“Lisa Su of Advanced Micro Devices is the first woman ever to top the Associated Press’ annual survey of CEO compensation: Her 2019 pay package was valued at $58.5 million following a strong performance for the company’s stock during her five years as CEO.

The median pay for women on the list was $13.9 million, versus $12.3 million for men. Pay for women was up 2.3% from last year, looking at the median; the median change for men was 5.4%. And, women remained significantly underrepresented as CEOs, heading just 5% percent of S&P 500 companies.

‘Women are making incremental progress achieving leadership positions in the C-suite,’ said Lorraine Hariton, President & CEO of Catalyst, a nonprofit organization focused on women in the workplace. ‘However, the fact remains that women CEOs still represent a disproportionately small share of corporate leadership and women of color aren’t represented at all.’”

https://apnews.com/e9e5fb359e462d50543f79cd9b2ebc48

FEAR SELLS, BUT EXCITEMENT BUYS

Great headline

https://www.investmentnews.com/behavioral-finance-market-downturn-189970

WHO KNEW?

From my friend Howard

The space between your eyebrows is called the glabella

The way it smells after the rain is called petrichor

The rumbling of stomach is actually called a wamble

The cry of a newborn baby is called a vagitus

The day after tomorrow is called overmorrow

The wire cage that holds the cork and a bottle of champagne is called an agraffe

When you combine an exclamation mark with a question mark (like this ?!), it is referred to as an interrobang

The space between your nostrils is called columella nasi

Illegible handwriting is called griffonage

The dot over an ”i” or a “j” is called a tittle

BE A SKEPTIC. DO YOUR HOMEWORK.

I received a marketing piece from Yacktman Funds touting their long-term performance.

“Given the unprecedented times that we find ourselves in and the fact that Yacktman has been one of the few active managers to outperform the S&P 500 for close to three decades...”

Not sure where they got their data from, but after checking with Morningstar, I found a quite different picture (SPXTR is the S&P 500 Total Return Index). Problem is, the long term (i.e., 20 years) looks great, but after the first 5 years the outperformance disappears and the 1, 3, 5, & 10 year is pretty underwhelming.

NICE GIG

“Why New York Is In Trouble – 290,304 Public Employees with $100,000+ Paychecks Cost Taxpayers $38 Billion” Forbes, 5/26/2020

ALWAYS CURIOUS TO SEE HOW TECHNICIAL GURU PREDICTIONS DO

On April 12 COMEX Silver closed at $15.76.

As I close out on this NewsLetter, July futures are priced at $17.39.

“BENJAMIN GRAHAM’S TIMELESS ADVICE”

I recently read this article in Kiplinger’s by a Mr. Glassman (according to the short Kiplinger bio, Mr. Glassman’s firm is a public affairs consulting firm). I have mixed feelings about his column. An avowed “fanatic when it comes to dollar-cost-averaging,” he mixes some good and not so good advice about dollar- cost-averaging (DCA). As it is such a popular and attractive strategy, I though it worthwhile to discuss the pros and cons.

Pros – If you have funds that you will be investing over time; e.g., savings from your paycheck, it may well be a useful strategy. However, there is a catch. “Over time” needs to be a long time – 3 to 5 years (i.e., an economic cycle) so that you have a reasonable chance of buying shares while they are cheap as well as expensive. The example in the column is misleading at best and dangerous at worse. Over a four-month period, it’s far more likely that the investment cost will go up rather than the extreme volatility in the example.

Nonsense, Not Magic

Cons – If the dollar-cost-averaging funds are coming from current saved assets, as decades of research confirm, the opportunity cost of keeping non-invested funds in a liquid account (e.g., money market) historically overwhelms the DCA advantage.

The Exception – If you believe you’re likely to bail out of your investment if it suffers a significant loss in the short term, stretching your investment out over a number of months may be a better alternative if you recognize it’s also likely to result in your paying a premium for your investment. That’s not DCA, but a potentially costly behavioral framing strategy to protect you from making a bad short-term mistake.

In academic speak, over a decade ago, Mr. Simon Hayley, a lecturer in finance at Cass Business School, concluded:

“Identifying this hidden bias means that we can now regard the continued popularity of DCA as resulting from a specific and demonstrable cognitive error. This explanation uses the observable fact that proponents of DCA almost invariably use a flawed argument to suggest that DCA generates higher profits...

Previous research has shown that if investors have non-variance risk preferences, they may prefer to continue using DCA. Behavioral finance effects such as the avoidance of regret can also bring real psychological benefits. However, abandoning a misguided belief that DCA increases expected returns will leave investors better able to assess whether such non-pecuniary benefits and alternative risk preferences justify the use of DCA. The existence of such effects does not alter our conclusion that eliminating the cognitive error should improve investor welfare.”

WORST-PERFORMING ACTIVELY MANAGED FUNDS OF THE PAST 10 YEARS

Well, at least it’s not the “worst-performing from the past 10 minutes.”

While expenses explain many of the laggards, it’s interesting to note that gold funds represented about 40% of the list.

ONE MORE TIME

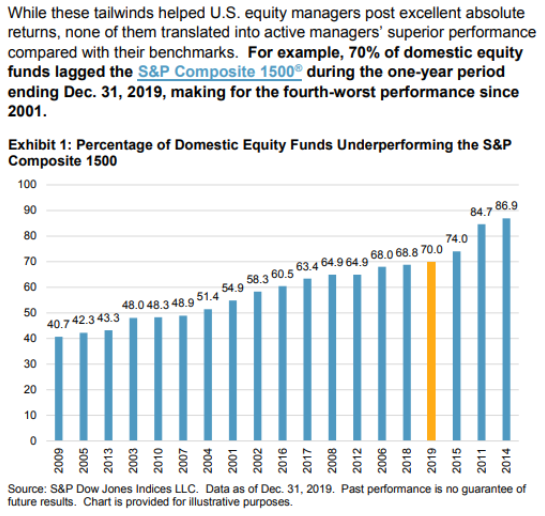

Active management bites the dust. From S&P Dow Jones Indices, 2019 SPIVA U.S. Scorecard:

https://us.spindices.com/documents/spiva/spiva-us-year-end-2019.pdf

INCOME PORTFOLIOS

“What Ultralow Yields Mean for Your Financial and Retirement Plan”

What's the saying, "More money has been lost chasing yield than at the point of a gun"?

FOR FUN

COOL TRIVIA FROM MY FRIEND PETER

Q. The State with the highest percentage of people who walk to work:

A. Alaska

Q. The first novel ever written on a typewriter:

A. Tom Sawyer (although it might have been Life on the Mississippi)

111,111,111 x 111,111,111 = 12,345,678,987, 654,321

Q. Half of all Americans live within 50 miles of what?

A. Their birthplace

Q. If you were to spell out numbers, how far would you have to go until you would find the letter 'A'?

A. One thousand

20 LOWEST-COST FUNDS WITH THE WORST 10-YEAR RETURNS

“The pursuit for rock-bottom fees doesn’t always pay off.

Analysis of mutual funds and ETFs with some of the lowest net expense ratios in the industry show even the cheapest funds can underperform. The 20 worst-performers with expense ratios under 5 basis points — and with at least $500 million in assets under management – notched an average 10-year return of just 2.77%, data from Morningstar Direct show. On the bonds side, the $174.7 billion Vanguard Total Bond Market Index Fund (VBTLX) – the biggest fixed-income fund – had a 0.09 % expense ratio and notched a 10-year gain of 3.81%.”

I’ve frequently referred to some financial media as financial pornography, but now and then a story really gets my goat. This is a classic example of pornographic BS, published in a publication directed at advisers.

For example:

“The pursuit for rock-bottom fees doesn’t always pay off” is a catchy but grossly misleading statement.

Lumping the combined performance of 20 funds invested in completely unrelated markets (from 1-5 year corporate bonds to international value) is utter nonsense.

The return quoted for the Vanguard Total Bond Market Index Fund (VBTLX) of 3.81% does not match the 3.95% return listed in the article’s table.

Finally (only because adding more comparisons to appropriate indexes would be beating a dead horse), the iShares Core US Aggregate Bond ETF (AGG) 10-year performance as of 3/31/2020 was 3.79% versus the Bloomberg Barclays U.S. Aggregate Bond Index (the ETF benchmark) performance of 3.88%.

Bottom line, I hope advisors are not reading and swayed by this nonsense. If they are, their clients’ financial future is likely to be the poorer for it.

CREDIT TO OnWallStreet FOR A THOUGHTFUL RESPONSE

Here is an excerpt from OnWallStreet’s response to my rant:

In our intro, we take pains to provide analysis – not recommendations – regarding these data points and ensure the funds' performances are taken with a grain of salt.

This story should be seen as a platform for discussion on overarching themes, some of which may dispel myths. We are careful not to provide investment advice. These stories are not directed at individual investors and we would never expect our readers to take these as recommendations and act on them such.

All data is provided by Morningstar, including the return data for VBTLX.

As to the discrepancy, you noted: Return data in the story is from the day the story was written. The slides were made a day or two later. Typically, there is no difference, but it seems things had fluctuated so much there was a discrepancy in the intro text. We added a line to address that.

Still, I didn’t think much of the story.

CAVEAT EMPTOR

“Disclosure Obfuscation in Mutual Funds”

An interesting and important paper in Professor Victor Ricciardi’s excellent Behavioral & Experimental Finance eJournal

“Mutual funds hold 31% of the U.S. equity market and comprise 61% of retirement savings, yet retail investors consistently make poor choices when selecting funds. Theory suggests that investors’ difficulty in choosing between funds is partially due to mutual fund managers creating unnecessarily complex disclosures to keep investors uninformed and obfuscate poor performance. An empirical challenge in investigating this ‘disclosure obfuscation’ theory is isolating manipulated complexity from complexity arising from inherent differences across funds. We address this concern by examining disclosure obfuscation among S&P 500 index funds, which have largely the same risks and gross returns but charge widely different fees. Using bespoke measures designed specifically for mutual funds, we find evidence consistent with funds attempting to obfuscate high fees with unnecessarily complex disclosures.”

HOPE SPRINGS ETERNAL

“A survey of 468 financial advisers, conducted by Fidelity Investments during the second week of April, when the S&P 500 Index was down more than 14% from the start of the year, showed 41% of respondents were increasing exposure to active management in client portfolios.”

https://www.investmentnews.com/fidelity-advisers-active-management-covid-19-192625

STICKING TO PRINCIPLES

Thoughts from Dimensional Funds

BAD NEWS - GOOD NEWS

“Retail investors who don’t have financial advisors may be a hard group to convince to employ one, as the majority of them don’t trust the financial services industry – but neither do nearly half of retail investors with an advisor, according to a recent survey...

Only 33% of retail investors without an advisor trust the industry, CFA Institute found. That figure rises to only 57% for retail investors with an advisor, according to the survey ...

There may be some consolation for advisors in the U.S., where 93% of retail investors rank politicians low on trust, according to the survey.”

FUN TEACHER NONSENCE

NEAT PICTURES

From my friend Judy

VALUE INVESTING

For anyone following market returns it’s not a surprise to learn that value oriented investing has been in the doldrums for many years. E&K is well aware, as we’ve long had a value bias to our equity investments. It’s not a bias that we have blindly maintained but one we constantly monitor. Question is, why do we continue to maintain it? While there are many reasons, a recent posting by Morningstar and a research paper by AQR succinctly address our thought process. Below are a few excerpts. Links to the full articles follow.

AQR – Is (systematic) value investing dead?

This is a most thoughtful 57-page research paper with a very clear conclusion.

“We agree that it is always reasonable and rational to continue to ask whether a given characteristic is likely to be associated with future returns. But it is also useful to remind ourselves why we hold that prior belief. Systematic value measures, such as B/P and E/P, are indicators of expected returns for several reasons. First, part of the expectation is attributable to hard to diversify sources of risk which an investor is compensated for holding. Second, part of the return can be attributable to errors in expectations of investors...

Value strategies ‘work’ when the wedge between fundamental value and price converges. For a value investor this primarily comes from prices reverting to fundamentals. Value could also ‘work’ by buying cheap cash flows with prices remaining unchanged (but we will see below that this is not typical). If fundamentals converge to price, or the wedge between price and fundamentals continues to grow, value strategies will ‘not work.’ This can happen when stock prices respond less to fundamental (cash flow) news...

Before concluding, there is one last, but very important, point to make about value strategies. Value strategies, as analyzed in this paper, are typically not utilized on a stand-alone basis. Investors tend to incorporate value measures with other well-known momentum and quality/defensive themes. Given that (i) each of these investment themes work well individually, and (ii) each of the themes are lowly, or negatively correlated (value and momentum are negatively correlated, as are value and profitability), a risk-balanced combination across themes is a powerful diversifier. This diversification benefit of value strategies cannot be overstated. The focus in this paper has been to assess criticism levelled at value strategies on a stand-alone basis. While we have found these criticisms generally lacking in merit, none of those criticisms challenged the powerful diversification potential of combining measures of value with momentum, defensive and other investment themes...

Conclusion

Despite the extensive prior research supporting value strategies (across asset classes, across time periods, and across geographies), the recent underperformance of value in the equity class has led some to question whether systematic value strategies are now broken. We assess many of these criticisms, ranging from (i) increased share repurchase activity, (ii) the changing nature of firm activities, the rise of ‘intangibles’ and the impact of conservative accounting systems, (iii) the changing nature of monetary policy and the potential impact of lower interest rates, and (iv) value measures are too simple to work. Across each criticism we find little empirical evidence to support them. What we do find, consistent with academic research back to at least Ball and Brown (1968), is strong evidence that fundamental (i.e., earnings) information is relevant for stock prices.”

Morningstar: “Value and Momentum Fall Out of Favor, but for How Long?”

A much shorter piece, but the conclusion also reflects our thinking.

“Our examples illustrate that both value and momentum have been out of favor, and it is uncertain when these factors will bounce back. While these factors should outperform over the long term (and have historically), they can go through long stretches of underwhelming results. Further, during times of market duress, correlations often go to 1 and could further impair strategies that rely on a factor-based approach. Nevertheless, investors are likely better off weathering the storm than trying to time the efficacy of factors or different investing styles.”

https://www.morningstar.com/articles/974061/value-and-momentum-fall-out-of-favor-but-for- how-long

https://www.aqr.com/Insights/Perspectives/Is-System themesatic-Value-Investing-Dead

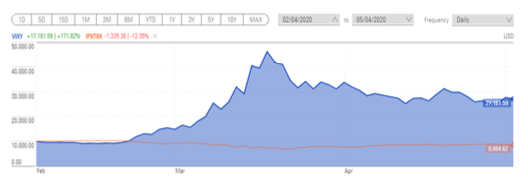

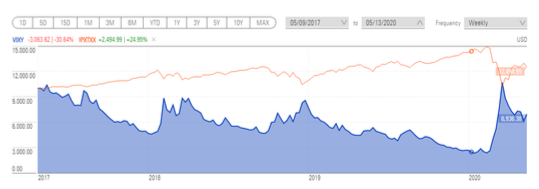

A MARKET TIMER’S DREAM

By now, my readers are familiar with my opinion of market timing and my distain for headlines like the one below. “Three months”! Really?

“ETFs with the Best Three-Month Returns

Funds focused on short-term futures, gold, healthcare and online retail performed well amid the market tumult of the past three months. Based on three-month returns. Data as of 5/4/2020.”

Well, if you can consistently and accurately time the market (not only getting out but also getting back in), number one on the list, ProShares VIX Short-Term Futures ETF (VIXY), would have served you well for the 3 months highlighted in the story.

I must admit it looks pretty good for the prior 3 months compared to the S&P.

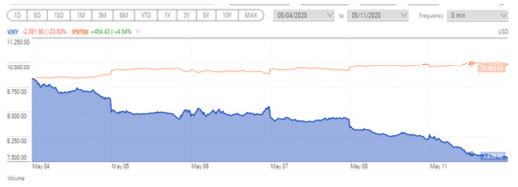

Of course, if your crystal ball was a bit cloudy, you might have been a tad concerned a week later.

How about for the past 3 years? Not too bad if you bailed out on 3/20, but for shame if your crystal ball remained cloudy and you stayed until 5/13, the day before the story was printed.

Of course, no crystal ball would have helped had you been in for the past 5 years. Not pretty.

NOW I KNOW WHAT I AM

I’m a Seenager!

STOP WORRYING

From my friend Freddie

MORE MARKET TIMING WARNING

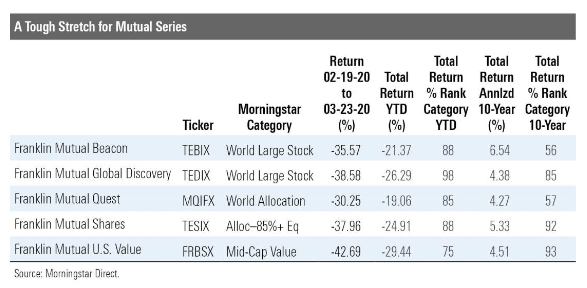

Although mutual funds may boast quality management teams, that doesn’t help beat the market over time. While they looked brilliant in 2008, having built up significant cash positions, they missed much of the subsequent run-up (a classic market timing Achilles heel). Compounded by the recent market fall-off, the long-term results are less than impressive. The moral: stop trying to game the system. To make money in the market you need to stay in the market. Here’s a recent story from Morningstar.

“From Feb. 19 to March 23, 2020, Franklin Mutual Quest lost 30%, while the others lost 36% to 43%. The year-to-date rankings aren't pretty. All are bottom-quartile. Funds that held up nicely in 2008 are hurting today.

Of course, you'd hope their conservative stock selection would have taken some of the sting out of the sell-off even without a cash buffer, but it hasn't. And now the funds' long-term records are less impressive, as a down market didn't help them make up the ground lost in the up market.

You don't see a lot of equity or allocation funds with big cash stakes. You could make the case that Mutual Series shouldn't have reined in its managers, but it's not that simple. As that missed rebound indicates, timing is really difficult. And if your timing is off, then you've just got a big opportunity cost in that cash stake.”

THE FUTURE IS HERE

From my #1 son

GOOGLE:

No sir, it's Google Pizza.

CALLER:

I must have dialed the wrong number. Sorry.

GOOGLE:

No sir, Google bought Gordon’s Pizza last month.

CALLER:

OK. I would like to order a pizza.

GOOGLE:

Do you want your usual, sir?

CALLER:

My usual? You know me?

GOOGLE:

According to our caller ID data sheet, the last 12 times you called you ordered an extra-large pizza with three kinds of cheese, sausage, pepperoni, mushrooms, and meatballs on a thick crust.

CALLER:

OK! That’s what I want...

GOOGLE:

May I suggest that this time you order a pizza with ricotta, arugula, sun-dried tomatoes, and olives on a whole wheat gluten-free thin crust?

CALLER:

What? I detest vegetables!

GOOGLE:

Your cholesterol is not good, sir.

CALLER:

How the hell do you know!

GOOGLE:

Well, we cross-referenced your home phone number with your medical records. We have the result of your blood tests for the past 7 years.

CALLER:

OK, but I do not want your rotten vegetable pizza! I already take medication for my cholesterol.

GOOGLE:

Excuse me sir, but you have not taken your medication regularly. According to our database, you purchased only a box of 30 cholesterol tablets once, at Drug RX Network, 4 months ago.

CALLER:

I bought more from another drugstore.

GOOGLE:

That doesn’t show on your credit card statement.

CALLER:

I paid in cash.

GOOGLE:

But you did not withdraw enough cash, according to your bank statement.

CALLER:

I have other sources of cash.

GOOGLE:

That doesn’t show on your last tax return, unless you bought them using an undeclared income source, which is against the law.

CALLER:

WHAT THE HELL!

GOOGLE:

I'm sorry, sir, we use such information only with the sole intention of helping you.

CALLER:

Enough already! I'm sick to death of Google, Facebook, Twitter, WhatsApp, and all the others.

I'm going to an island without an Internet, or cable TV, where there is no cell phone service and no one to watch me or spy on me.

GOOGLE:

I understand sir, but Alexa says you need to renew your passport first. It expired 6 weeks ago...

GREAT MINDS THINK ALIKE

|

Goldman Sachs says bitcoin is not a viable investment for client portfolios |

|

Goldman Sachs analysts are not buying the idea that bitcoin – or any cryptocurrency – should be seen as a worthwhile investment for the firm's clients... "Cryptocurrencies including bitcoin are not appropriate as an asset class ... |

... pointed to cryptocurrencies' volatile price movements, its unstable correlations with other asset classes and the lack of evidence that it can serve as an inflation hedge as some of the major reasons...

We believe that a security whose appreciation is primarily dependent on whether someone else is willing to pay a higher price for it is not a suitable investment for our clients.

https://finance.yahoo.com/news/goldman-sachs-says-bitcoin-not-173335785.html

WHERE’S THE RICH PEOPLE?

Kiplinger did a story, “Millionaires in America 2020: All 50 States Ranked”

Here are the winners and losers.

CAVEAT EMPTOR

“Can Industry Groups Handle The Truth?”

An opinion piece (and one I agree with wholeheartedly) by my friend Knut Rostad, president of the Institute for the Fiduciary Standard:

Last week industry trade associations and lobbyists, led by the Financial Services Institute (FSI) and American Securities Association, petitioned the SEC for a new rule to authorize the SEC to tell advisers and brokers how to disclose conflicted fees.

Specifically, they sought redress for what they viewed as a grave injustice brought on by the SEC.

The injustice?

They claimed that the SEC exceeded its rule-making authority by requiring that advisor-brokers (a.k.a. “dual registrants”) make a certain explicit disclosure. Specifically, they don’t want a disclosure to clients that says, “a identical lower-cost class share was available.”

The petitioners alleged their complaint was of the utmost gravitas. “This is about the rule of law. In this country there is law that governs the government.”

The petitioners alleged new rulemaking is required to make disclosures more informative.

Witness how the petitioners asserted the SEC’s conduct undermines the rule of law. The petitioners wrote, “It is insufficient, according to the SEC that advisers disclose that they placed their clients in a 12b-1 fee paying share class, and that the receipt of 12b-1 fees created a potential conflict of interest.”

Rather, “The (SEC) Initiative declared that the advisers had more to do. Advisers must state explicitly, in very particular language, that ‘A lower-cost class share was available.’” (Then) “The Commission doubled down on its claim that investment advisers are required to disclose, ‘More than one mutual fund share class is available.’”

This is a head-scratcher. The petitioners are clearly animated by the righteousness of their allegations. Yet their implicit goals are avowedly anti-investor. By eliminating explicit and particular 12b-1 fee disclosures, the petitioners allow for a fiduciary breach and for advisor-brokers to hide important facts.

Advisor-brokers can hide the truth about conflicted recommendations. They can hide the truth that they recommended a more expensive mutual fund share class with a 12b-1 fee over a less expensive one. That they put their own financial interests first. They can hide the truth that they don’t meet a fiduciary standard.

Hope you enjoyed this issue, and I look forward to “seeing” you again.

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

Important Disclosure

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz / Foldes Financial Wealth Management (“EK- FF”), or any non-investment-related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from EK-FF. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. EK-FF is neither a law firm, nor a certified public accounting firm, and no portion of the newsletter content should be construed as legal or accounting advice. A copy of EK-FF’s current written disclosure Brochure discussing our advisory services and fees is available upon request. Please Note: If you are an EK-FF client, please remember to contact EK-FF, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. EK-FF shall continue to rely on the accuracy of information that you have provided.

© Evensky & Katz/ Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All