U.S. Small Caps After a Downturn: Stock Declines in Early 2020 Likely Created Attractive Valuations

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsASSESSING WHERE U.S. SMALL CAPS STAND

To get a handle on the state of U.S. small caps after the pandemic-induced losses in early 2020, we start by looking at the performance of stock prices: How did the U.S. small-cap group perform relative to other market-cap groups during the several years through 2019? How did they perform during the downturn in February and March 2020? And how did they perform for the entire 2020 year-to-date period through April?

Then, we ask, what does history tell us about the potential performance going forward? And what are the overall characteristics in each market-cap group? Finally, we address, how are the Wasatch U.S. small cap strategies positioned today—and why?

Our conclusion is that our successful, long-term approach still makes sense: We invest in high-quality small-cap companies with great management teams that are able to rapidly grow sales and earnings in markets with significant headroom to expand.

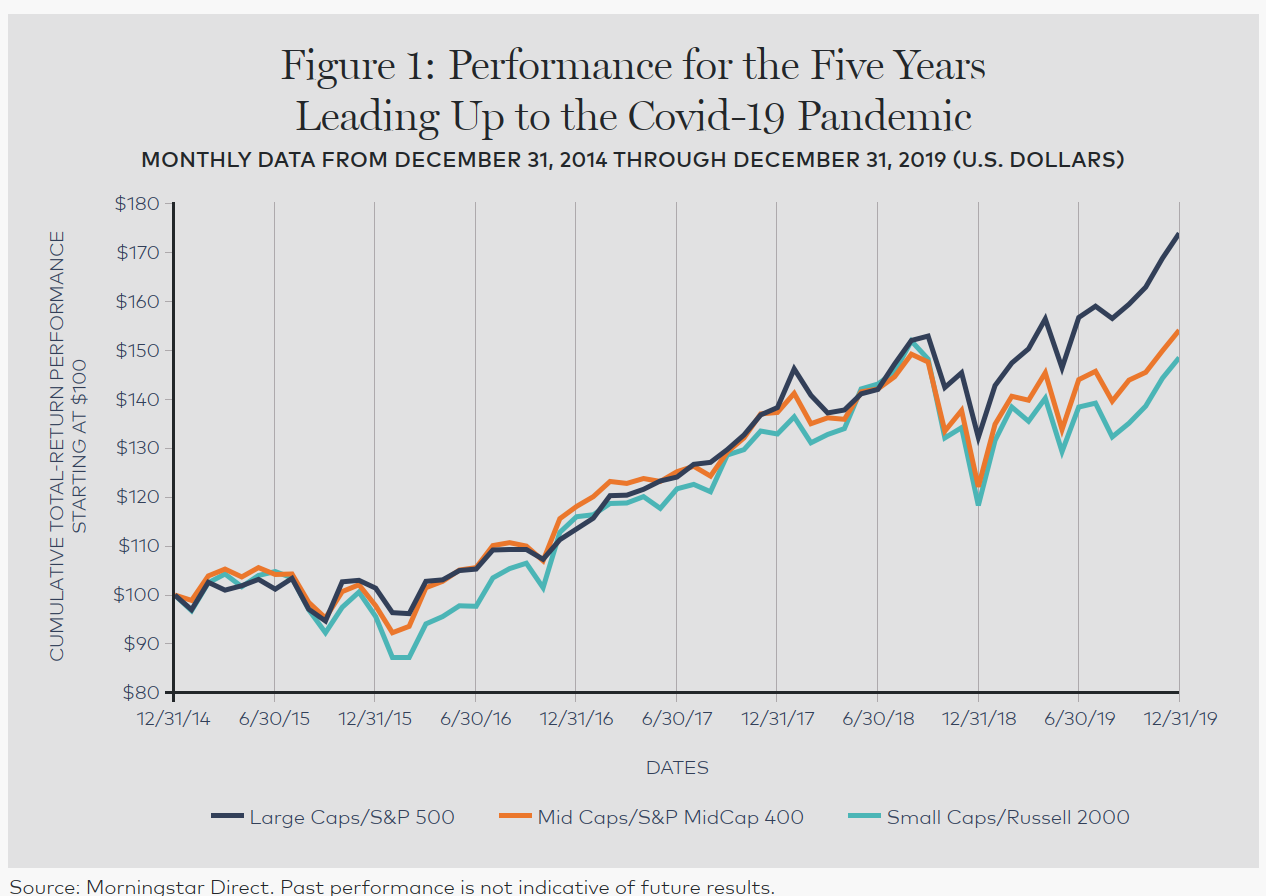

LEADING UP TO THE PANDEMIC

For the five years ended December 31, 2019, the large-cap S&P 500® Index rose a cumulative 73.86%, compared to 54.07% for the S&P MidCap 400® Index and 48.49% for the small-cap Russell 2000® Index. These returns are depicted in Figure 1 below.

What this means is that—despite small caps’ long-term outperformance of mid caps and large caps—small caps were the relative laggards leading up to the pandemic.

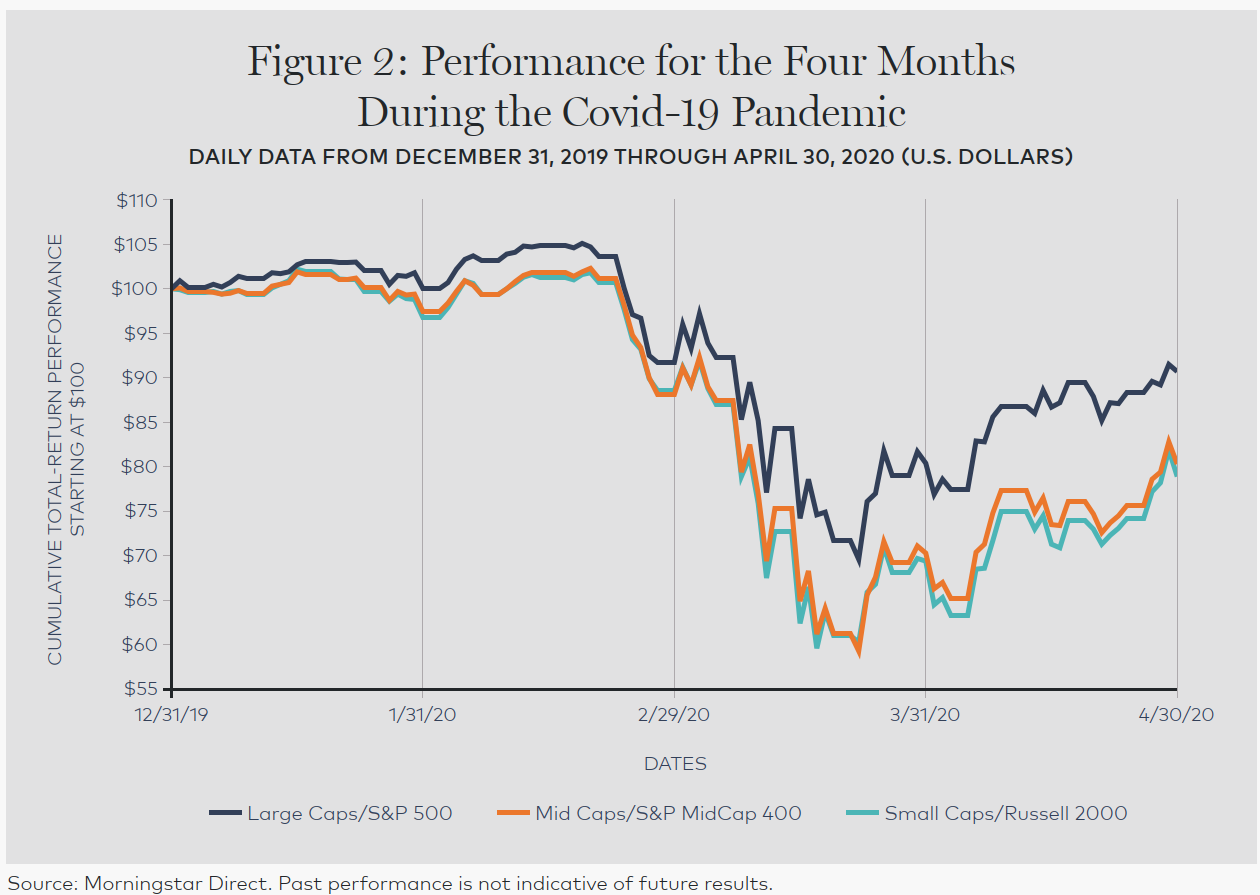

DURING THE PANDEMIC

Now let’s look at 2020, which includes market performance amid the Covid-19 pandemic. As you can see from Figure 2 below, small caps fell in near lockstep with mid caps—but both groups dropped to a significantly greater extent than large caps. Even more disappointing for investors in companies with lower market capitalizations is that through April 30, small caps and mid caps had recouped less than half of their 2020 losses—while large caps had recouped almost 60% of their losses.

As a result, for the year to date through April 30, 2020, the large-cap S&P 500 Index was down only -9.29%, while the S&P MidCap 400 Index was down -19.73% and the small-cap Russell 2000 Index was down -21.08%.

It’s not surprising that small caps and mid caps declined more than large caps through April because stocks in lower market-capitalization ranges are generally perceived as riskier. What is somewhat surprising is that, for the five years presented in Figure 1 and the four months presented in Figure 2, stocks in the lower market-capitalization ranges experienced the worst of both worlds—generally performing less robustly in rising market environments and more poorly in falling market environments.

PUTTING THE TWO PERIODS IN CONTEXT

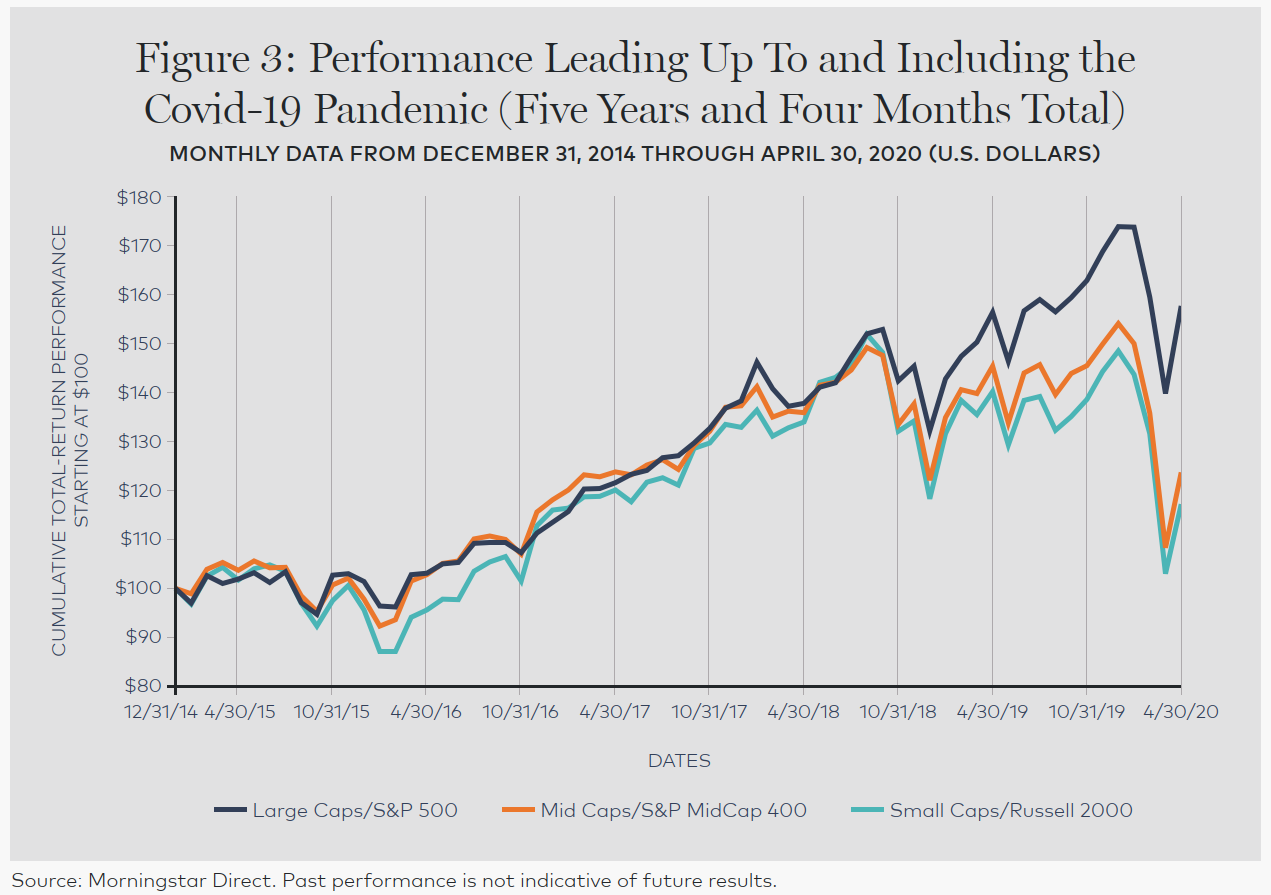

When we combine the two periods—the five years leading up to the pandemic and the four months of 2020 during the pandemic—we see the total effects of stocks in lower market-capitalization ranges experiencing the worst of both worlds. The combination of the two periods is presented in Figure 3 below.

For the entire five years and four months, the large-cap S&P 500 Index—even with the recent volatility—returned a cumulative 57.71%. But the S&P MidCap 400 Index returned just 23.67%. And the small-cap Russell 2000 Index returned only 17.18%. What are the reasons for this underperformance? After all, lower-capitalization stocks typically had better long-term sales and earnings growth historically—and we expect that to be the case going forward. We explore some potential reasons later in this paper.

HISTORICAL SELLOFFS AND REBOUNDS

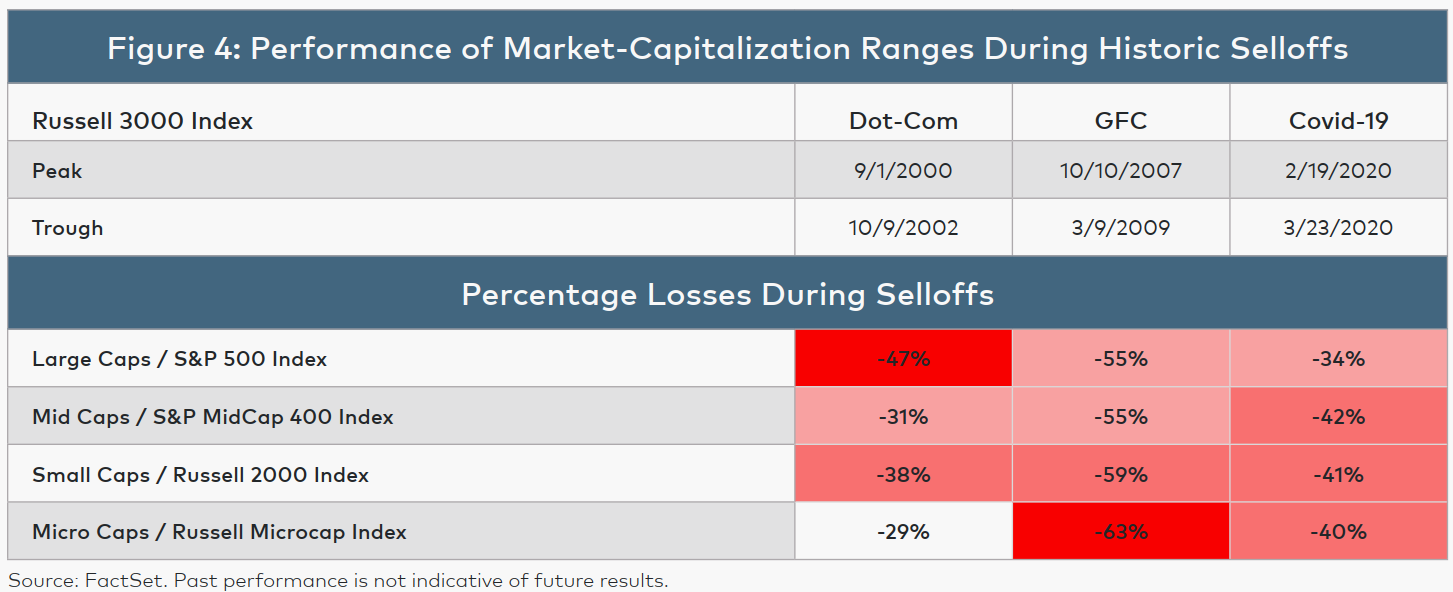

Before we delve into the recent characteristics of the various indexes, which are defined by market-capitalization ranges, let’s look at how these indexes performed during a few historic selloffs and subsequent rebounds in the past two decades. Here, we consider the dot-com crash from September 1, 2000 to October 9, 2002; the global financial crisis (GFC) from October 10, 2007 to March 9, 2009; and the Covid-19 panic from February 19, 2020 to March 23, 2020. The dates for these periods were determined by looking at the peaks and troughs of the Russell 3000® Index, which represents about 98% of the total value of all U.S. incorporated equities. Another important point is that the Covid-19 panic has been very short in duration, and only represents what we’ve seen so far. (See Figure 4 below.)

Also in Figure 4 under “percentage losses during selloffs,” large caps are represented by the S&P 500 Index, mid caps by the S&P MidCap 400 Index, small caps by the Russell 2000 Index and micro caps by the Russell Microcap® Index. What we see is that stocks in the lower market-capitalization ranges were often some of the biggest decliners during selloffs. The major exception was during the dot-com crash, when many large-cap tech names were particularly vulnerable.

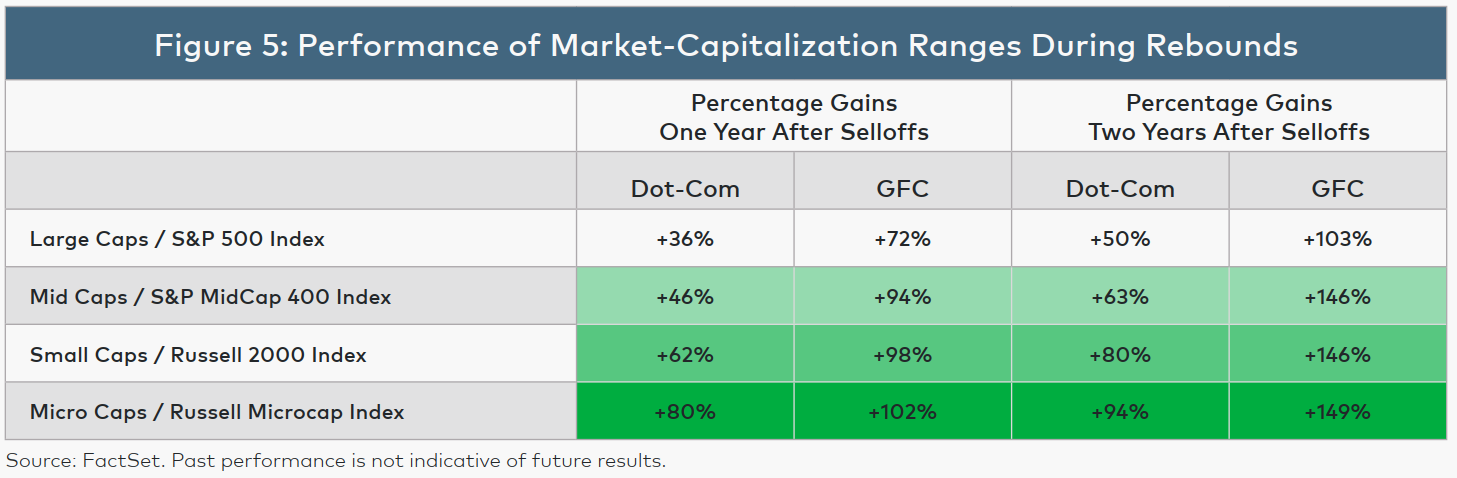

After the selloffs, the rebounds showed even clearer tendencies. Figure 5 below illustrates the one-year and two-year gains subsequent to the end of the preceding losses. As you can see, for both time periods after both the dot-com and GFC selloffs, the rebounds were consistently higher among the lower market-capitalization ranges: Micro caps had the biggest gains, followed by small caps, then by mid caps and ending with large caps showing lesser gains.

Because we’re still in the midst of the Covid-19 pandemic, we don’t know whether or not we’ve seen the market lows or what the subsequent performance will be. But regardless of what the future holds, Figure 4 and Figure 5 provide important context in our view.

WHY HAVE SMALL CAPS LAGGED?

We think the major reasons for small caps’ underperformance during the past several years have less to do with small caps themselves and more to do with large caps, which have benefited lately from phenomenal success in technology and communications. Moreover, this success hasn’t been broad-based—it’s been concentrated in relatively few mega caps.

In this regard, the Wall Street Journal recently noted that Microsoft, for example, “is closing in on the value of the whole of London’s FTSE 100, an index that includes global giants such as Royal Dutch Shell, HSBC and Unilever.” Moreover, “the value of the five biggest U.S. companies—Microsoft, Apple, Amazon, Alphabet [Google’s parent company] and Facebook—is now more than five entire S&P 500 sectors.”

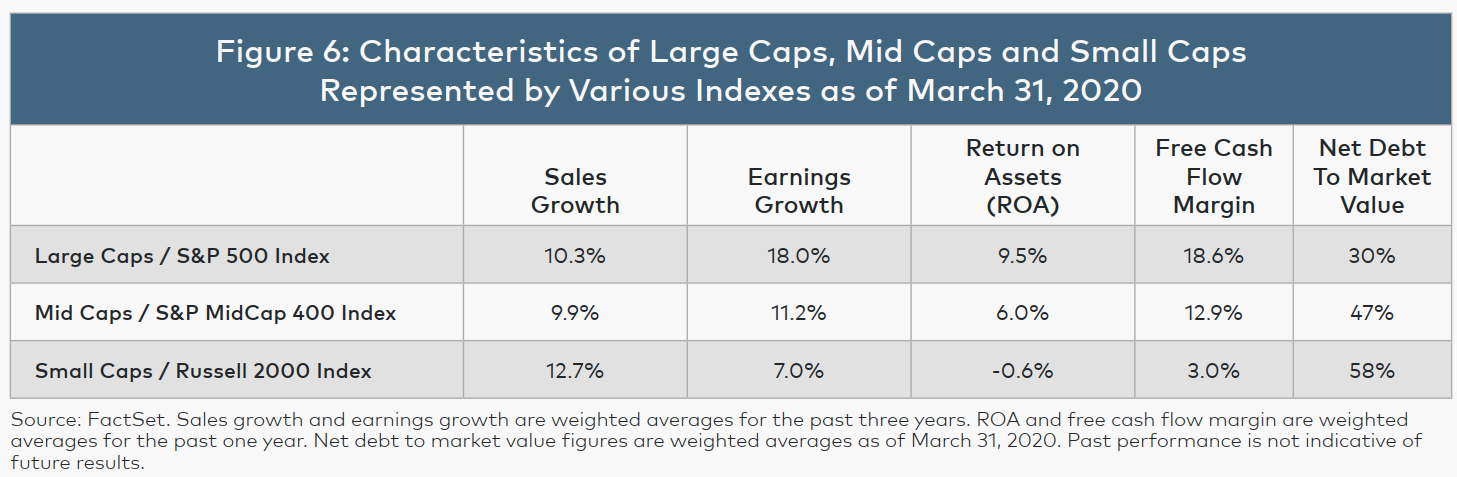

As you can see from Figure 6 below, small caps—relative to mid caps and large caps—led the way in terms of sales growth as of March 31, 2020. But small caps weren’t as strong in terms of earnings growth, return on assets (ROA), free cash flow margin and net debt to market value.

From our perspective, there are two main reasons (in addition to the recent mega-cap success explained above). First, because they’re earlier in their business development, small caps as a group often look less robust based on the metrics in Figure 6—with the exception of sales growth.

Second, some small caps have recently taken on incrementally higher debt levels (see “net debt to market value” in Figure 6) in order to increase sales. Although that’s not necessarily a bad strategy amid record low interest rates, other metrics—earnings growth rates, ROAs and free cash flow margins—have suffered in certain cases.

Similar to the propensity to take on debt, it’s relatively common for small caps to lose money (have negative earnings) while they grow sales. For example, in 2019 according to FactSet, approximately 31% of the companies in the Russell 2000 Index and 37% of the companies in the Russell 2000 Growth Index lost money.

WASATCH IS DIFFERENT

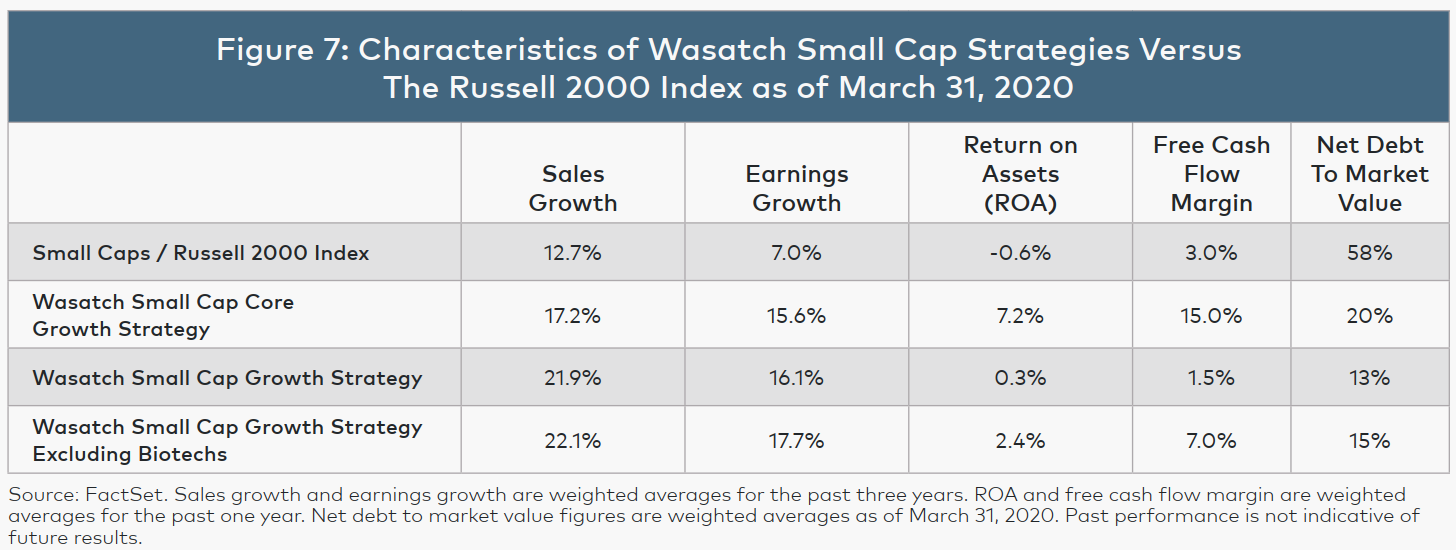

In contrast to the Russell 2000 and Russell 2000 Growth indexes, for 2019, only about 7% of the companies in the Wasatch Small Cap Core Growth strategy and 24% of the companies in the Wasatch Small Cap Growth strategy lost money. And most of the money losers in the Small Cap Growth strategy were medical-device or biotech businesses, which for the reasons described below require special consideration in our view. As you can see in Figure 7 below, the Wasatch strategies compare very favorably to small caps overall, as defined by the Russell 2000 Index.

In particular, as portfolio managers of these Wasatch strategies, our focus is on high-quality companies with healthy, low-debt balance sheets. We look for great management teams that are generally able to grow sales and earnings at rates significantly better than the growth rates for companies in the benchmark indexes.

It’s important to note here that small-cap biotech companies typically have low earnings growth rates, ROAs and free cash flow margins because these companies usually find it necessary to plow capital back into research-and-development spending. Since the Small Cap Growth strategy invests more heavily in biotechs than the Small Cap Core Growth strategy, Figure 7 shows the metrics excluding biotechs as applicable.

THE CASE GOING FORWARD

Regardless of whether or not March 23, 2020 remains the permanent trough of the Covid-19 panic, we think we’ve been able to invest in dynamic companies at prices that may look like bargains several years from now. Moreover, we believe small caps in general could benefit from 1) the potential for small caps to return to their historical outperformance versus large caps, and 2) the possibility for stocks in lower market-capitalization ranges to be especially strong beneficiaries during rebounds following large market selloffs.

As for Wasatch, we think our focus on companies with high-quality characteristics could serve us well. Consider ROAs, for example. Small companies typically have much lower ROAs than large companies because small companies’ higher growth rates and costly research spending (e.g., for biotechs as described above) usually require more reinvestment in the business. But within the context of relatively low ROAs for small companies, we try to find management teams that are disciplined in the pursuit of increased ROAs over time.

THE IMPORTANCE OF QUALITY AND ACTIVE MANAGEMENT

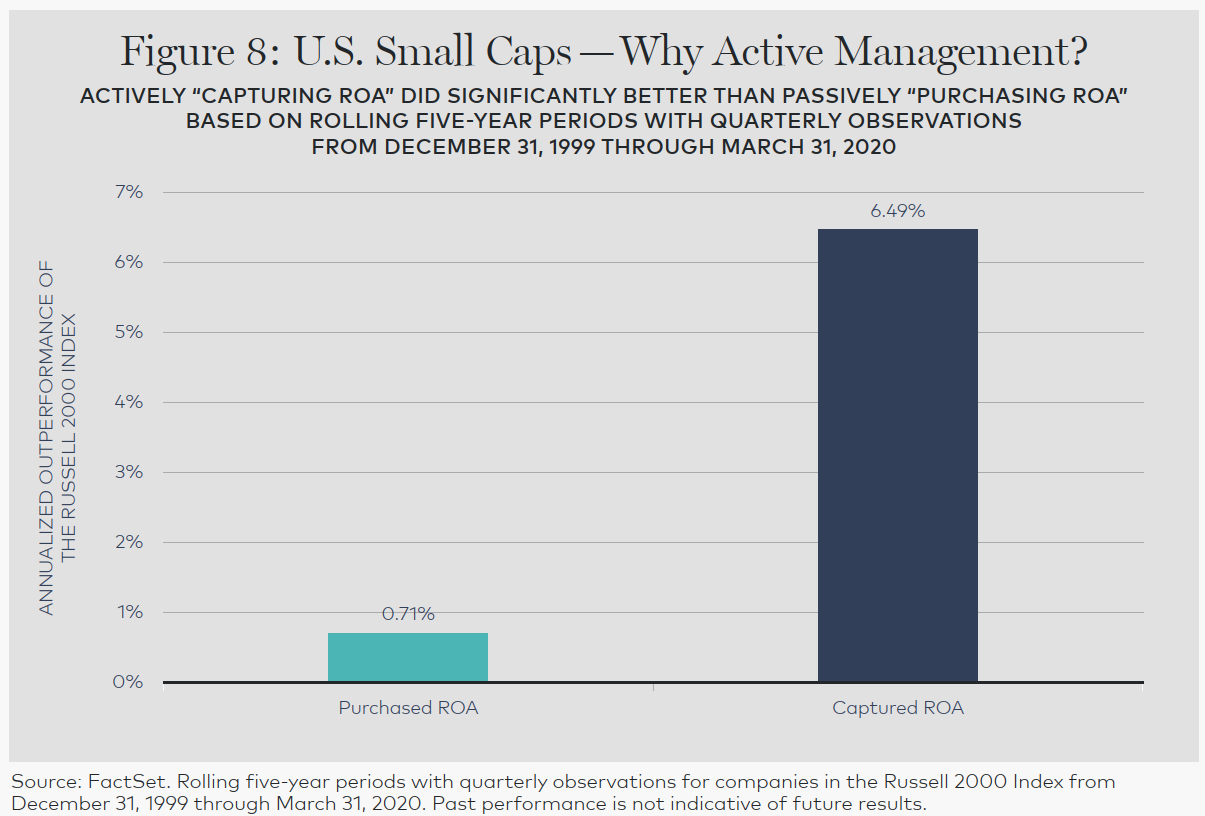

One of the historical benefits of investing in comparatively high-ROA companies is that once a company has achieved a high ROA, that company has tended to maintain its quality. More specifically, based on rolling five-year periods updated quarterly from December 31, 1999 through March 31, 2020, 60.7% of the companies in the Russell 2000 Index that started a five-year period in the top two ROA quintiles ended that five-year period still in the top two quintiles. Additionally, these companies outperformed the Index as a whole by 0.71% per year. As shown in Figure 8 below, we call this “purchased ROA” because the theoretical investment process involved purchasing companies that had already exhibited high ROAs.

While “purchased ROA” is impressive, what’s much more powerful from an investment perspective is for an active manager to buy companies that will be in the top two ROA quintiles at the end of five years. If an investor had been able to do this, outperformance of the Russell 2000 Index over the time period defined above would have been 6.49% per year. We call this “captured ROA” in Figure 8 because the process theoretically involves capturing companies that will have high ROAs in the future.

An important point regarding this ROA analysis is that there are obviously factors other than ROA that contribute to an active manager’s performance. Here, we chose to focus on ROA because it’s a measure of quality that’s important to us at Wasatch Global Investors. We also did a similar analysis focused on sales growth. That analysis showed the theoretical benefits of “capturing sales growth” and the relative ineffectiveness of “purchasing sales growth.” We encourage you to review the performance of the various Wasatch strategies, all of which are actively managed.

WASATCH OUTLOOK AND POSITIONING

As we’ve said, we think the major reasons for small caps’ underperformance during the past several years have less to do with small caps themselves and more to do with some powerful trends among bigger-capitalization companies—especially mega caps like Microsoft and Apple. In fact, based on price/earnings ratios, our analysis shows that today’s profitable small caps are undervalued relative to profitable large caps by one of the widest margins in over 20 years. The reason we confined our analysis to the universe of profitable companies is because that’s where we make most of our investments.

Although mega caps may soon experience the declining growth rates characterized by the “law of large numbers,” we don’t see this as a problem for our small caps—which we think can grow relatively quickly for years on end. Rapidly growing companies with enormous headroom have always been the main reasons for our success at Wasatch Global Investors. Moreover, during the past several years, we’ve been pleased that our growth-oriented investment strategies have generally outpaced their benchmarks in both rising and falling market environments.

While the Covid-19 pandemic has been incredibly difficult for everyone around the world, we remain optimistic regarding the prospects for our companies. In fact, we believe sales and earnings for many of our names could be higher in 2021 than in 2019.

To be sure, the economy has entered a recession even though the current situation hasn’t yet been labeled as such. But once there is more definitive news regarding vaccines and treatments for Covid-19 and there are increasingly positive developments in society’s ability to deal with periodic outbreaks, we believe we’ll see a remarkable pickup in economic activity. Having said that, we’re by no means predicting a V-shaped recovery. We think the recovery for broad sections of the economy will take much longer to play out.

Because small companies are typically more sensitive to the level of economic activity and they frequently get hurt to a greater extent during a downturn, they could be outsized beneficiaries as the recovery strengthens. In fact, during almost all of the one-year periods following recessions in the post-World War II era, small-cap stocks surpassed large-cap names by wide margins.

For our part—especially in the upcoming environment—we favor profitable, industry-leading companies that are mostly able to self-fund their growth without much debt and, if possible, without high fixed costs. We believe these companies may be situated to withstand periodic Covid-related challenges and emerge from the pandemic even stronger with increased market share.

More specifically, we’ve always favored information-technology and health-care companies—and we think certain companies in these sectors are particularly well-positioned for growth during and after the pandemic. We also like industrials and consumer-discretionary names, many of which should benefit from an extended period of low interest rates and from increased spending on infrastructure and housing.

Finally, we generally like small companies that are focused on domestic economies. We believe these companies should have fewer challenges if global supply chains and world-wide demand are disrupted by Covid-19 for an extended period.

RISKS AND DISCLOSURES

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets and political and social instability, which are described in more detail in the prospectus.

An investor should consider investment objectives, risks, charges, and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit wasatchglobal.com or call 800.551.1700. Please read the prospectus carefully before investing.

Information in this document regarding market or economic trends or the factors influencing historical or future performance reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

References to individual companies should not be construed as recommendations to buy or sell shares in those companies.

The Wasatch Small Cap Core Growth strategy and the Wasatch Small Cap Growth strategy do not hold any of the large-cap companies mentioned in this document.

ALPS Distributors, Inc. is not affiliated with Wasatch Global Investors.

CFA® is a trademark owned by the CFA Institute.

DEFINITIONS

Earnings growth measures the growth in a company’s net income over a specific period, often one year.

Free cash flow measures a company’s financial performance, calculated as operating cash flow minus capital expenditures. It is the cash a company generates after spending the money required to maintain or expand its asset base. The free cash flow margin is an indication of how well a company converts sales to cash.

The FTSE 100 Index (The Financial Times Stock Exchange 100 Share Index) is an average of the share prices of the 100 largest, most actively traded companies on the London Stock Exchange. The Index is co-owned by the London Stock Exchange and The Financial Times.

The global financial crisis, also known as the 2008-2009 financial crisis, is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Net debt to market value is the ratio of net debt to the market capitalization of a company.

The price/earnings (P/E) ratio, also known as the P/E multiple, is the price of a stock divided by its earnings per share.

Return on assets (ROA) measures a company’s profitability by showing how many dollars of earnings a company derives from each dollar of assets it controls.

The Russell 3000 Index seeks to track the entire U.S. stock market. The Russell 1000, Russell Midcap and Russell 2000 indexes are sub-segments of the Russell 3000 Index.

The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index. The Russell 2000 is widely used in the industry to measure the performance of small company stocks.

The Russell 2000 Growth Index measures the performance of Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell Microcap Index is an unmanaged total return index of the smallest 1,000 securities in the small-cap Russell 2000 Index along with the next smallest 1,000 companies, based on a ranking of all U.S. equities by market capitalization.

You cannot invest directly in these or any indexes.

The Wasatch strategies have been developed solely by Wasatch Global Investors. The Wasatch strategies are not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the Russell 3000, Russell 2000, Russell 2000 Growth and Russell Microcap indexes vest in the relevant LSE Group company, which owns these indexes. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license.

These indexes are calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in these indexes or (b) investment in or operation of the Wasatch strategies or the suitability of these indexes for the purpose to which they are being put by Wasatch Global Investors.

Sales growth is the increase in sales over a specified period of time, not necessarily one year.

The S&P 500 Index includes 500 of the United States’ largest stocks from a broad variety of industries. The Index is unmanaged and is a commonly used measure of common stock total return performance. You cannot invest directly in this or any index.

The S&P MidCap 400 Index provides investors with a benchmark for mid-sized companies. The index, which is distinct from the large-cap S&P 500, is designed to measure the performance of 400 mid-sized companies, reflecting the distinctive risk and return characteristics of this market segment. You cannot invest directly in this or any index.

Valuation is the process of determining the current worth of an asset or company.

©2020 Wasatch Global Investors

https://www.wasatchglobal.com/

Wasatch Funds are distributed by ALPS Distributors, Inc. Separately managed accounts and related investment advisory services are provided by Wasatch Global Investors, a federally registered investment advisor. ALPS Distributors, Inc., is not affiliated with Wasatch Global Investors.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits