The effects of COVID-19 have been tough on the Energy sector, to say the least. With businesses around the global shuttered and vacations called off—and an estimated 40% of the global population ordered to stay at home—demand has fallen sharply. And that has taken both the price of oil and energy stocks down with it.

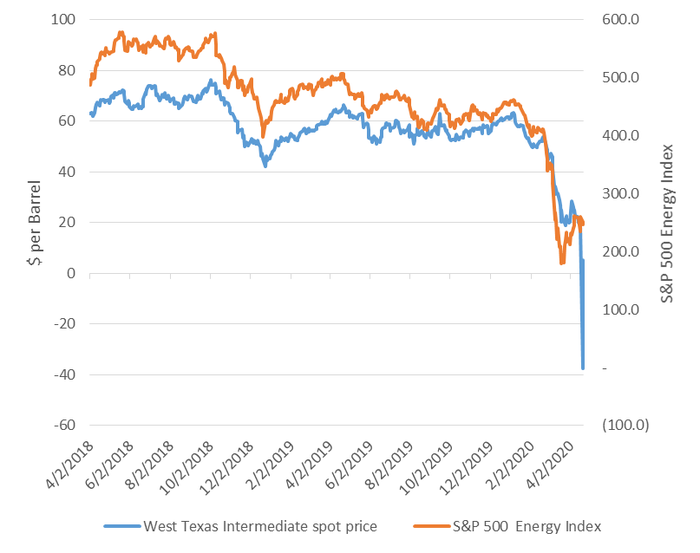

During the first three months of the year, the price of WTI crude oil fell by more than 83%, from $61.06 per barrel on December 31st to $10.01 on April 21st. It briefly dropped below zero on April 20th, falling as low as -$37.63—something that has never been seen in the 155-year historical record.

Oil prices have experienced a record-breaking drop

Source: Bloomberg, as of 04/21/2020

With the viability of hundreds of companies threatened, the sector has seen the highest volatility within the overall market. While energy shares have outperformed since the overall market low on March 23rd, we don’t advise chasing performance. Rather, until there is more clarity around the economic impact from COVID-19, we think taking a more measured approach to sector allocations is appropriate at this time. Therefore, we are maintaining a marketperform rating on the Energy sector.

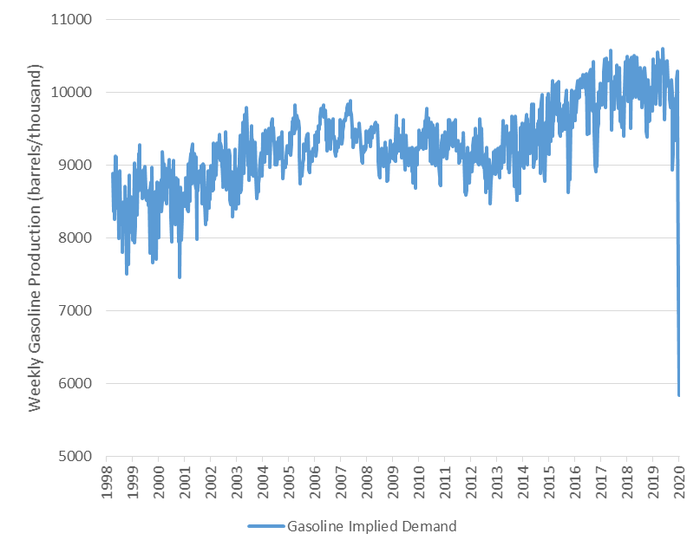

Oil demand is down

Unprecedented business closures and stay-at-home orders around the globe are having a major impact on the demand for oil, which the U.S. Energy Information Administration (EIA) has forecast to fall by more than 23 million barrels per day in Q2—or about -23%. As of April 7th, airlines had cut flights by more than 75% in the U.S., according to Official Aviation Guide (OAG). The number of travelers has declined to about 100,000 per day, down from more than 2 million one year ago, based on Transportation Security Administration (TSA) records. Implied demand for gasoline has plummeted, with refineries cutting back liquid fuel production by more than 40%, according to the April 17th EIA report.

Implied demand for gasoline has fallen

Source: Bloomberg, as of 04/21/2020

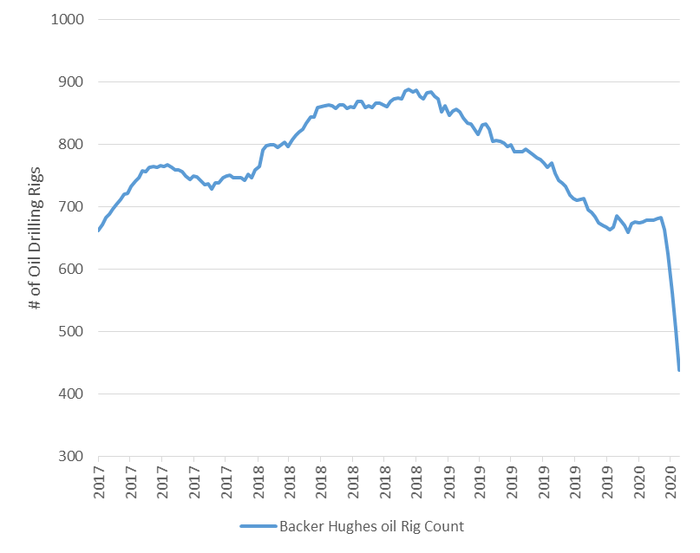

Supply has fluctuated

On the supply side, the tide has turned, but there are still imbalances that are keeping oil prices suppressed. After starting a price war with Russia that resulted in a production increase of more than two million barrels a day, Saudi Arabia made a deal with 23 oil-producing countries to cut production by nearly 10 million barrels per day. Informally, the U.S. will fulfill its part of the deal to cut supply, but in large part because U.S. producers are capping wells anyway.

In the U.S. oil market, major oil companies plan big production cuts, net oil imports continue to fall sharply, and new drilling is coming to a halt, with the Baker Hughes oil drilling rig count dropping to about 438 in April from over 800 a year ago. Despite all this, oil prices are trading at record lows. Even with the supply cuts—which will take some time to implement—it’s estimated that global supply will still outstrip demand by millions of barrels a day in Q2. And it all has to be stored somewhere.

Oil rig count has fallen

Source: Bloomberg, as of 04/21/2020

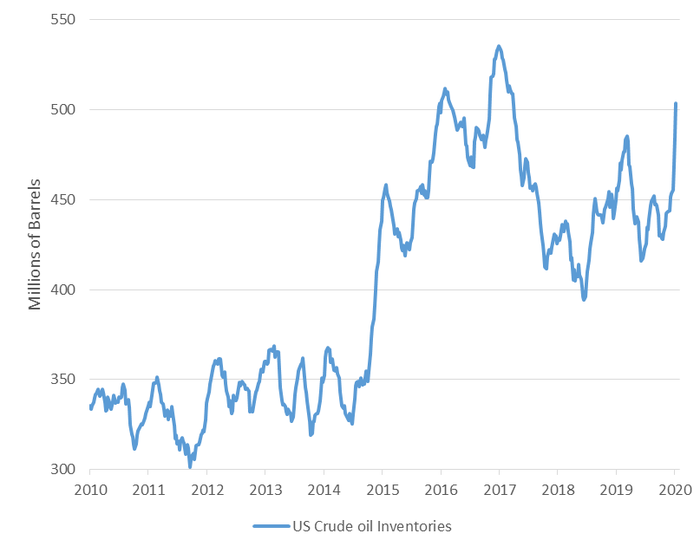

Inventories: Fill ’er up

Although the actual global oil storage capacity is unknown, U.S. oil storage capacity is quickly being filled by the excess supply. It is estimated the total U.S. capacity is 653 million barrels, and 519 million barrels are currently stored. That leaves just 134 million barrels in spare capacity. In the April 17th EIA report, inventories saw a four-week average build of 15.82 million barrels (2.26 million bbl/day). At that pace, U.S. storage tanks will be full in about two months.

U.S. crude oil inventories have risen

Source: Bloomberg, as of 04/21/2020

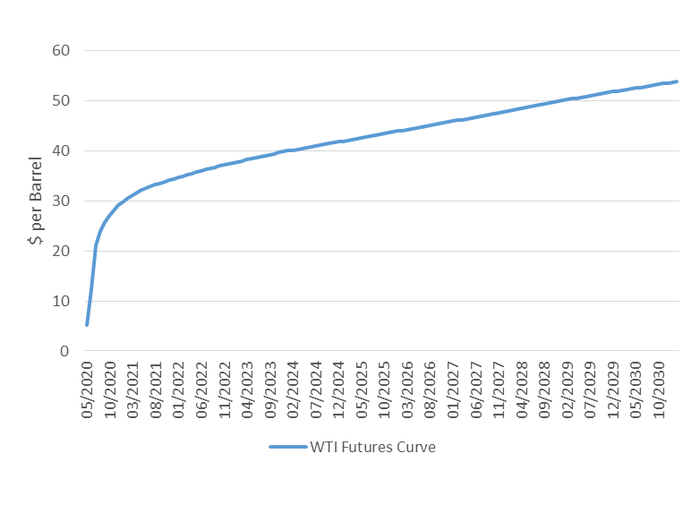

The oil futures curve can help illustrate this imbalance. When the futures price (that is, the price of oil for delivery in one or two years, for example) is higher than the current (or spot) oil price, the futures curve is said to be in “contango.” That is the normal state, as higher future prices reflect the carrying cost (storage and financing costs) of holding the oil for future delivery, but it can also signal that the price is expected to rise over time.

The futures curve has historically been a reliable forecaster of increasing inventories. If there is too much supply (particularly when there is no place to store it), the current price of oil will be driven lower than oil priced for future delivery. Normally, producers adjust over time by decreasing production, which means there will be lower supplies in the future, and the market will price oil at a level that will meet expected demand. Typically, that is somewhere in the range of the price per barrel to cover operating costs (currently about $30 per barrel)1 and the average cost per barrel of drilling new wells (currently $49 per barrel).2

Oil futures prices are higher for future delivery

Source: Bloomberg, as of 04/21/2020

However, U.S. oil producers can’t cap their oil wells quickly enough to reduce supply to match lower demand. Oil storage facilities around the country are nearing full capacity, so on a regional basis more producers are having to pay to get rid of their oil, if they can get rid of it at all.

Slippery slope for energy company fundamentals

A recent Dallas Federal Reserve Bank survey found that the average WTI price necessary to cover operating expenses in the region was $30 per barrel,3 which suggests producers are no longer covering expenses and will cap their wells. But this takes time, and in the meantime companies are burning through their cash reserves. In a recent Kansas City Federal Reserve Bank survey, nearly 40% of the oil companies said that they would be insolvent within a year if oil prices were to stay at $30 per barrel.4 That certainly sounds alarming from an investor’s perspective—and it should, particularly for shareholders of smaller exploration & production and oil services companies that are being the hardest hit.

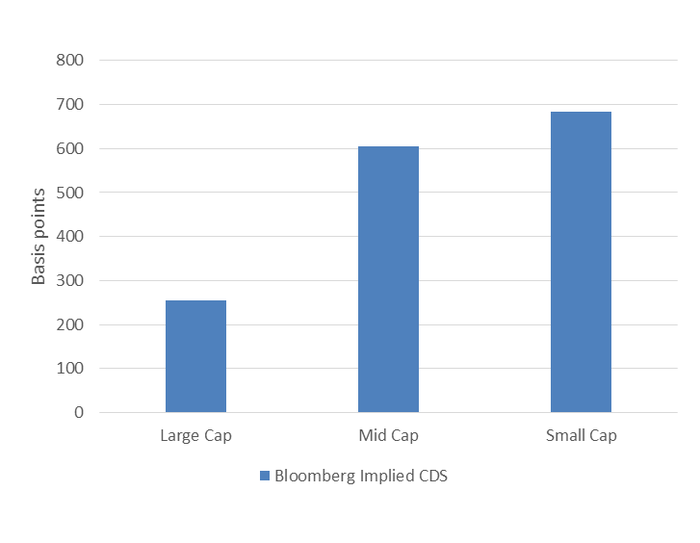

However, larger companies represented in the broader stock indexes, like the S&P 500® index, are in much better shape in relative terms. While they also are seeing negative cash flow in the short term, they have much better staying power, with plans to sharply cut spending and current assets (excluding inventories) sufficient on average to cover short-term liabilities. Even though debt levels have risen in recent years, low rates and longer maturities make their debt more serviceable. The implied risk of default for large-cap S&P 500 energy companies is about one-third that of S&P small cap energy companies.

Smaller-cap energy companies have higher credit risk

Source: SCFR, Bloomberg, as of 04/21/2020 Credit default swaps (CDS) are the most common type of OTC credit derivatives and are often used to transfer credit exposure on fixed income products in order to hedge risk. The figures illustrated here are implied by a Bloomberg proprietary model.

To be sure, earnings expectations are being cut and even many large-cap companies will see sharp quarterly losses, particularly with potential charge-offs on the value of their inventories. However, the ability to cut cost and access to credit lines are helping most of the biggest companies represented in the S&P 500 Energy sector maintain investment-grade long-term credit ratings. The situation is highly fluid. The re-opening of the economies around the world will help reignite demand. In the meantime, there could be a support package offered by the U.S. government, as the energy sector is considered a strategically important sector.

Why we’re keeping a marketperform rating

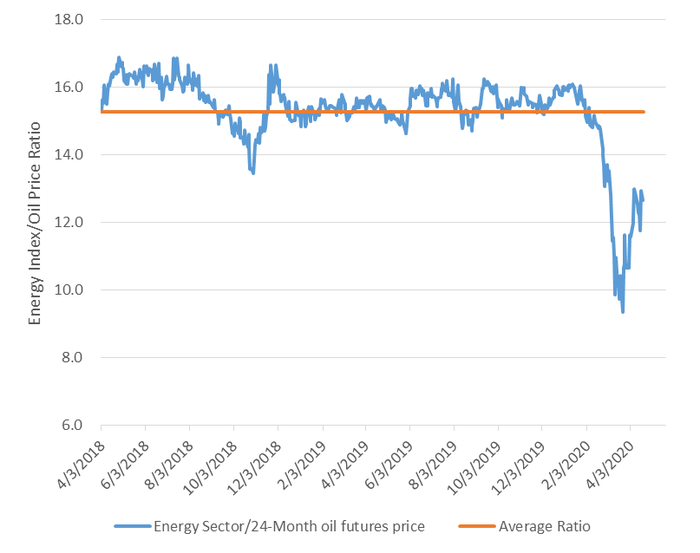

Even with the spot price of oil trading at record lows, oil shares have held up for a couple of reasons: First, investors likely recognize that the larger energy companies in the S&P index are more resilient to the lower oil prices, and that the sell-off in March was excessive; second, energy companies historically have closer relationship with price of future-dated oil—which is trading at a higher price than the current price for oil. As the chart below reflects, energy stocks are trading lower than their historic relationship to the two-year oil futures price. This provides some cushion to the energy sector even if those longer-dated oil prices fall further.

Energy stocks are trading below their average level vs. two-year oil futures prices

Source: SCFR, Bloomberg, as of 04/21/2020. The ratio represents the S&P 500 Energy Total Return Index divided by the price for the 24-month WTI oil futures contract.

In general, the Energy sector’s high sensitivity to the overall market provides a macroeconomic tailwind if the rally from the March lows continues. While we expect high volatility to continue, we think that the S&P 500 Energy sector may have put in at least an intermediate low, particularly as short-term relative strength has been positive.

However, we don’t suggest overweighting the sector at this point. The value characteristics are questionable because of the uncertainty around future earnings revisions, which is weighing on the fundamentals of the sector. Finally, it has already rallied significantly from recent lows, and it is far from clear how long it will take for the oil market to rebalance supply and demand. Therefore, we are maintaining a marketperform rating on the sector for the time being.

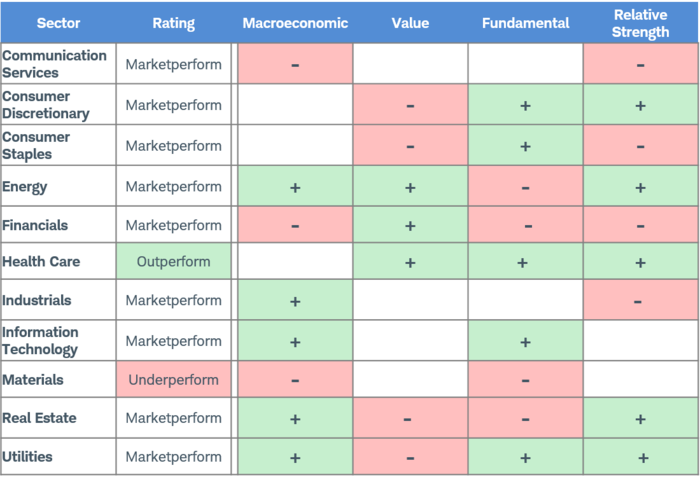

Note: Each of the sector lenses shown above—Macroeconomic, Value, Fundamental and Relative Strength—is both intuitive and evidenced-based in nature. Within each, there are a varying number of factors. The Macroeconomic lens includes sector sensitivities to interest rates, stocks and the value of the U.S. dollar; the outlook for each of these is determined by the Schwab Center for Financial Research (SCFR)’s Asset Allocation Working Group, which uses a mosaic approach of quantitative and qualitative considerations. Value includes six different valuation metrics that provide a holistic perspective on current valuations relative to each of the sectors’ own historical valuations, as well as relative to the other sectors. Fundamental provides insight as to how efficiently the companies within each sector use invested capital to produce earnings; this historically has been informative as to future relative performance of the sectors. Finally, Relative Strength measures momentum of the individual sectors against all of the other sectors. We also consider the data in the context of factors outside the scope of these indicators—for example, geopolitical risk or central bank policy changes.

Source: Charles Schwab, as of 4/21/2020

1 Federal Reserve Bank of Dallas, First Quarter Energy Survey, “Oil Price Collapse Reverberates With Job, Capital Expenditure Cuts,” March 25, 2020.

2 Ibid

3 Ibid

4 Federal Reserve Bank of Kansas City, First Quarter Energy Survey, “Tenth District Energy Activity Decreased as a Steep Pace,” April 7, 2020.

Schwab Sector Views: Our current outlook

|

Sector

|

Schwab Sector View

|

Date of last change to Schwab Sector View

|

Share of the

S&P 500® Index

|

Year-to-date total return as of 04/21/2020

|

|

Communication Services

|

Marketperform

|

01/23/2020

|

10.7%

|

-12.5%

|

|

Consumer Discretionary

|

Marketperform

|

07/17/2014

|

9.8%

|

-9.6%

|

|

Consumer Staples

|

Marketperform

|

05/07/2015

|

7.8%

|

-7.2%

|

|

Energy

|

Marketperform

|

11/20/2014

|

2.6%

|

-45.1%

|

|

Financials

|

Marketperform

|

03/05/2020

|

10.9%

|

-30.3%

|

|

Health Care

|

Outperform

|

01/26/2017

|

15.4%

|

-4.5%

|

|

Industrials

|

Marketperform

|

01/29/2015

|

8.2%

|

-25.9%

|

|

Information Technology

|

Marketperform

|

08/16/2018

|

25.5%

|

-7.8%

|

|

Materials

|

Underperform

|

01/23/2020

|

2.4%

|

-21.6%

|

|

Real Estate

|

Marketperform

|

08/16/2018

|

3.0%

|

-14.7%

|

|

Utilities

|

Marketperform

|

03/05/2020

|

3.6%

|

-10.6%

|

|

S&P 500 Index

|

|

|

|

-14.8%

|

Source: Schwab Center for Financial Research, Bloomberg (for YTD total returns) and S&P Dow Jones Indices (for S&P 500 sector weightings). Sector performance data is based on total return for each S&P 500 sector subindex (see “Important Disclosures” for index definitions). Sector weighting data is as of 3/31/2020; data is rounded to the nearest tenth of a percent, so the aggregate weights for the index may not equal 100%.

Past performance is no guarantee of future results.

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab